Thahbib Rahman

Research Analyst

Despite escalating geopolitical tensions, crypto-asset spot prices have shown a sustained recovery in sentiment, with BTC briefly breaching $74K and ETH flirting with $2,200. Demand for optionality ticked up following President Trump’s weekend announcement that the US had launched airstrikes against Iran, with the latter then retaliating across the Gulf region – which moderately inverted the term structure of volatility, though absolute implied volatility levels remain far lower than their highs in early February. Relative to delivered volatility, implied volatility is also trading lower, and the skew towards OTM puts is no longer as strong as it was.

Despite escalating geopolitical tensions, crypto-asset spot prices have shown a sustained recovery in sentiment, with BTC briefly breaching $74K and ETH flirting with $2,200.

Demand for optionality ticked up following President Trump’s weekend announcement that the US had launched airstrikes against Iran, with the latter then retaliating across the Gulf region – which moderately inverted the term structure of volatility, though absolute implied volatility levels remain far lower than their highs in early February. Relative to delivered volatility, implied volatility is also trading lower, and the skew towards OTM puts is no longer as strong as it was.

Meanwhile, AAVE has shown divergences from ETH’s spot behaviour amid growing governance tensions within the ecosystem, following announcements that major service providers, including BGD Labs and the Aave Chan Initiative (ACI), will not renew their engagements. This comes as “Aave Will Win,” a proposal to route all Aave product revenue to the DAO while funding future development, including Aave V4, narrowly passed its first vote.

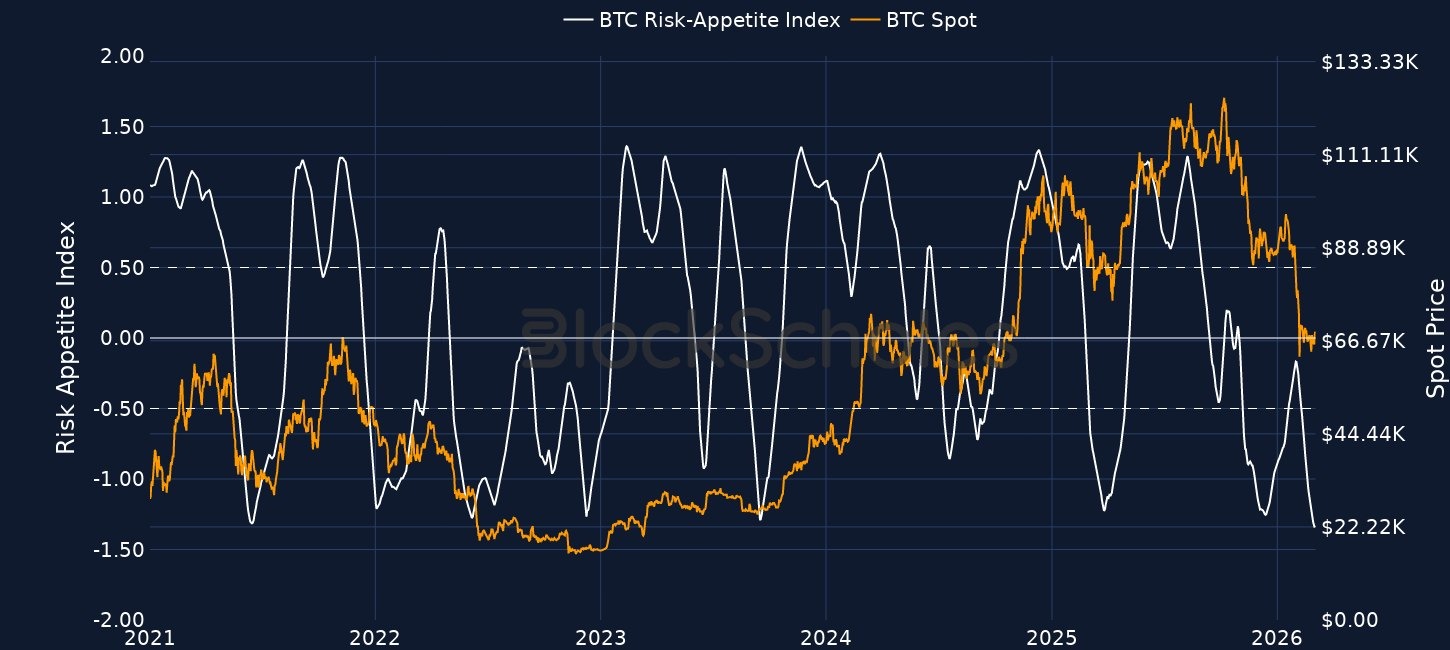

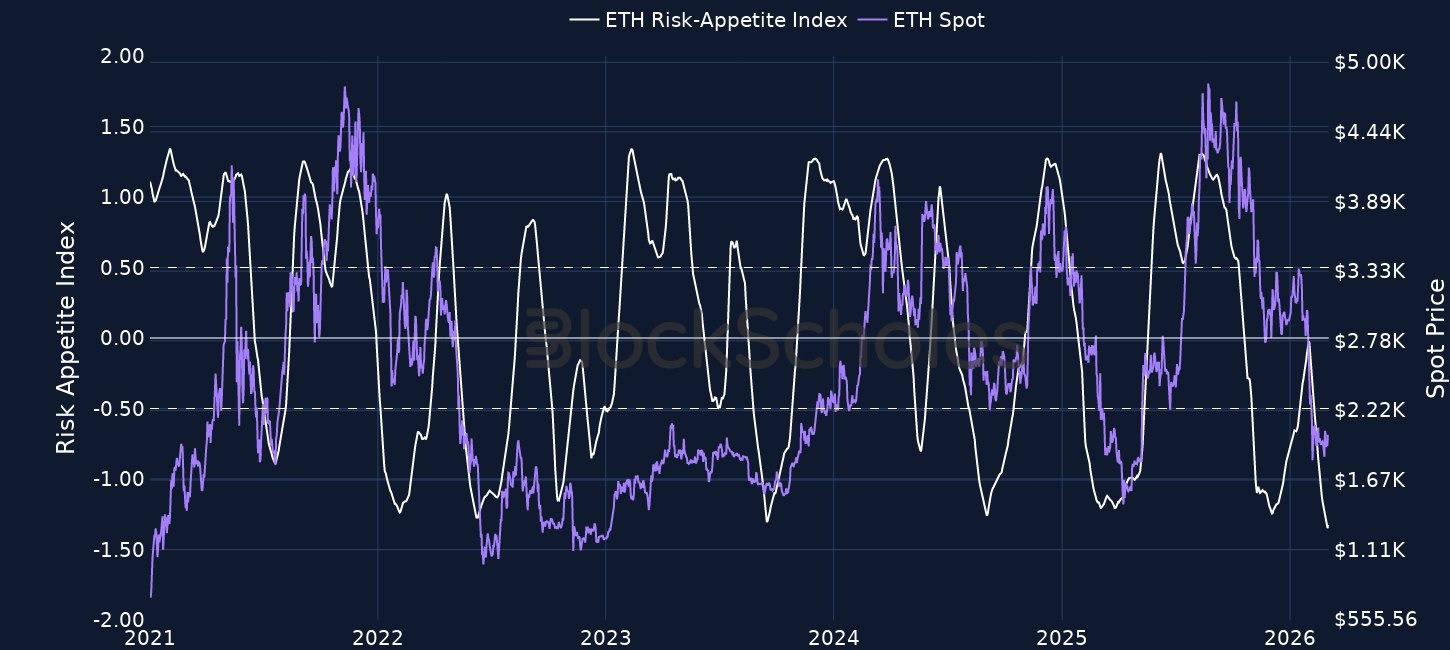

Block Scholes’ Risk Appetite Index measures the level of euphoria (above 1) or panic (below -1) in the spot market. Momentum in this index shows a strong relationship to spot returns.

Over the past week, President Trump’s announcement of joint US-Israeli airstrikes on Iran has been the main narrative gripping crypto (and broader macro asset) prices. Given that the announcement was made on a weekend, crypto markets were the only ones that could react in real-time.

After a brief wick below $63K and $1,800 following the announcement, BTC and ETH spot prices have respectively shown significant resilience, amidst the worsened macro and geopolitical backdrop.

BTC briefly reached $74K before paring back those gains slightly, while ETH reached close to $2,200 before meeting some resistance. Additionally, Spot Bitcoin ETFs have also showed tentative signs of a rebound in sentiment – the first three trading days of March has seen Spot Bitcoin ETFs hoover up $1.145B worth of bitcoins, while Strategy (the largest Bitcoin digital asset treasury firm) bought $204M worth of bitcoins last week, marking the firm’s largest purchase since late January.

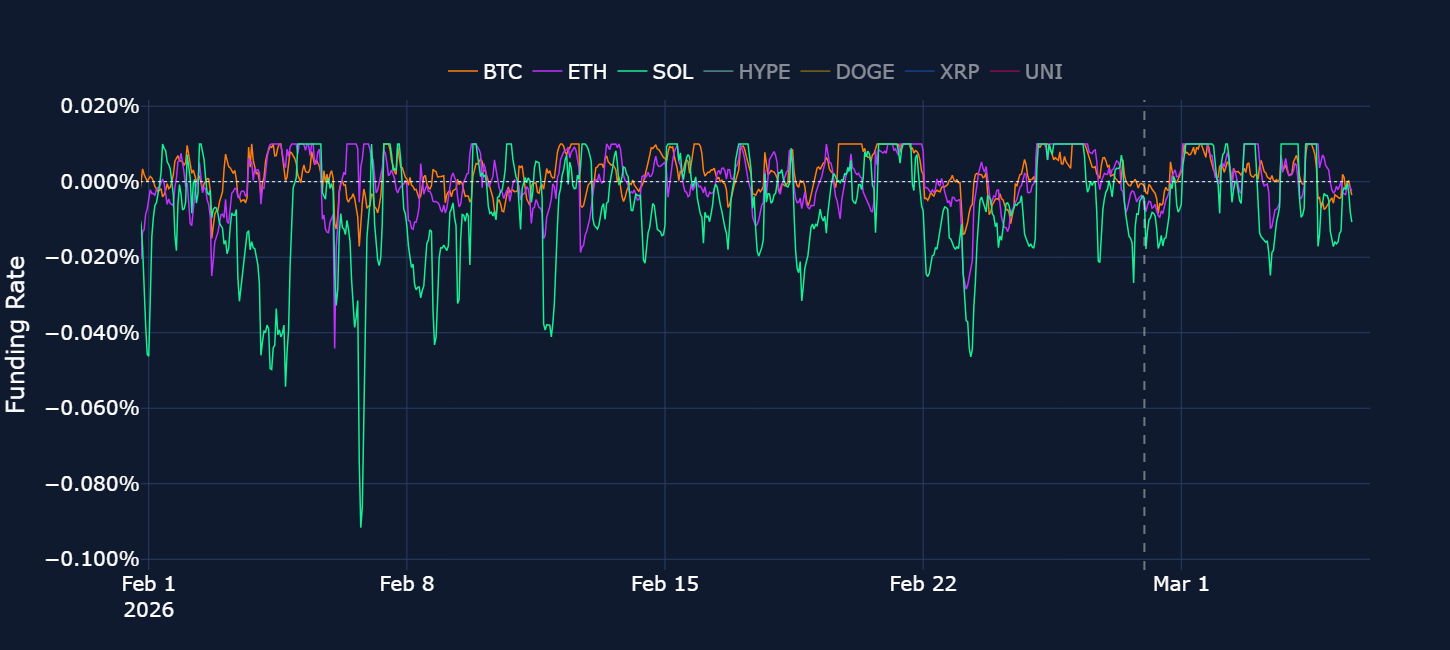

For most of the past week and particularly in the immediate aftermath of Trump’s airstrike announcement, funding rates indicated that the selloff in altcoins may have been driven more by selling in perpetual futures markets rather than spot markets.

BTC, ETH and SOL funding rates all turned negative over the weekend as Iran almost immediately responded to US missiles. For BTC however, funding rates quickly recovered back to neutral levels. ETH funding rates on the other hand took a second leg lower, before reaching neutral levels at a lag to BTC, while funding in SOL has mostly been negative.

Negative funding rates indicate futures prices traded below spot prices, with short traders willing to pay a premium to hold their positions — at the start of the Middle East war, that sentiment was visibly more bearish in altcoins than in BTC.

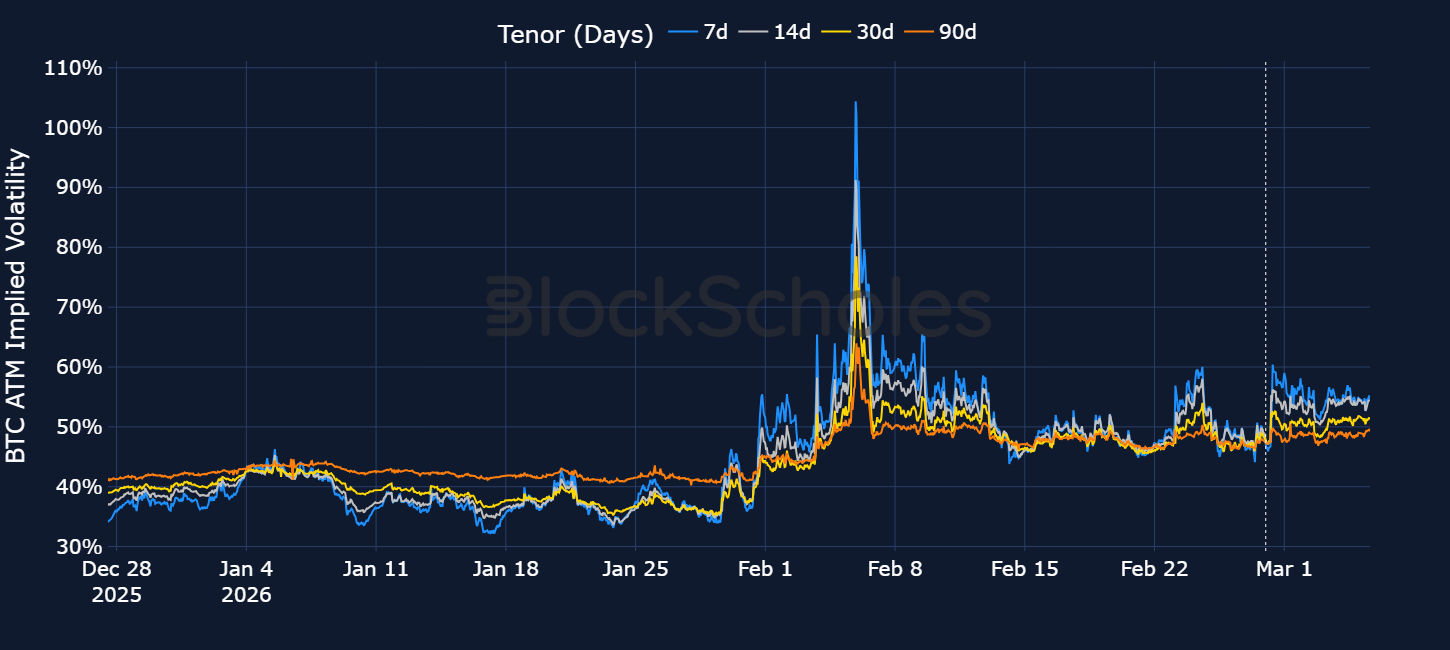

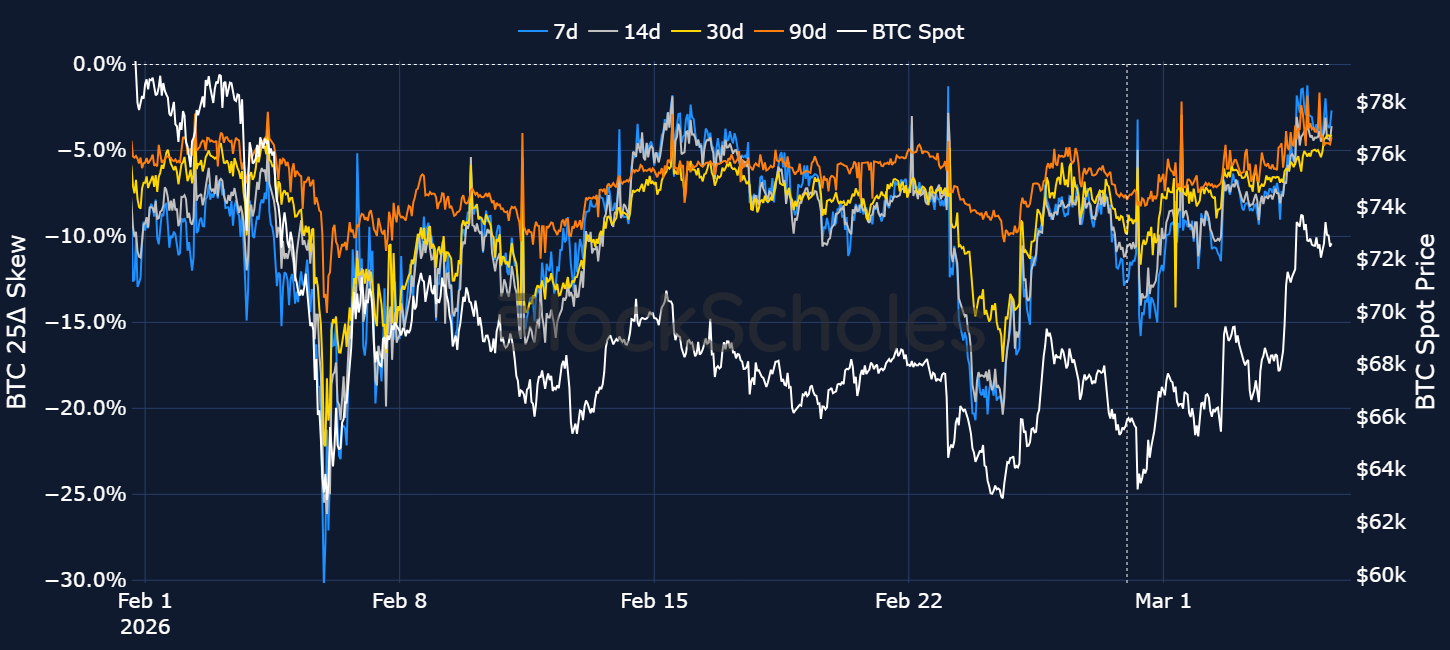

Options markets have shown a similar resilience. Traders bid up optionality immediately after the US airstrikes were confirmed, pushing short-term implied volatility to 60%. That resulted in a modest inversion of the term structure of volatility which has since alleviated slightly. However, despite the nature and severity of the attacks, demand for optionality remains significantly lower than in early February. This time last month, short-tenor implied volatility rose to its highest (100%) since the depths of the 2022 bear market, as BTC fell towards $60K. The ongoing war has so far not seen optionality demand return to those levels.

In fact, back in early February, the volatility implied by options prices far exceeded the volatility that had been delivered in spot prices – a sign that traders were in a deep rush for downside protection. Currently, despite ATM implied volatility following a move higher up in realized volatility, IV remains lower than realized volatility at both short-and mid-dated tenors.

BTC option markets volatility smiles also show some of the bearishness having been priced out. As spot price revisited $63K, put options traded with a 15 vol point premium over calls (traders looking for downside protection). However, similar to the recovery in spot price, 25-delta put-call skew quickly bounced off its lows. Despite that bounce, make no mistake – options markets are still bearishly positioned across the volatility surface. However, they are still less bearish than during the weekend when the US-Israel strikes began.

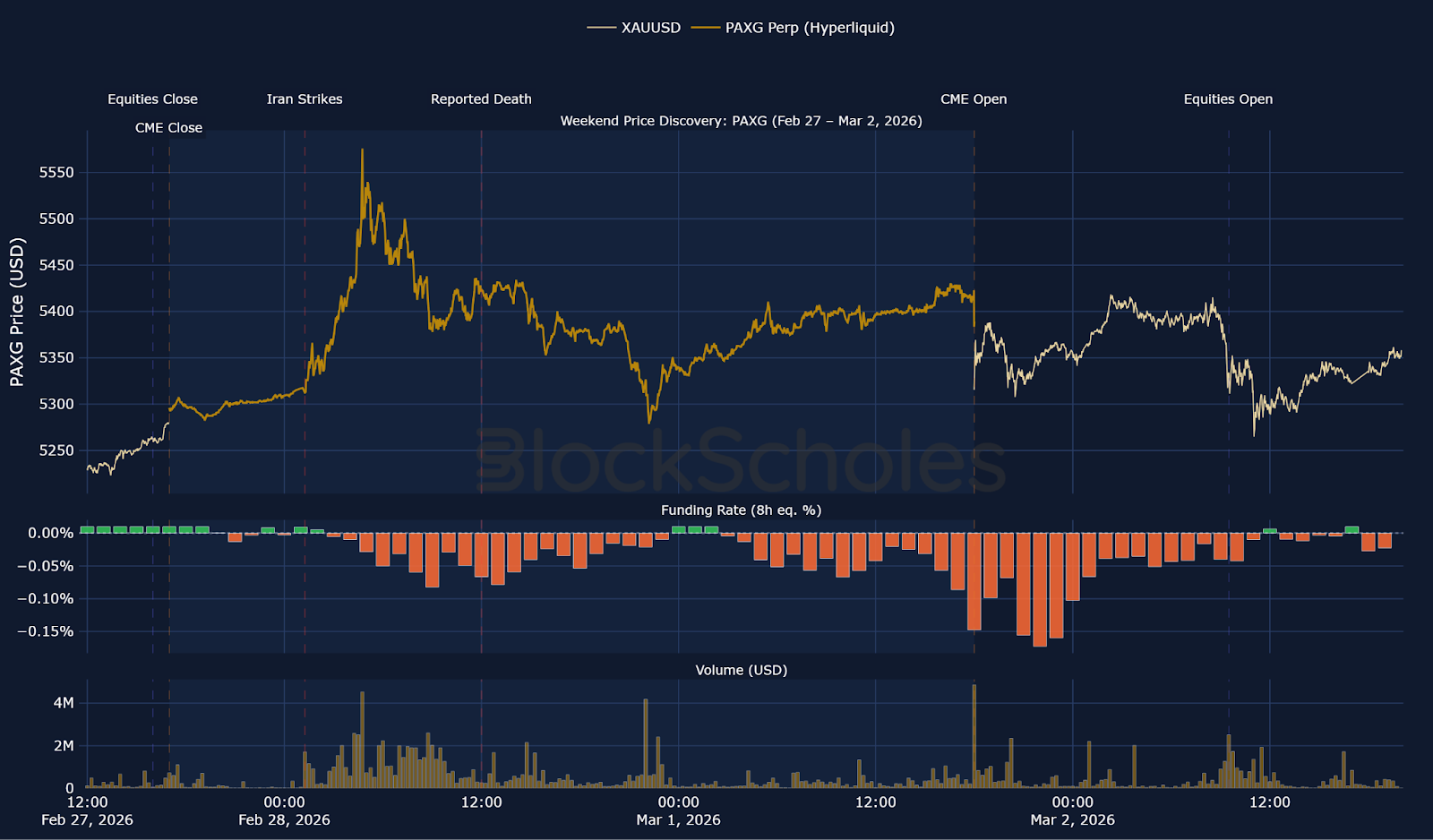

On Feb 27, 2026 at 3:38PM ET, President Trump gave the order to proceed with Operation Epic Fury, with the public in the dark. The strikes on Iran were not reported by Iranian media and published by Al Jazeera until Feb 28 at 1:27AM ET.

However, a spike in volume occurred in onchain perp markets tracking TradFi assets (such as precious metals and equities) at 1:15AM ET (12 minutes before the first official report).

Trump announced to the public at 2:30AM ET that U.S forces had begun operations but, looking at onchain markets, spot prices began to move at 1:15AM, and higher volumes continued through the announcement over an hour later.

Rumours of Khamenei’s death surfaced at around 10:30AM ET with a negligible market reaction. His death was officially confirmed at 12:00PM ET, and the following market reaction was even more muted, suggesting maximum geopolitical uncertainty was being priced in from initial strikes and by midday Saturday the onchain markets had fully absorbed the shock and were trading retracement rather than anticipating further catalysts.

This gives an insight into 24/7 markets and highlights crypto as the most liquid market to navigate geopolitical tension over weekends.

Gold-usdc went into the weekend around the same price as spot gold – trading at $5,277 vs $5,278.93 respectively, with a spread of under $2.

Within a few hours of the Iran strike, volumes substantially increased and the perpetual futures surged to $5,464 while traditional venues were closed.

Funding rates tell a story of conviction, with rates spiking positive immediately after the strikes, indicating longs are willing to pay 0.40% every 8 hours equivalent at the peak to hold positions. This quickly flipped negative as initial panic subsided and participants started to sell.

At Friday’s CME close, PAXG perpetual futures traded at a $17 premium to CME gold ($5,296 vs $5,279) taking a liquidity premium into account.

Price quickly reacted to strikes in Iran before any news release of the incident, peaking at $5,576, $112 above xyz:GOLD's peak of $5,464. This is higher than the peak in xyz:GOLD despite being a more mature market and having significantly more volume and market depth.

At CME open on the following Monday, XAU opened at $5,315 with PAXG perpetual futures at a $68 premium – four times the normal $17 spread.

In contrast to the funding rates for spot gold perps, PAXG perp rates were negative for almost the entire weekend (indicating that shorts were paying longs to pull the perp price to spot).

Unlike the perps tracking Gold and Silver, the PAXG perp tracks tokenised gold with spot trading available onchain over the weekend. The difference in behaviour may indicate hedging or arbitrage activity between perps or spot PAXG tokens, which was not possible in spot gold or silver over the weekend.

DeFi protocol Aave, best known for its lending protocol, is now facing an internal dismantlement, as some of its largest and most influential service providers announce their departure from the ecosystem.

Aave DAO is the decentralized governance body that oversees the protocol, with AAVE token holders voting on upgrades, budgets, and strategic direction. Development of the ecosystem is currently carried out by independent service providers responsible for running and building key components such as Aave v3, governance infrastructure, security systems, and growth initiatives.

However, news that major contributors, including BGD Labs and the Aave Chan Initiative (ACI), will not renew their engagements has sent shockwaves through the community.

In particular, both BGD and ACI pointed directly to Aave Labs’ growing concentration of power. BGD Labs and the Aave Chan Initiative (ACI) have both directly accused Aave Labs of consolidating control within the Aave ecosystem through its significant voting power in the DAO, including participation in votes tied to its own budget proposals, to what has been characterised as governance capture through voting influence.

BGD Labs, the technical service provider that led the development of Aave v3 and contributed to much of the protocol’s core infrastructure since 2022, has announced it will not renew its engagement with the Aave DAO and will cease contributions on April 1, 2026.

Over four years, BGD built and continuously improved Aave v3, while also supporting governance infrastructure, the Umbrella safety mechanism, chain expansions, security processes, and broader operational frameworks. The firm says it is leaving due to what it characterises as a radical shift in the DAO’s organisational balance following Aave Labs’ pivot toward V4, citing concerns over asymmetric influence stemming from Labs’ significant voting power, control of brand and communication channels, an aggressive push to deprioritise V3 through “Promote v4 by implicit/explicit criticism of v3” and through plans to “making v3 parametrisation worse in order for v4 to “shine”. Additionally, they cite limited collaboration around V4 development.

BGD argues this environment creates artificial constraints on improving the live system and no longer aligns with its decentralised operating philosophy. It will complete its current scope, publish off-boarding documentation, transition responsibilities to the DAO or successor providers, and propose an optional two-month security retainer through June 1, 2026, to support continuity through the handover.

Similarly, the Aave Chan Initiative (ACI), founded by Marc Zeller, has announced it will not renew its engagement with the Aave DAO and will wind down over four months despite its contract running through November 2026.

ACI states it is leaving because, after applying what it describes as accountability and transparency standards to Aave Labs’ record budget request, it concluded that governance had become untenable due to Labs-linked addresses voting on their own proposals and holding undisclosed voting power.

The exact AAVE holdings of all 3 entities, ACI, BGD Labs and Aave Labs, are not publicly disclosed. Aave Labs historically retained 23% of the original LEND supply (converted to AAVE at 1:100), yet there is no verified evidence that Aave Labs has recently increased its stake—rather, what has changed is scrutiny around its governance voting influence, not confirmed token accumulation.

Marc Zeller is increasingly vocal on his own account, promoting the narrative that “Labs used their own voting power to fund themselves with DAO money.” In his Feb 25, 2026 post, he argues that Aave Labs was already heavily capitalized through the ICO, VC rounds, and prior DAO payments, yet is requesting substantial additional funding without publishing a full financial accountability report, while also highlighting what he describes as a weak product track record and missed business development opportunities.

Aave Chan Initiative (ACI) argues that there is no meaningful role for an independent service provider in a system where the largest budget recipient can influence outcomes tied to its own funding and strategic direction. As part of the handover, ACI will make its code base open-source and hand over all governance tooling, incentive frameworks, committee seats, and operational responsibilities before formally exiting and winding operations down.

Despite Aave DAO turmoil, AAVE tracks and outperforms ETH, with only a brief single day spot price divergence following BGD’s departure.

These announcements come in tandem with the recent development framework titled “Aave Will Win” which narrowly passed the first stage of voting with 622.3k YAE votes (52.58%), 497.1k NAY votes (42%), and 64.2k ABSTAIN votes (5.42%), representing a total of 302 votes.

The proposal, put forward by Aave Labs, outlines a strategic plan for the protocol’s next phase and structurally changes the funding framework. It proposes a new economic model that would direct 100% of revenue from all Aave-branded products — including aave.com, Aave App, Aave Card, Aave Pro, Aave Kit, Aave Horizon, and related integrations — to the DAO treasury, while establishing a structured funding model to support large-scale growth.

Aave Labs frame the proposal as creating a token-centric model where both protocol-layer revenue (from Aave V3 and V4) and product-layer revenue accrue directly to the DAO, enabling it to fund security, development, expansion, and institutional growth at scale.

Crucially, the proposal also outlines that the DAO would fund Aave Labs through a $25M stablecoin grant, 75,000 AAVE tokens, and additional milestone-based growth incentives tied to product launches.

Aave Lab’s “Aave Will Win” proposal prioritises Aave V4 as the foundational technology for future development, arguing that V3 is mature but architecturally limited, while V4 introduces a modular “Spoke” design that allows new markets, features, and revenue models to be added without modifying the core protocol.

V4 is presented as a strict superset of V3, capable of replicating all prior functionality while unlocking new monetization avenues, including reinvestment modules and expanded institutional use cases. The framework also includes plans for brand governance through a proposed foundation structure and expanded market access for $AAVE via regulated products, positioning the DAO to operate with the scale, capital allocation discipline, and strategic focus of a major financial institution.

The framework positions Aave as already dominant in DeFi lending, with roughly 60% market share, but argues that the larger opportunity lies ahead as institutions, fintechs, and traditional finance move onchain. The goal is to transform Aave from a leading DeFi protocol into core infrastructure for global finance.

The narrow passage of the “Aave Will Win” first vote highlights the fragile sentiment within the Aave ecosystem. Representing roughly 25% of the vote, ACI voted against the proposal, linking its opposition to calls for greater financial transparency from Aave Labs and transparency on their currently undisclosed AAVE holdings, particularly as the “Aave Will Win” proposal seeks further Aave Labs funding. At the same time, the sharpened focus on prioritizing Aave V4 aligns

with BGD’s reasons for departure, reflecting deeper fractures and rising tensions within the ecosystem.

The firm said in its update that its validator network expanded to 33,568 unique wallets, while its STKESOL liquid staking product, launched in January, surpassed 691,039 SOL staked and more than 1,000 holders.

Total assets under delegation reached 3.87M SOL, spanning treasury stake and third-party delegations, with proprietary validators earning roughly 1,276 SOL in February and delivering 99.99% uptime.

Custody of the fund’s digital assets would be handled through Coinbase Custody alongside The Bank of New York Mellon (BNY).

As of Dec. 31, 2025, the company held 53,822 BTC, including 9,377 BTC loaned to counterparties and 5,938 BTC pledged as collateral for $350M in outstanding credit facilities.

The framework would also allow limited exceptions, with holdings of up to 34% permitted in cases defined later by the Financial Services Commission through enforcement decrees.

The measure is expected to be folded into South Korea’s forthcoming Digital Asset Basic Act, which is intended to set a broader regulatory baseline for the sector and has faced timeline slippage from earlier targets.

The company produced 5,686 bitcoin in 2025 versus 4,828 in 2024, with average mining costs excluding depreciation rising to $49,645 per bitcoin from $32,216, primarily due to a 47% increase in global network hash rate.

Riot ended the year with 18,005 bitcoin, plus $309.8M in cash, over $1.9B in total liquidity, and began generating revenue in January 2026 from the first phase of its data center lease with AI chipmaker AMD.

According to the filing, the contracts would trade at prices ranging from $0.01 to $1.00, with the price representing the market-implied probability of a specified outcome occurring.

Michael Saylor’s Strategy Inc. purchased $204M worth of bitcoins last week, while BitMine acquired an additional 50,928 ETH last week (bringing its total holdings to 4,473,587 ETH, or 3.71% of the token's entire circulating supply).

Over the past 10 days, the company repurchased 782,408 common shares at a significant discount to Net Asset Value (NAV), and said it will continue buybacks as long as BRR trades materially below NAV, in an effort to reduce the share count at prices below the company’s underlying asset value, which in turn lifts NAV per share and helps close the discount.

The firm is said to be using its existing technical and research-led team to evaluate opportunities outside crypto, rather than creating a separate AI unit.

Issuance is managed by SBI Shinsei Trust Bank, bringing a trust-bank framework with tighter governance and operational safeguards.

SBI VC Trade is set to be the main distribution partner, while Startale leads the technical build, including plans for interoperability across traditional rails and multiple blockchain networks.

If approved, the system would introduce a 180-day minimum lock-up, weighted voting based on stake, staking rewards for active voters (targeting ~2% APR), and tiered incentives including USD1 benefits and prioritised partnership access for long-term supporters.

The feature integrates third-party DeFi strategies via Morpho, TAC and Re7, with the highest-yield USDT option advertised at up to 18% blended APY through a Re7-powered strategy.

Block Street (BSB) is a cryptocurrency project positioned as liquidity infrastructure for on-chain capital markets, designed to make trading and settlement more efficient when liquidity is scattered across issuers, pools, and blockchains.

The project’s main focus is the long-standing issue of liquidity fragmentation. As more financial instruments and tokenised real-world assets move on-chain, liquidity often gets split across different venues and networks, leading to wider spreads, higher slippage, and inconsistent execution. Block Street presents its solution as a unified layer that aggregates and routes liquidity more effectively, allowing applications and users to tap into deeper combined liquidity rather than interacting with isolated pools individually. In principle, that kind of aggregation can tighten effective spreads and improve execution quality by matching flow across multiple sources instead of forcing every market to operate as a standalone silo.

Block Street specifically frames this challenge in the context of tokenised capital markets products, such as tokenised equities, derivatives, and securities-lending style activity, where fragmented liquidity can become a structural bottleneck to scale. By aiming to unify liquidity across both issuers and chains, the platform’s stated goal is to make these markets function with more “institutional-grade” efficiency while preserving on-chain composability.

Block Street also emphasises composability and multi-chain connectivity. By aiming to provide a simplified integration surface for accessing liquidity across environments, the platform’s ambition is to reduce friction for developers building DeFi and tokenised asset applications, while also supporting smoother execution for market participants interacting with these markets. In the project’s positioning, this is reinforced by an institutional-style API layer intended to make integration straightforward for both developers and professional participants, so they can connect to the liquidity layer without stitching together multiple fragmented endpoints.

A key part of Block Street’s value proposition is stronger capital efficiency. By supporting cross-protocol collateral use, tokenised assets can be deployed more flexibly across DeFi rather than remaining confined within isolated pools or venues. In this context, “best execution” is positioned as a practical outcome: improved pricing driven by smarter routing and access to deeper, aggregated liquidity across markets.

Bybit announced that BSB is listed on the Spot trading platform from 4 March 2026.

Open interest and trading volume data are sourced “as is” from the Bybit exchange platform API exclusively, and as such do not represent a comprehensive picture of the sum of trading activity across all derivatives markets or exchanges. The data visualized in this report consists of hourly and daily snapshots, recorded over the previous 30 days. Daily (hourly) snapshots of trade volume record the total sum of the notional value of trades recorded in the 24H (1 hour) period, beginning with the snapshot timestamp.

If not explicitly labelled as derived from another exchange, the input instrument prices to all derivatives analytics metrics in this report are sourced from the appropriate endpoints of Bybit’s public exchange platform API. In the event that data is labeled or referred to as representing the market on another exchange source, that data is sourced from the appropriate endpoint of each respective exchange’s public API.

Macroeconomic charts and data are sourced “as is” from the Bloomberg Terminal. Exchange data is sourced “as is” from publicly available exchange APIs. Block Scholes makes no claims about the veracity of public third-party data.

After acquisition of underlying-denominated raw data for open interest and trading volume on the Bybit exchange platform from Bybit’s API endpoint, equivalent dollar-denominated figures are calculated using the concurrent value of Block Scholes’s Spot Index for the relevant underlying asset.

Block Scholes’s Spot Index represents the aggregate Spot mid-price for a given currency across the top five CEXs by volume (with USD-quoted markets). It considers the proportion of total volume in the instrument on the exchange, as well as the deviation of a data point from those on other exchanges.

Futures prices are used for Block Scholes’s futures-implied yields calculation services in order to derive the constant-tenor annualized yields displayed in the Futures section of this report.

Options prices are used for Block Scholes’s implied volatility calculation services in order to calibrate volatility surfaces, from which all derivatives volatility analytics displayed in the BTC Options and ETH Options sections of this report are calculated. Volatility smiles are constructed by calibrating to mid-market prices observed in Bybit options markets. As part of the calibration process, prices go through rigorous filtration and cleaning steps, which ensures that the resulting volatility surface is arbitrage-free and has exceptional fit to the market observables.

.jpg)

.jpg)