Thahbib Rahman

Research Analyst

The CLARITY Act "markup": Here's what you need to know.

The Senate Banking Committee is set to hold a markup of the Digital Asset Market Clarity Act (CLARITY Act) on Thursday, May 14th , following a bipartisan agreement on one of the bill’s largest sticking points: restrictions around stablecoin yield and rewards.

The CLARITY Act will establish the first comprehensive US crypto market-structure framework, including clearer SEC-CFTC jurisdictional boundaries and a federal regulatory regime for digital asset exchanges, brokers, and dealers.

Despite the significance of the markup, derivatives markets are not showing evidence of strong positioning ahead of the event.

The term structure of volatility for BTC options shows no event-related kink nor implied volatility premium around the debate date, while perpetual futures open interest and funding rates remain broadly neutral, suggesting traders are taking a cautious and balanced approach rather than aggressively positioning for a major volatility event.

The Digital Asset Market Clarity Act of 2025 (H.R. 3633), (the CLARITY Act) marks the most comprehensive US crypto market-structure bill ever to clear a chamber of Congress.

It passed the House by 294 votes to 134 on July 17, 2025, and has spent the last four months under consideration by the Senate.

As of May 6, 2026, a bipartisan compromise on stablecoin yield (struck between Senators Thom Tillis (R-NC) and Angela Alsobrooks (D-MD)) has cleared the last major hurdle and the Senate Banking Committee is set to hold a “markup”.

DECODE: A “markup” is a legislative process where the Senate committee members debate and vote on amendments to the bill to refine, edit, and ultimately decide whether a bill should advance to the full Senate for a vote.

This highly-anticipated Senate “markup” on the CLARITY Act is set for Thursday, May 14, 2026 at 10:30 am ET.

The CLARITY Act achieves two things.

First, it draws a clear line between the CFTC and SEC, the two main US financial regulators, to decide which is in charge of regulating each type of cryptoasset.

Second, it sets up a federal rulebook for the exchanges, brokers, and dealers that trade it:

The Senate Banking Committee is made up of 24 members in the current Congress, with 13 Republicans and 11 Democrats.

For the CLARITY Act to pass the markup and be reported out of committee, it would need a simple majority (13 votes, in the case that every member participates).

Since Republicans hold 13 seats on the committee, they could technically advance the bill without Democratic support; however, unanimous Republican support has not been formally confirmed.

The markup is led by Chairman Tim Scott (R-SC), who controls the committee agenda and manages the bill through the session, while Ranking Member Elizabeth Warren (D-MA) leads the Democratic side of the committee’s response.

There are four main potential sources of contention at this week’s markup, based on public criticism and commentary from senators on the CLARITY Act:

The latest compromise on the CLARITY Act is defined in “SEC. 404. PROHIBITING INTEREST AND YIELD ON PAYMENT”, which:

However, the bank lobby is still not satisfied.

Although President Trump signed the GENIUS Act in July 2025, which created a framework for payment stablecoins and barred issuers from paying interest on digital dollars, the American Bankers Association (ABA) argues that the CLARITY Act still leaves a major loophole. Their concern is that even if stablecoin issuers cannot pay interest directly, other crypto companies, such as exchanges, could still offer interest-like rewards, potentially drawing deposits away from banks and increasing risks for consumers who may not understand that stablecoin wallets are not insured bank accounts.

“Urge your lawmakers to tighten restrictions on paying interest, yield or rewards that function like interest on payment stablecoins to cover all market participants” — American Bankers Association (ABA)

Lummis, Tillis and Alsobrooks have collectively described the stablecoin language as final.

Tillis has pushed back on the bank lobby’s objections, saying they “respectfully agree to disagree,” and signaling that the negotiation is closed.

The possible outcomes are that the committee:

If the Senate rewrite is limited to amendments that have already been negotiated, it could be handled during the markup itself.

But if senators need to reopen major disputes, the committee could delay the vote and postpone the markup, needing to circulate revised text before moving ahead.

This has happened previously with the CLARITY Act when the Senate Banking Committee postponed a January markup after industry support weakened and disputes over stablecoin yield intensified.

If the bill is reported favorably by the committee, it advances for potential consideration by the full Senate.

The White House and several senators have floated July 4, 2026 as a target for signing the CLARITY Act into law, but that appears to be the most optimistic scenario.

"We're targeting July 4th. I think that would be a tremendous birthday present for America, celebrating our 250th." — Patrick Witt, Executive Director, President's Council of Advisors for Digital Assets, Consensus Miami

Based on the timelines for previous bills becoming law, an August–September target appears more realistic, assuming the bill moves through each stage without major objections or procedural delays:

The biggest risk in the realistic schedule is the August recess.

If the bill is not on the President's desk by mid-September, midterm campaigning may take precedence and make a politically charged crypto vote harder to secure the necessary support.

Polymarket bets are pricing in the likelihood of "CLARITY Act signed into law in 2026?" as more likely than not, after the odds repriced from roughly 46% to 64% in the 24 hours after the stablecoin yield compromise release on May 1, 2026. It has since fluctuated between highs of 80% and lows of 60% in anticipation of the markup.

Bloomberg Intelligence also sees a greater-than-even (60%) chance that the CLARITY Act is passed within 2026.

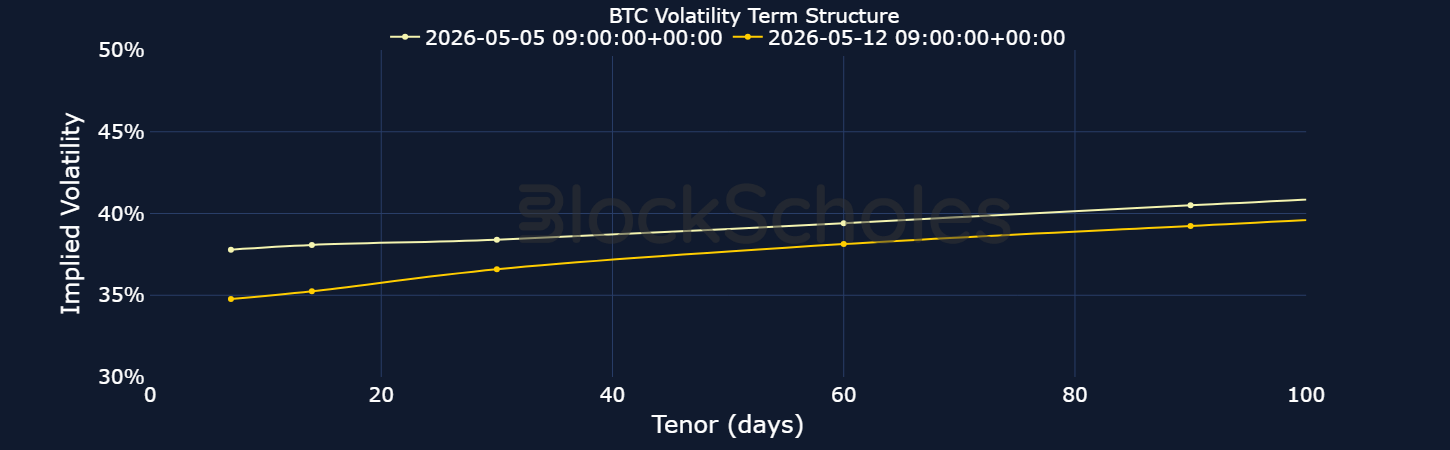

In options markets, the implied volatility term structure for BTC (which shows the relationship between implied volatility of BTC options across different expiration dates) is in its usual upward-sloping form — that is, short-dated options are trading at relatively cheaper levels than longer-dated expirations.

This upward slope represents 'normal' market conditions, where traders demand a premium for selling a potentially higher volatility level over a longer time horizon.

We can check whether the market is pricing in a specific event risk by analyzing any kinks in the term structure at a tenor that straddles the event date.

For example, a snapshot of implied volatility across expirations on May 5, 2026 reveals a mildly upward-sloping curve. On that date, the Senate markup was 9 days away.

Had traders viewed the event as carrying significant tail risk, we would have expected implied volatility to be higher (i.e., a kink in the term structure) for expirations after the date of the Senate markup.

We do not find evidence of BTC's term structure pricing in a higher implied volatility premium around May 14, 2026.

This suggests that BTC options markets are not pricing the Senate markup as a meaningful catalyst for volatility.

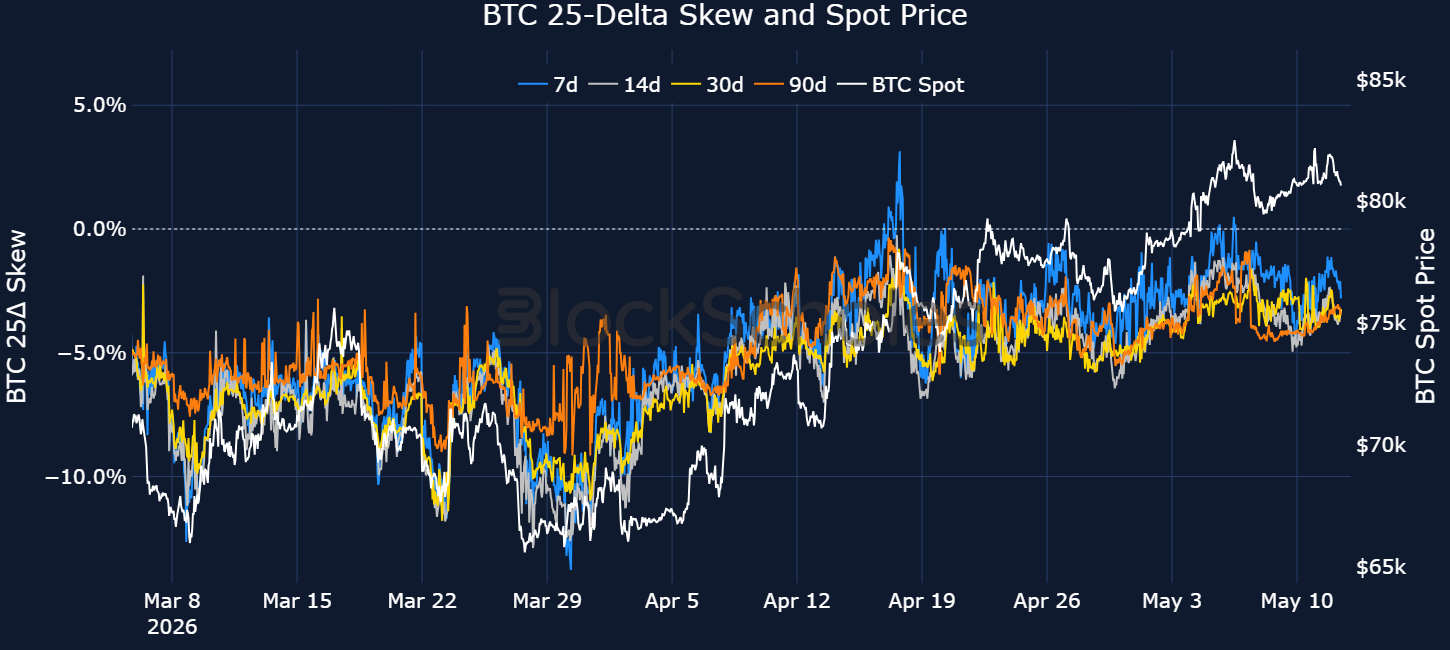

Looking at put-call skew, we also find evidence that, despite spot trading in a new higher range near $80K and the regulatory tailwind that would come from the passing of the CLARITY Act, traders remain bearish in options markets.

7-day BTC skew currently shows close to a 3 vol-point premium of out-of-the-money puts over calls.

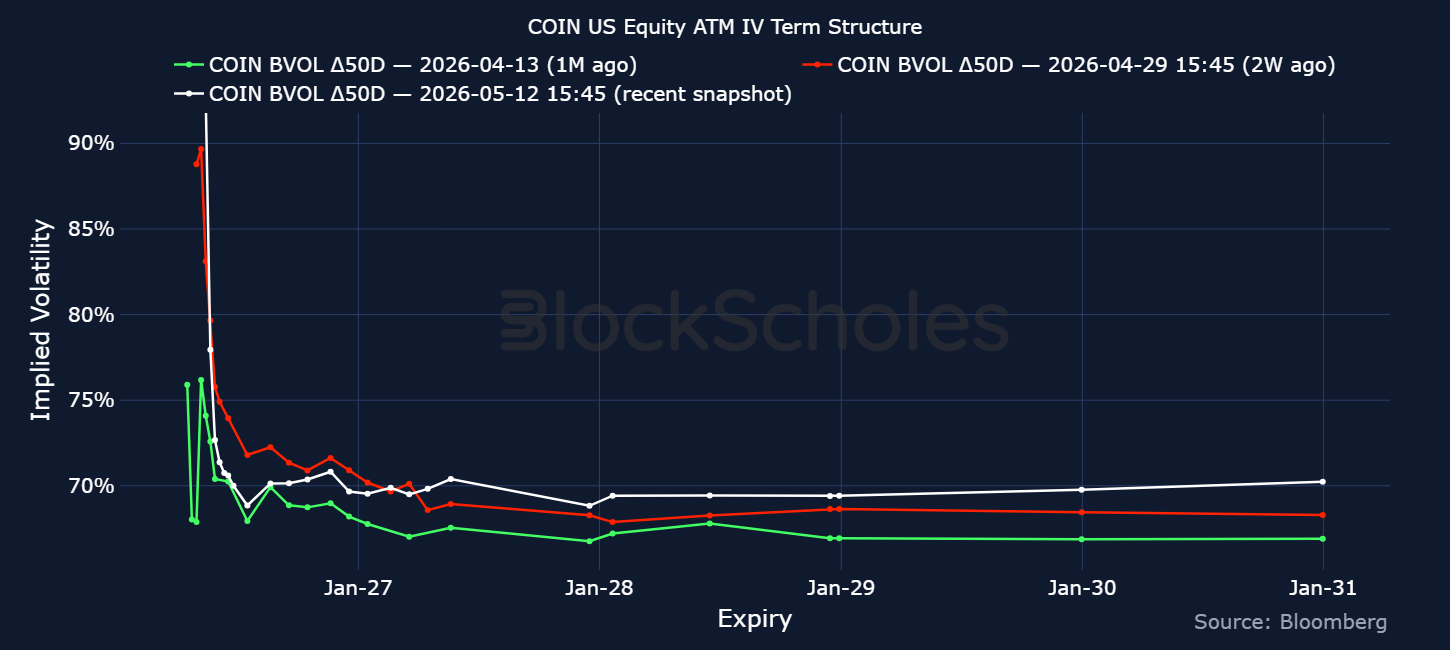

However, while no clear event risk is priced into BTC options around the Senate markup, a much clearer kink is apparent in Coinbase's COIN options.

At-the-money implied volatility for the May 15, 2026 expiry — the first listed expiry after the May 14 markup — is trading at 91%, significantly higher than contracts further out along the curve, such as the May 22 contract at 78% and the May 29 contract at 73%. That significant vol-point spread shows a clear event-risk premium attached to the markup itself.

The migration of this kink across the three snapshots further supports this.

One month ago (April 13, 2026), the May 15 expiry traded at a similar implied volatility level to its neighbours, around 74%, given that the markup was still over a month away. At that time, the front-end of the curve was dominated by the May 8 expiry, which captured Coinbase's Q1 earnings released on May 7.

Two weeks ago (April 29, 2026), with 15 days to the markup, the May 15 contract had begun to detach from the curve at 83%, and now, just days ahead of the markup, the same contract trades at 91%.

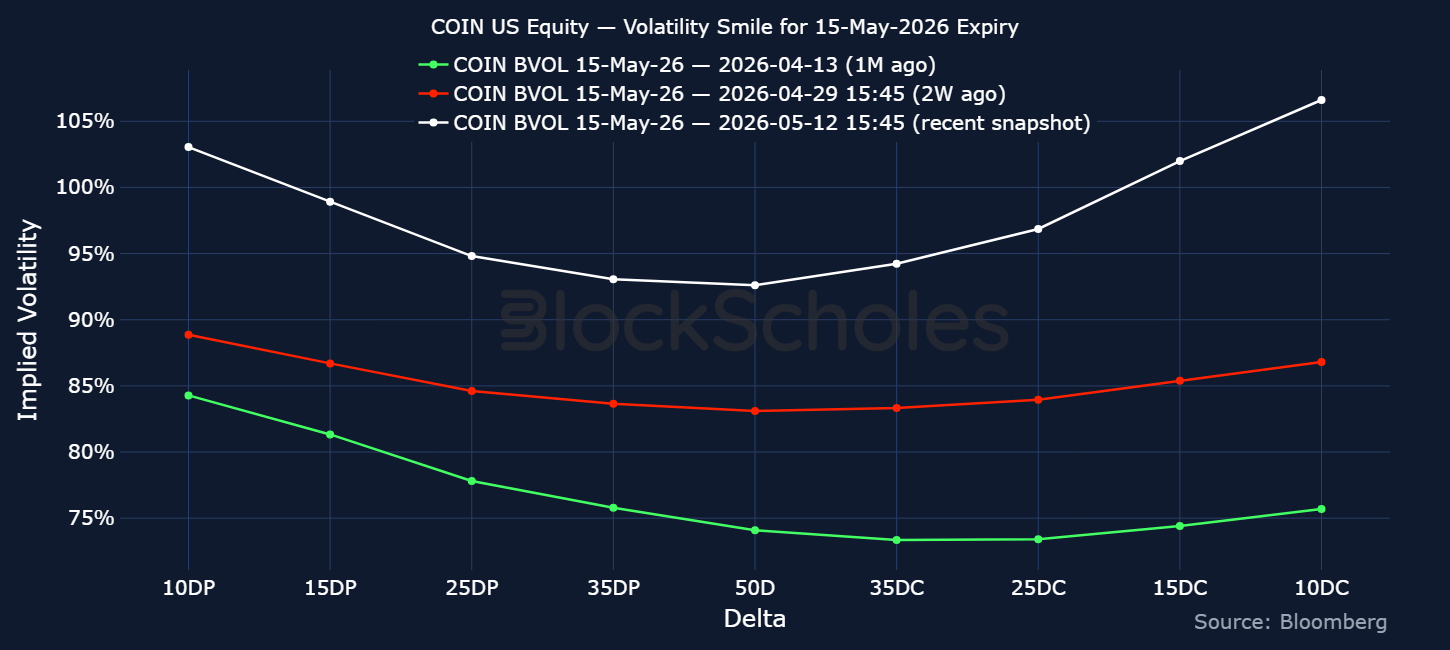

Looking at the evolution of the volatility smile for the May 15, 2026 expiry — which covers the markup date — we see that options traders have priced out the put-premium in COIN options over the past month and rotated to bullish positioning ahead of the event.

One month ago (green curve below), the 25-delta put-call skew was trading around −4.4%. That put premium has now flipped, with OTM calls trading around 2 vol points above puts (white curve). This has occurred alongside a rally in the COIN spot price from $181 to $207 over the same period.

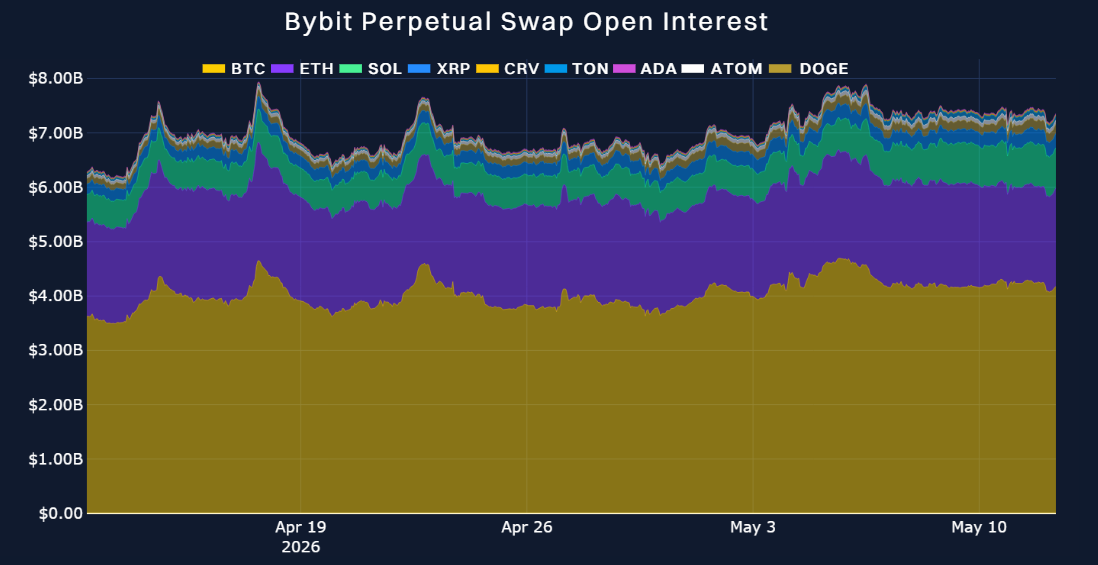

Open interest in altcoin perpetual futures contracts does not show traders rushing in to open new contracts or take speculative positions ahead of the bill markup.

Over the past week, open interest across a selection of blue-chip altcoins and Bitcoin has moved sideways above $7B, suggesting a lack of interest from traders in entering leveraged perp positions.

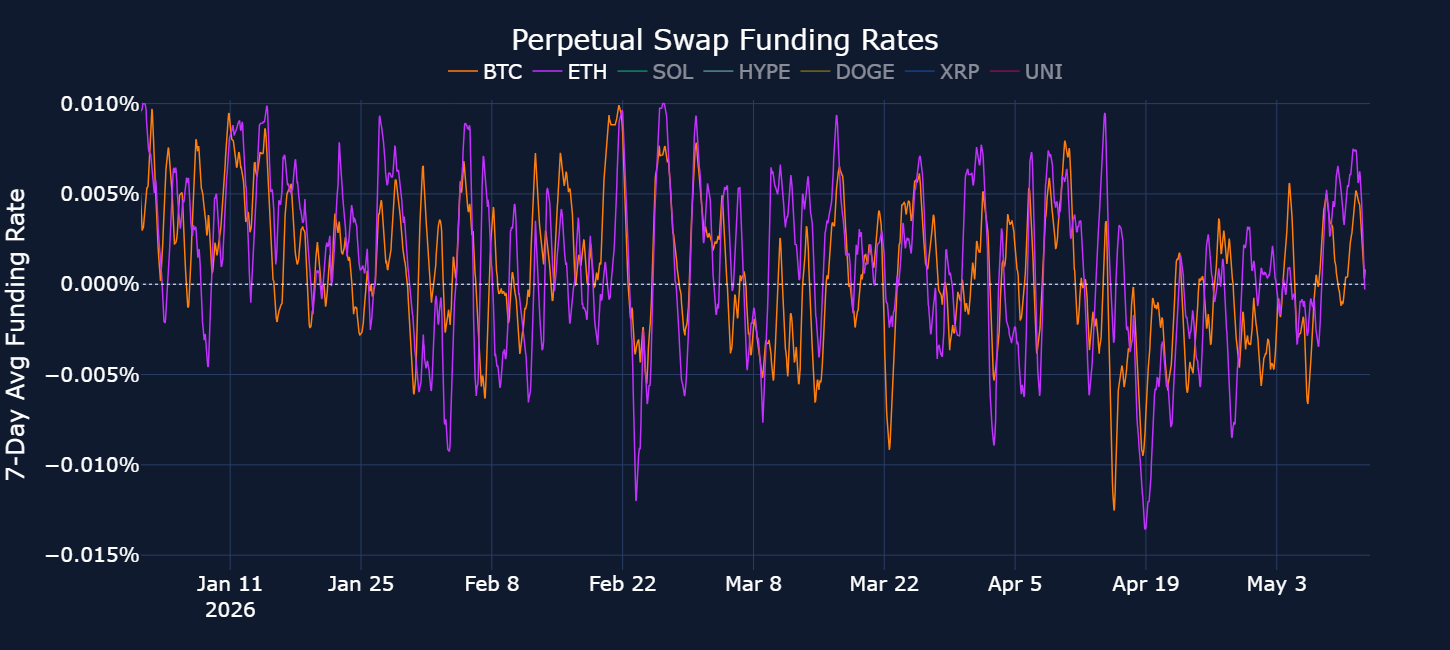

The same lack of interest is reflected in funding rates. Average 7-day rolling funding rates for BTC and ETH are both close to the neutral 0% level, indicating balanced sentiment amongst traders.

1) Strategy Chairman Michael Saylor said the company may selectively sell bitcoin to support dividends tied to its STRC preferred stock program, but stressed that Strategy intends to remain a net BTC accumulator.

“In these periods, even if we were to sell one bitcoin, we’d be buying 10 to 20 more bitcoin,” Saylor said.

He added: “When I said ‘never sell your bitcoin,’ I mean make sure if you were to spend it on something, you replenish in the time you spend it,” following comments during last week’s earnings call where executives said Strategy could use its bitcoin treasury to fund STRC dividend obligations.

2) Ethereum core developers and client teams met for a week-long interoperability event focused on preparing the network’s upcoming Glamsterdam upgrade.

Teams aligned around a target 200M gas limit floor, stabilised ePBS infrastructure — a proposer-builder separation system designed to improve block production efficiency and reduce centralisation risks — and finalized EIP-8037 repricing changes.

The repricing adjusts Ethereum’s state storage costs to better reflect network resource usage and support higher throughput.

3) Boundary Labs, a New York-based stablecoin infrastructure startup, has raised $2M in pre-seed funding led by Galaxy Ventures to launch USBD, a stablecoin protocol designed for institutional users with on-chain reserve verification and compliance-focused onboarding.

The company said USBD is targeting the growing $300B+ stablecoin market by offering continuous on-chain auditability, institutional-only access through KYC/KYB-gated onboarding, and infrastructure aimed at treasury management with regulated wrappers.

4) TON Core has launched Acton, a new all-in-one CLI for building AI agents and smart contracts on the TON network.

Built around Tolk, Acton brings the full smart contract workflow into one unified toolchain, including project creation, native testing, debugging, dApp integration, deployment and verification.

5) Ondo announced on Tuesday that its tokenised stocks and ETFs can now be bridged to Hyperliquid’s HyperEVM via LayerZero.

The move brings equity-linked assets into HyperEVM’s DeFi ecosystem, giving traders access to spot positions that can support more advanced strategies, including basis trades and delta-neutral hedging.

6) Sui, the Layer 1 blockchain developed by Mysten Labs, has seen its native token SUI rally around 40% over the past week after Nasdaq-listed SUI Group Holdings staked its entire treasury of over 108M SUI tokens, worth approximately $143M.

Mysten Labs co-founder Adeniyi Abiodun said the network will soon introduce zero-fee stablecoin transfers and private transaction functionality.

The team is positioning Sui as low-cost infrastructure for payments, liquidity movement, and AI-driven on-chain transactions amid growing market interest in privacy-focused crypto systems.

7) MARA, a publicly traded Bitcoin miner, reported Q1 2026 revenue of $174.6M, down 18% year-on-year, while net losses widened to $1.26B primarily due to a $1.0B mark-to-market loss on its bitcoin holdings following BTC’s 22% quarterly decline.

The company mined 2,247 BTC during the quarter and ended March with 35,303 BTC worth roughly $2.4B, including 9,995 BTC that were loaned or pledged as collateral.

Energised hashrate rose 33% year-on-year to a record 72.2 EH/s, and fleet efficiency improved to 17.6 J/TH.

8) LayerZero, a cross-chain interoperability and messaging protocol, issued a public apology over its handling of the April 18 exploit that drained roughly $292M in rsETH from Kelp DAO’s bridge.

The firm admitted it “made a mistake” by allowing its DVN verifier network to operate in a vulnerable 1-of-1 configuration for high-value transactions.

LayerZero said the protocol itself was not compromised, but that internal RPC infrastructure used by the LayerZero Labs DVN was allegedly poisoned by the Lazarus Group while external RPC providers were simultaneously hit by DDoS attacks.

The incident impacted a single application representing around 0.14% of LayerZero apps and 0.36% of bridged asset value.

9) Amazon Web Services, Coinbase, and Stripe have launched preview support for Amazon Bedrock AgentCore Payments, enabling AI agents to autonomously pay for APIs, web content, MCP servers, and other agent services using stablecoin micropayments executed inside the agent workflow itself.

AgentCore integrates Coinbase’s x402 protocol and wallet infrastructure alongside Stripe-owned Privy wallets, allowing developers to set spending limits, manage authentication, and execute machine-to-machine payments in real time when an agent encounters a paid endpoint returning an HTTP 402 “Payment Required” response.

Transactions are settled through stablecoin payment rails.

10) 21Shares has launched the first U.S. exchange-traded fund offering direct exposure to Canton Coin (TCAN), the native utility token of the Canton Network.

The new fund, the 21Shares Canton Network ETF, began trading on Nasdaq under the ticker TCAN.

According to 21Shares, institutional interest in Canton has been driven by its focus on privacy-preserving infrastructure for capital markets.

11) TrustedVolumes, a liquidity provider and market maker integrated with 1inch, a decentralised exchange aggregation protocol, has suffered an ongoing exploit targeting its Ethereum-based resolver contract, with losses initially estimated at $6.7M.

According to Blockaid, a blockchain security and transaction monitoring firm, the attacker exploited a vulnerability in a TrustedVolumes-controlled custom RFQ (request-for-quote) swap proxy.

Drained assets include 1,291 WETH, 206K USDT, 16.9 WBTC, and 1.26M USDC.

12) American Bitcoin, a Bitcoin mining and treasury company co-founded by Eric Trump, reported an $81.8M net loss in Q1, primarily driven by a $117.2M mark-to-market loss on digital assets as BTC declined 22% during the quarter.

Despite lower mining revenue ($62.1M vs. $78.3M in Q4), the firm achieved record production of 817 BTC and acquired an additional 803 BTC for treasury reserves.

Total holdings rose to 7,021 BTC while mining costs improved by 23% to $36,200 per BTC.

13) Ondo Finance, a tokenisation platform for real-world assets, alongside Kinexys by J.P. Morgan, Mastercard, and Ripple, completed a pilot transaction linking the XRP Ledger with traditional interbank settlement infrastructure to process cross-border settlement of tokenised US Treasuries.

The workflow involved redemption of Ripple-held OUSG (Ondo Short-Term US Government Treasuries Fund) on the XRP Ledger.

Settlement instructions were routed through Mastercard’s Multi-Token Network, with final USD settlement via Kinexys by J.P. Morgan into Ripple’s Singapore banking account.

14) Morgan Stanley has begun a pilot rollout of spot cryptocurrency trading on its E*Trade retail brokerage platform, according to Bloomberg.

The pilot introduces a 50-basis-point transaction fee on the dollar value of each crypto trade.

The service is currently live for a limited group of users, with broader access for E*Trade’s 8.6M clients expected later this year.

15) BNY is expanding its digital asset custody business into the United Arab Emirates through new partnerships with Finstreet and ADI Foundation.

The bank said the collaboration will focus on delivering institutional-grade crypto custody services within the Abu Dhabi Global Market.

The initial offering will support custody for Bitcoin and Ether on behalf of Finstreet’s clients.

BNY, Finstreet and ADI Foundation also plan to explore further integration with ADI Foundation’s blockchain infrastructure.

CoreWeave Inc. is a publicly traded US-based cloud infrastructure company focused on high-performance computing for artificial intelligence, machine learning, visual effects, rendering, and other GPU-intensive workloads.

This new TradFi perpetual contract provides market participants with exposure to CoreWeave as a listed AI infrastructure company.

Rather than operating as a broad general-purpose cloud provider, CoreWeave has built its platform around specialised GPU infrastructure, high-speed networking, orchestration, storage, and workload management designed for customers that need scalable compute capacity for advanced AI and accelerated computing applications.

CoreWeave is purpose-built for accelerated computing rather than traditional enterprise cloud workloads.

Its platform is designed around large GPU clusters connected by high-speed interconnects, with workload orchestration built specifically for AI training and inference.

At this scale, performance depends less on the number of GPUs available and more on how efficiently they work together. That requires a tightly integrated infrastructure layer: fast networking to reduce bottlenecks, workload management to maintain high utilisation, scalable storage to support large datasets, and reliability across the full compute environment.

CoreWeave’s focus on purpose-built AI infrastructure gives it a differentiated role in the market as demand for high-performance compute continues to grow.

This makes CoreWeave relevant to several structural themes in technology markets.

Demand for AI computers continues to grow as companies move from experimentation to production deployment of generative AI, model fine-tuning, inference, and enterprise AI applications.

At the same time, GPU supply, data-centre power availability, and infrastructure efficiency remain key bottlenecks.

CoreWeave’s business model is therefore closely linked to the expansion of the AI infrastructure layer: the physical and software stack that supports large-scale artificial intelligence workloads.

For market participants, CoreWeave stands out because it provides exposure to the compute infrastructure underpinning the AI value chain.

Public-market AI narratives often centre on model developers, semiconductor companies, and software platforms. CoreWeave occupies a different position: it sits closer to the infrastructure layer, supplying the capacity that AI companies and enterprises need to build and run increasingly compute-intensive systems.

Its growth prospects are therefore linked to the continued expansion of AI workloads, rising enterprise adoption, and broader demand for accelerated computing.

Open interest and trading volume data are sourced “as is” from the Bybit exchange platform API exclusively, and as such do not represent a comprehensive picture of the sum of trading activity across all derivatives markets or exchanges. The data visualised in this report consists of hourly and daily snapshots, recorded over the previous 30 days. Daily (hourly) snapshots of trade volume record the total sum of the notional value of trades recorded in the 24H (1 hour) period, beginning with the snapshot timestamp.

If not explicitly labelled as derived from another exchange, the input instrument prices to all derivatives analytics metrics in this report are sourced from the appropriate endpoints of Bybit’s public exchange platform API. In the event that data is labelled or referred to as representing the market on another exchange source, that data is sourced from the appropriate endpoint of each respective exchange’s public API.

Macroeconomic charts and data are sourced “as is” from the Bloomberg Terminal. Exchange data is sourced “as is” from publicly available exchange APIs. Block Scholes makes no claims about the veracity of public third-party data.

After acquisition of underlying-denominated raw data for open interest and trading volume on the Bybit exchange platform from Bybit’s API endpoint, equivalent dollar-denominated figures are calculated using the concurrent value of Block Scholes’ Spot Index for the relevant underlying asset.

Block Scholes’s Spot Index represents the aggregate Spot mid-price for a given currency across the top five CEXs by volume (with USD-quoted markets). It considers the proportion of total volume in the instrument on the exchange, as well as the deviation of a data point from those on other exchanges.

Futures prices are used for Block Scholes’s futures-implied yields calculation services in order to derive the constant-tenor annualised yields displayed in the Futures section of this report.

Options prices are used for Block Scholes’s implied volatility calculation services in order to calibrate volatility surfaces, from which all derivatives volatility analytics displayed in the BTC Options and ETH Options sections of this report are calculated. Volatility smiles are constructed by calibrating to mid-market prices observed in Bybit options markets. As part of the calibration process, prices go through rigorous filtration and cleaning steps, which ensures that the resulting volatility surface is arbitrage-free and has exceptional fit to the market observables.

.jpg)

.jpg)