Thahbib Rahman

Research Analyst

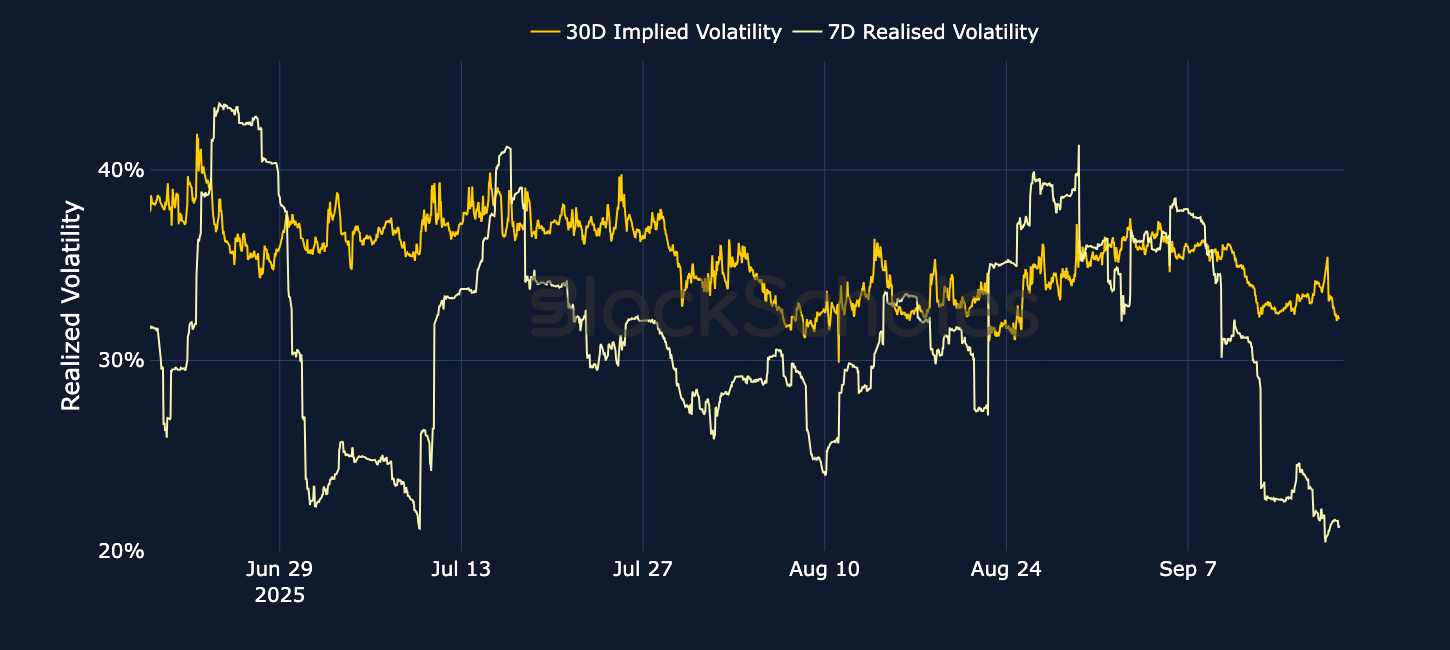

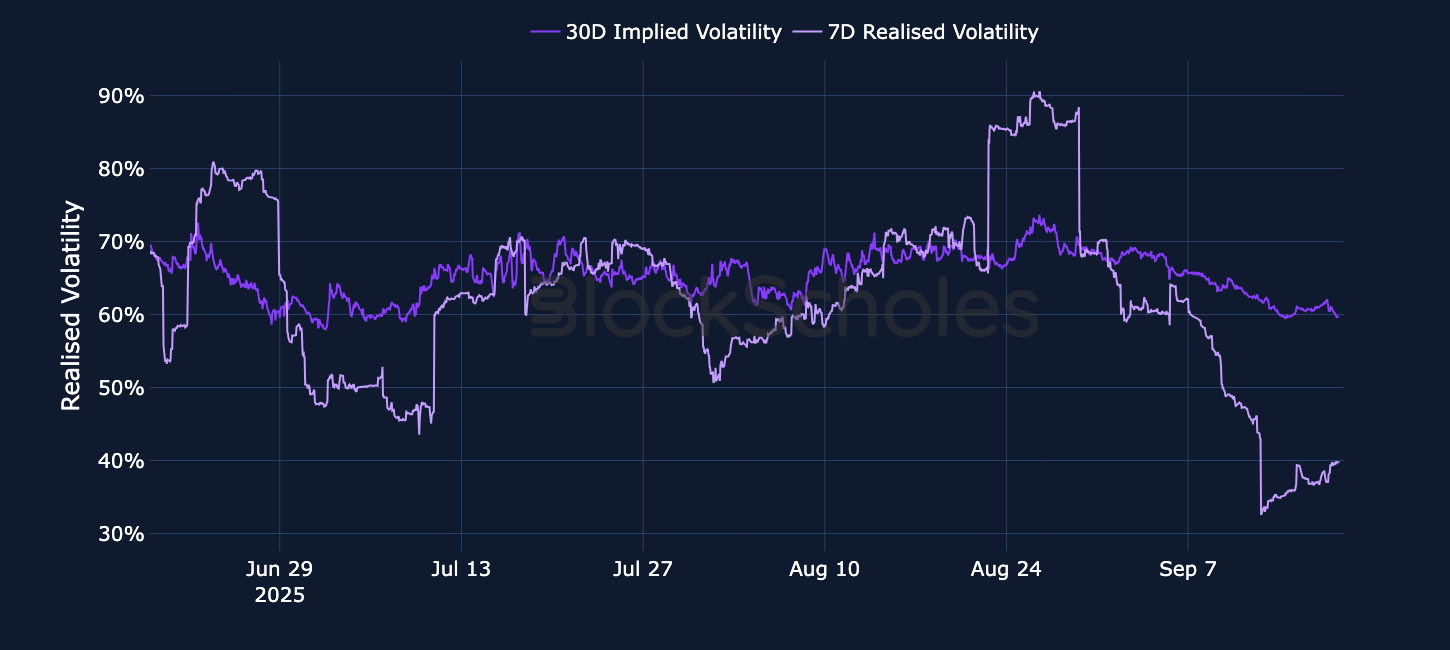

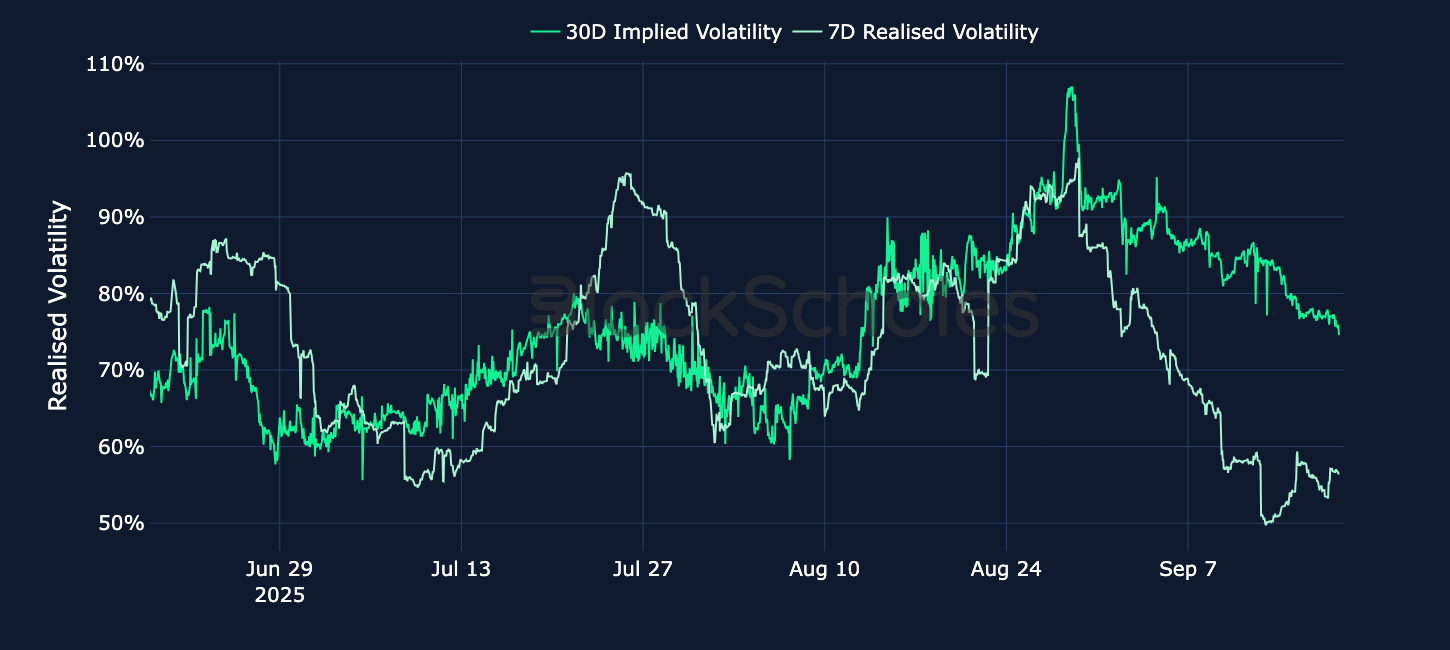

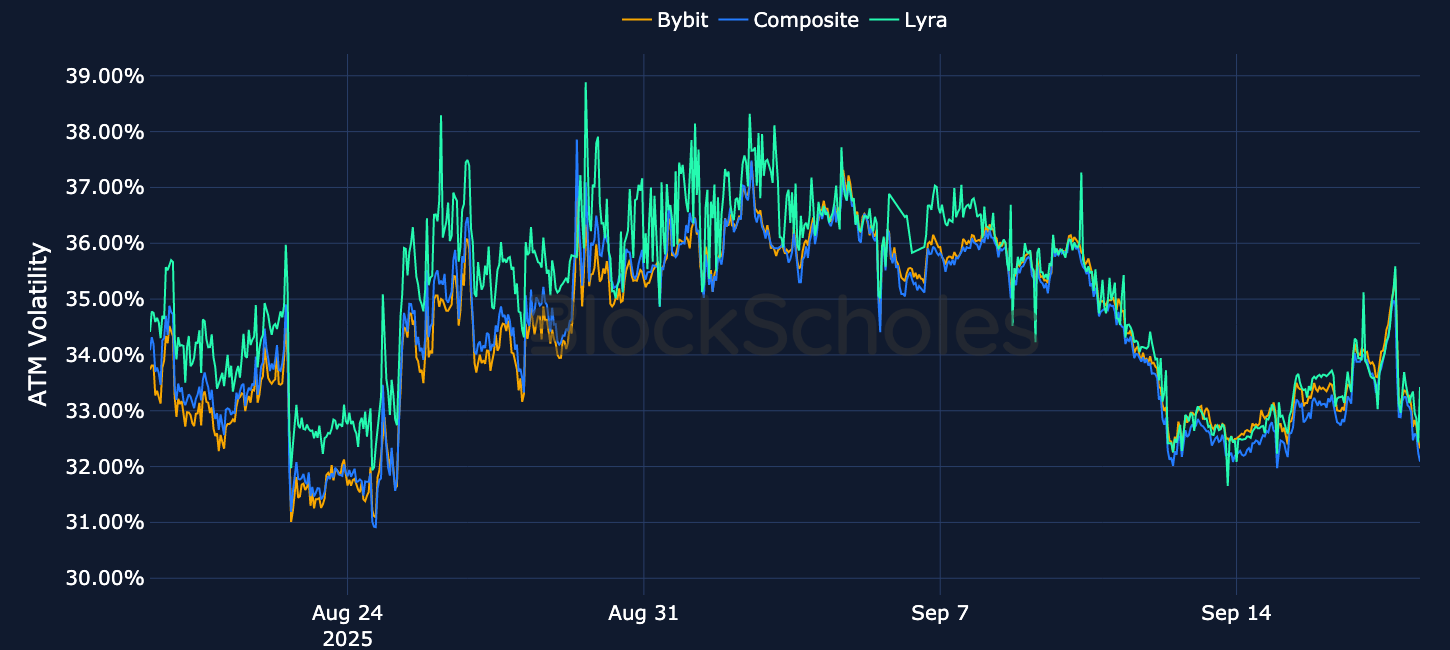

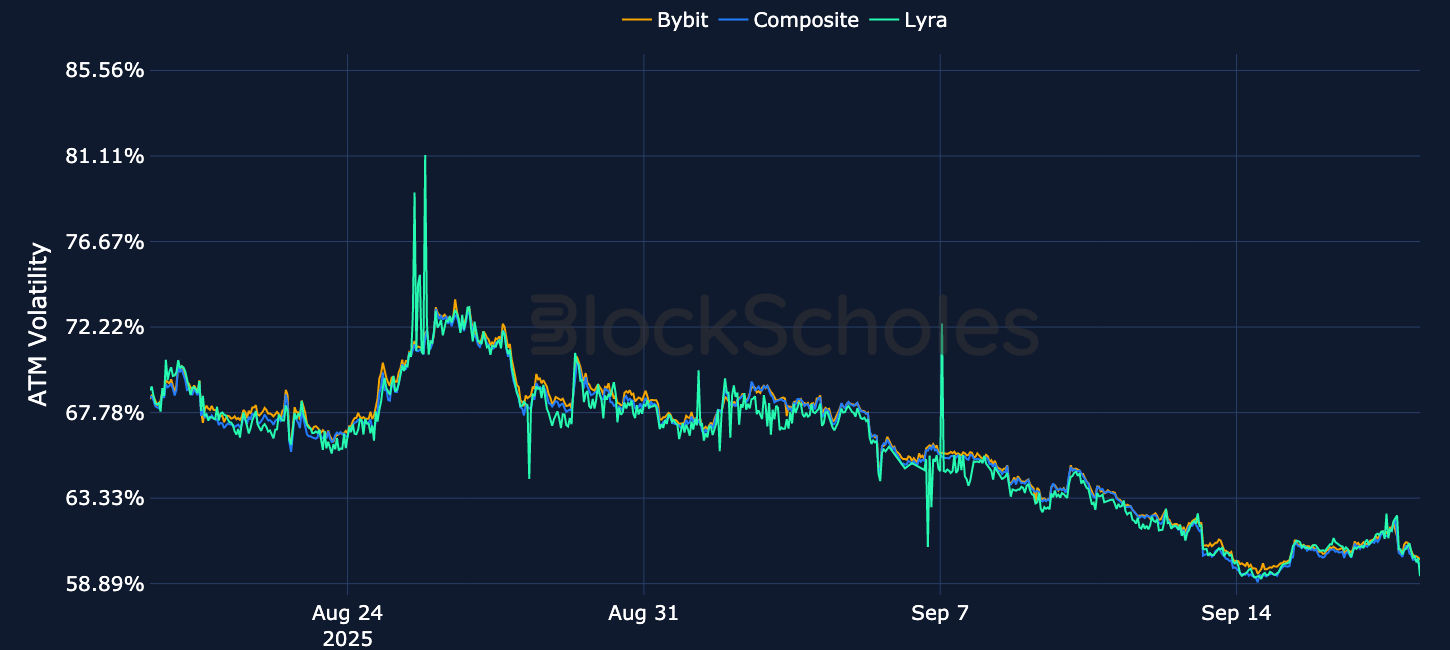

This week saw markets grapple with a pivotal FOMC meeting — not for the on-the-day interest rate cut decision, which was a near lock-in for a 25 bps cut, but for the likely path of monetary policy at the remaining two meetings in 2025. The whipsawing reaction to the release of contradictory signals resulted in significant intraday volatility, but options markets have been quick to return to a slow slog lower in implied volatility levels since then. This shouldn’t come as a surprise, given that realized volatility levels for BTC and ETH have fallen to extreme lows (close to 20% and 40%, respectively). In fact, what’s truly surprising is that implied volatility hasn’t fallen with them, instead trading at elevated levels (10 and 20 points higher, respectively).

This week saw markets grapple with a pivotal FOMC meeting — not for the on-the-day interest rate cut decision, which was a near lock-in for a 25 bps cut, but for the likely path of monetary policy at the remaining two meetings in 2025. The whipsawing reaction to the release of contradictory signals resulted in significant intraday volatility, but options markets have been quick to return to a slow slog lower in implied volatility levels since then. This shouldn’t come as a surprise, given that realized volatility levels for BTC and ETH have fallen to extreme lows (close to 20% and 40%, respectively). In fact, what’s truly surprising is that implied volatility hasn’t fallen with them, instead trading at elevated levels (10 and 20 points higher, respectively).

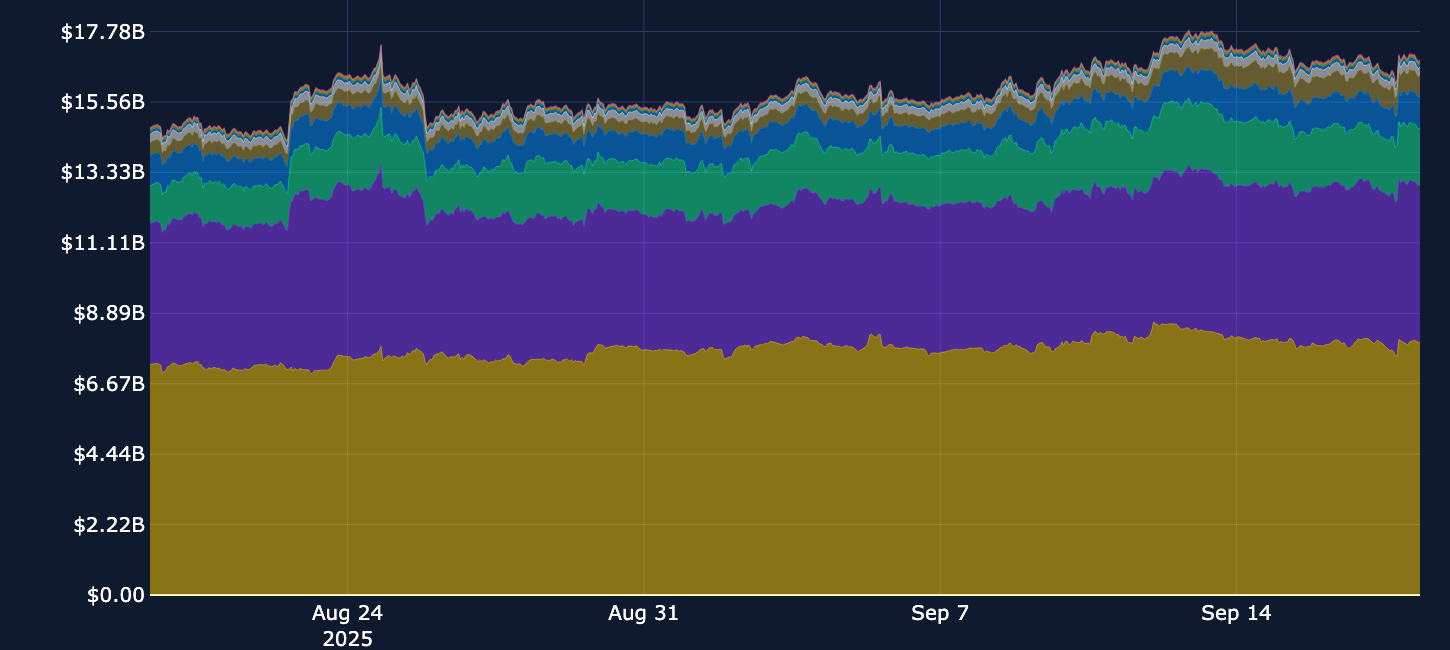

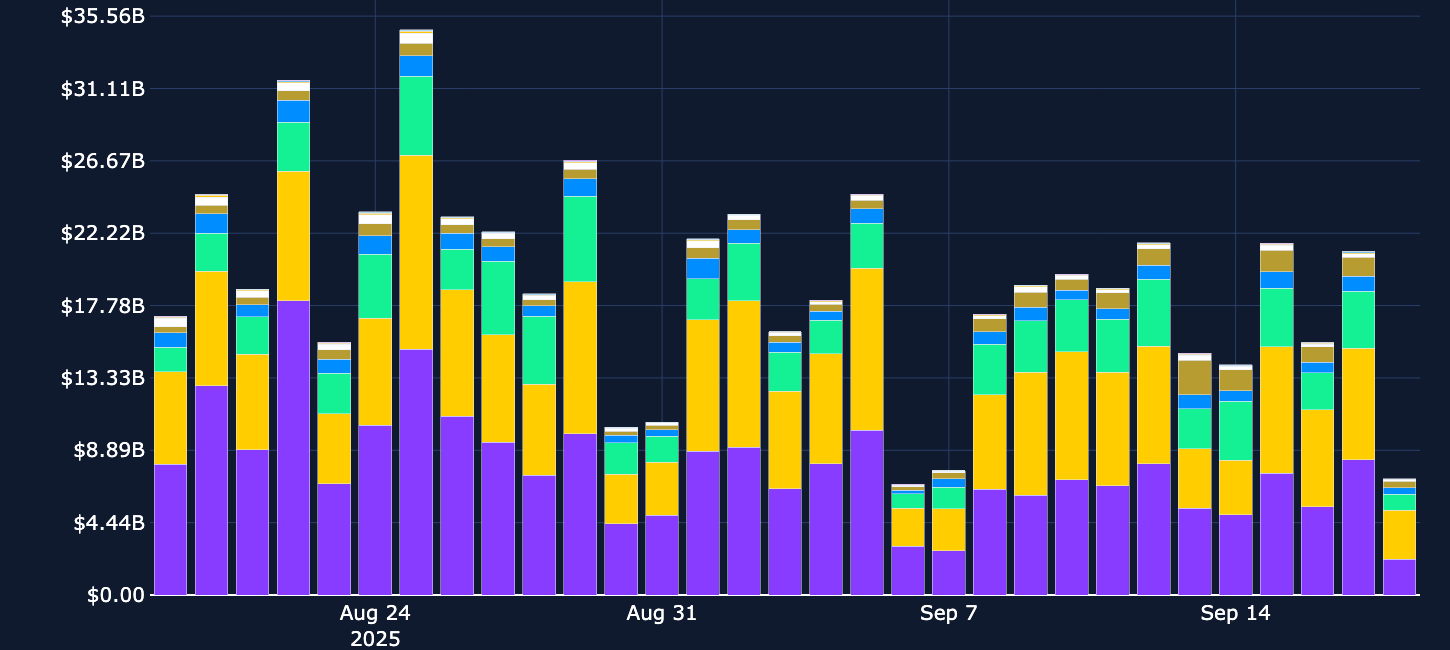

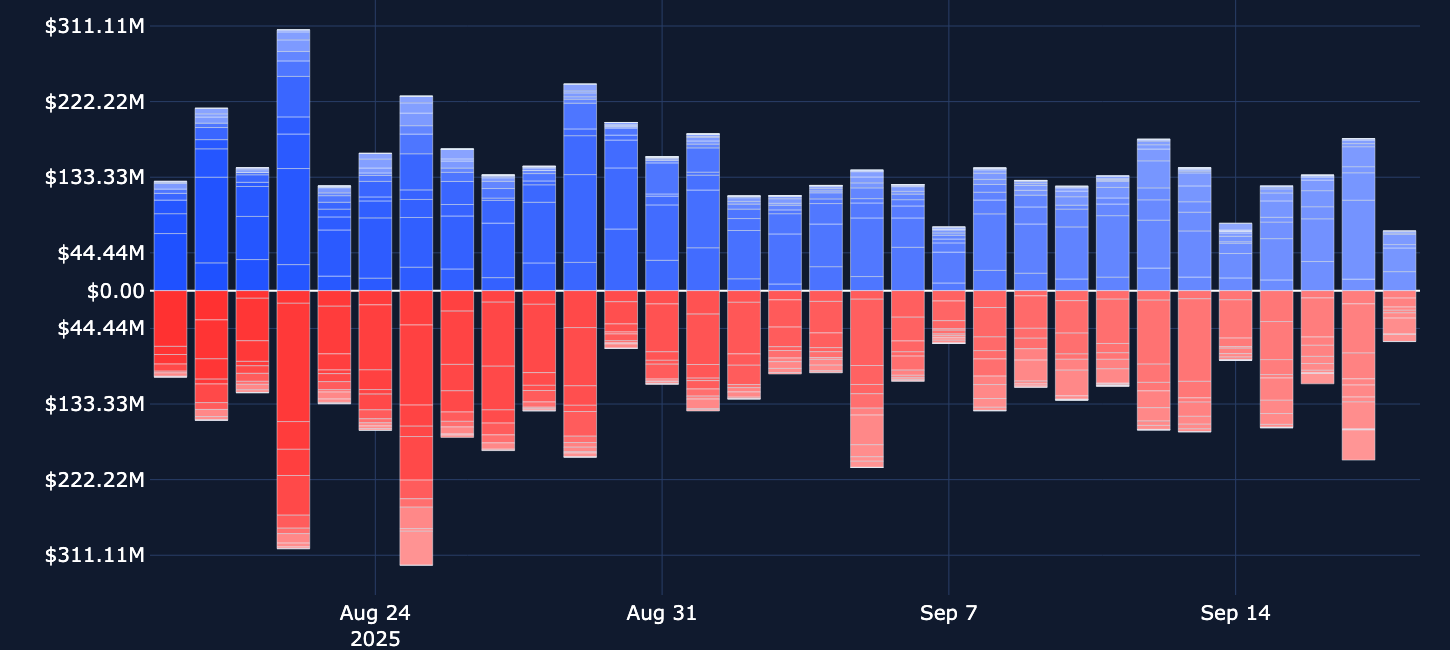

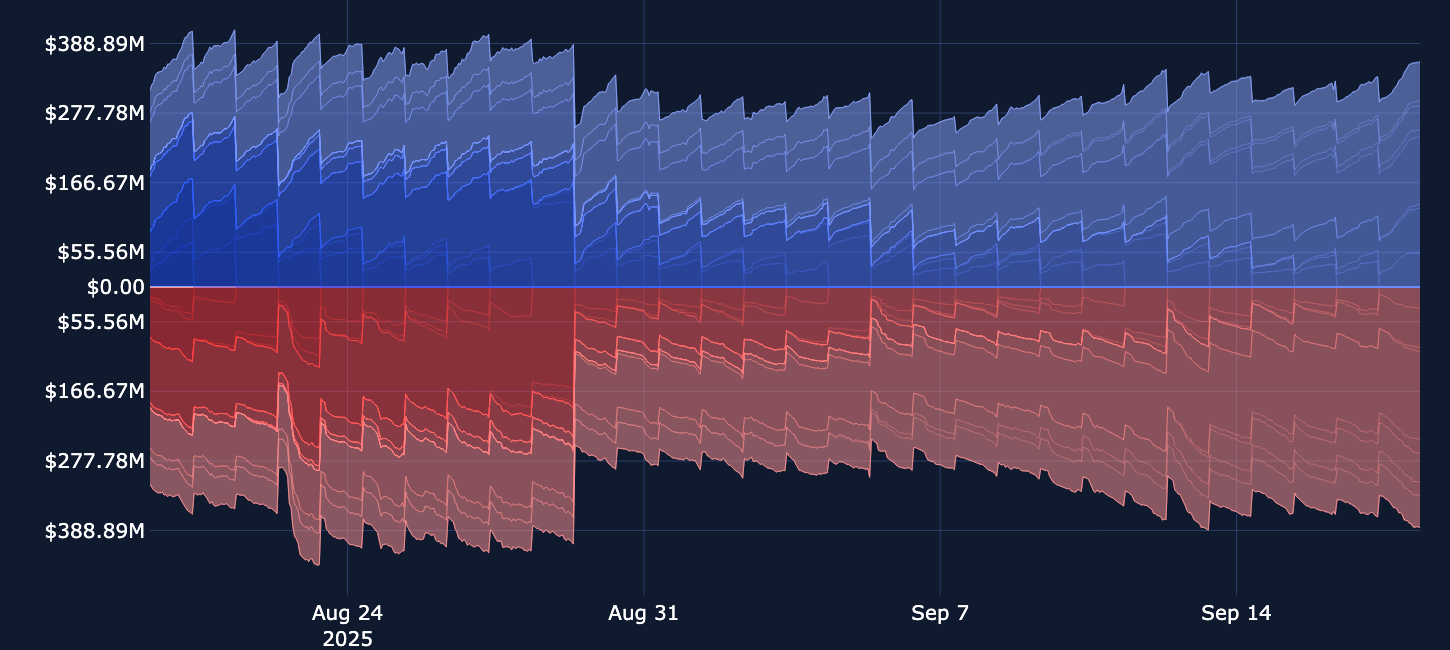

Perpetuals: Open interest remains close to all-time high levels.

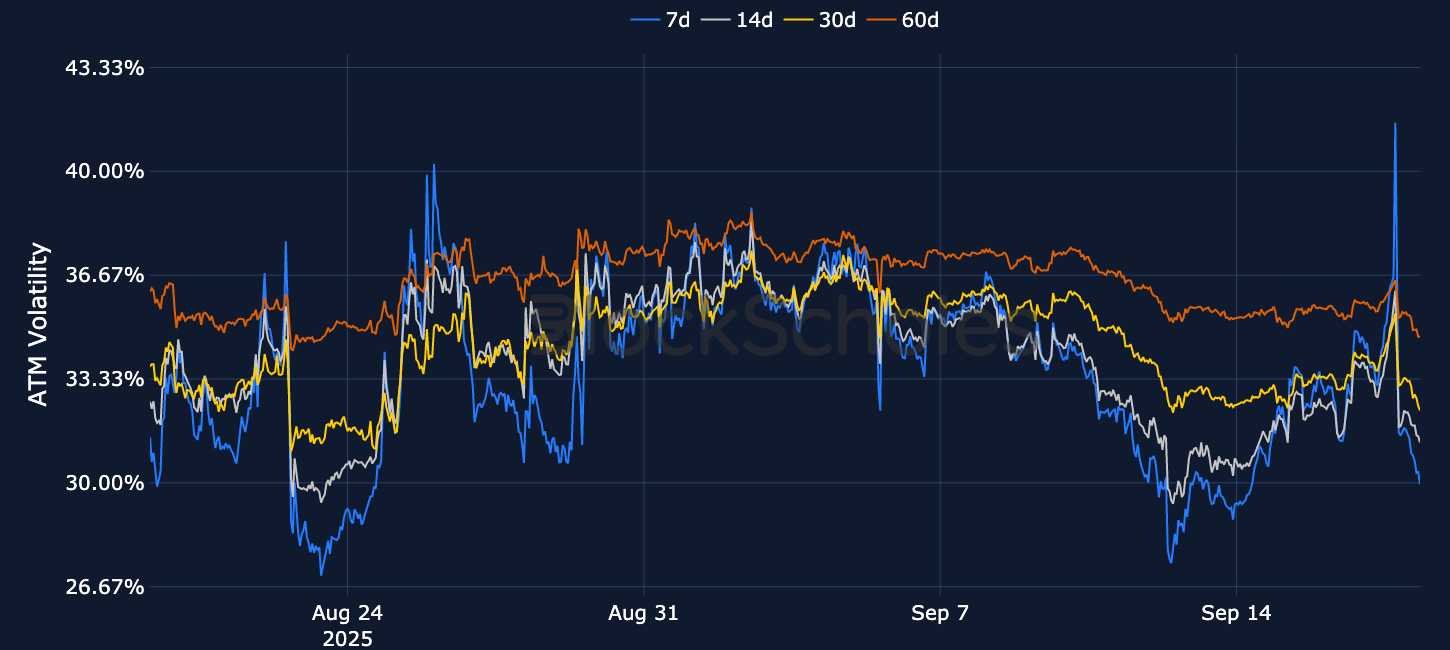

Options: Short-tenor implied volatility levels enjoyed an all-too-brief rally higher during the FOMC event, before resuming their grind lower in search of an even lower level of realized volatility.

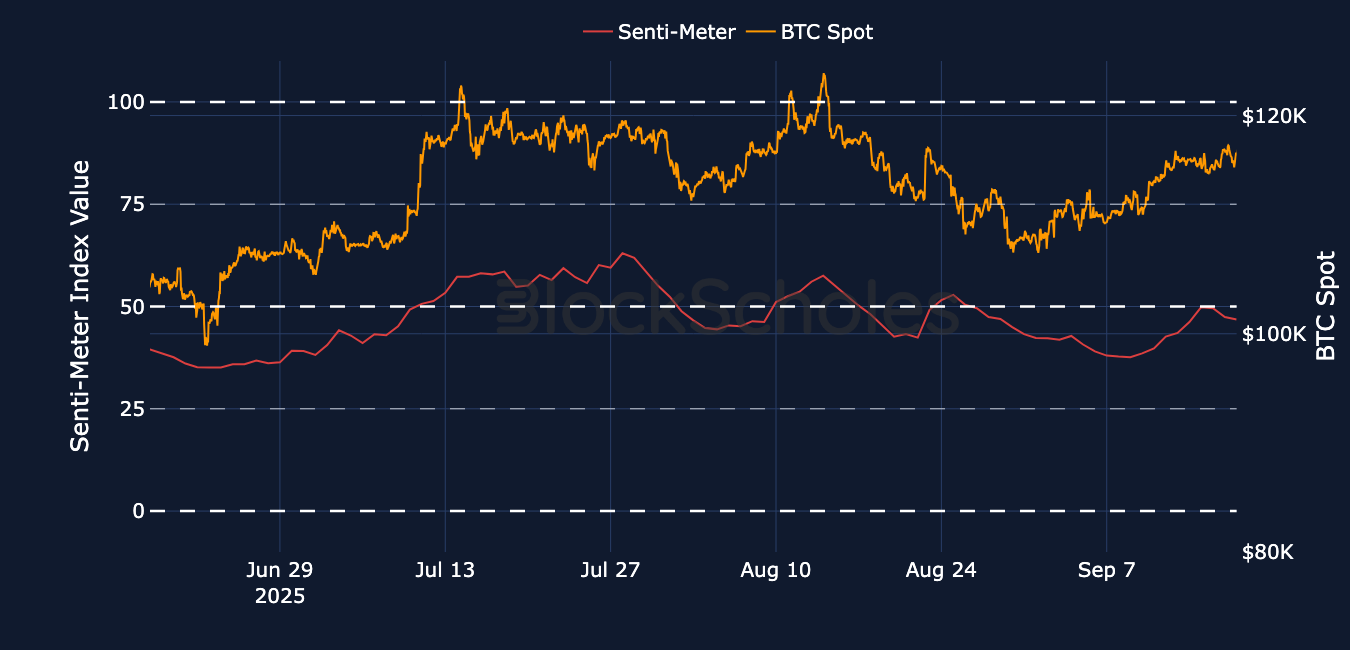

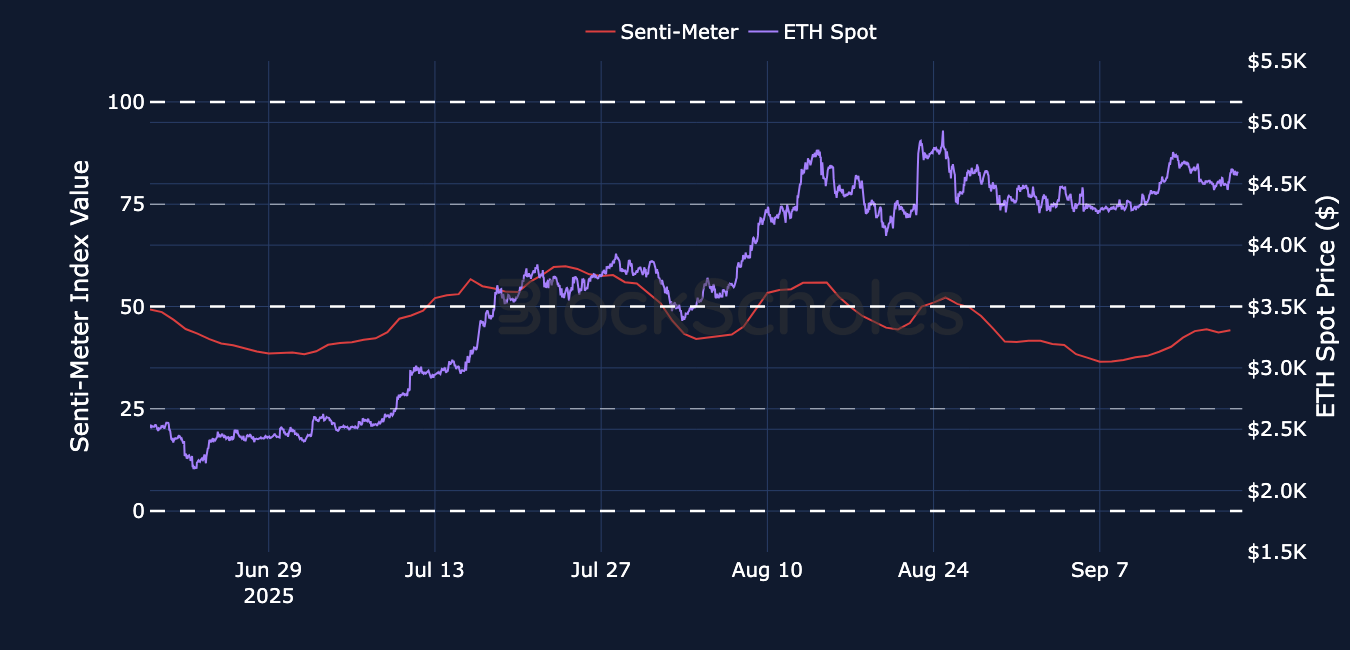

Block Scholes’s Senti-Meter Index aggregates the funding rate, future-implied yield and volatility smile skew into a single expression of sentiment in derivatives markets. See more in the methodology article here.

Galaxy Digital bought 1.2M SOL (worth around $306M) on Monday, Sep 15, 2025, bringing its total purchases over the past five days to around 6.5M SOL (worth around $1.55B). This follows its work with Multicoin Capital and Jump Crypto on a $1.65B private placement for the Forward Industries Solana treasury strategy.

On the same day, Helius Medical Technologies (Nasdaq: HSDT) raised over $500M to make SOL its primary reserve asset. The round was led by Pantera Capital and Summer Capital, with participation from Animoca Brands, FalconX, Arrington Capital and HashKey Capital.

Yesterday, FalconX withdrew 413,075 SOL (worth around $98M) from major exchanges. Removing this supply from the market decreased the number of tokens available for trading, a reduction in circulating supply that may have helped support SOL’s price immediately after the withdrawal.

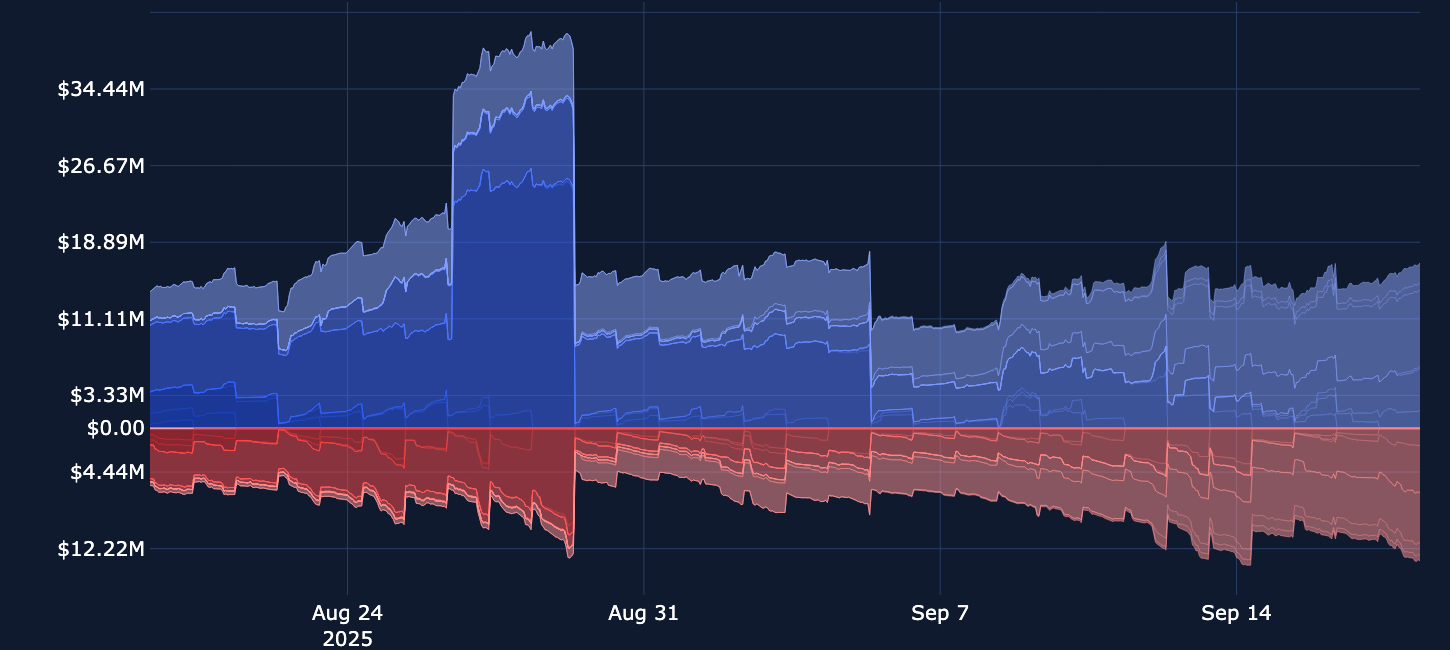

Perpetual swap open interest has remained just below all-time high levels throughout the buildup and resolution of the FOMC meeting on Wednesday, Sep 18, 2025. While volumes across the tracked tokens have been lower in the first two weeks of September than they were at the end of August, SOL has enjoyed a far higher level of daily trade volumes than at the end of August.

SOL’s extra volumes explain at least part of the volatility in the funding rates for its perpetuals, indicating that while SOL’s outperformance in the past week has returned its spot price to levels last seen in February 2025, the path higher hasn’t been clear and straightforward. This data suggests signs of profit-taking and fading the rally along the path upward.

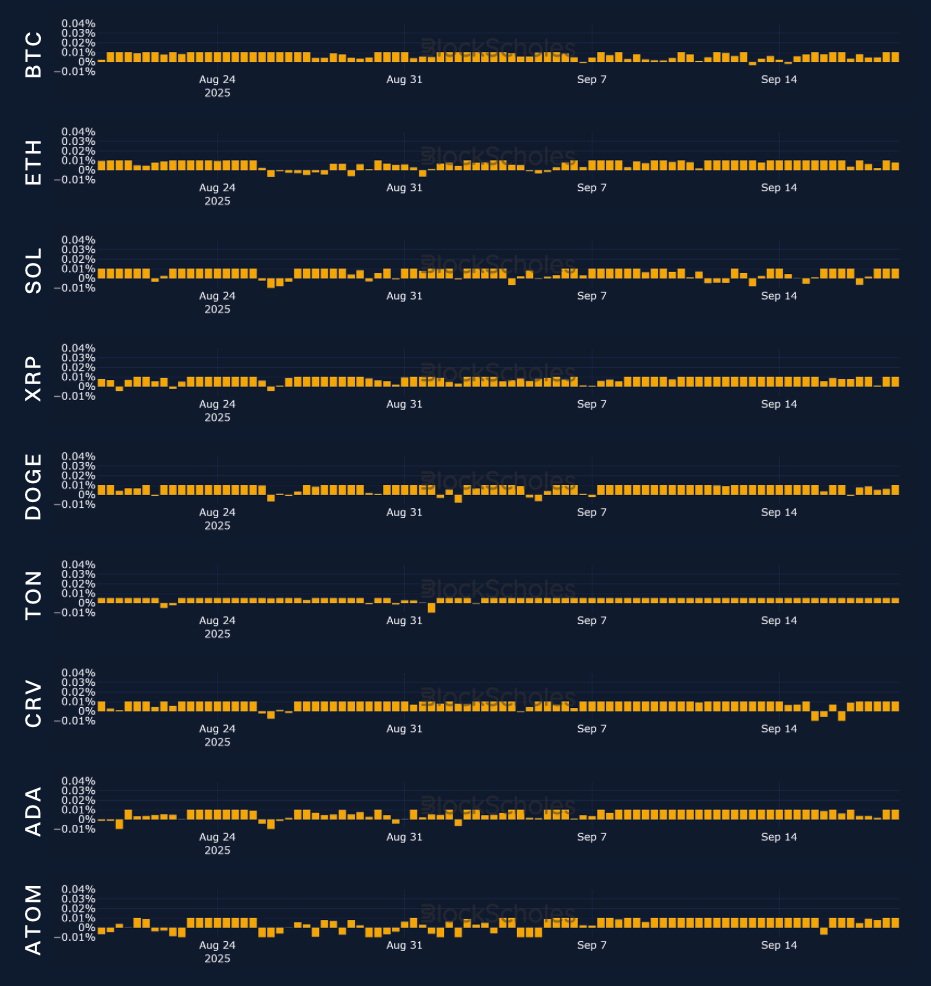

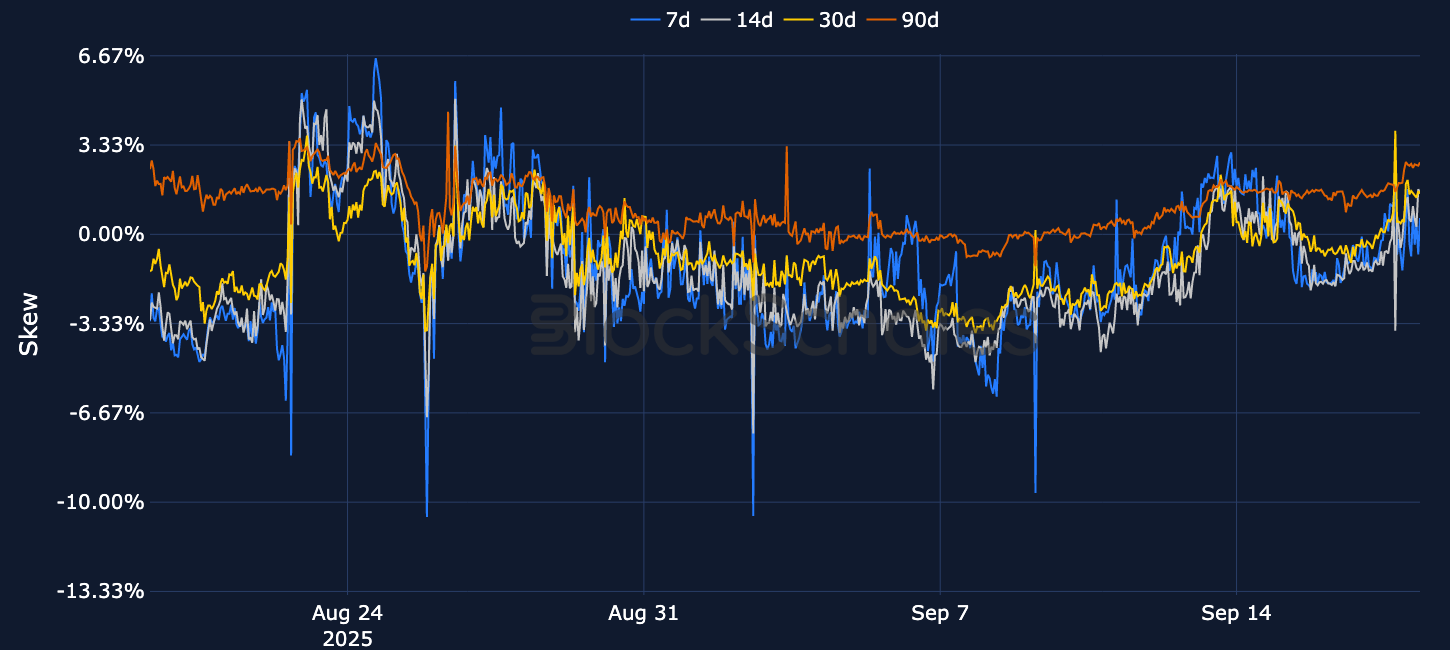

Funding rates for almost all coins tracked have refused to price for the same bearishness as options markets, as they have done throughout much of the same market conditions since late August. This has led to an interesting dislocation between the skew of volatility smiles toward puts (an ostensibly bearish sign), and to the willingness by perpetual swaps traders to pay for long exposure. SOL is a notable exception to the consistency in other tokens: While its spot price has outperformed that of other tokens over the past week, it has frequently reported traders willing to pay a premium in order to take short exposure against further rallies higher.

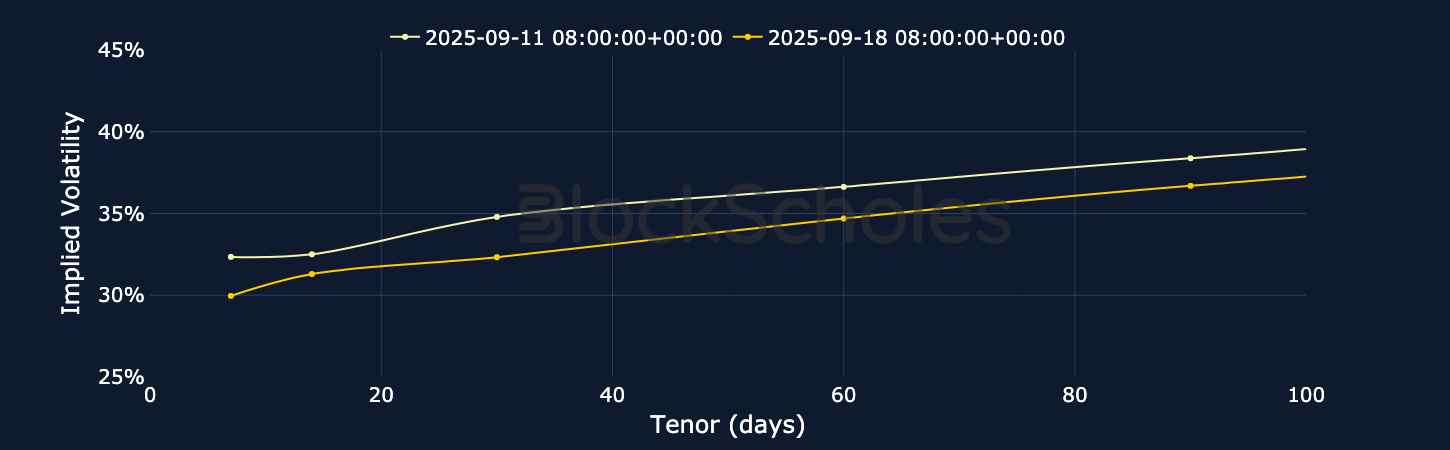

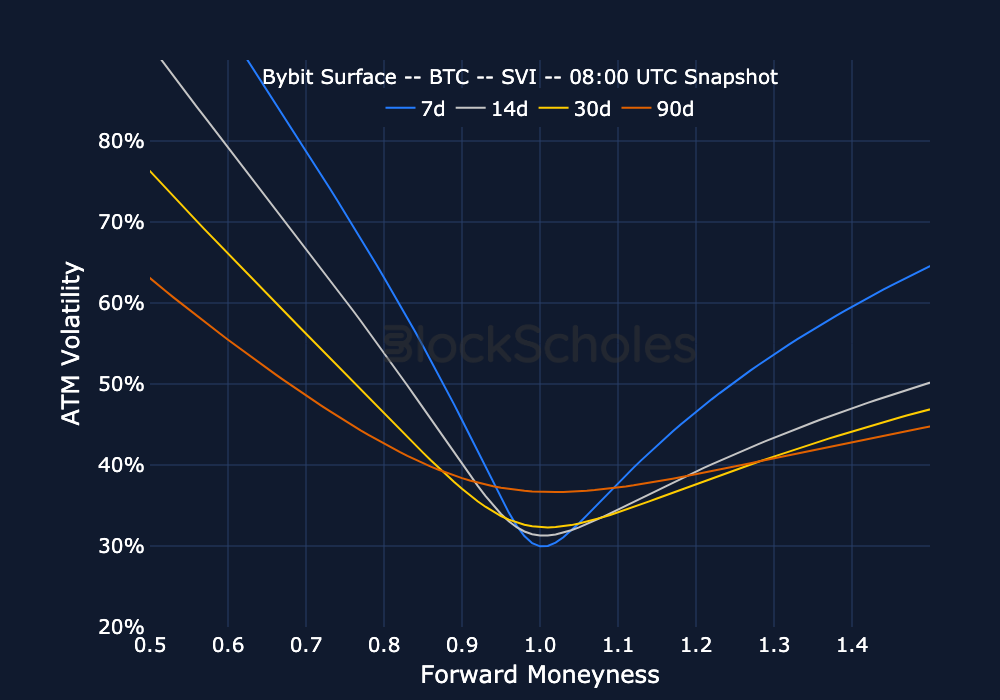

The FOMC meeting caused the first inversion in BTC’s term structure of volatility since Trump’s erratic tariff announcements earlier this year. The low level of options volumes during the event suggests that the spike occurred during a period of relatively low liquidity, which may have acted to push pricing higher during the temporary panic that followed the release of the FOMC’s decision (ahead of Chair Powell’s subsequent press conference).

In the aftermath, realized volatility has cratered to historically low levels at just 20% and, despite moving lower itself, has resulted in a sizeable spread to the level of implied volatility at tenors longer than 30 days.

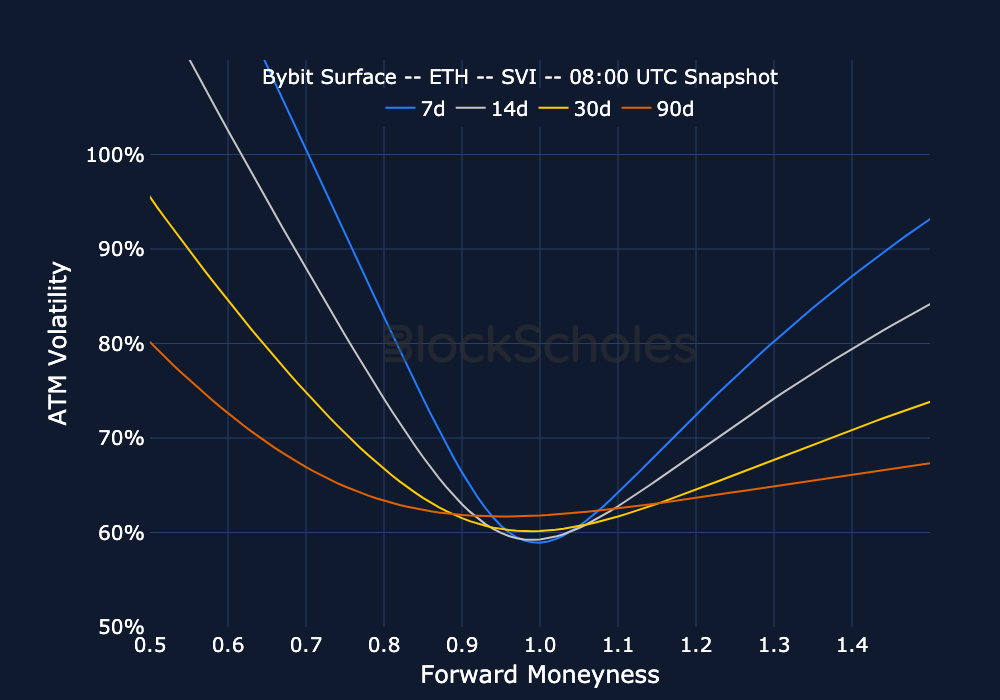

Among the three major cryptocurrencies that enjoy liquid options markets, ETH had the standout reaction to the FOMC meeting. A slew of contradictory signals — such as the surprising lack of dissent from the 25 bps rate cut decision by Governors Waller and Bowman, and the expectation among governors that inflation would remain above the Fed’s goal of 2% well into 2026 — saw short-tenor implied volatility levels spike to invert the term structure. The ultimate resolution of options markets after the event was to price out much of the bearish skew toward puts that had dominated since the end of August. Open interest levels remained largely unchanged by the event, and volumes didn’t spike in line with volatility pricing, suggesting that this was a short-lived event.

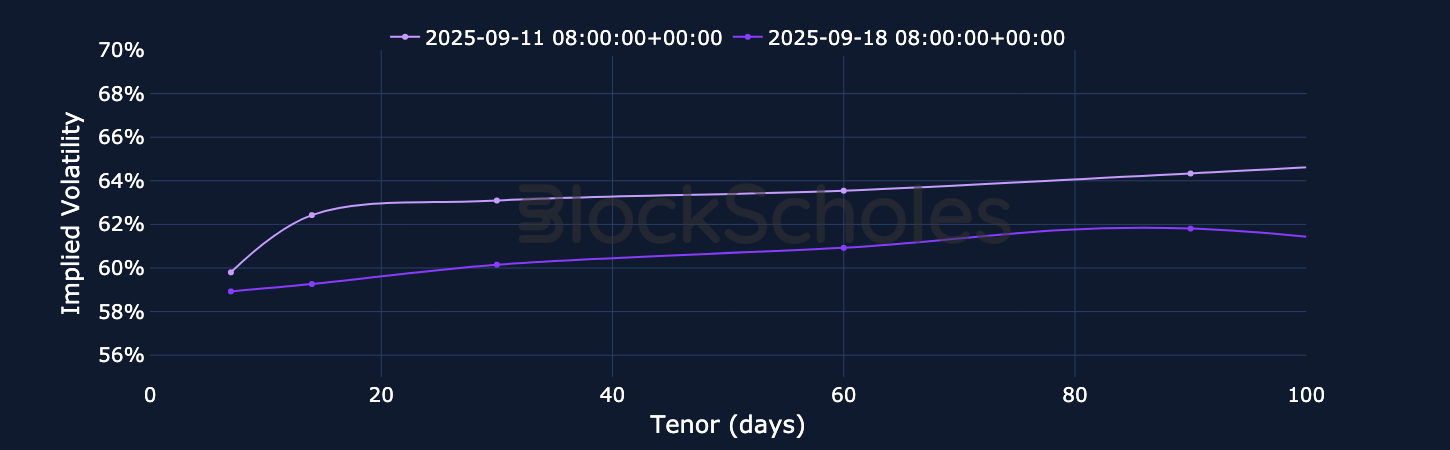

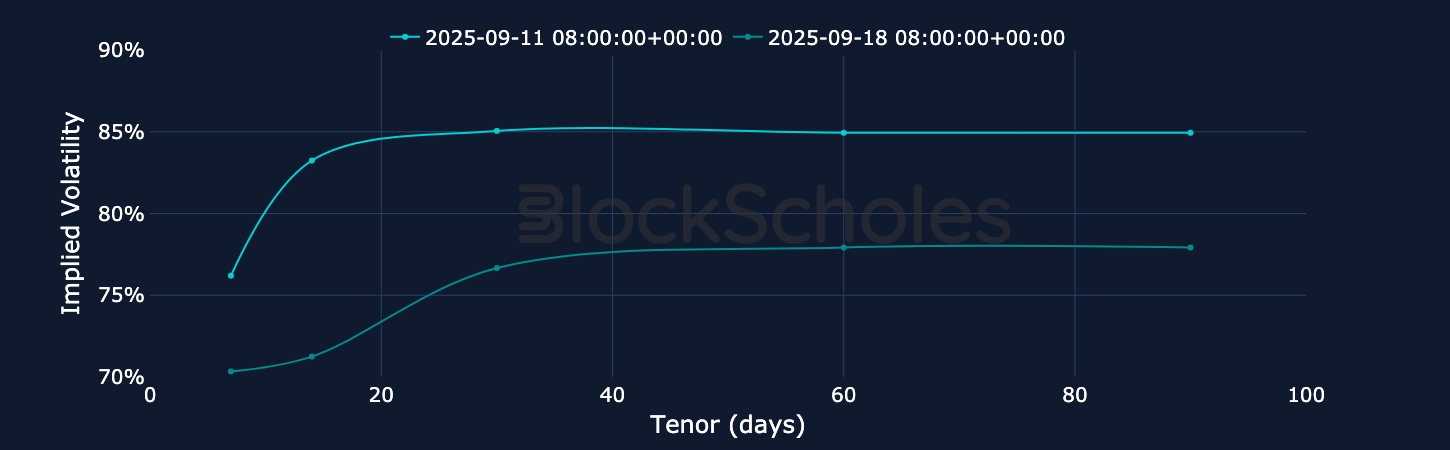

The decline in ATM implied volatility across SOL’s term structure mirrors a major drop in SOL’s realized volatility. SOL’s ATM implied volatility, which spiked to 104% on August 29, has since fallen, and now sits almost level with ETH’s — but at the 30-day tenor, implied volatility still trades roughly 20 percentage points above realized volatility.

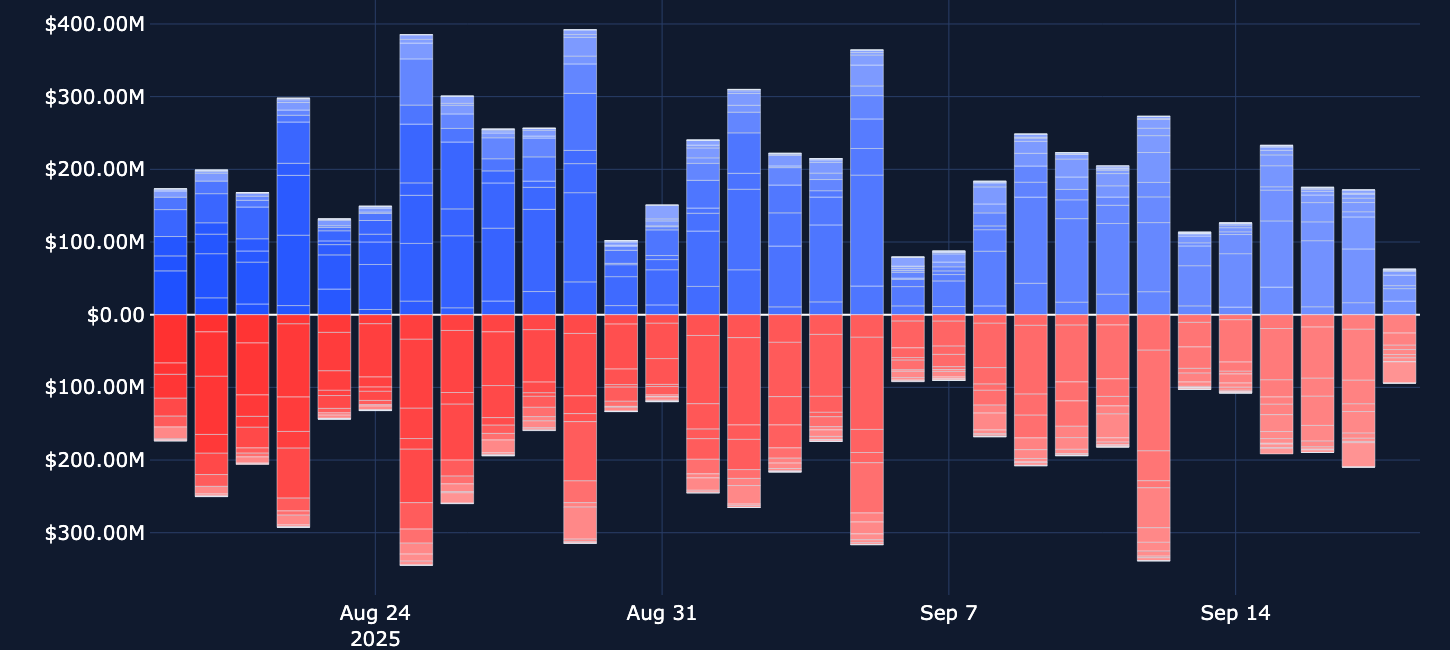

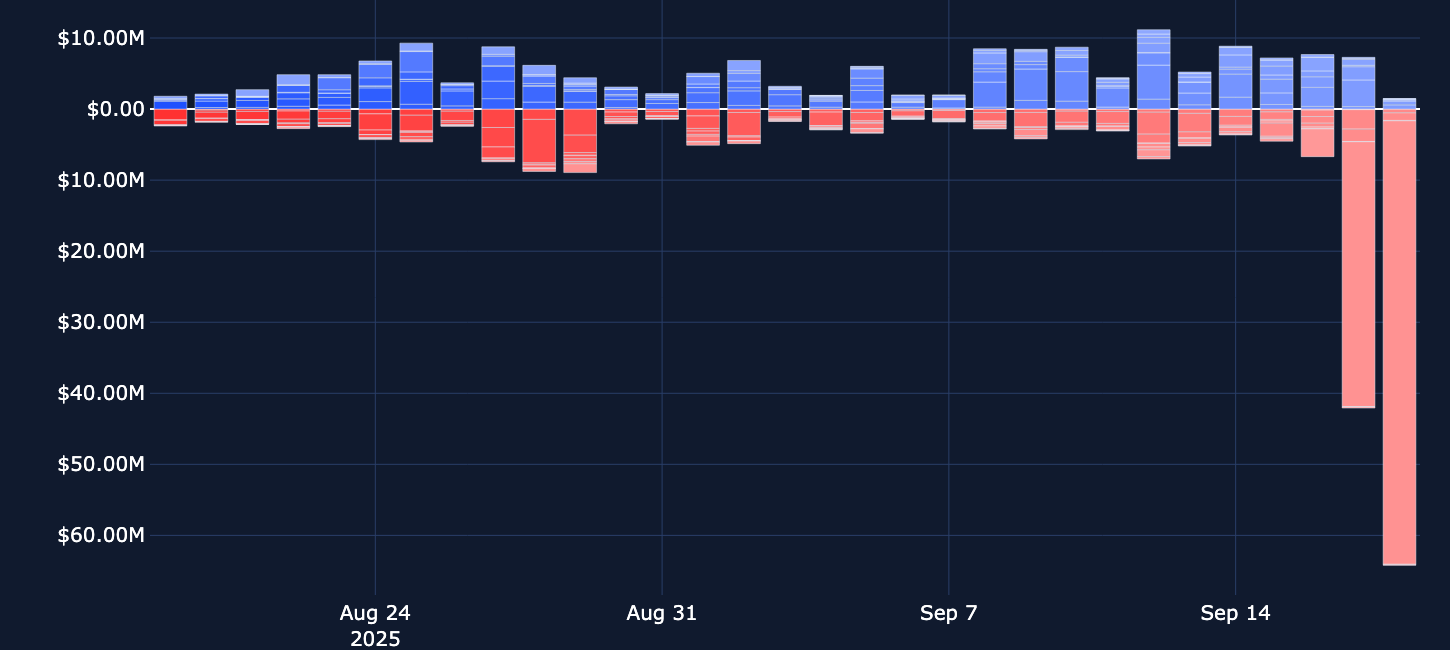

SOL’s put option volumes reached $40M yesterday (Sep 17, 2025). This exceeds the $60M recorded today (September 18), and was concentrated in longer-dated expirations. This surge coincides with large institutional activity, such as Galaxy Digital’s accumulation of SOL and FalconX’s exchange withdrawals. Call option volumes over the same period were much smaller (at just $1M), indicating that trading activity has been far heavier in downside protection than in upside participation.

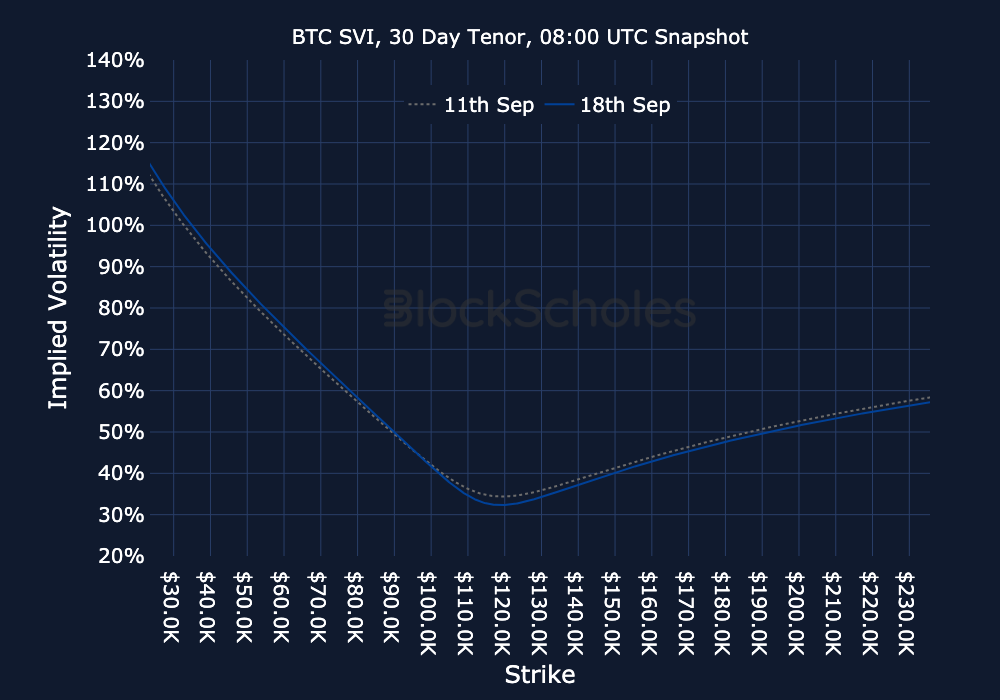

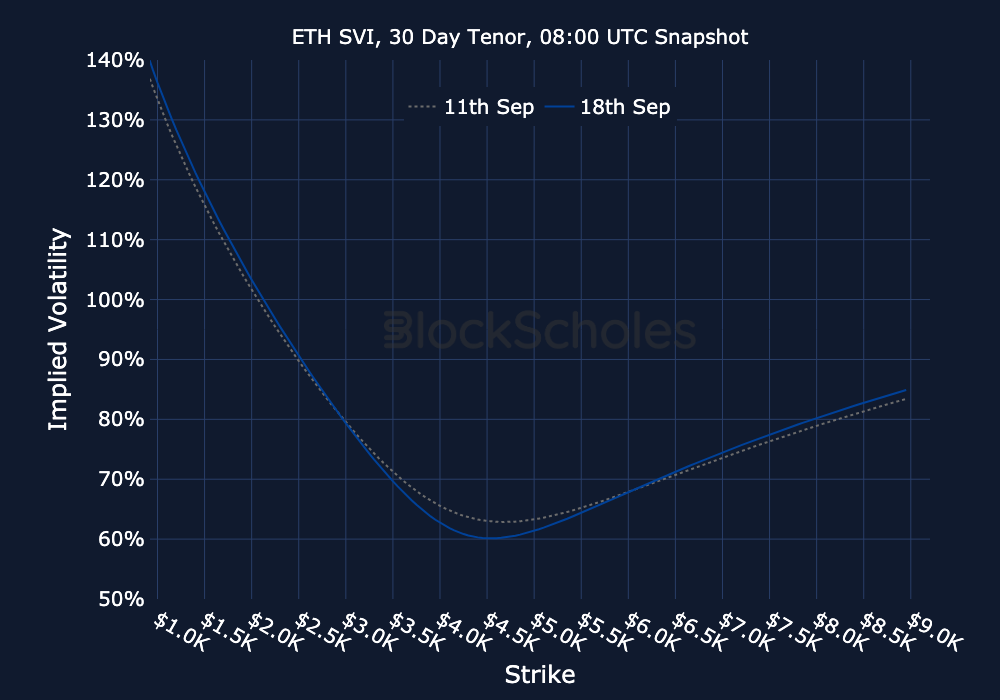

Ahead of the FOMC meeting on Sep 18, 2025, markets had priced in a bearish skew toward OTM puts across the term structure for BTC (−3.33%) and ETH (−1.9%). Despite a confusing whiplash in spot prices as markets digested the slew of information while it was released, the skew toward puts was ultimately priced out in favor of neutrality.

Although this is a stark divergence from the bearish positioning that had dominated the market since the end of August, it doesn’t yet mark a recovery to the exuberant bullish sentiment we saw earlier in the year. This is unusual, as ETF products for both coins have recorded extreme levels of bullish inflows over the past 7–10 days.

Open interest and trading volume data are sourced “as is” from the Bybit exchange platform API exclusively, and as such do not represent a comprehensive picture of the sum of trading activity across all derivatives markets or exchanges. The data visualized in this report consists of hourly and daily snapshots, recorded over the previous 30 days. Daily (hourly) snapshots of trade volume record the total sum of the notional value of trades recorded in the 24H (1 hour) period, beginning with the snapshot timestamp.

If not explicitly labeled as derived from another exchange, the input instrument prices to all derivatives analytics metrics in this report are sourced from the appropriate endpoints of Bybit’s public exchange platform API. In the event that data is labeled or referred to as representing the market on another exchange source, that data is sourced from the appropriate endpoint of each respective exchange’s public API.

Macroeconomic charts and data are sourced “as is” from the Bloomberg Terminal. Exchange data is sourced “as is” from publicly available exchange APIs. Block Scholes makes no claims about the veracity of public third-party data.

After acquisition of underlying-denominated raw data for open interest and trading volume on the Bybit exchange platform from Bybit’s API endpoint, equivalent dollar-denominated figures are calculated using the concurrent value of Block Scholes’s Spot Index for the relevant underlying asset.

Block Scholes’s Spot Index represents the aggregate Spot mid-price for a given currency across the top five CEXs by volume (with USD-quoted markets). It considers the proportion of total volume in the instrument on the exchange, as well as the deviation of a data point from those on other exchanges.

Futures prices are used for Block Scholes’s futures-implied yields calculation services in order to derive the constant-tenor annualized yields displayed in the Futures section of this report.

Options prices are used for Block Scholes’s implied volatility calculation services in order to calibrate volatility surfaces, from which all derivatives volatility analytics displayed in the BTC Options and ETH Options sections of this report are calculated. Volatility smiles are constructed by calibrating to mid-market prices observed in Bybit options markets. As part of the calibration process, prices go through rigorous filtration and cleaning steps, which ensures that the resulting volatility surface is arbitrage-free and has exceptional fit to the market observables.

.jpg)

.jpg)