Thahbib Rahman

Research Analyst

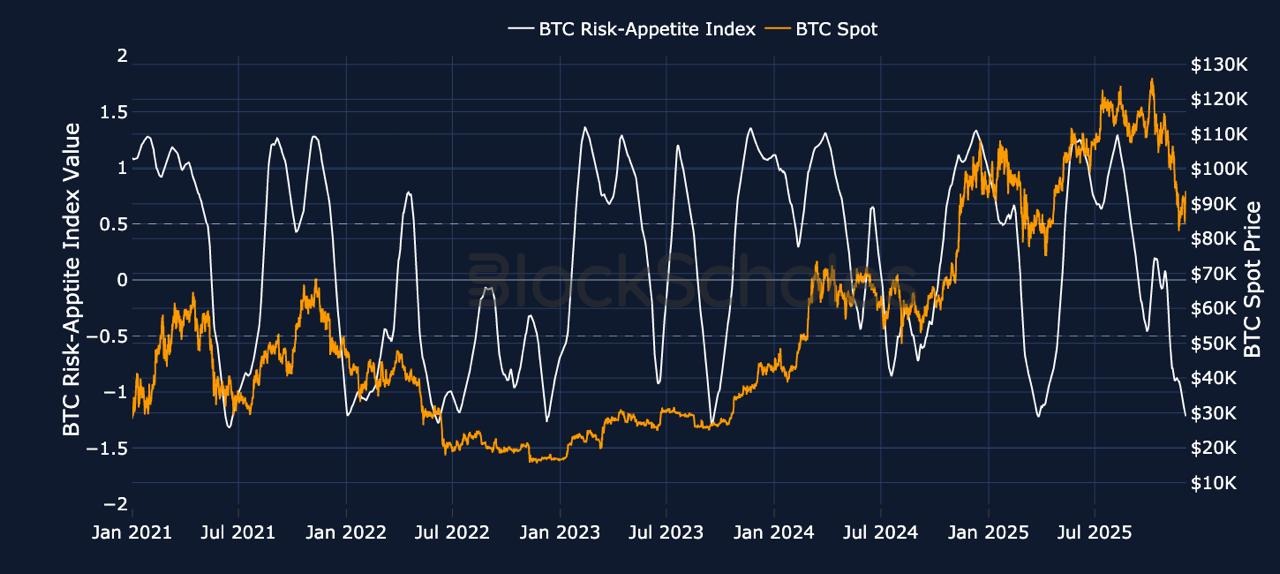

After an early scare at the start of the month, crypto asset spot prices have enjoyed a modest recovery rally that’s seen BTC reach a two-week high above $94K and ETH reclaim the psychological $3,000 mark. To recap, during early Asian trading hours on Dec 1, 2025, BTC led other risk-on assets and sold off sharply amidst hawkish signs from the Bank of Japan and a spike in JGB bond yields, foreshadowing the move in US equities when trading in New York began. However, recent bullish developments (including Vanguard opening its platform up for trading crypto ETFs and mutual funds) have encouraged a sharp recovery rally. As such, sentiment in derivatives markets, particularly in options markets has picked up.

After an early scare at the start of the month, crypto asset spot prices have enjoyed a modest recovery rally that’s seen BTC reach a two-week high above $94K and ETH reclaim the psychological $3,000 mark.

To recap, during early Asian trading hours on Dec 1, 2025, BTC led other risk-on assets and sold off sharply amidst hawkish signs from the Bank of Japan and a spike in JGB bond yields, foreshadowing the move in US equities when trading in New York began. However, recent bullish developments (including Vanguard opening its platform up for trading crypto ETFs and mutual funds) have encouraged a sharp recovery rally. As such, sentiment in derivatives markets, particularly in options markets has picked up.

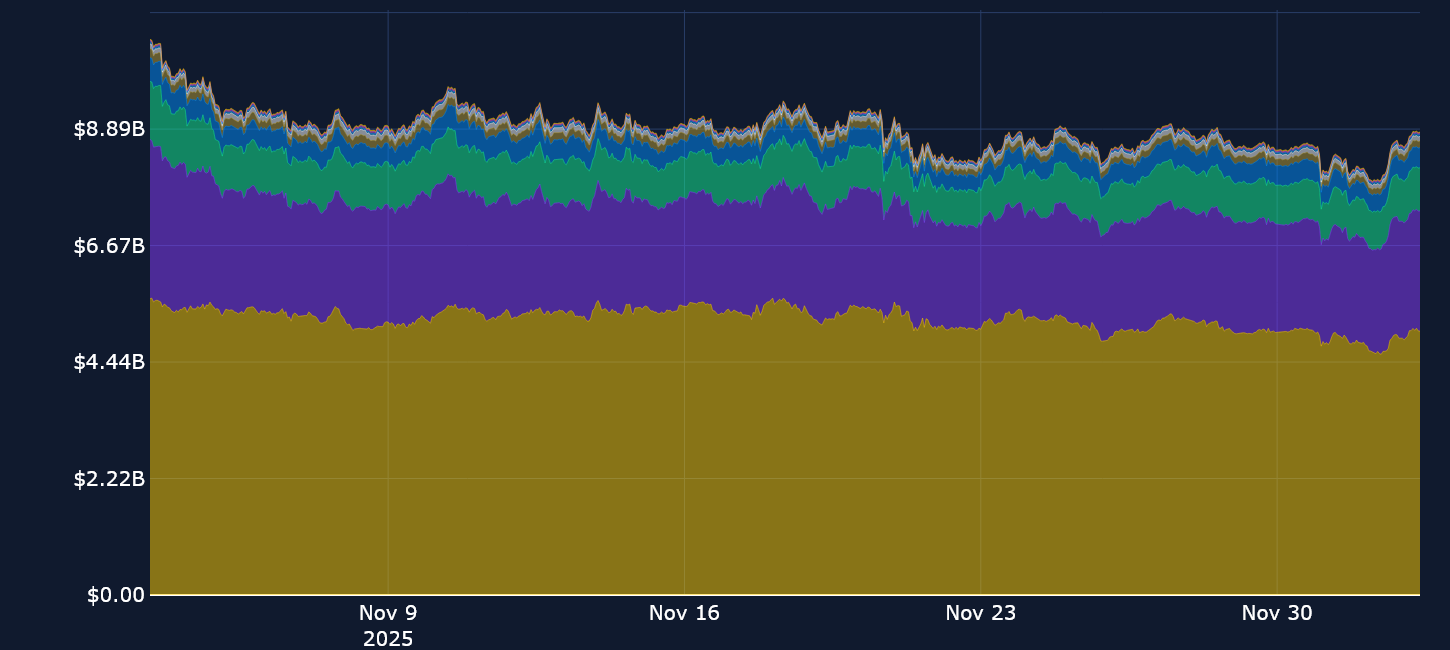

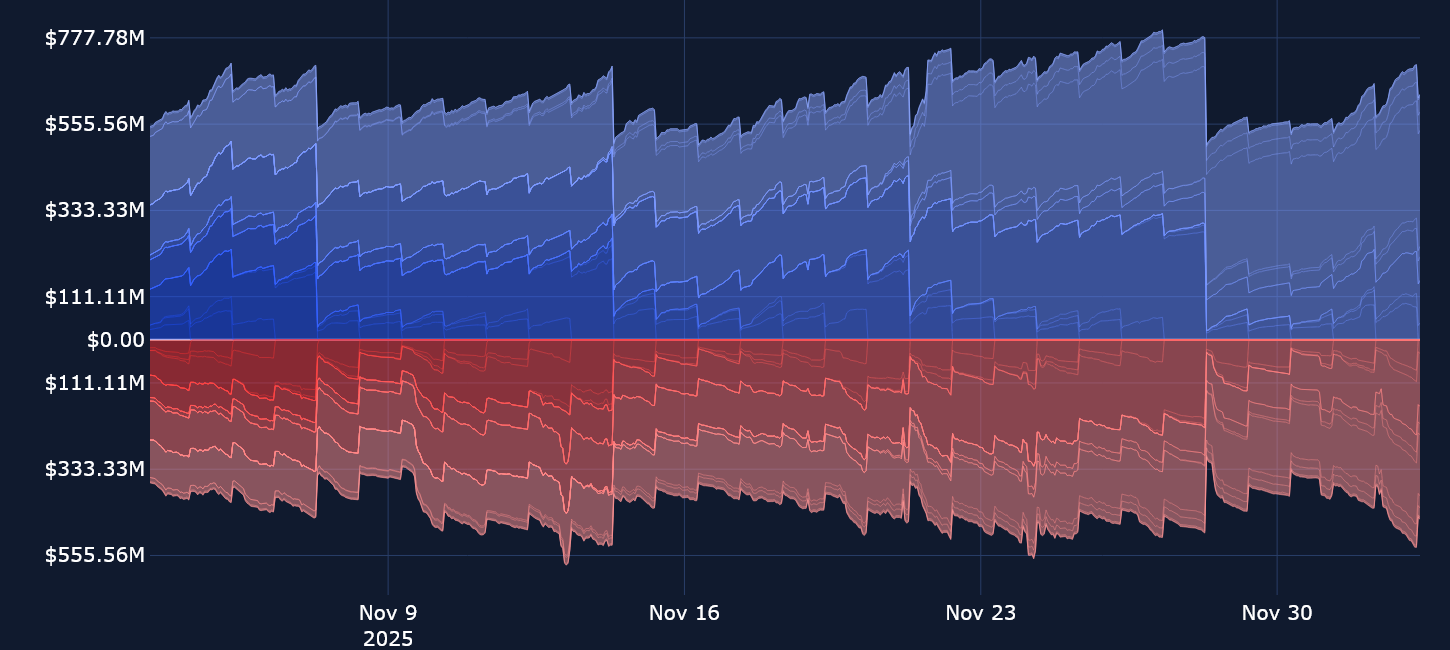

Open interest in perpetual futures positions has increased slightly, though remains far below pre-Oct 10, 2025 levels, and volatility smiles for BTC and ETH have priced out the most extreme part of their bearish premium towards ‘crash protection’. Still, the recovery has not been enough to turn options traders bullish just yet – unsurprising given how far both BTC and ETH trade relative to their all-time high levels.

Block Scholes’ Risk Appetite Index measures the level of euphoria (above 1) or panic (below -1) in the spot market. Momentum in this index shows a strong relationship to spot returns.

Basic Attention Token (BAT) is an Ethereum-based utility token at the heart of Brave’s blockchain-powered digital advertising system, created by Brendan Eich (co-founder of Mozilla and Firefox) to make online ads more secure, fair, and efficient.

Instead of relying on traditional ad networks and opaque tracking, BAT underpins Brave’s rewards system, using locally measured “attention”, which is the time and focus users give to digital content to decide how value is shared: users receive BAT for viewing privacy-respecting ads from major brands such as Amazon, Ford and eBay, while content creators are paid through the Brave Creators programme.

Brave’s open-source, privacy-centred browser blocks invasive trackers and malware by default, with additional privacy features including Brave Shields ad-blocking, tracker blocking, storage partitioning, Global Privacy Control, and bounce tracking prevention, which protects against a type of tracking where a user is redirected through an intermediate site before reaching their final destination. The platform also offers Leo, a privacy-centric AI assistant, and a VPN with around 100,000 subscribers, while the integrated Brave Wallet supports shielded Zcash transactions and wider Web3 activity.

Over time, this has grown into a sizeable ecosystem: Brave now reports more than 100M monthly active users and over 40M daily users, tens of millions of wallets and nearly 2M verified creators, with BAT ranked among the most widely distributed tokens on Ethereum and over 99% of its 1.5B supply already in circulation, with around 437,800 holder addresses and over 3,100 transfers in a single day.

Since October 11th, the token has surged more than 100%, trading around $0.27 with an 8% gain over 24 hours and 24% over the past week, outpacing the broader altcoin recovery following the 10 October liquidation event. This move has helped make social tokens the second-best performing sector over the past month, behind only privacy coins.

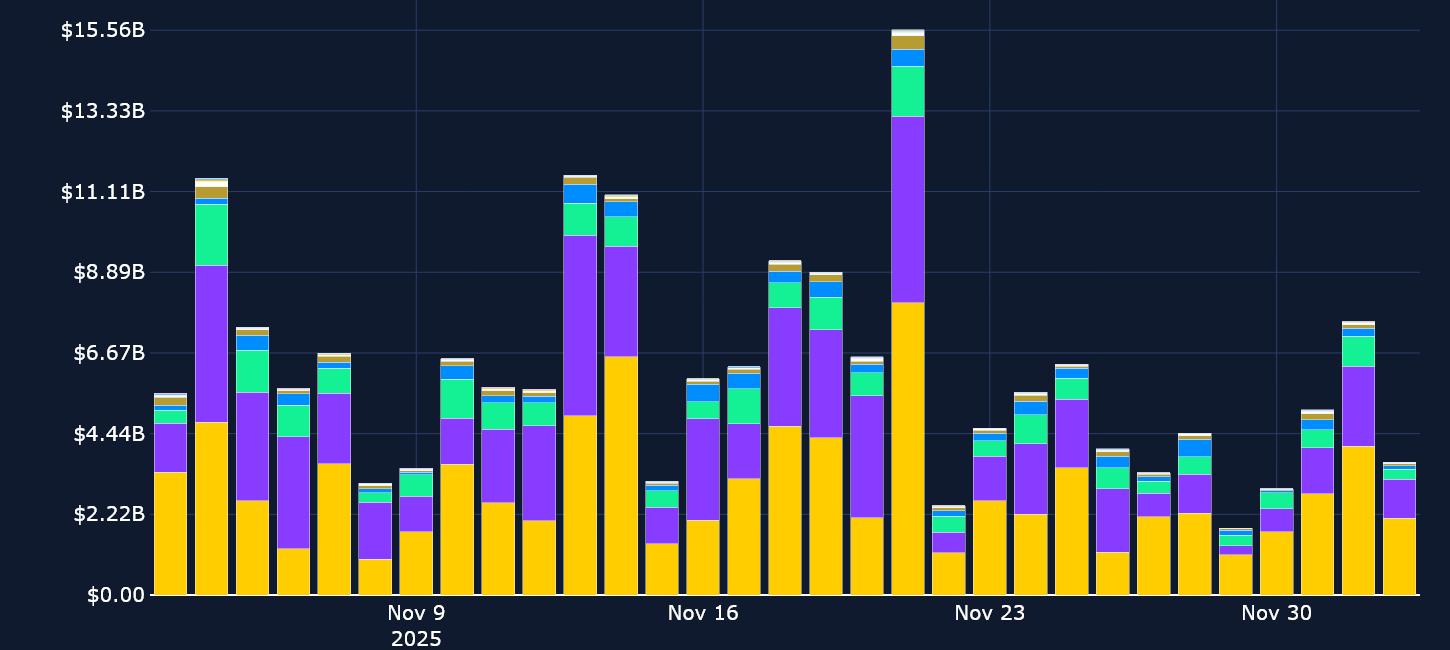

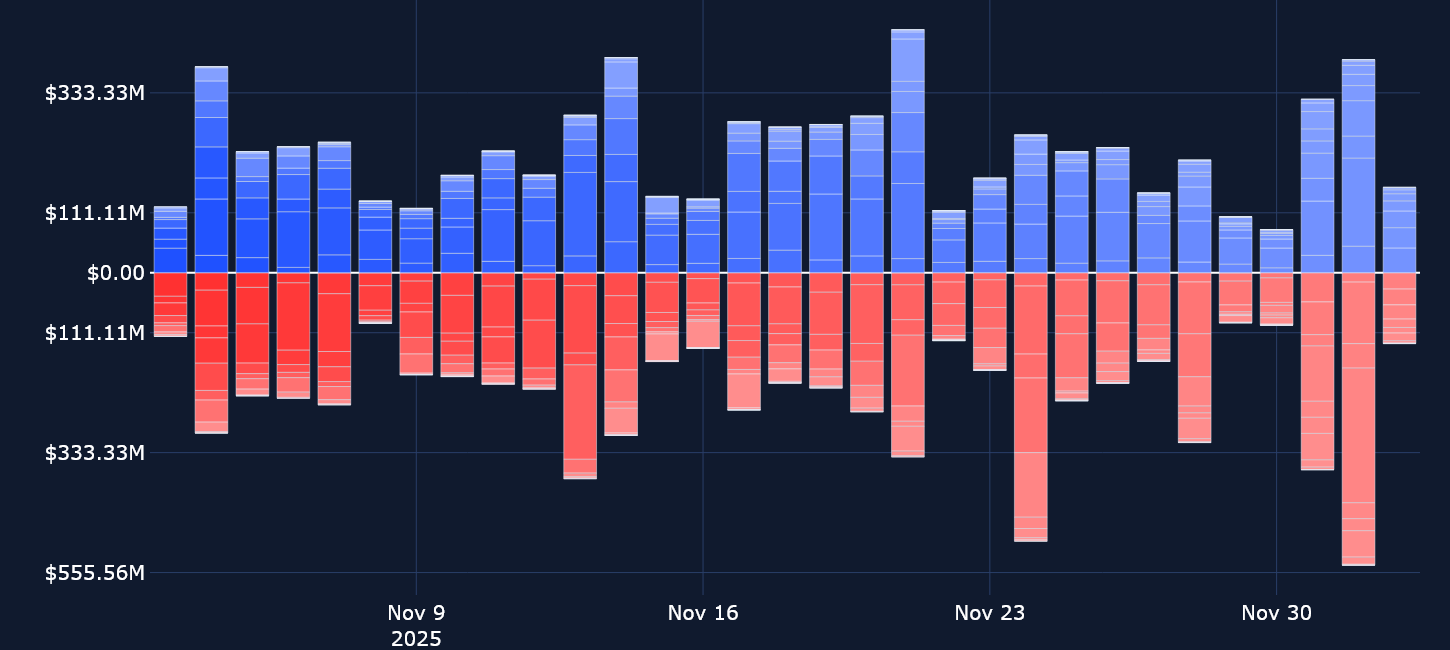

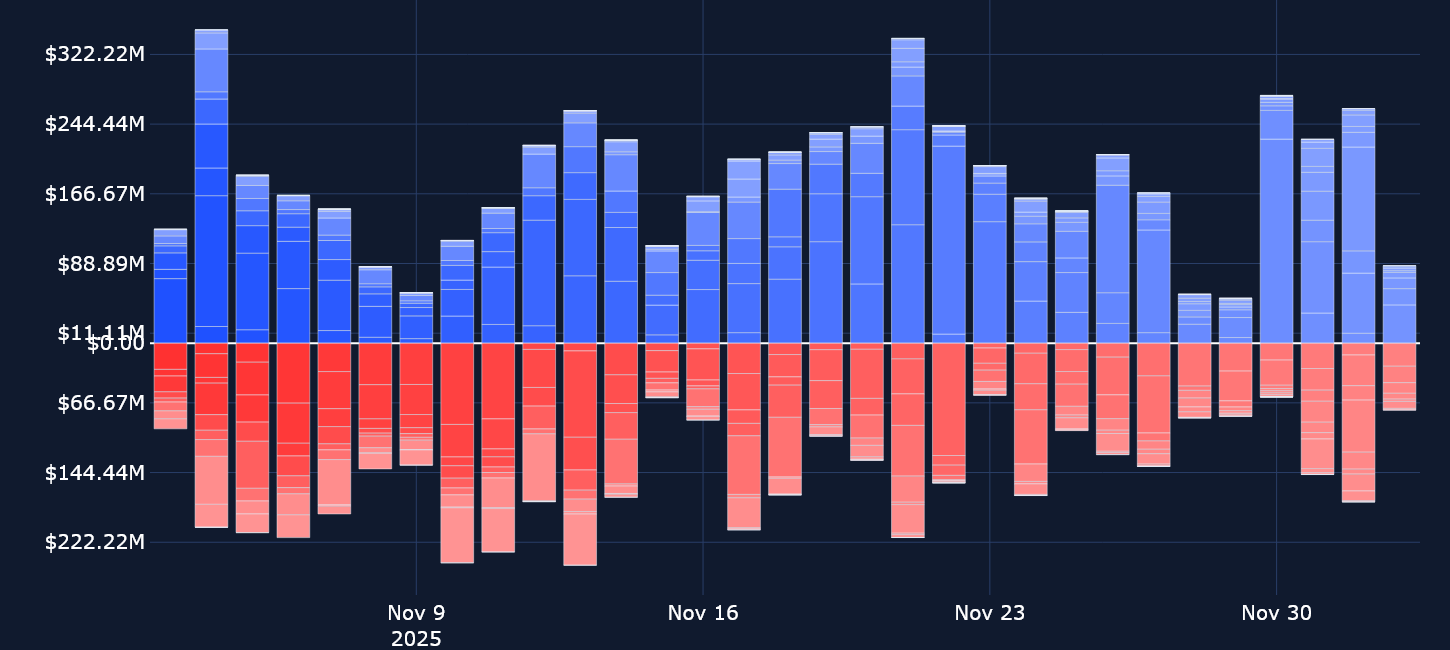

The month of December began with a crypto selloff in early Asian trading hours as Japanese government bond yields spiked higher after Bank of Japan Governor Kazuo Ueda indicated the central bank would be open to an interest rate hike in its December meeting. The selloff extended through the day and BTC fell as low as $83K – however, that did not have much of a noticeable impact on perpetual swap contract open interest.

We’ve noted in previous editions that recent selloffs in spot price have not shown the tell-tale signs of a liquidation cascade, particularly as post Oct 10, 2025, there appears to be a far lower participation rate in leveraged positions.

Nonetheless, the recent recovery rally back above $93K, a two-week high, did encourage some traders to get back into the market, with open interest levels now rising slightly to just under $9B.

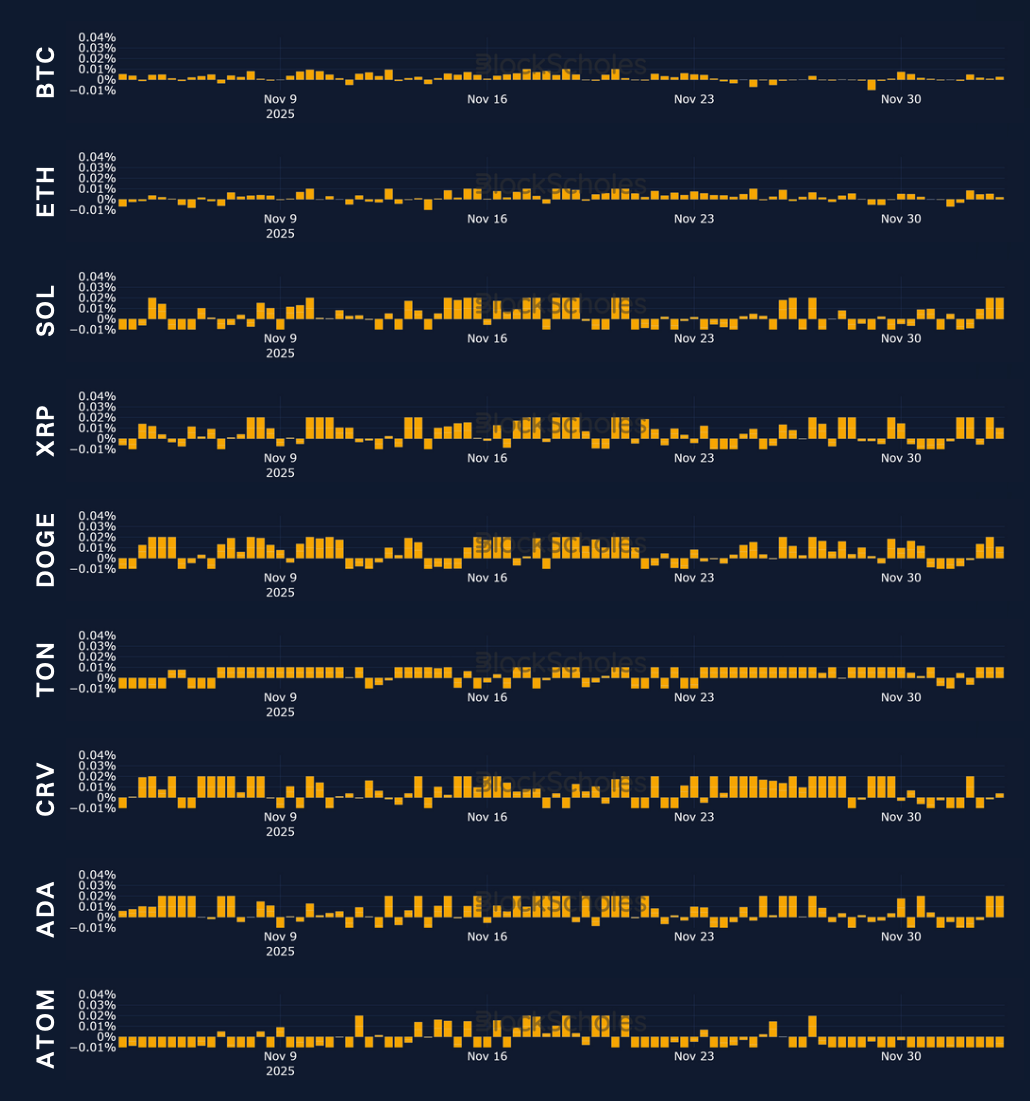

The past week of funding rates highlights a phenomenon we have been observing since the Oct 10, 2025 crash: that funding rates show a clear pattern of altcoin weakness.

The funding rate shows the relative demand for leveraged long or short exposure through perpetual swap contracts. What we find is that, excluding BTC, the majority of tokens, including large-caps such as ETH, SOL, and XRP have recorded negative funding rates during downturns in spot price. On Dec 1, 2025, the aforementioned tokens all saw their funding rate drop below 0, an indication of shorts willing to pay a fee to maintain their position and bet on further downside. All the while, despite BTC’s spot price also falling alongside altcoins, traders were not willing to pay for the privilege of being short: BTC funding rates for the most part have shown incredible resilience, recording only one negative funding rate over the past seven days.

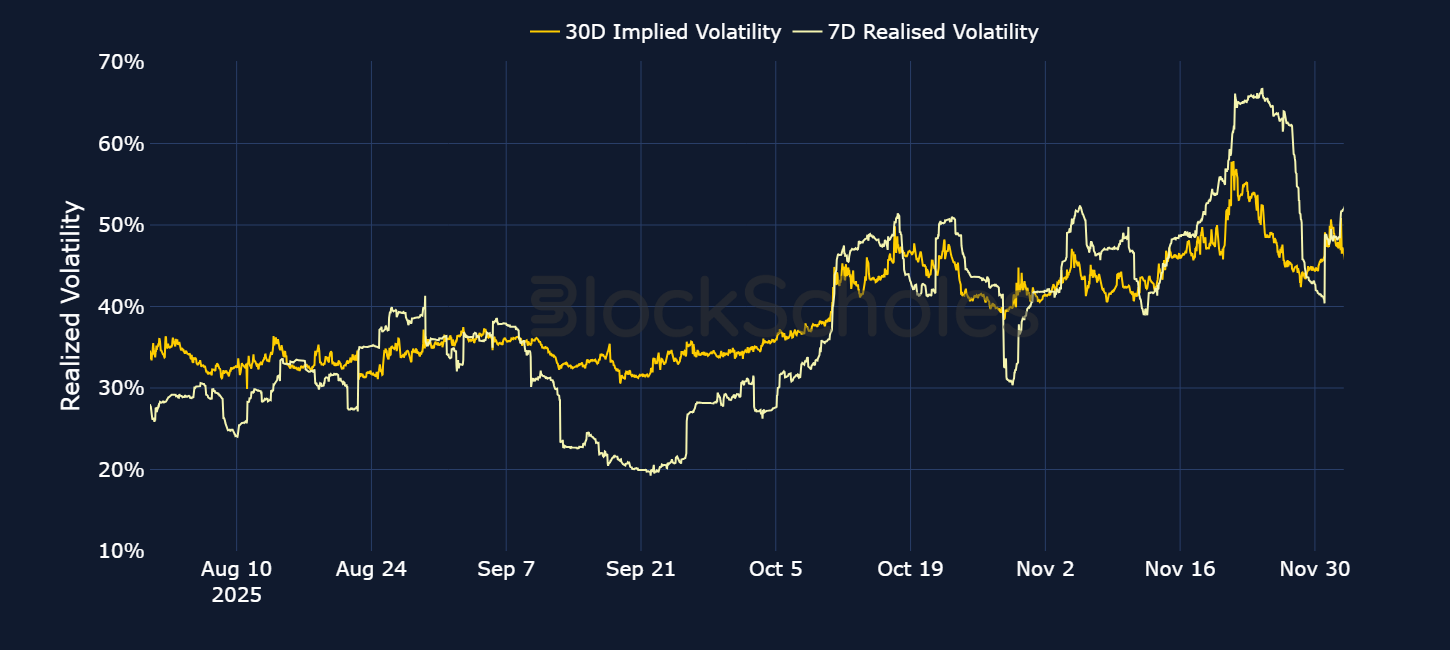

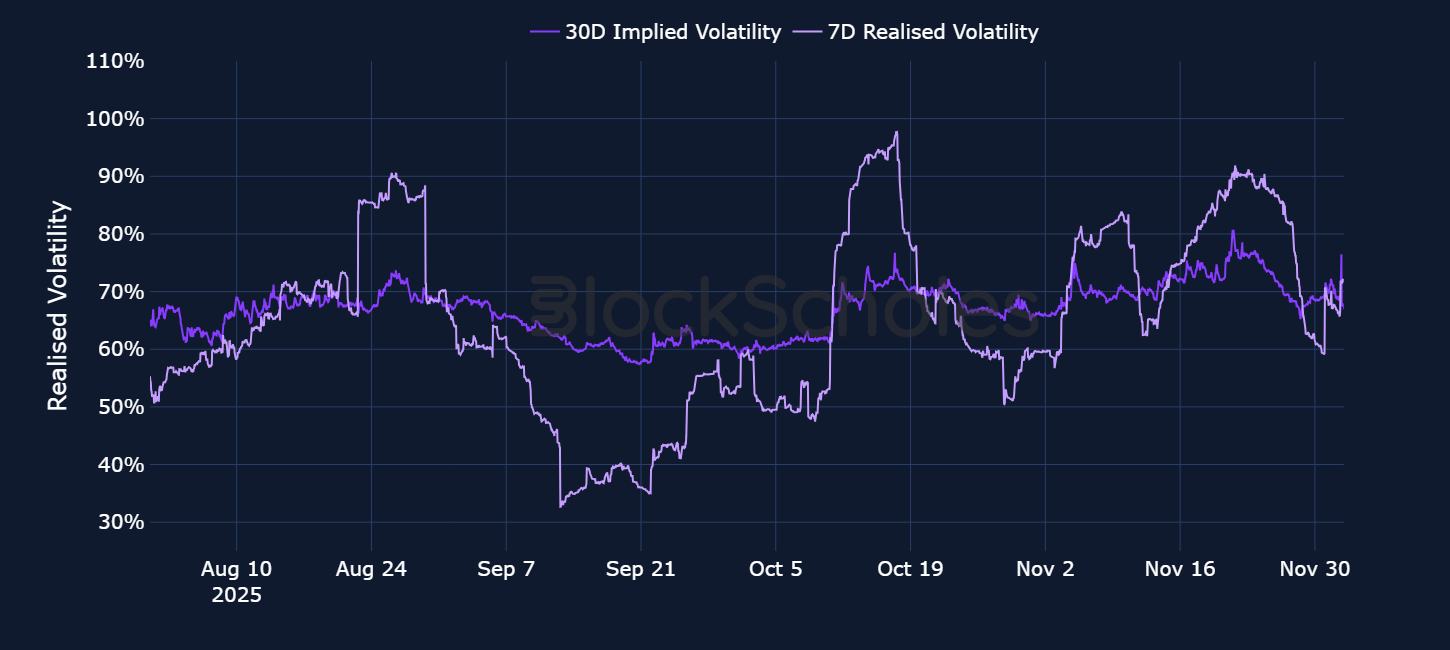

BTC’s continued tight correlation with risk-on macro asset classes has seen it mostly move in line with US equities over the past week. Having become almost a short-hand for risk appetite, BTC was the first to sell off amidst the most recent jump higher in JGB bond yields after the Bank of Japan announced it was weighing the pros and cons of an interest rate hike. When US equities began trading later in the day, BTC extended its drop and fell alongside the S&P 500. That inspired a small and short-lived inversion in the term structure of implied volatility, as well as a 10 percentage point increase in realized volatility.

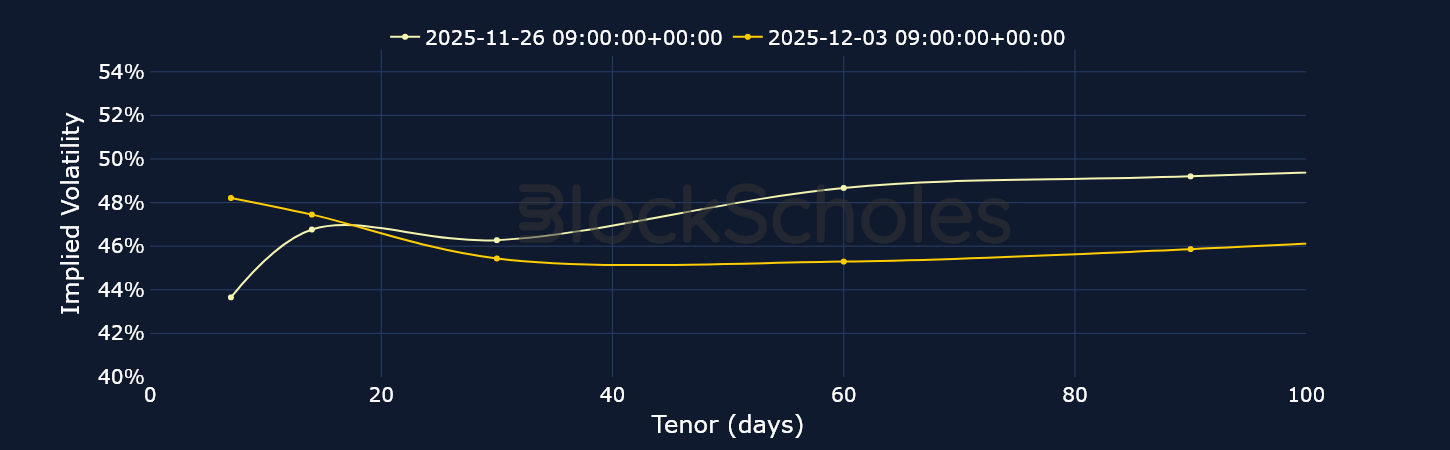

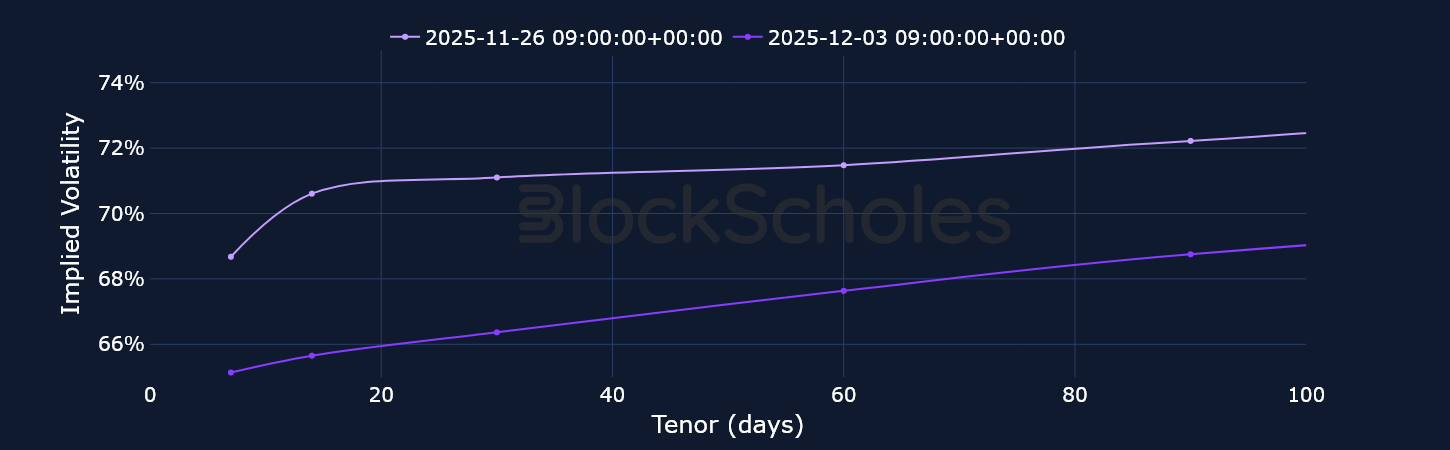

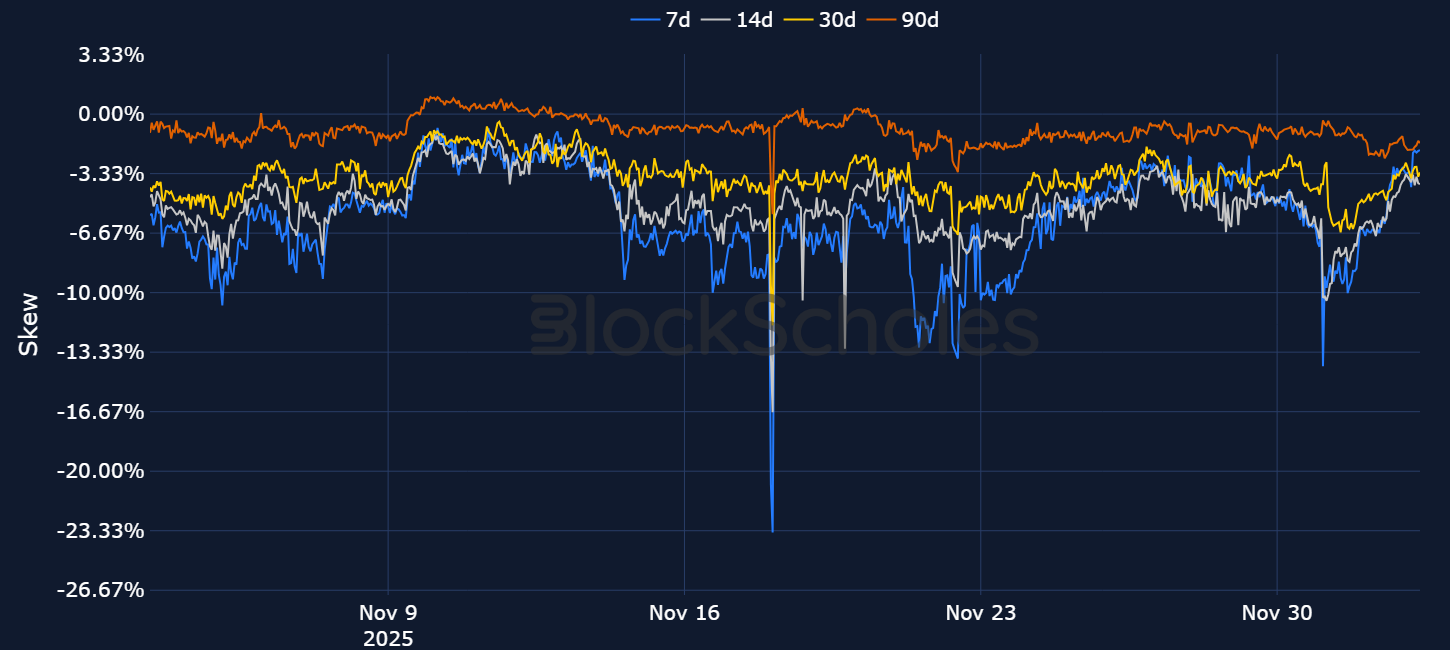

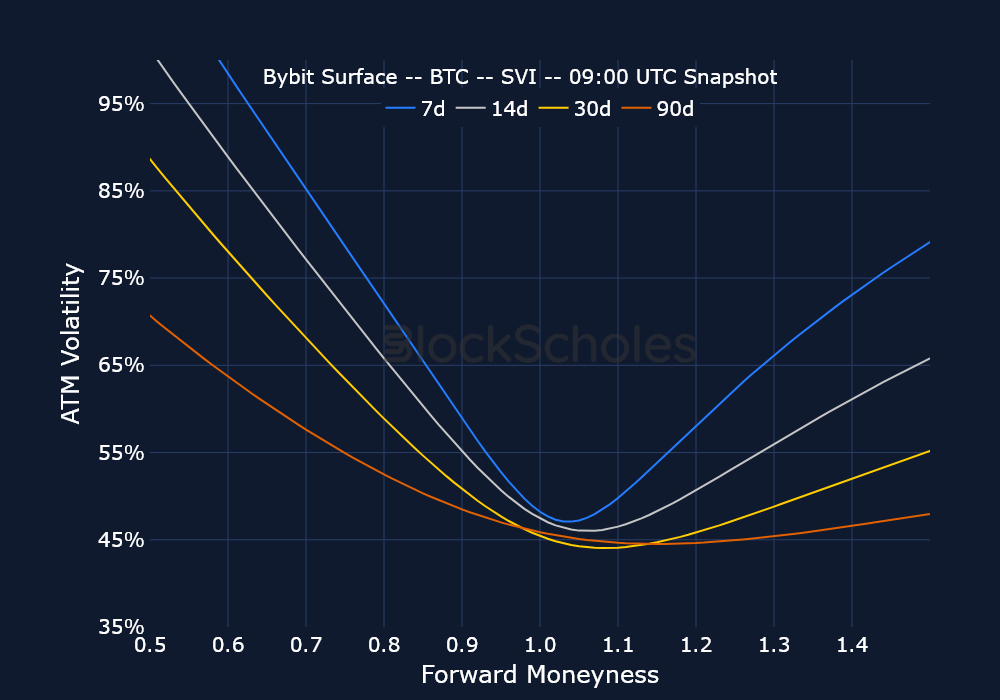

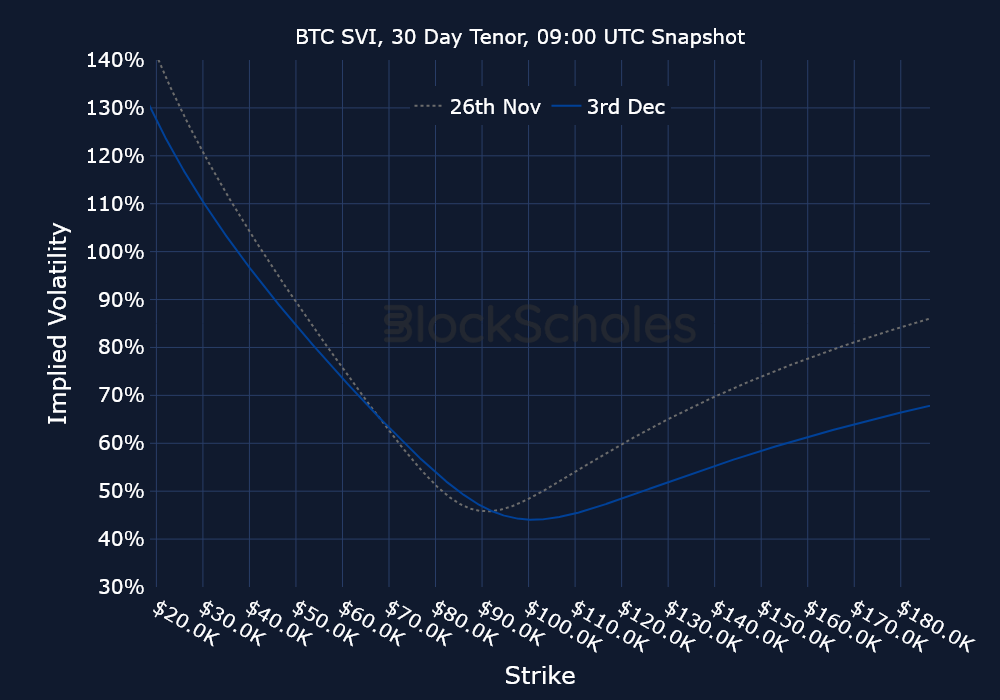

Short-tenor ATM implied volatility quickly fell back down however as BTC spot price began to recover back above $90K. That’s also bolstered a repricing in BTC’s volatility smiles which are now far less bearish than they were coming into the month, though still remain slightly skewed towards OTM puts.

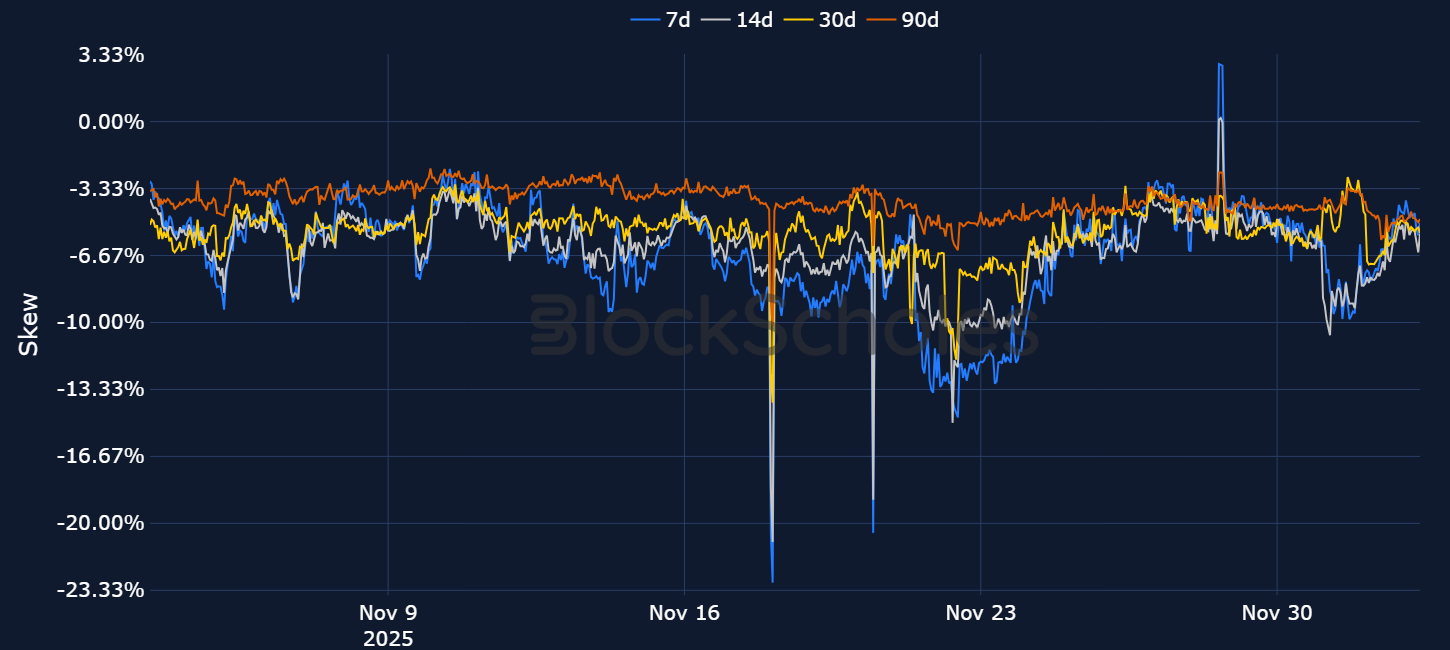

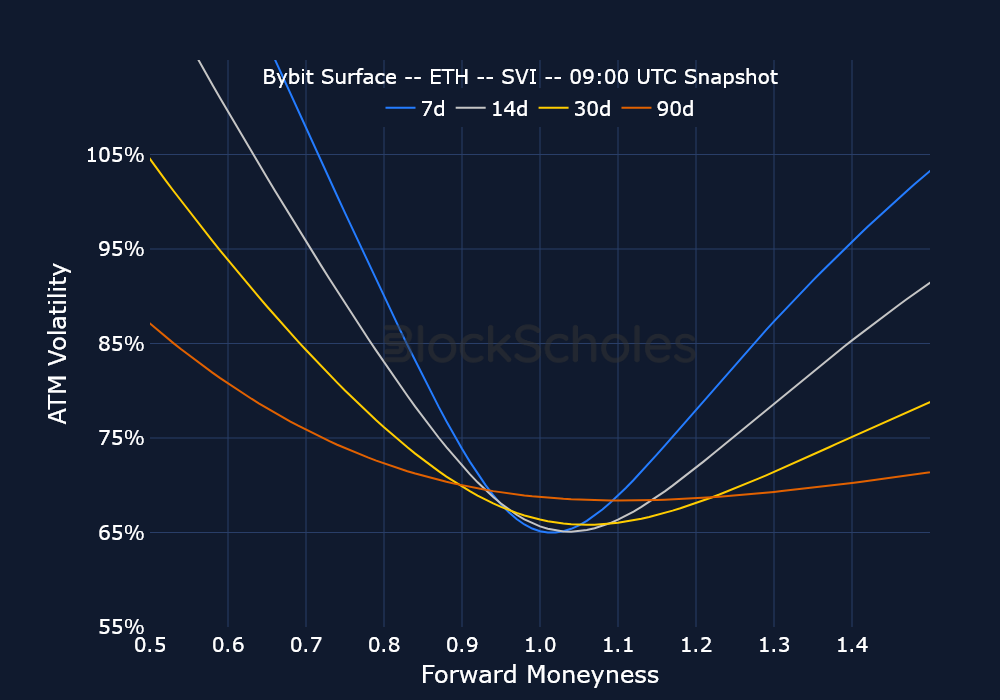

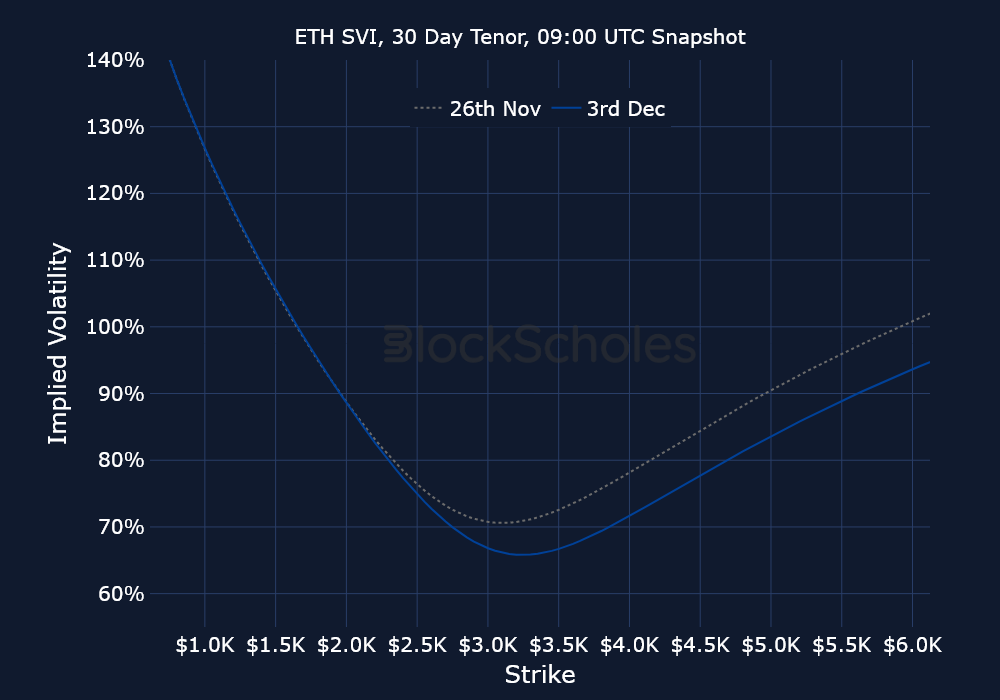

ETH’s spot price has once more reclaimed the $3,000 mark after falling as low as $2,700 on the first trading day of December. Still, it remains below its all-time high by 35%. Therefore, positioning in its options markets are unsurprisingly bearish. While the recent reclaim of the psychological $3,000 level has seen a sharp recovery in its put-call skew ratio, that recovery hasn’t been enough to shift towards a premium towards calls just yet. Instead, markets have priced out much of their extreme premium for downside protection, without pricing-in a dramatic reversal of the circa 40% drawdown just yet. Similar to BTC, ETH’s term structure of at-the-money volatility inverted during the selloff on Dec 1, 2025, following a more than 10 point increase in realized volatility. Both open interest and trade volumes have been dominated in calls over the past week, a reprieve from the put-heavy activity we saw in early November.

The most recent bounce back above $93K and $3,000 for BTC and ETH respectively has had its most noticeable impact on the volatility smiles of both assets in their options markets. At the start of the month, short-tenor smiles for BTC showcased OTM put options trading with a 10 vol point premium over call options at a similar moneyness. For ETH put options, that premium was closer to 13 percentage points. Since then, the put-call skew ratio has recovered from its bearish tilt, with put contracts for BTC demanding a smaller, though still notably bearish 4% premium, and for ETH only a 2% premium. While they are not yet pricing-out further downside, traders are at least pricing downside protection with far less of the premium they had been willing to pay only one week ago.

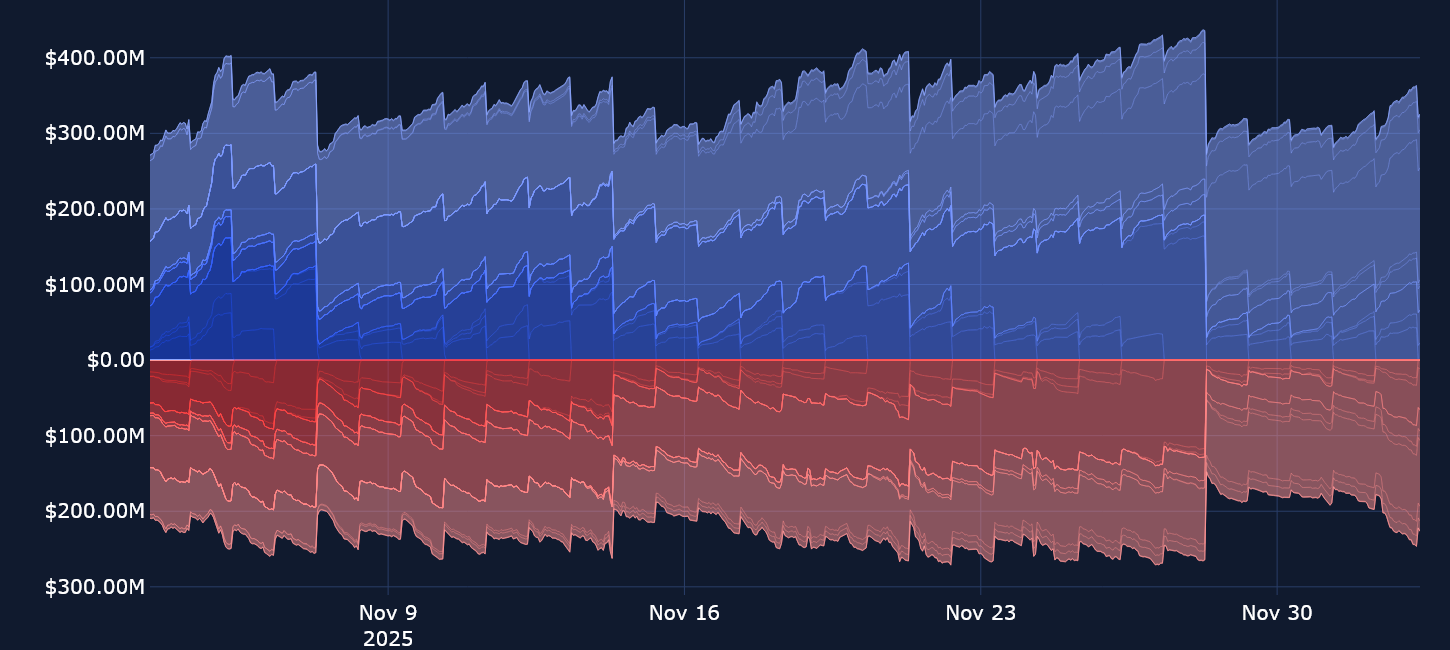

Open interest and trading volume data are sourced “as is” from the Bybit exchange platform API exclusively, and as such do not represent a comprehensive picture of the sum of trading activity across all derivatives markets or exchanges. The data visualized in this report consists of hourly and daily snapshots, recorded over the previous 30 days. Daily (hourly) snapshots of trade volume record the total sum of the notional value of trades recorded in the 24H (1 hour) period, beginning with the snapshot timestamp.

If not explicitly labeled as derived from another exchange, the input instrument prices to all derivatives analytics metrics in this report are sourced from the appropriate endpoints of Bybit’s public exchange platform API. In the event that data is labeled or referred to as representing the market on another exchange source, that data is sourced from the appropriate endpoint of each respective exchange’s public API.

Macroeconomic charts and data are sourced “as is” from the Bloomberg Terminal. Exchange data is sourced “as is” from publicly available exchange APIs. Block Scholes makes no claims about the veracity of public third-party data.

After acquisition of underlying-denominated raw data for open interest and trading volume on the Bybit exchange platform from Bybit’s API endpoint, equivalent dollar-denominated figures are calculated using the concurrent value of Block Scholes’s Spot Index for the relevant underlying asset.

Block Scholes’s Spot Index represents the aggregate Spot mid-price for a given currency across the top five CEXs by volume (with USD-quoted markets). It considers the proportion of total volume in the instrument on the exchange, as well as the deviation of a data point from those on other exchanges.

Futures prices are used for Block Scholes’s futures-implied yields calculation services in order to derive the constant-tenor annualized yields displayed in the Futures section of this report.

Options prices are used for Block Scholes’s implied volatility calculation services in order to calibrate volatility surfaces, from which all derivatives volatility analytics displayed in the BTC Options and ETH Options sections of this report are calculated. Volatility smiles are constructed by calibrating to mid-market prices observed in Bybit options markets. As part of the calibration process, prices go through rigorous filtration and cleaning steps, which ensures that the resulting volatility surface is arbitrage-free and has exceptional fit to the market observables.

.jpg)

.jpg)