Andrew Melville

Head of Research

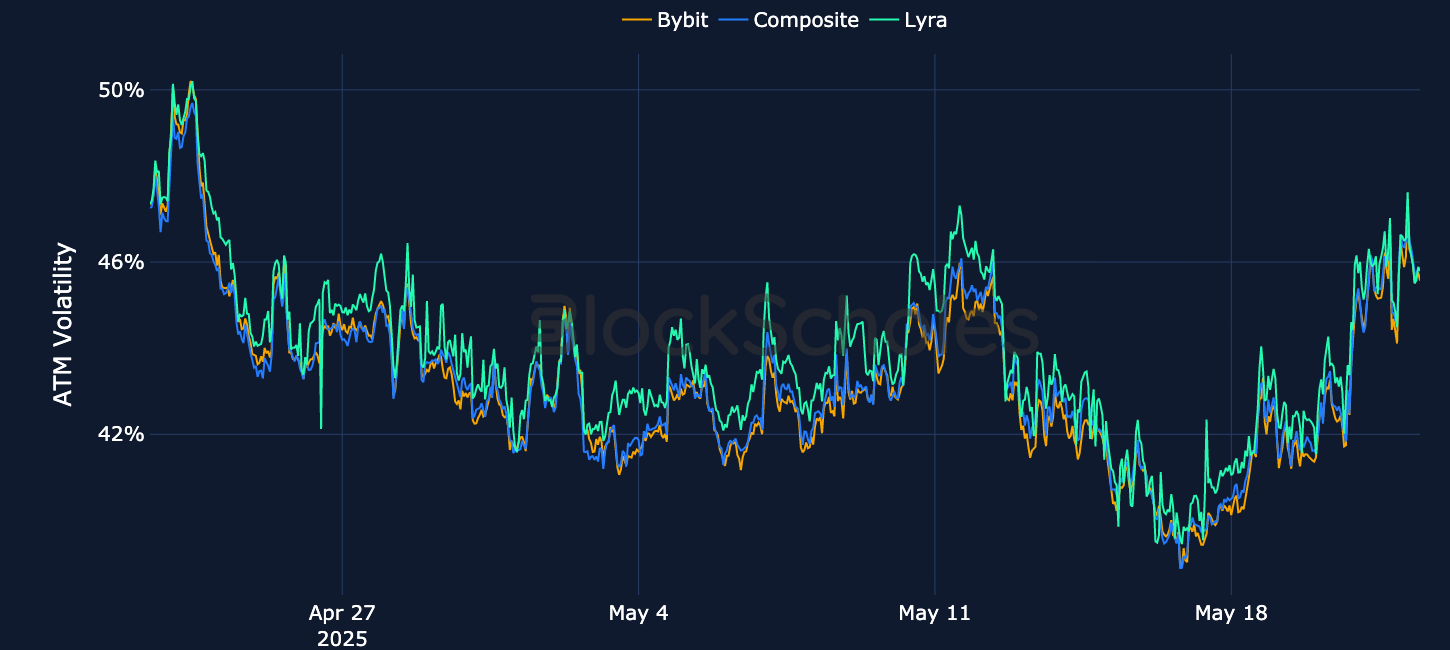

Front-end volatility for BTC has been reactive to the whipsaw in spot price over the past week, which has more recently resulted in BTC reaching a new all-time high (ATH) of $$111.97K – the first new ATH since January 20, 2025, four months ago. At-the-money implied volatility levels remain between 45% and 50%, as short-tenor volatility expectations have now picked up significantly from their lows of last week. Perpetual funding rates remain tempered despite a spot price that has reached new highs, although options skew temporarily steepened towards calls by as much as 7%, due to renewed demand for OTM calls.

Front-end volatility for BTC has been reactive to the whipsaw in spot price over the past week, which has more recently resulted in BTC reaching a new all-time high (ATH) of $$111.97K – the first new ATH since January 20, 2025, four months ago. At-the-money implied volatility levels remain between 45% and 50%, as short-tenor volatility expectations have now picked up significantly from their lows of last week. Perpetual funding rates remain tempered despite a spot price that has reached new highs, although options skew temporarily steepened towards calls by as much as 7%, due to renewed demand for OTM calls.

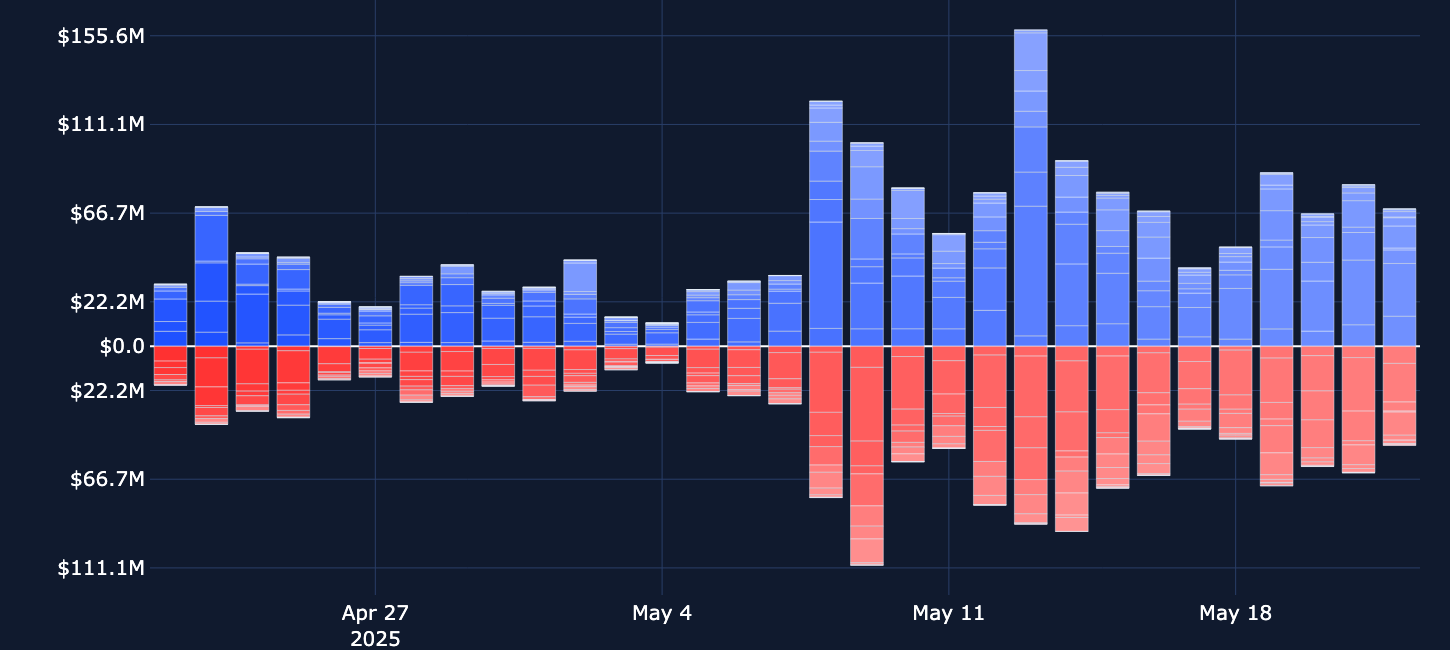

Perpetuals: Open interest in perpetual swaps reached a new high for May this week, exceeding $11B, as May has so far exhibited a stronger risk-on sentiment than April.

Options: ETH short-tenor options maintain their volatility premium relative to longer-tenor options and ETH skew still shows firm support for OTM calls despite a slowdown in ETH’s spot price increase, relative to last week when it surged by more than 50%.

Block Scholes’s Senti-Meter Index aggregates the funding rate, future-implied yield and volatility smile skew into a single expression of sentiment in derivatives markets. See more in the methodology article here.

After staying mostly flat for the first half of this past week, open interest for ETH has recently begun to tick up again. That increase in open interest coincides with BTC reaching and then exceeding its January ATH (now trading at $111K), which has brought the rest of the crypto spot market up, including Ether (+4.5% today). However, the increase in open interest comes at a slightly shallower gradient compared to last week, when ETH spot price had surged 50%. Total open interest and perpetuals trading volume across the nine tracked tokens rose to a new high for the month, upwards of $11B and $26B, respectively, as BTC flirted with new all-time highs. Perp volumes exceeded $20B on May 19, 2025, the first US equities trading session following credit agency Moody’s downgrading US debt. BTC, as with risk-on US equities, fell following the news, though it quickly recovered those intraday losses.

Neither BTC spot price’s whipsaw between $101K and $108K nor its sudden breakout past $111K has failed to translate into a similar movement in funding rates. For most of the past seven days, leveraged long traders have shown a willingness to pay a premium to shorts, as funding rates have mostly been positive. However, despite reaching a new ATH for the first time in four months, perpetual funding rates still exhibit a more tame and measured sentiment, failing to break past 0.01% not just this week, but for all of May so far. The same however, cannot be said for other measures of directional sentiment in derivatives markets for BTC. Call-skew, for example, shows topside demand for OTM calls. ETH funding rates began the week intermittently negative, though they have spiked in line with short bursts in spot.

.png)

Mid-May volatility expectations had been on the decline as BTC spot price mostly traded sideways between $102K and $104K. More recently, however, that range extended to $108K following the tariff détente between the US and China – even then, other macro uncertainties such as the downgrade of US treasuries temporarily placed a lid on a full spot breakout. That did not last long as advances on the regulatory front helped BTC reach escape velocity as it blew past $110K. That tug-of-war between different drivers has resulted in a reactive front-end volatility to spot moves, as outright implied volatility levels currently remain between 45% and 50% for BTC. Options volumes are still lopsided towards puts, despite a spot price that entered price discovery, and open interest equally remains dominated in puts by $200M.

After two consecutive weeks of ETH outperformance, something that has largely been lacking for most of this crypto cycle, ETH now once again takes a backseat to BTC. While its one-month returns have clocked in at an astounding 69%, ETH is up a lower amount over the past seven days (a move largely attributed to the most recent rally in BTC, which has dragged the rest of the market with it). The inversion in its term structure of volatility has not yet abated, and short tenors maintain a volatility premium relative to longer tenors. ETH put-call skew is also now significantly less bullish than levels only one week ago, though it still maintains a 5% skew for OTM calls. The dominance of call options in both volumes and open interest for ETH has narrowed significantly this week, with open interest in calls only $30M greater than in puts.

Positive developments in regulation, following years of regulatory targeting on the crypto industry, have provided the catalyst for the most recent leg up for BTC and altcoins. As BTC surpassed its January highs, SOL has benefited from the wider risk-on appetite among traders. Currently, it is up 5% over the past seven days, with its 30-day performance exceeding 31%. Open interest for SOL is greater in calls than in puts by $1.5M, and its term structure of volatility is now firmly inverted due to an 8 percentage point lift in front-end volatility compared to last week.

As BTC surpasses its all-time high of $109K, derivatives markets see renewed optimism. The skew of BTC volatility smiles has steepened significantly, as OTM calls trade at a higher implied volatility compared to puts across all tenors, with the one-week tenor put-call skew briefly exceeding 7% before coming back down. The whipsawing spot price action over the past week and subsequent surge to new highs has resulted in a small elevation of implied volatility across BTC’s term structure, which is now at 47% at the front-end. After a strong catch-up rally in spot price last week and a smaller rally this week in line with BTC, ETH derivatives markets also show a strong preference towards calls, as OTM calls trade with a 5% premium relative to puts.

Open interest and trading volume data are sourced “as is” from the Bybit exchange platform API exclusively, and as such do not represent a comprehensive picture of the sum of trading activity across all derivatives markets or exchanges. The data visualized in this report consists of hourly and daily snapshots, recorded over the previous 30 days. Daily (hourly) snapshots of trade volume record the total sum of the notional value of trades recorded in the 24H (1 hour) period, beginning with the snapshot timestamp.

If not explicitly labeled as derived from another exchange, the input instrument prices to all derivatives analytics metrics in this report are sourced from the appropriate endpoints of Bybit’s public exchange platform API. In the event that data is labeled or referred to as representing the market on another exchange source, that data is sourced from the appropriate endpoint of each respective exchange’s public API.

Macroeconomic charts and data are sourced “as is” from the Bloomberg Terminal. Exchange data is sourced “as is” from publicly available exchange APIs. Block Scholes makes no claims about the veracity of public third-party data.

After acquisition of underlying-denominated raw data for open interest and trading volume on the Bybit exchange platform from Bybit’s API endpoint, equivalent dollar-denominated figures are calculated using the concurrent value of Block Scholes’s Spot Index for the relevant underlying asset.

Block Scholes’s Spot Index represents the aggregate Spot mid-price for a given currency across the top five CEXs by volume (with USD-quoted markets). It considers the proportion of total volume in the instrument on the exchange, as well as the deviation of a data point from those on other exchanges.

Futures prices are used for Block Scholes’s futures-implied yields calculation services in order to derive the constant-tenor annualized yields displayed in the Futures section of this report.

Options prices are used for Block Scholes’s implied volatility calculation services in order to calibrate volatility surfaces, from which all derivatives volatility analytics displayed in the BTC Options and ETH Options sections of this report are calculated. Volatility smiles are constructed by calibrating to mid-market prices observed in Bybit options markets. As part of the calibration process, prices go through rigorous filtration and cleaning steps, which ensures that the resulting volatility surface is arbitrage-free and has exceptional fit to the market observables.

.jpg)

.jpg)