Andrew Melville

Head of Research

Cryptocurrency spot prices began their sell-off last Thursday on Aug 14, 2025 following a stronger-than-expected PPI inflation report that showed the largest increase in inflation (at the wholesale level) since June 2022. That sell-off has extended into this week at a slower pace as traders await Fed Chair Jerome Powell’s speech on Friday at the Jackson Hole Economic Policy Symposium, hoping for further clarity on the path of monetary policy in the US.

Cryptocurrency spot prices began their sell-off last Thursday on Aug 14, 2025 following a stronger-than-expected PPI inflation report that showed the largest increase in inflation (at the wholesale level) since June 2022. That sell-off has extended into this week at a slower pace as traders await Fed Chair Jerome Powell’s speech on Friday at the Jackson Hole Economic Policy Symposium, hoping for further clarity on the path of monetary policy in the US.

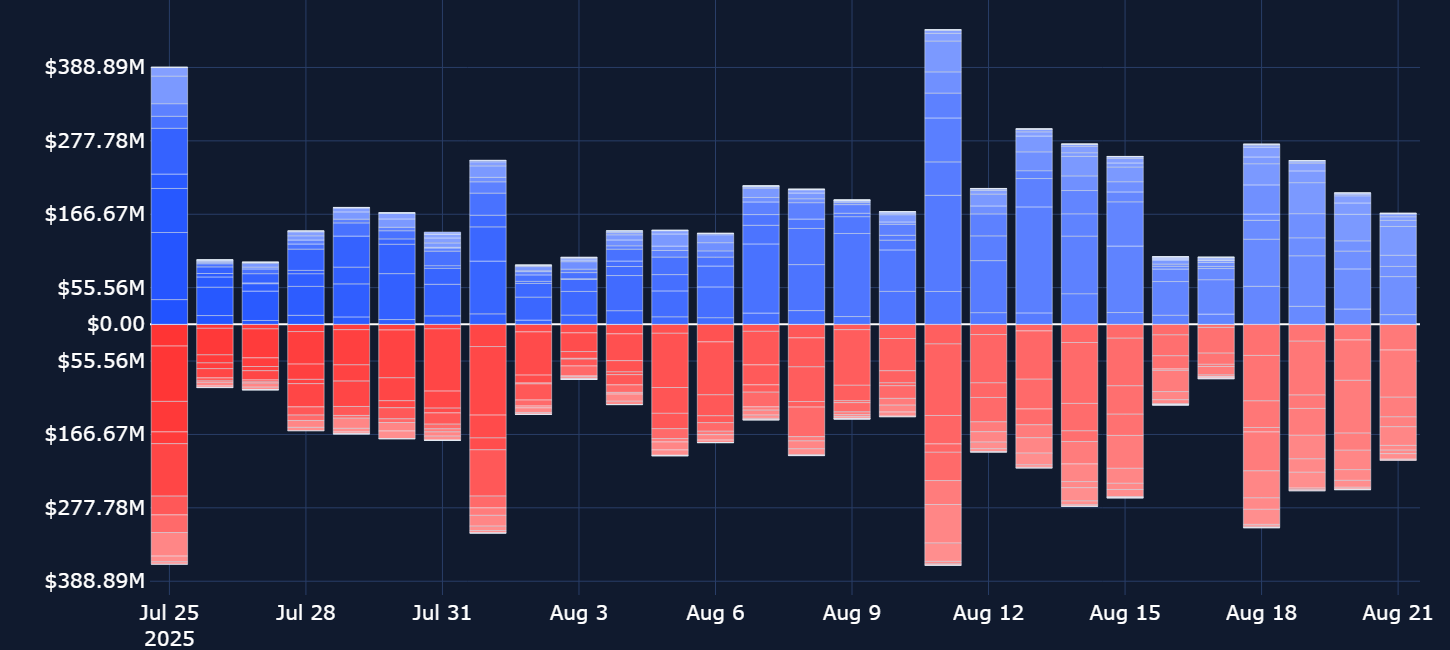

Derivatives data show that uncertainty regarding the health of the US economy and the impact of tariffs on inflation has culminated in a lack of willingness to make any outsized bets on the direction of the market. Open interest in perpetual futures contracts has declined from its record highs while daily trade volume has declined, perpetual swap funding rates have turned negative (but only temporarily) and options markets suggest a premium for downside protection, an indication that traders expect lower prices.

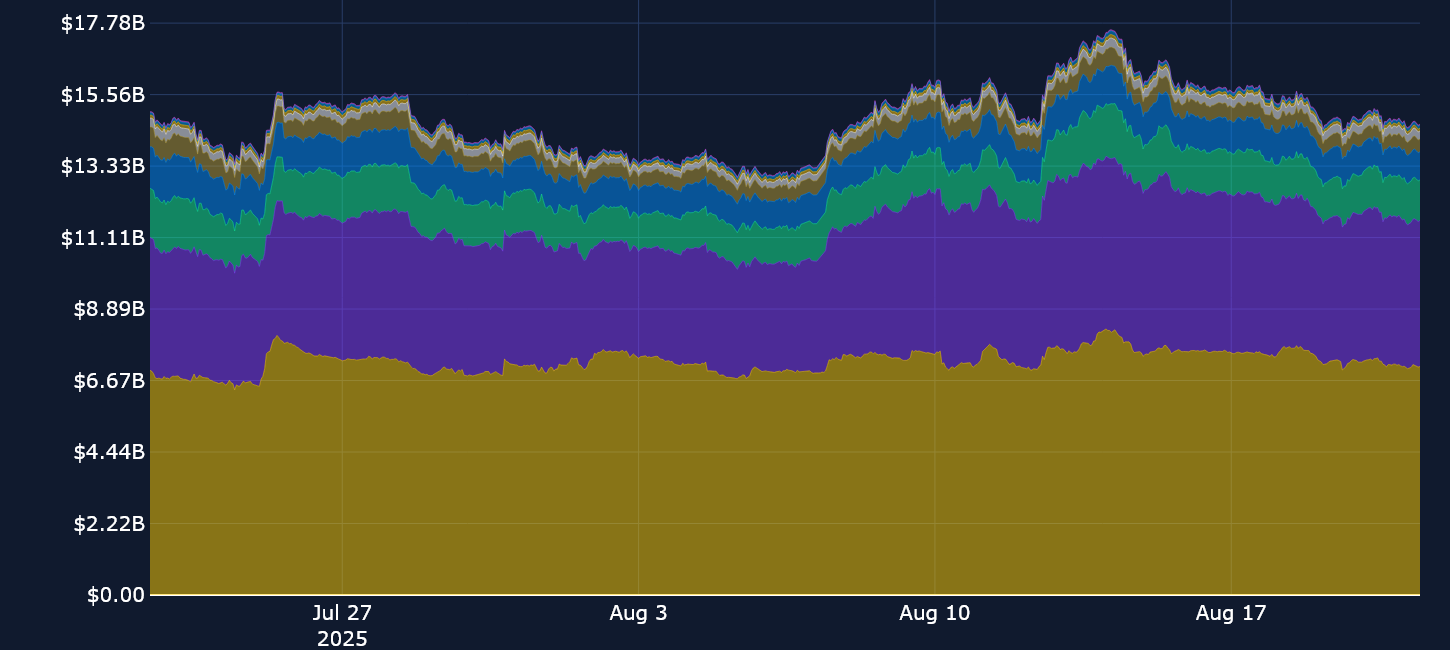

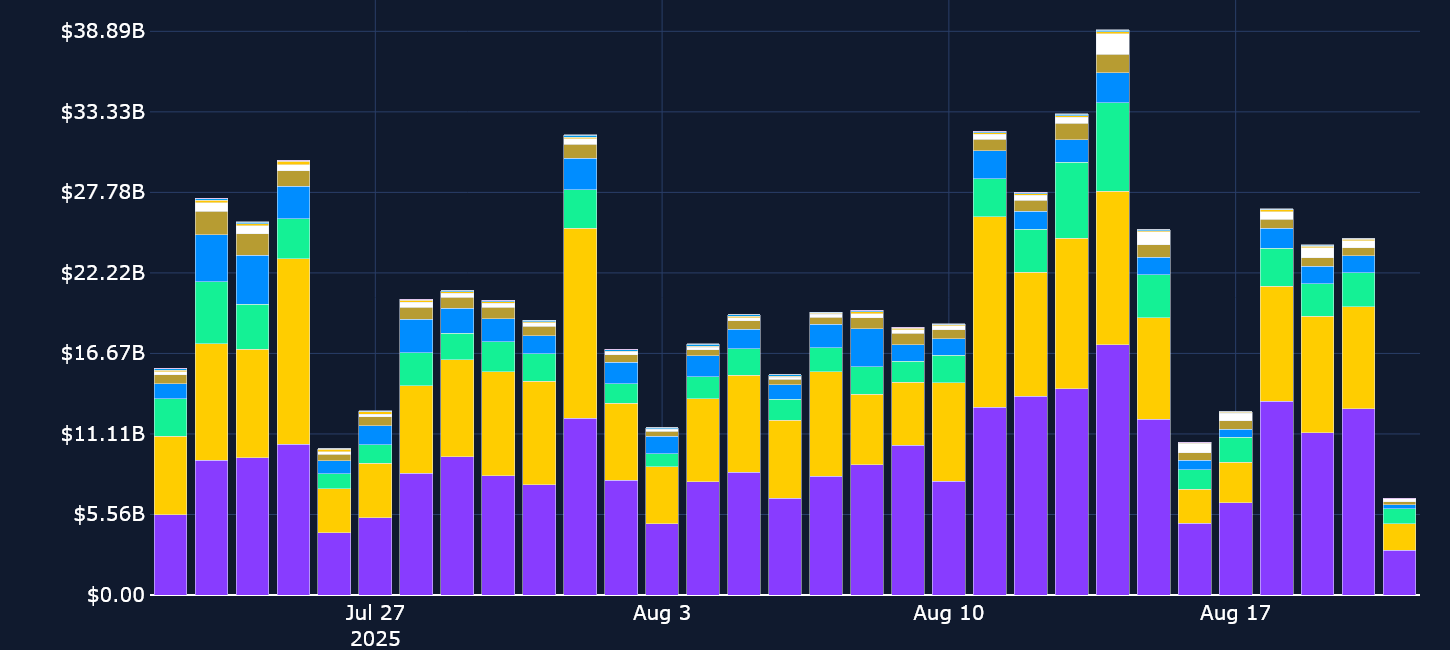

Perpetuals: Open interest in perpetuals has dropped to $14B, despite no major liquidations, suggesting some traders are on the sidelines awaiting clarity on the US economy and monetary policy from Chair Powell’s Friday speech.

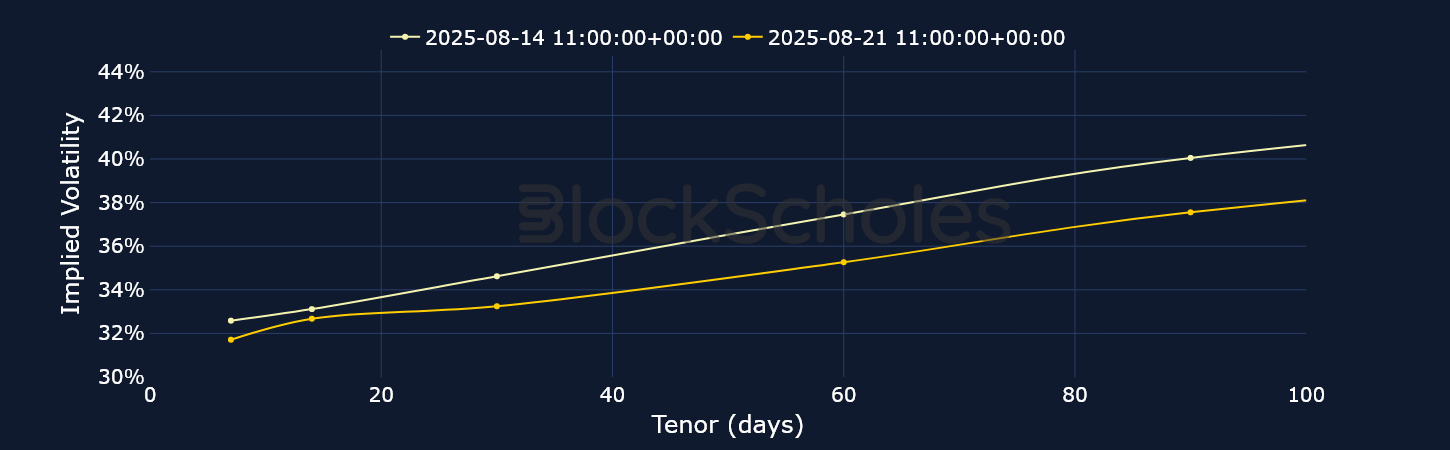

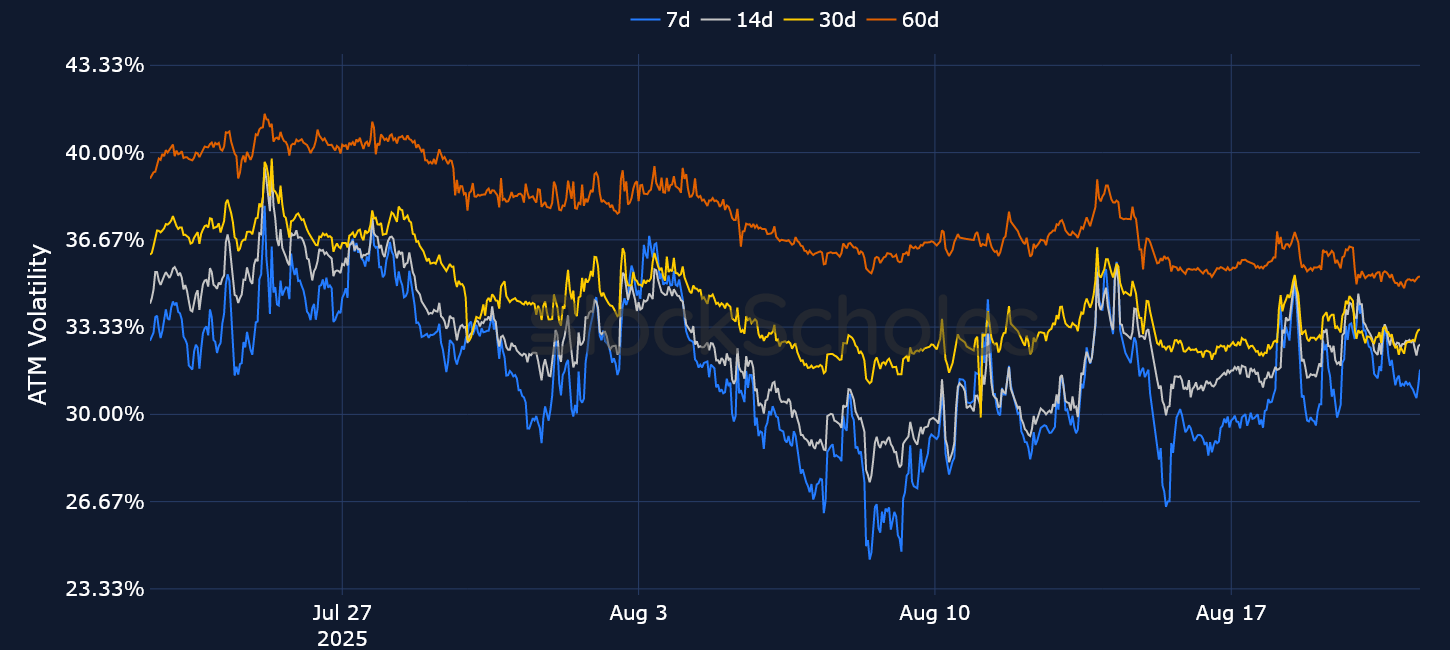

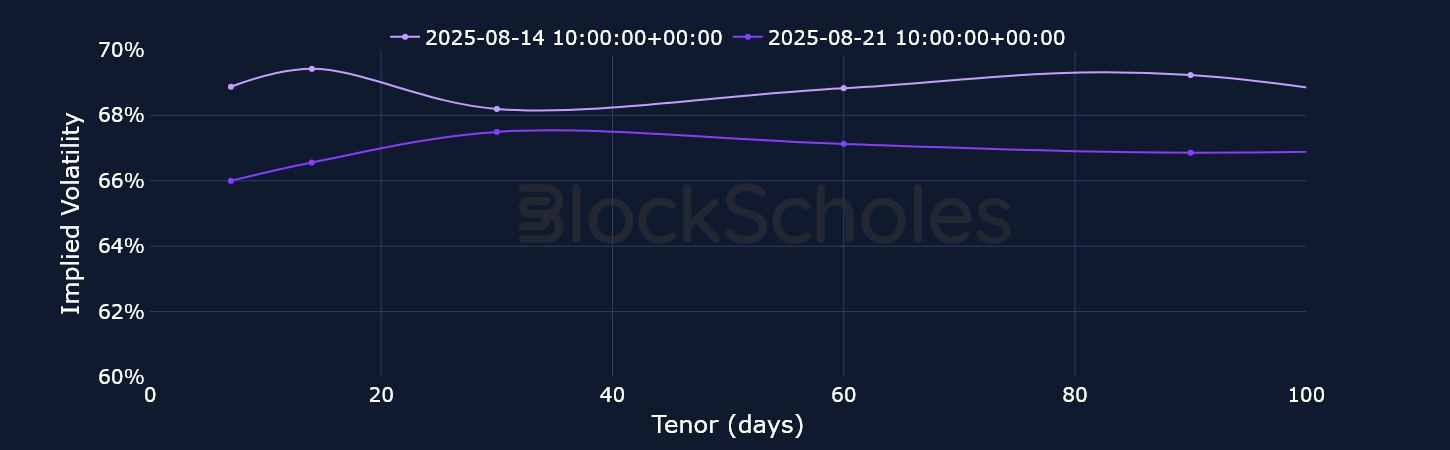

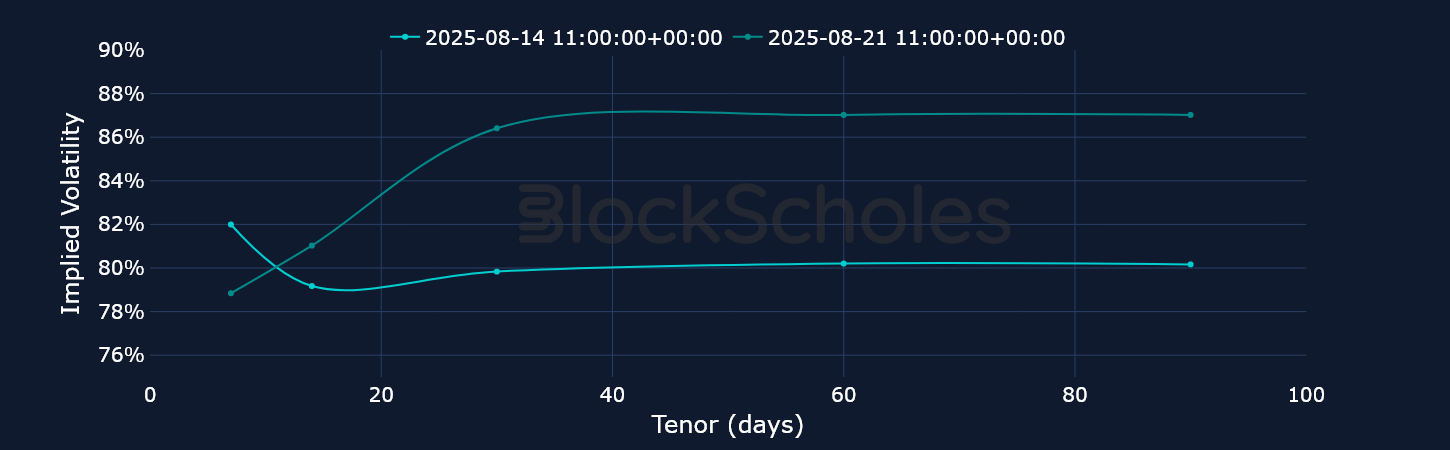

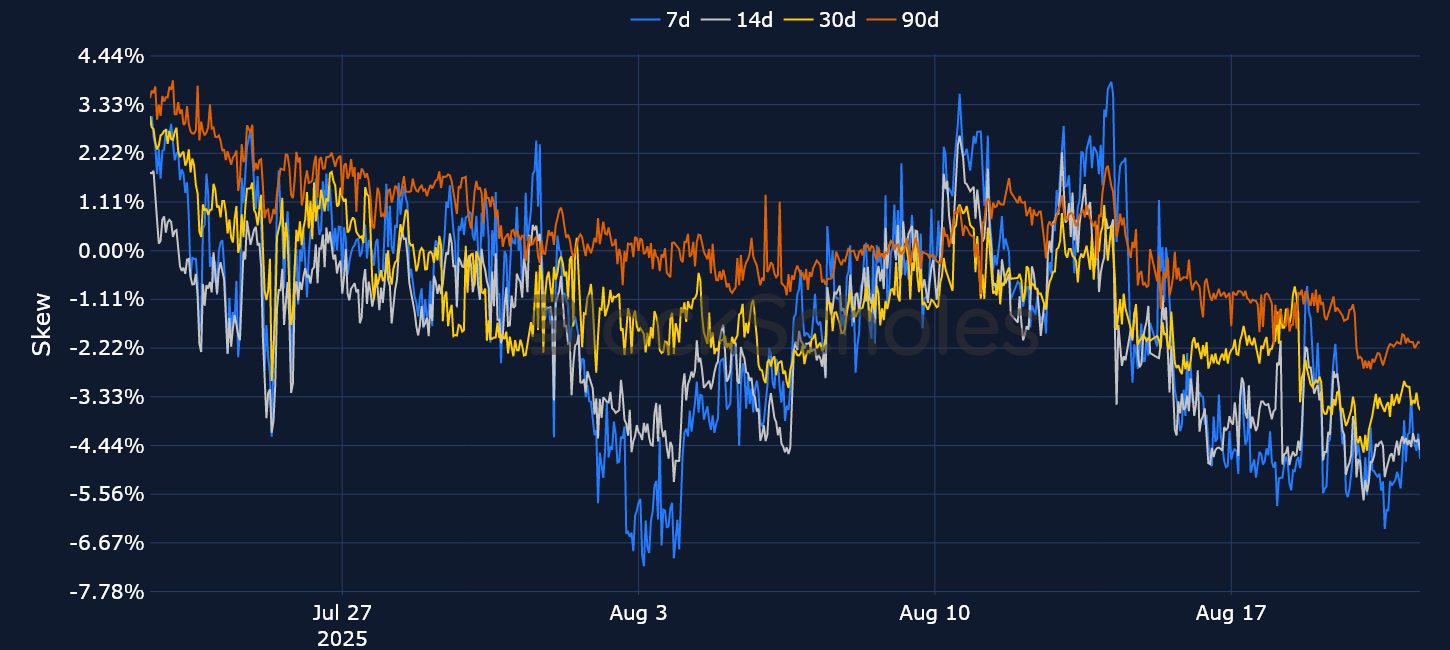

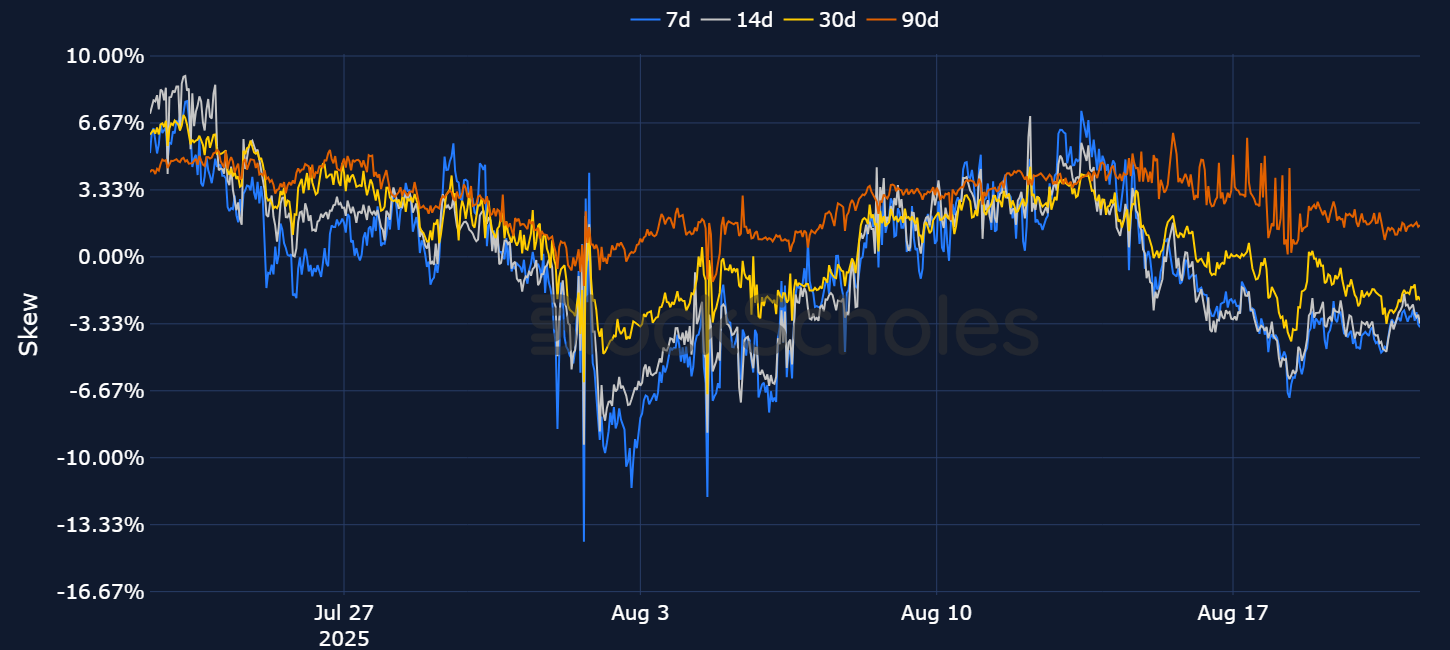

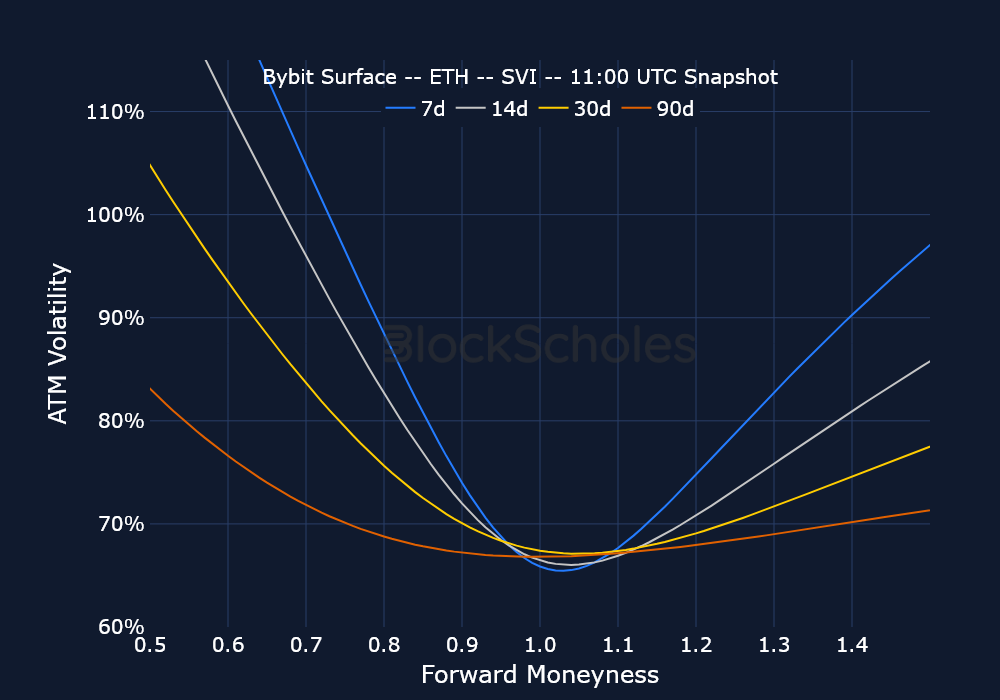

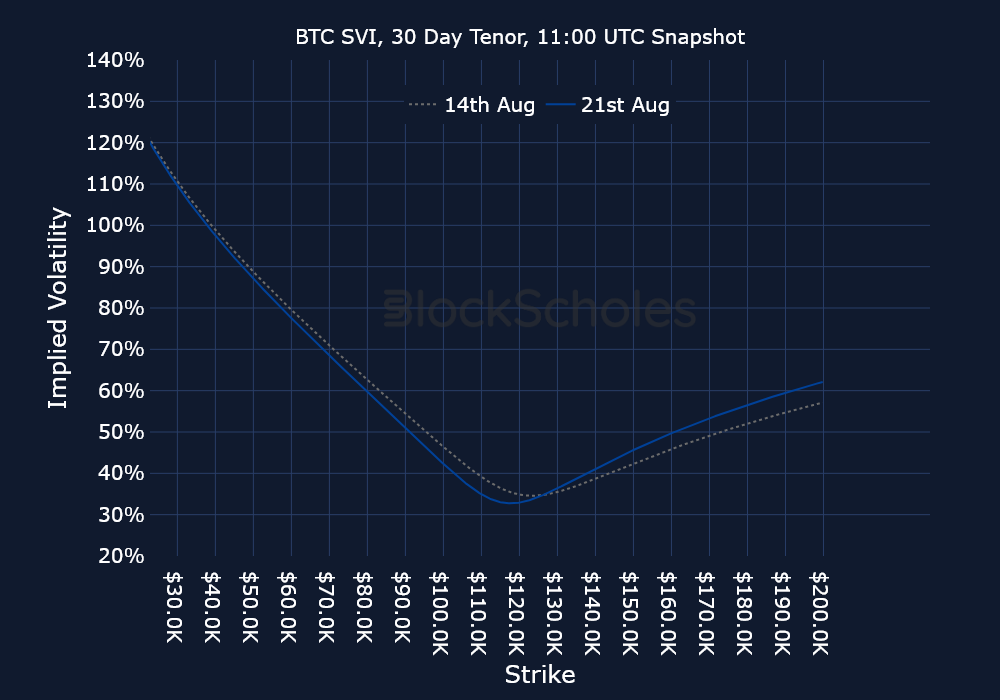

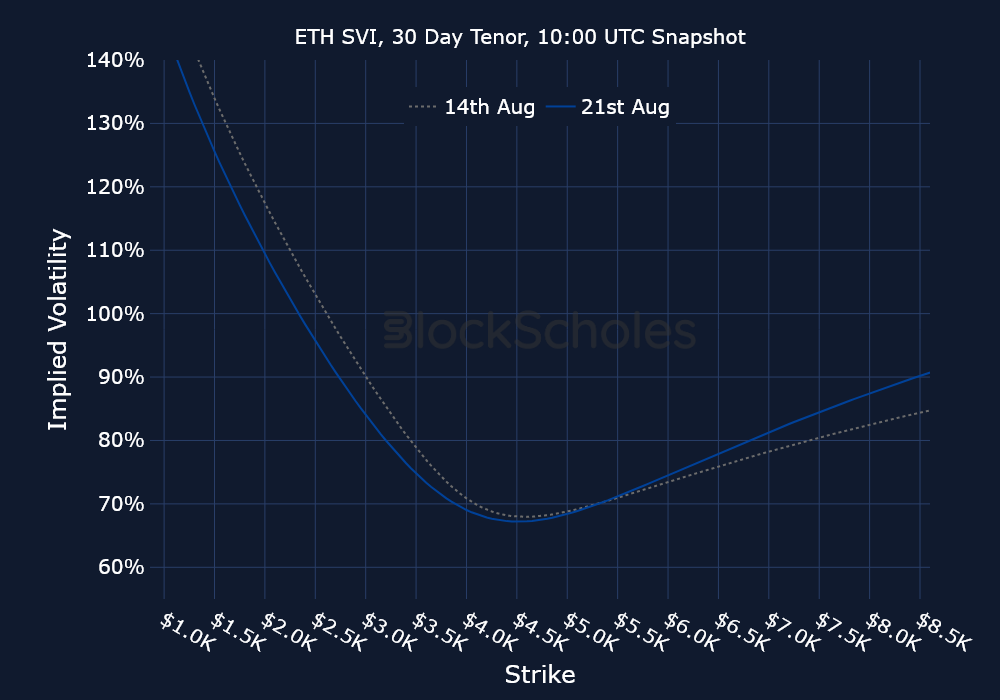

Options: Sentiment in BTC and ETH options has turned bearish, with short-tenor volatility smiles skewed toward OTM puts. Unlike previous spot price sell-offs, the bearishness in options isn’t just limited to short tenors, and is apparent across the term structure. In addition, the 90-day skew for BTC options has turned negative, suggesting traders are bracing for longer-term moves lower in spot.

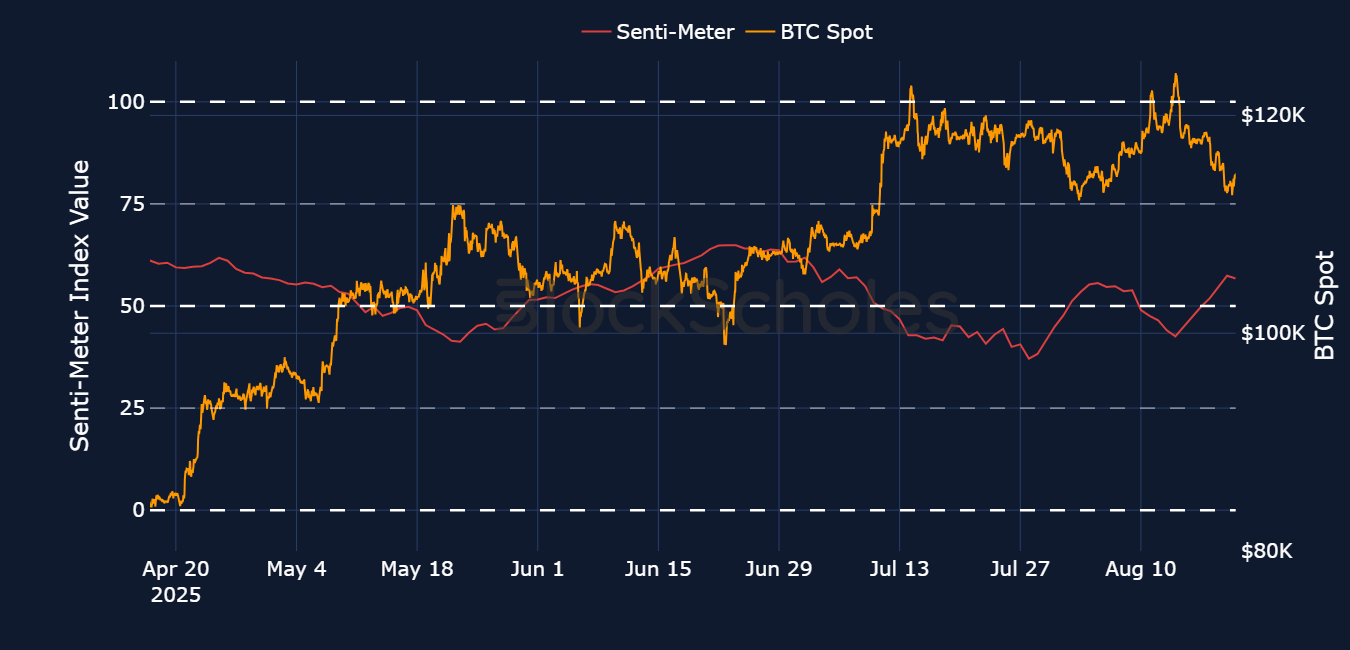

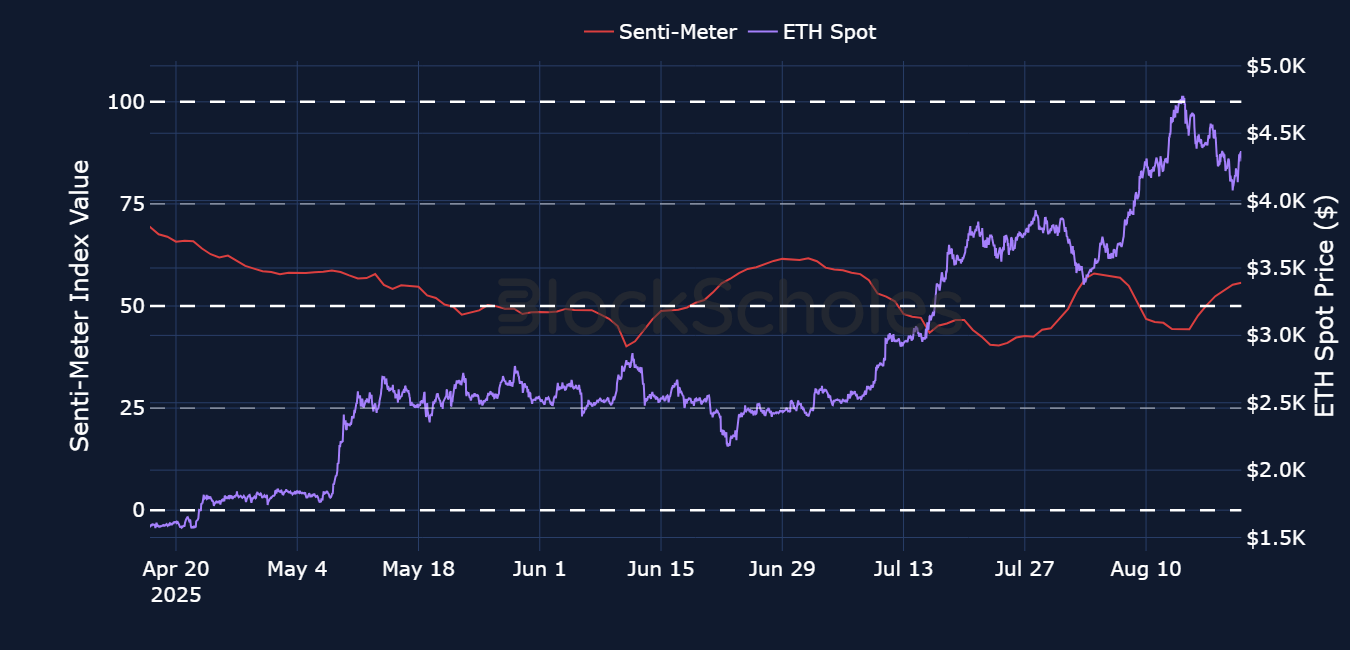

Block Scholes’s Senti-Meter Index aggregates the funding rate, future-implied yield and volatility smile skew into a single expression of sentiment in derivatives markets. See more in the methodology article here.

After a record level of open interest in perpetual futures last week, crypto markets have largely been buffeted by changes in the US macroeconomic environment. A CPI print that showed little tariff-induced inflation in goods first buoyed market expectations for a rate cut in September by the Fed. However, these expectations were pared back in response to a stronger-than-expected PPI inflation report that shows the largest increase in inflation (at the wholesale level) since June 2022.

These mixed signals mean that market participants have largely been awaiting Chair Powell’s Friday speech for further clues to the path of monetary policy before taking any major positions. In line with the famous adage ‘“markets hate uncertainty,” spot prices this week have declined across the board, and open interest has subsequently fallen closer to $14B. Moreover, this decline is broad-based across all tokens, not just concentrated in headline assets. The decline in open interest is also not due to large liquidations or a closing of positions, strengthening the view that markets are sitting on the sidelines awaiting clarity from Chair Powell.

As with perp open interest levels, there’s a night-and-day difference in funding rates this week relative to last week. Funding rates across the tracked tokens were almost entirely positive last week, in line with a surge in the total market cap of cryptocurrencies past $4.1T for the first time in history. This week, spot prices are all lower as part of a wider de-risking beyond just crypto assets (US risk-on equities have fallen all week), and therefore it’s not surprising that funding rates have been shaky. That same sentiment is seen in volatility smile skews, which assign a volatility premium to OTM puts. However, the negative sentiment in perpetuals has been short-lived, as most tokens are once again trading with positive funding rates in contrast to a deepening put-skew in volatility smiles.

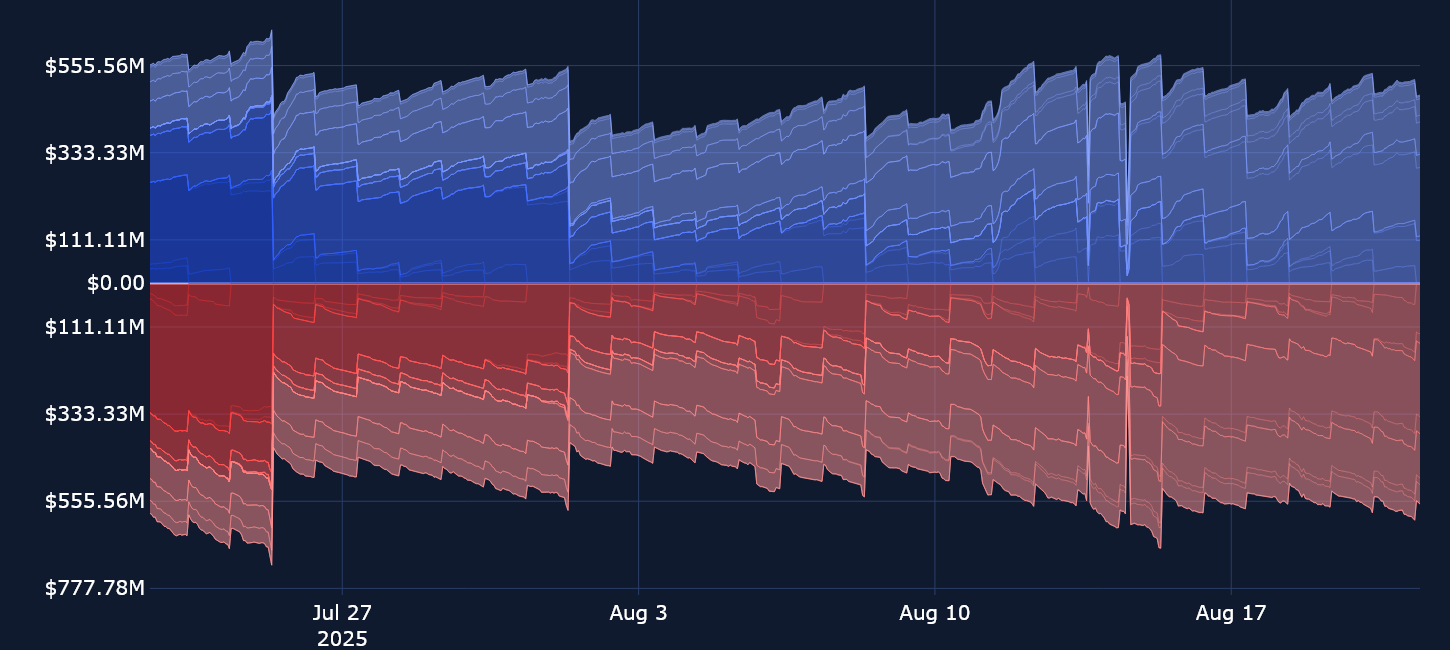

The mixed signals in derivatives markets could be an indication of a lack of clear position-taking, as well as markets sitting on the sidelines until we get more clarity on the state of the US economy. This perspective is supported by the calm decline in open interest, without any sharp liquidation events — which also indicates that perpetual markets haven’t been willing to take any outsized bets this week.

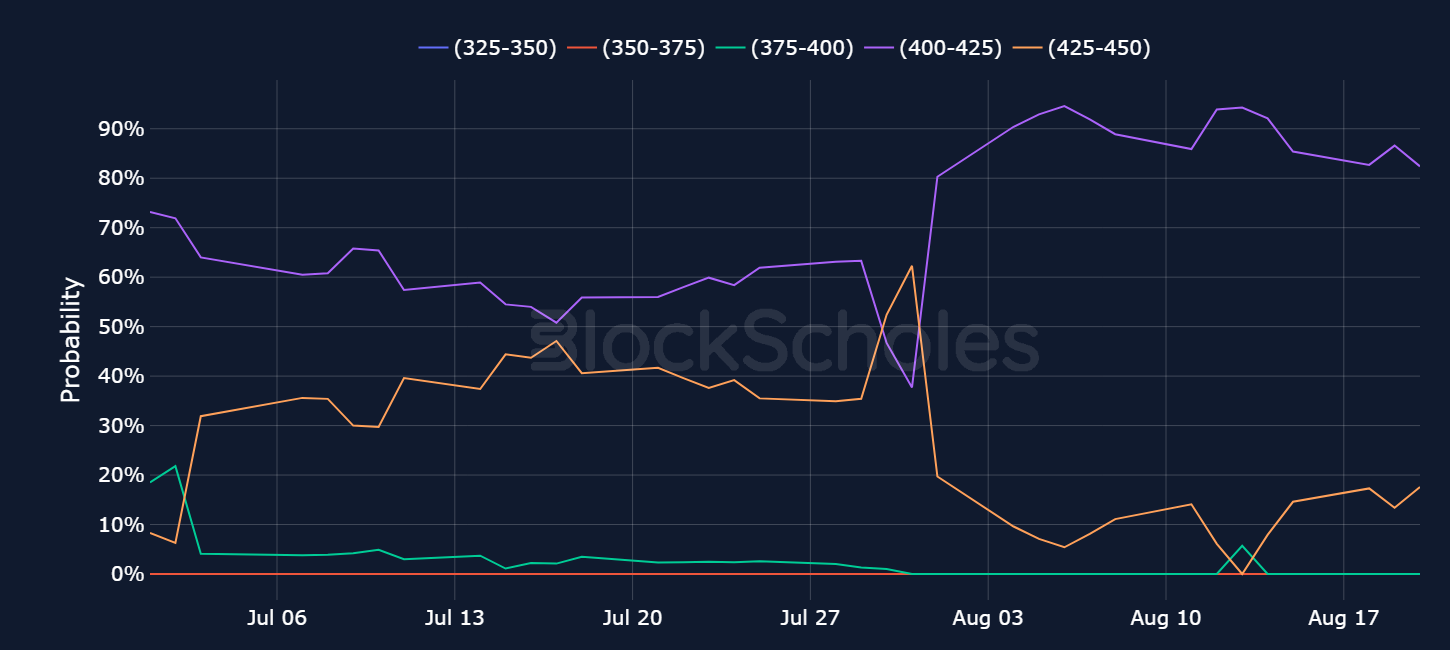

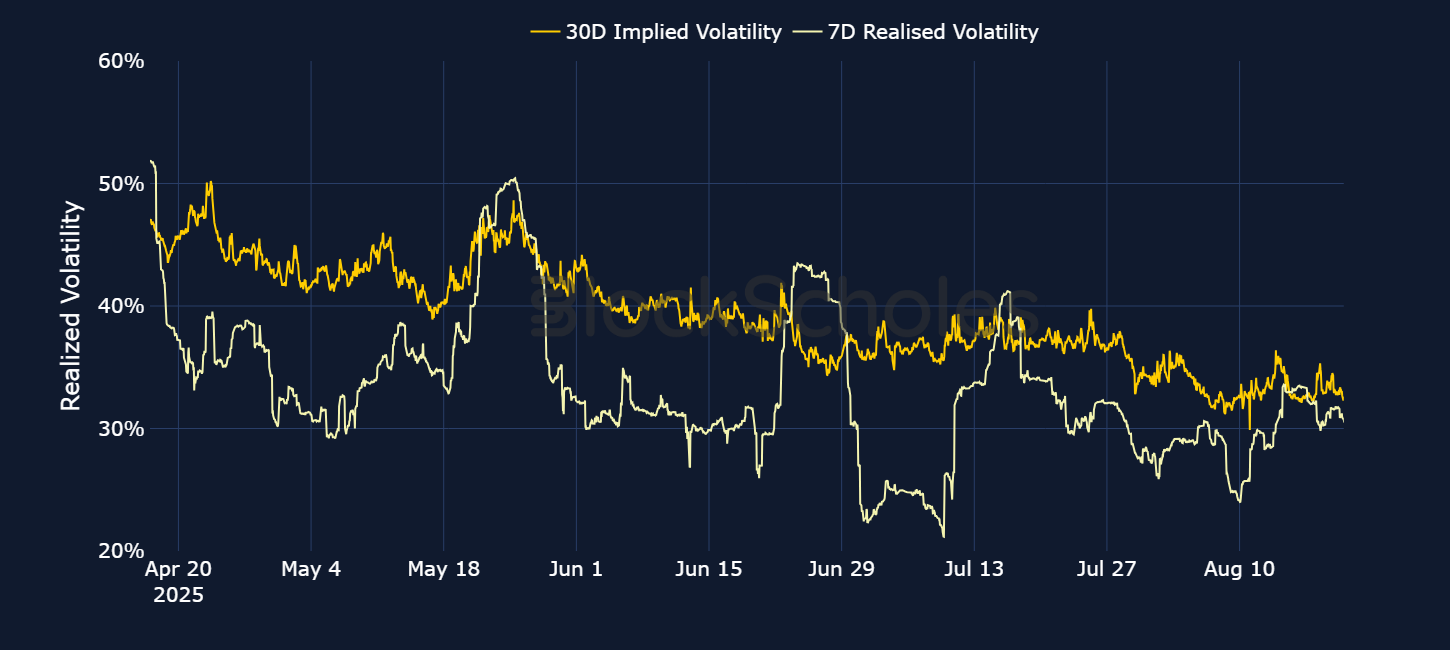

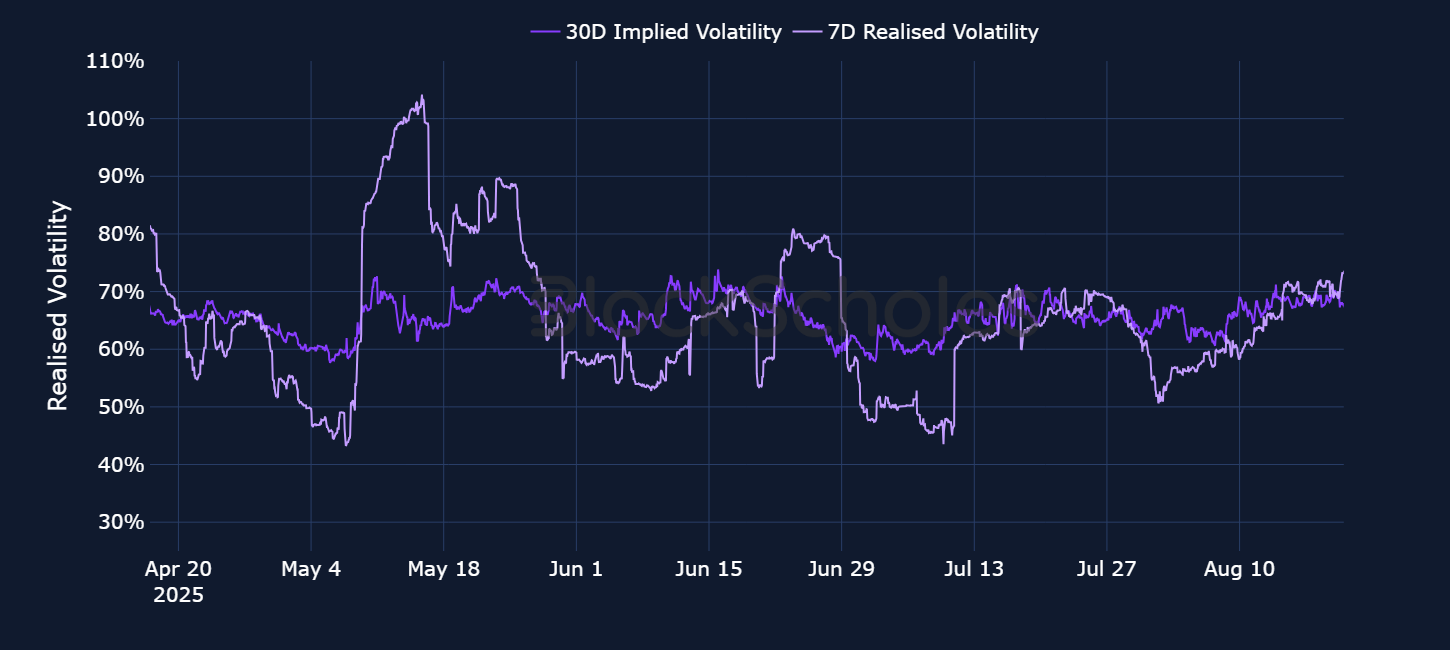

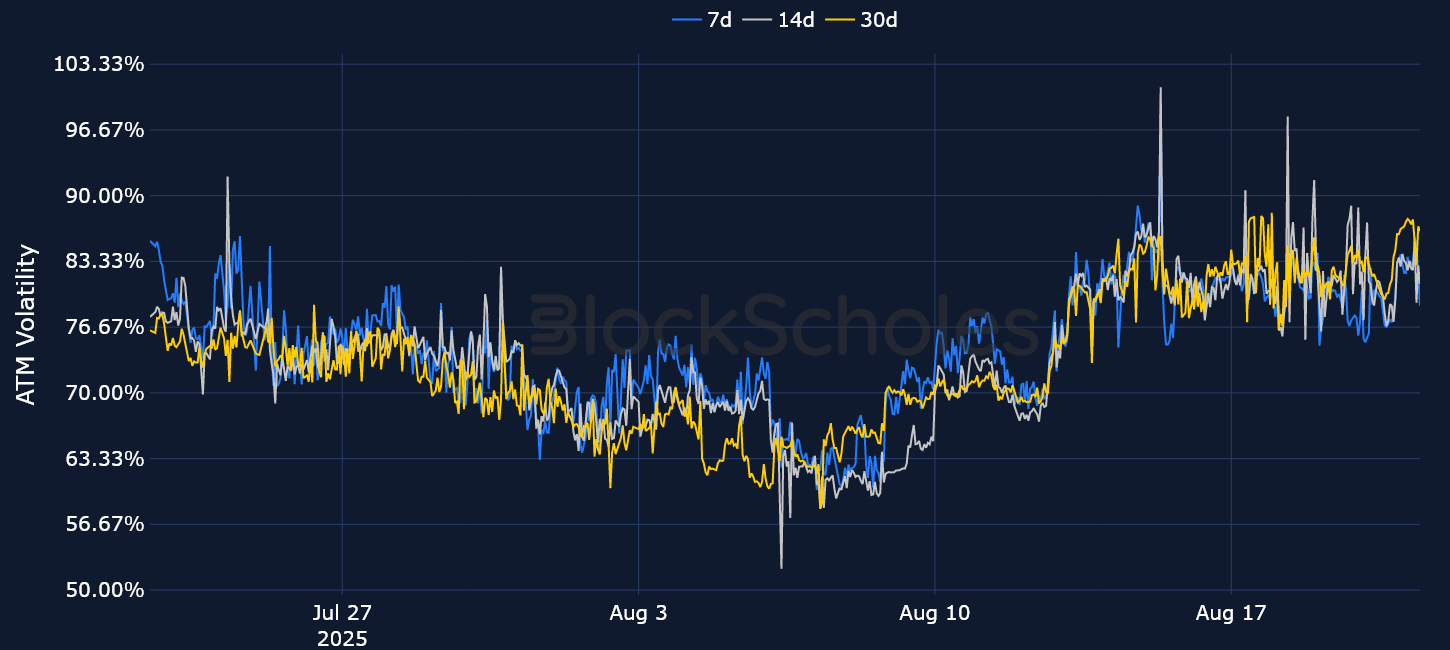

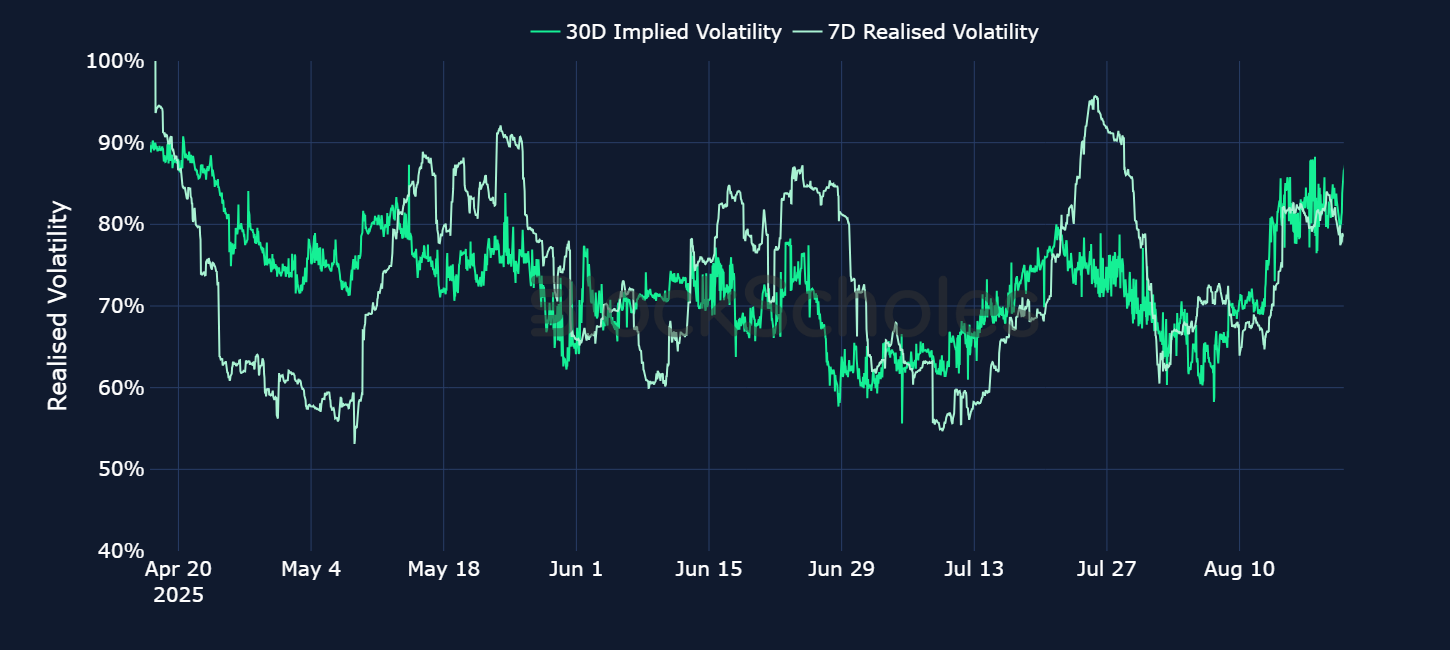

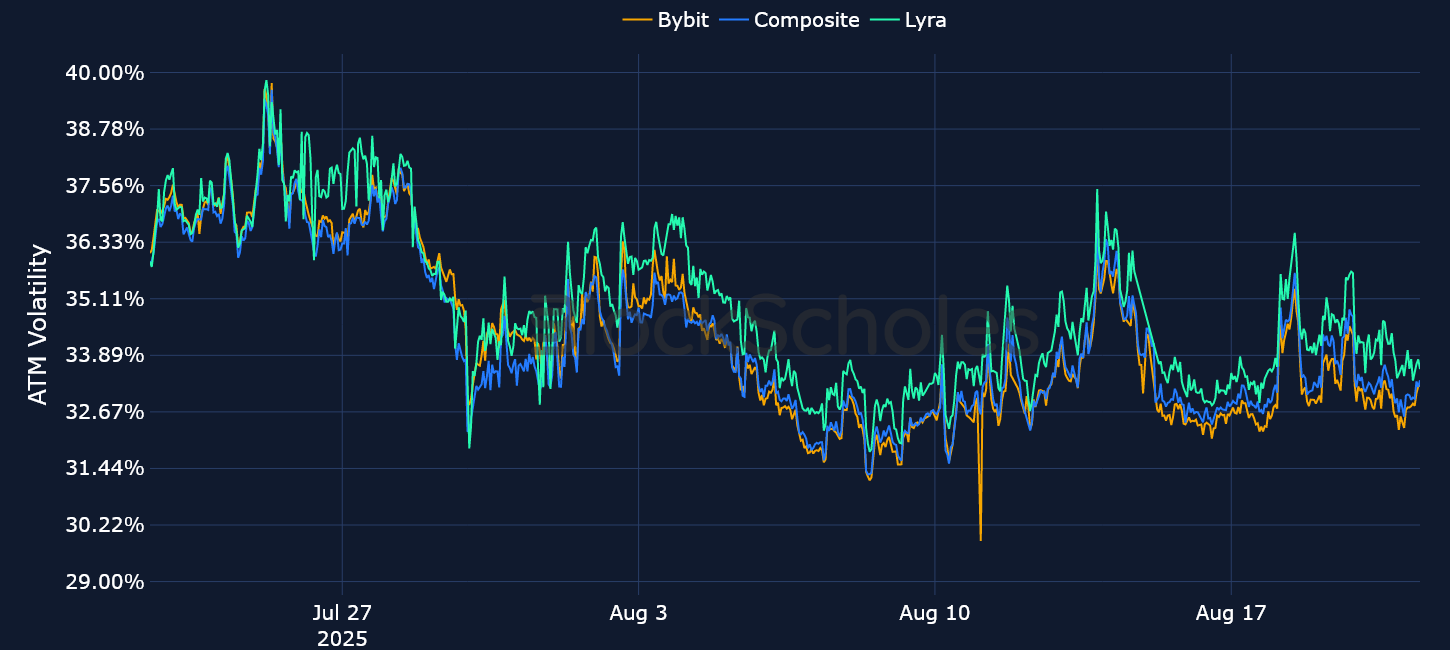

This week has seen BTC volatility act as an outlier, as 7-day delivered volatility has declined to 30% (compared with an increase in realized volatility for both ETH and SOL). Short-tenor at-the-money implied volatility is also trading close to the low 30% region, marking another week in which options IV remains in a historically low environment. There’s little evidence of any major positioning ahead of Chair Powell’s Jackson Hole speech on Friday, or ahead of the September FOMC meeting (which currently assigns a 73.3% probability of a rate cut — far lower than last week’s market-implied odds of 98%). Taking both realized and implied volatility together, what we find is that the volatility in recent BTC returns has been low, and that forward-looking options markets are only expecting a 2–3 percentage point increase in volatility level over the next 30 days, compared to what’s already been delivered. Additionally, options markets aren’t expecting any meaningful spike higher in implied volatility (at least over the short term).

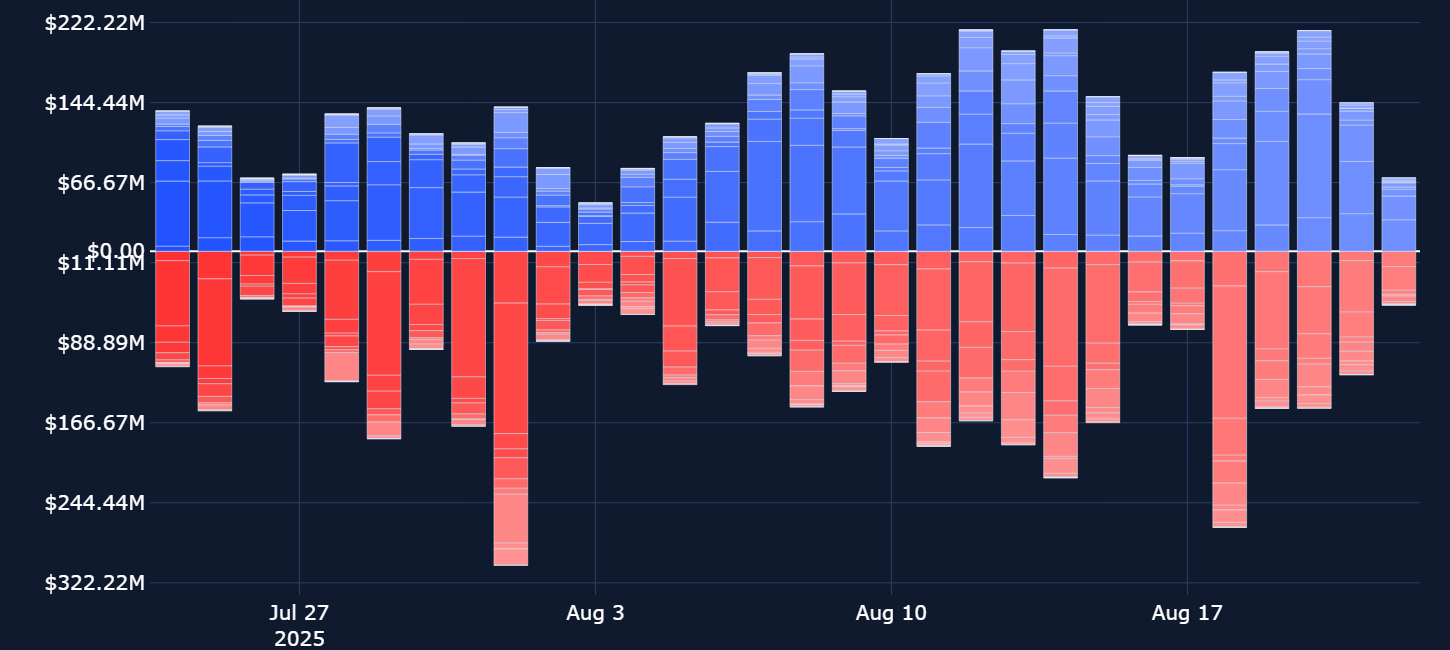

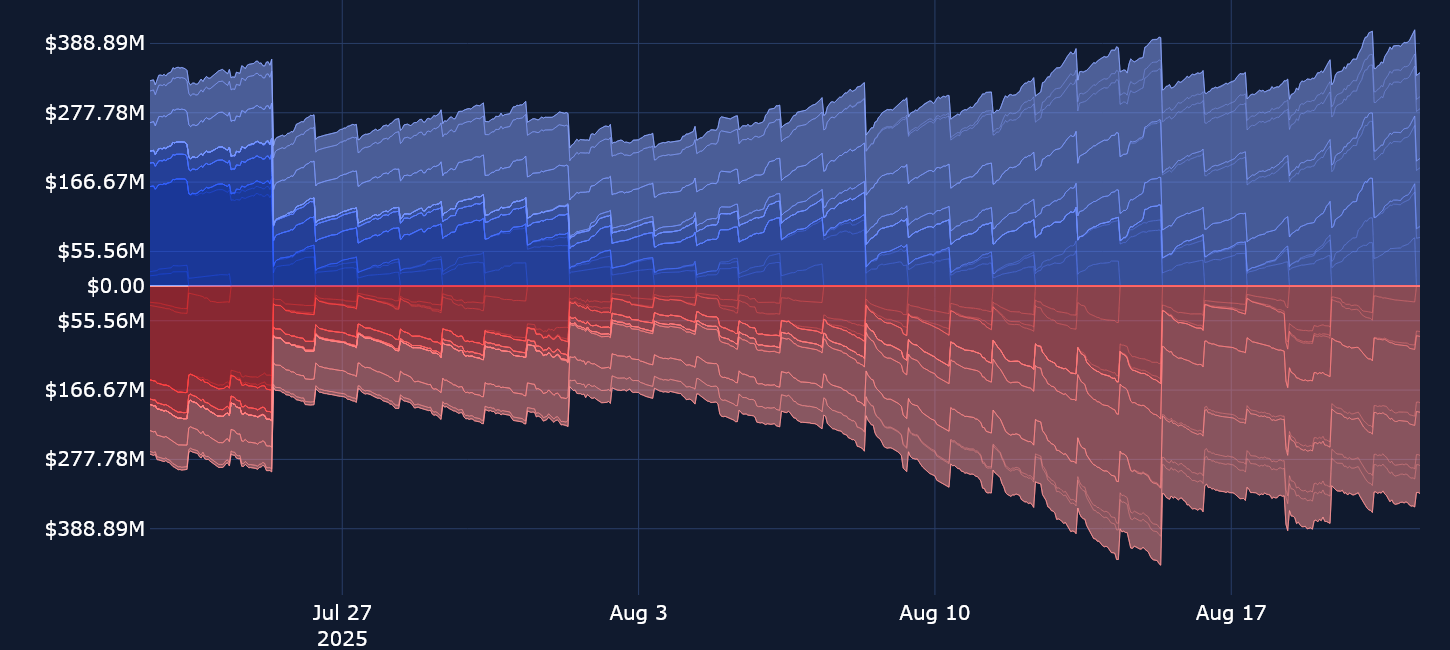

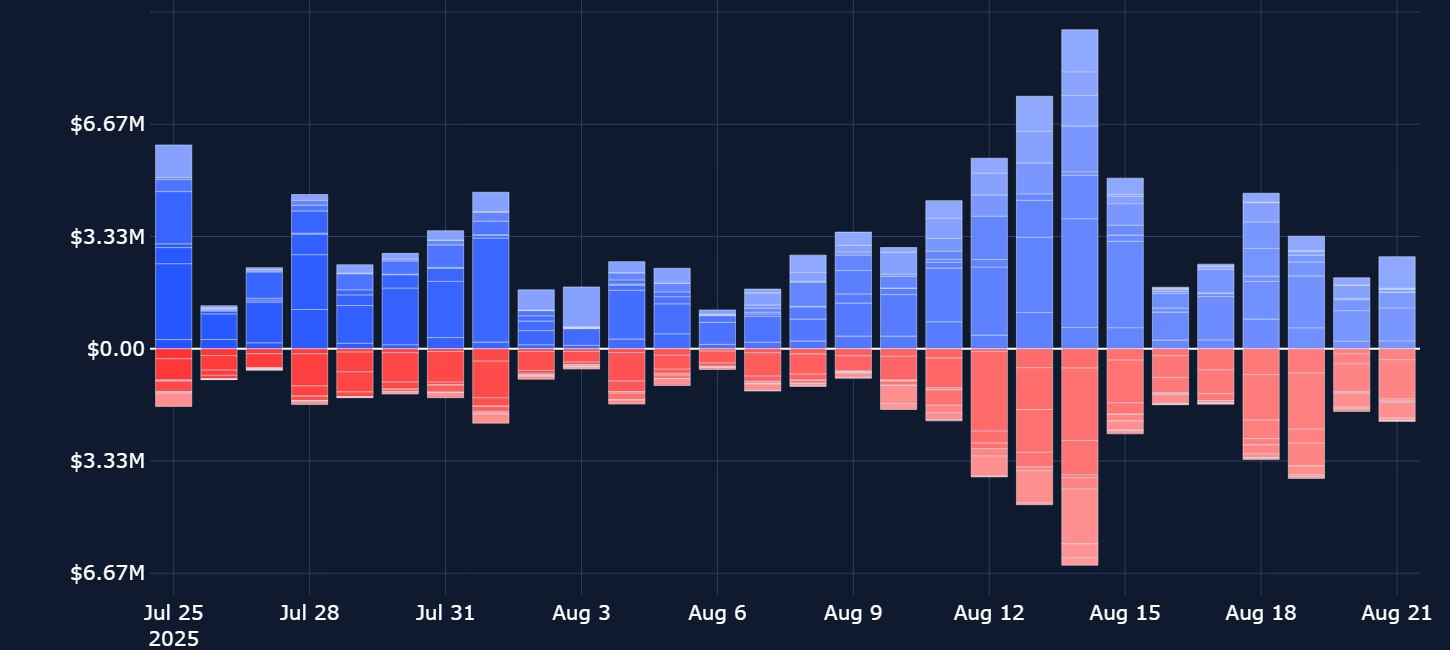

BYBIT BTC OPTIONS OPEN INTEREST

ETH’s spot price is down more than 7% over the past week, in line with the wider de-risking across financial markets. Spot ETFs have seen four consecutive days of outflows after a blockbuster July, and ETH options markets are pricing in a volatility premium for OTM puts.

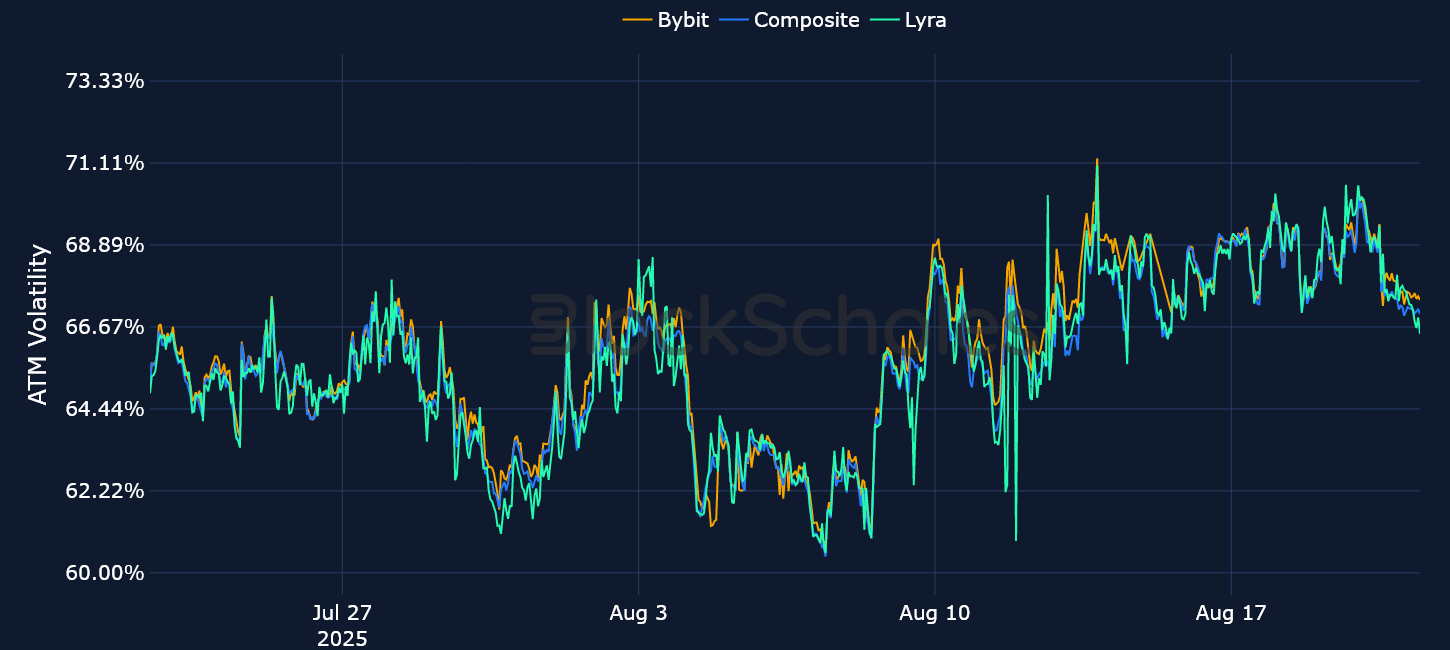

Unlike the low levels of implied volatility seen in BTC, implied volatility for ETH continues to hold between 65–70%, in line with a move higher in realized volatility from 68% to 74%. The most intriguing observation regarding ETH volatility is its divergence from BTC volatility. Realized volatility for ETH has ticked higher while it’s drifted lower for BTC, and options markets are pricing for a continuation of that trend as ETH IV hovers around a 2x premium to BTC options. Another divergence between the two options’ markets is in the term structure of volatility: ETH’s term structure of volatility remains flat, while BTC’s term structure is sloping firmly upward.

Implied volatility for SOL options has increased significantly over the past couple of weeks after finding a local bottom around 57% for 7-day tenors. That increase in forward-looking volatility expectations appears to be a reaction to the increase in realized volatility, suggesting the narrative in SOL volatility has been driven by increased choppiness in its spot price (which is down 6% over the past seven days), and not purely by options market positioning.

We also see that options volumes are noticeably lower following the sell-off in spot prices that began on Thursday, Jul 14, 2025. Volumes have dropped by 50% of their highs since that same date. However, open interest remains high for SOL options, suggesting that traders may have already taken their positions and are on the sidelines awaiting further developments for the macro picture in the US.

BTC and ETH skew dropped sharply toward out-of-the-money put options at the beginning of last week’s sell-off, as we’ve seen it do many times before — such as during the beginning of August following the pullback in spot prices after major revisions to US labor market data. However, the current move toward a negative put-call skew ratio is different from previous instances: this time, we’re seeing bearish sentiment across the term structure.

During the negative volatility smile skew for short-tenor options at the beginning of August, longer-tenor options skew remained positive. However, this time, even the 90-day skew ratio has turned negative. That makes it more difficult to understand exactly what the market is positioning for. It isn’t necessarily a reaction to the move in spot price, as prices are slowly leaking lower. However, it’s also likely that it’s not purely due to positioning for the Jackson Hole speech on Friday, given that it isn’t limited only to the short-term horizon.

Open interest and trading volume data are sourced “as is” from the Bybit exchange platform API exclusively, and as such do not represent a comprehensive picture of the sum of trading activity across all derivatives markets or exchanges. The data visualized in this report consists of hourly and daily snapshots, recorded over the previous 30 days. Daily (hourly) snapshots of trade volume record the total sum of the notional value of trades recorded in the 24H (1 hour) period, beginning with the snapshot timestamp.

If not explicitly labeled as derived from another exchange, the input instrument prices to all derivatives analytics metrics in this report are sourced from the appropriate endpoints of Bybit’s public exchange platform API. In the event that data is labeled or referred to as representing the market on another exchange source, that data is sourced from the appropriate endpoint of each respective exchange’s public API.

Macroeconomic charts and data are sourced “as is” from the Bloomberg Terminal. Exchange data is sourced “as is” from publicly available exchange APIs. Block Scholes makes no claims about the veracity of public third-party data.

After acquisition of underlying-denominated raw data for open interest and trading volume on the Bybit exchange platform from Bybit’s API endpoint, equivalent dollar-denominated figures are calculated using the concurrent value of Block Scholes’s Spot Index for the relevant underlying asset.

Block Scholes’s Spot Index represents the aggregate Spot mid-price for a given currency across the top five CEXs by volume (with USD-quoted markets). It considers the proportion of total volume in the instrument on the exchange, as well as the deviation of a data point from those on other exchanges.

Futures prices are used for Block Scholes’s futures-implied yields calculation services in order to derive the constant-tenor annualized yields displayed in the Futures section of this report.

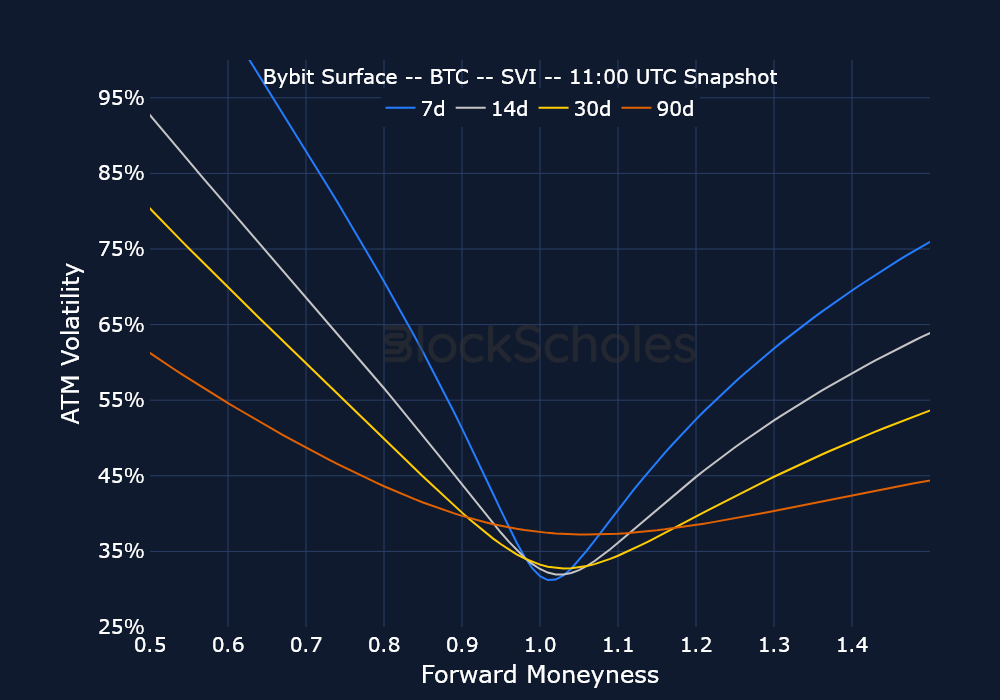

Options prices are used for Block Scholes’s implied volatility calculation services in order to calibrate volatility surfaces, from which all derivatives volatility analytics displayed in the BTC Options and ETH Options sections of this report are calculated. Volatility smiles are constructed by calibrating to mid-market prices observed in Bybit options markets. As part of the calibration process, prices go through rigorous filtration and cleaning steps, which ensures that the resulting volatility surface is arbitrage-free and has exceptional fit to the market observables.

.jpg)

.jpg)