Andrew Melville

Head of Research

ETH stole the spotlight this past week, with a rally of over 20% that brought it within inches of its November 2021 (ATH). That’s not to say BTC has traded quietly, however — on Aug 14, 2025 it reached a new all-time high (ATH) of $124K, driving a sentiment shift in options markets toward OTM calls. ETH has been strongly supported by a wave of institutional buying from corporate digital asset treasuries, such as SharpLink Gaming and BitMine Immersion Technologies, Inc. as well as Spot ETH ETFs, which had their first $1B inflow day on Aug 11, 2025. This is significant because derivatives markets signal a strong bullishness for the rally to continue.

ETH stole the spotlight this past week, with a rally of over 20% that brought it within inches of its November 2021 (ATH). That’s not to say BTC has traded quietly, however — on Aug 14, 2025 it reached a new all-time high (ATH) of $124K, driving a sentiment shift in options markets toward OTM calls. ETH has been strongly supported by a wave of institutional buying from corporate digital asset treasuries, such as SharpLink Gaming and BitMine Immersion Technologies, Inc. as well as Spot ETH ETFs, which had their first $1B inflow day on Aug 11, 2025. This is significant because derivatives markets signal a strong bullishness for the rally to continue.

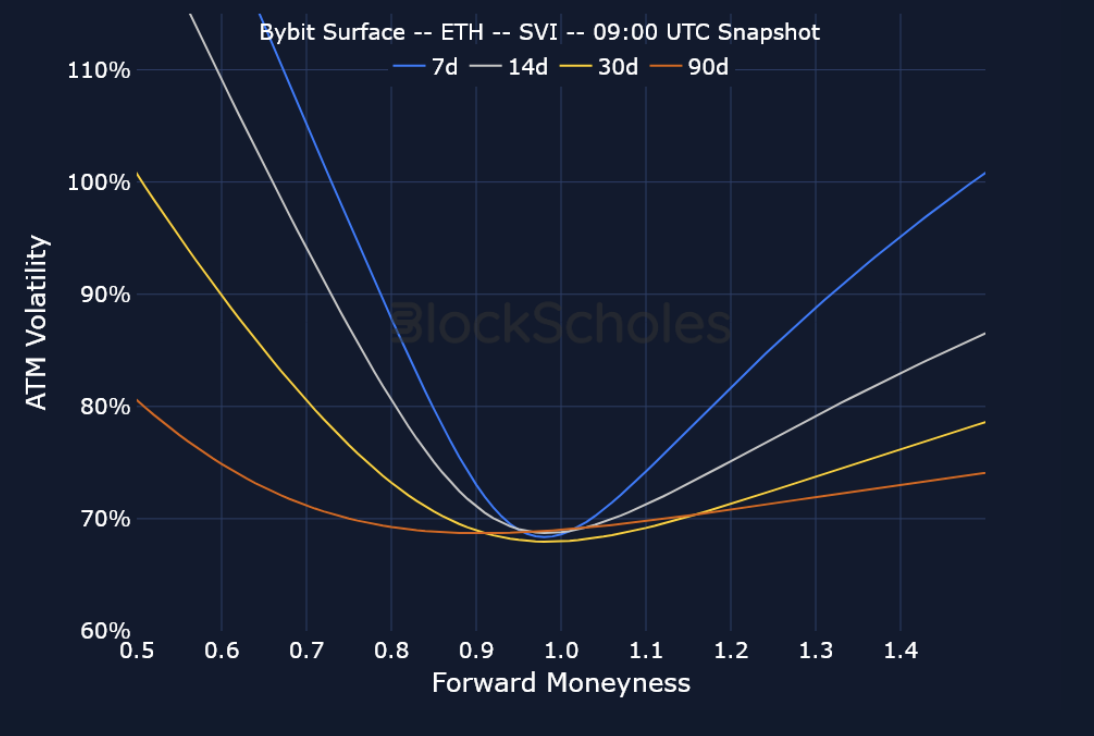

Volatility smiles for 7-day ETH options are skewed 4.8% toward OTM call options, and perpetual swap funding rates are positive, showing a willingness from traders to pay for leveraged upside exposure. BTC rose to a record high on the back of a rally that began when the US president signed an executive order that will allow 401(k) plans to invest in digital assets (such as BTC).

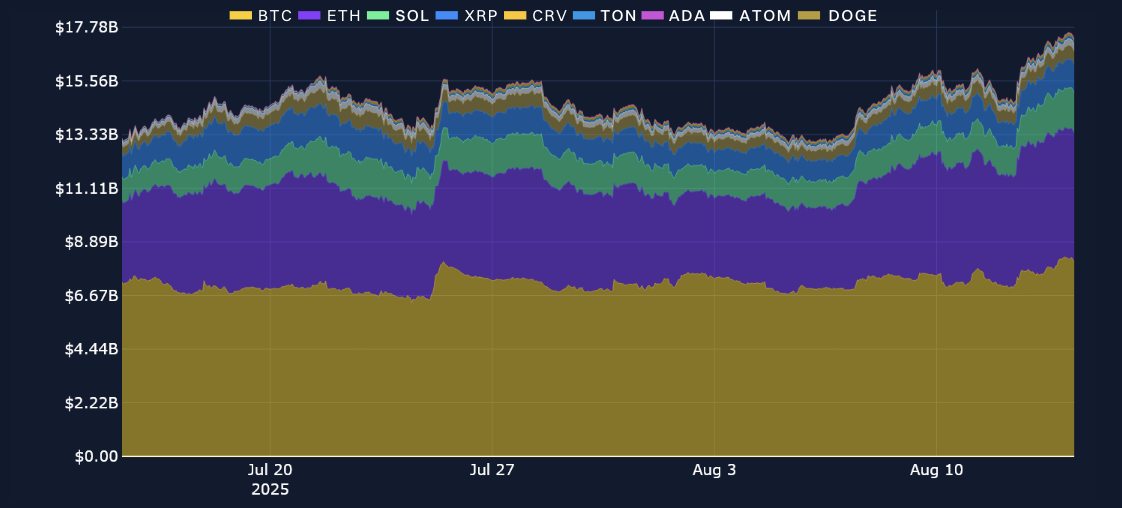

Perpetuals: Open interest in perpetuals reached their highest levels so far in August, largely a result of a $2B increase in open interest for ETH contracts.

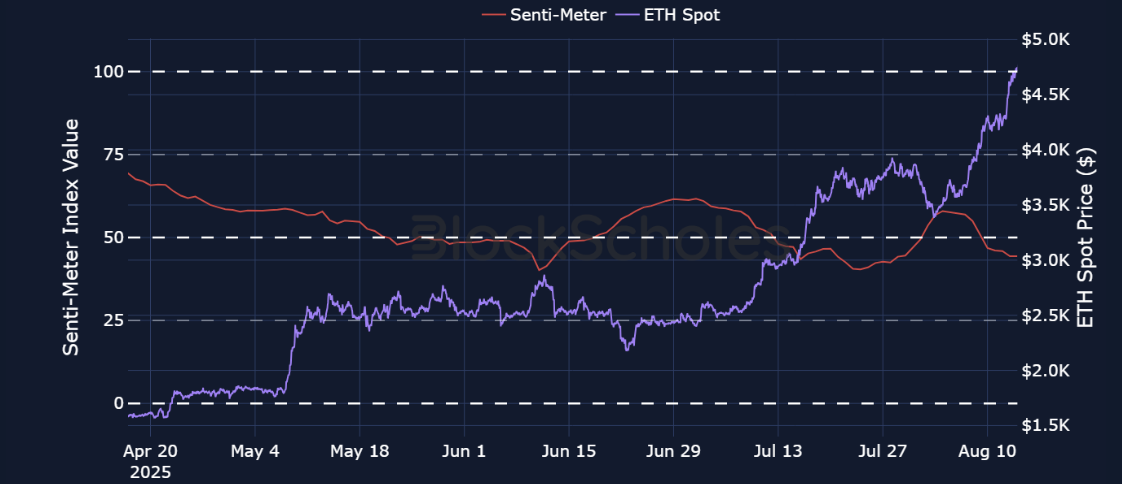

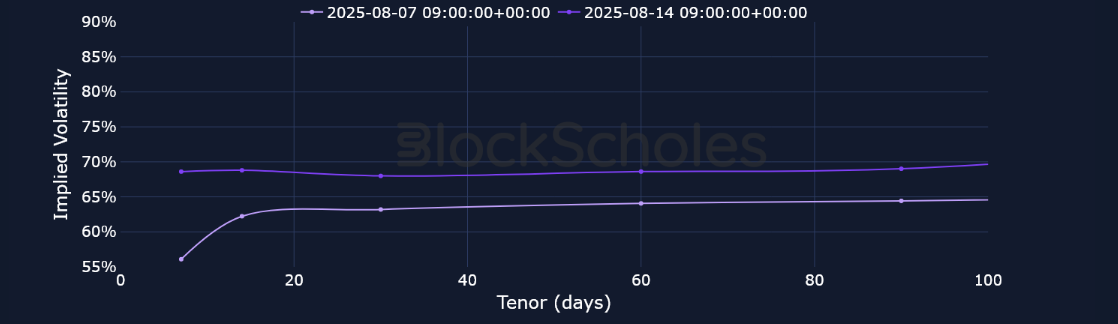

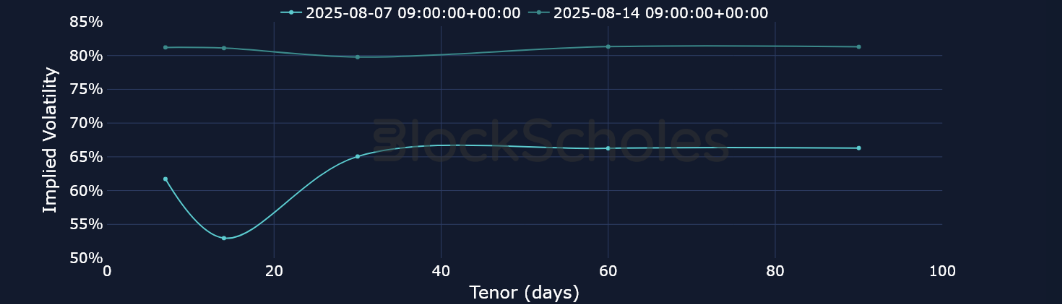

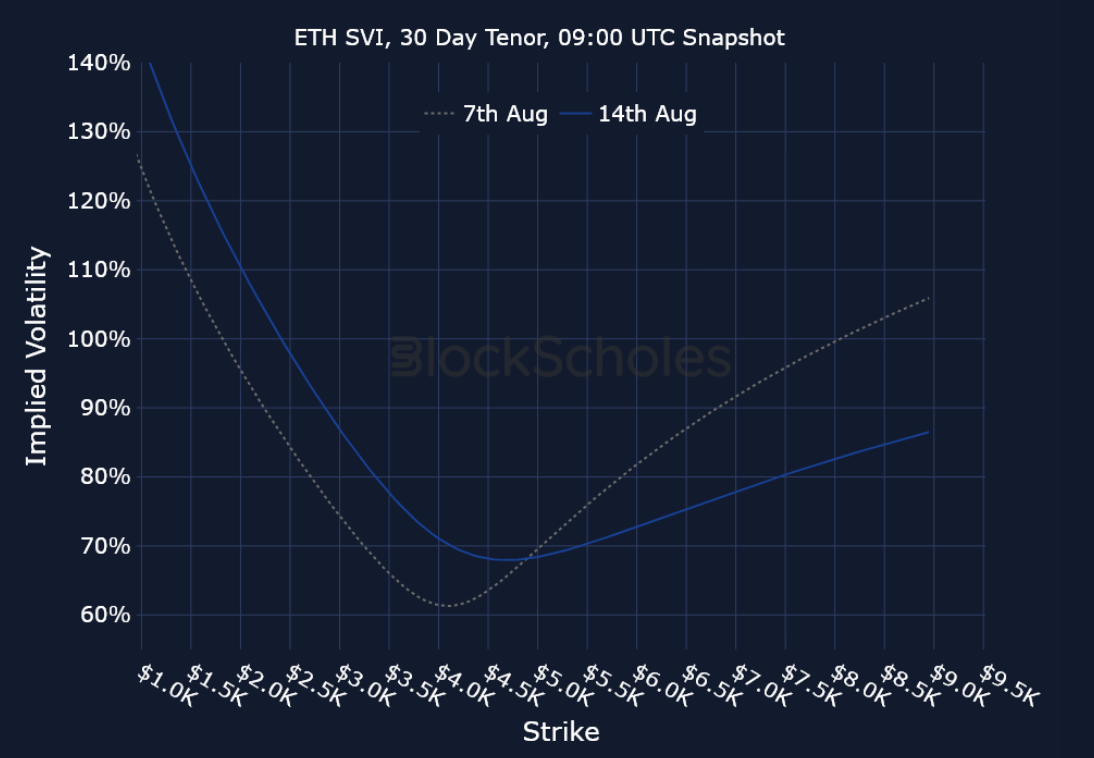

Options: Sentiment in ETH options have U-turned from their −11% skew at the start of August, 2025, and now assign a near 5% premium toward short-tenor OTM call options. Meanwhile, ETH’s term structure briefly inverted earlier in the week amidst the rally in its spot price.

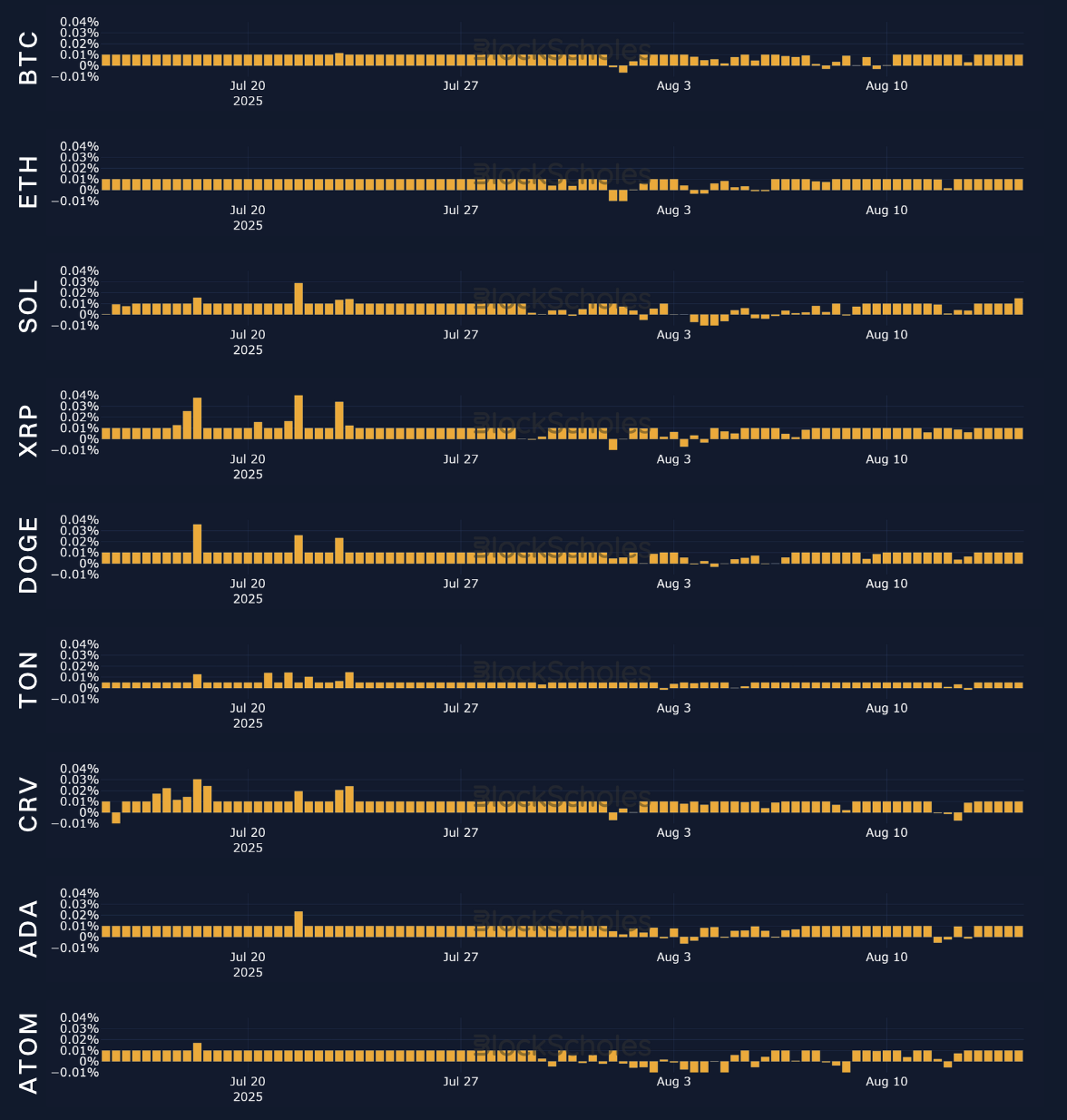

Block Scholes’s Senti-Meter Index aggregates the funding rate, future-implied yield and volatility smile skew into a single expression of sentiment in derivatives markets. See more in the methodology article here.

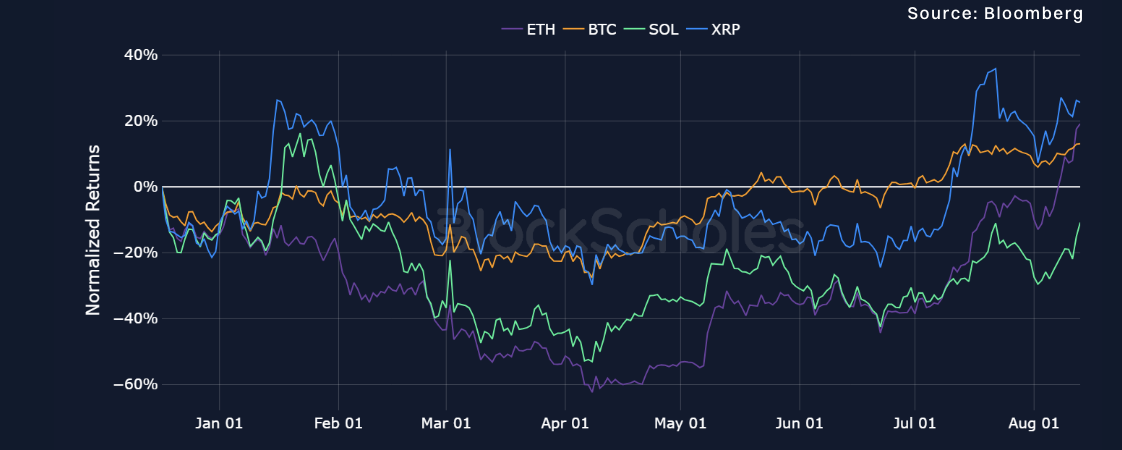

The total market cap of cryptocurrencies has smashed past $4.1T for the first time in history, as altcoins (and ETH in particular) have outperformed BTC. That outperformance has occurred even as BTC just recently touched a new ATH of $124K. Open interest for perpetual swap contracts has risen from $13B to $17B over the past week, its highest level in two months. One major driver of that increase has been a rise in contracts for Ether. In addition, since Aug 6, 2025, perp open interest for BTC contracts has increased from $6.9B to $8B. That increase occurred in two phases — first, when BTC came within inches of its then-$123K ATH on Aug 11, 2025 (though open interest fell as BTC failed to hold that level), and second (more recently) as BTC broke past $124K.

Nonetheless, open interest in ETH perps has risen at a much faster pace, from $3.4B to nearly $6B, as its spot price is trading 23% higher over the past week alone. This rally in ETH has also dented BTC’s dominance (its share of the overall crypto market cap), currently sitting at 57.2%.

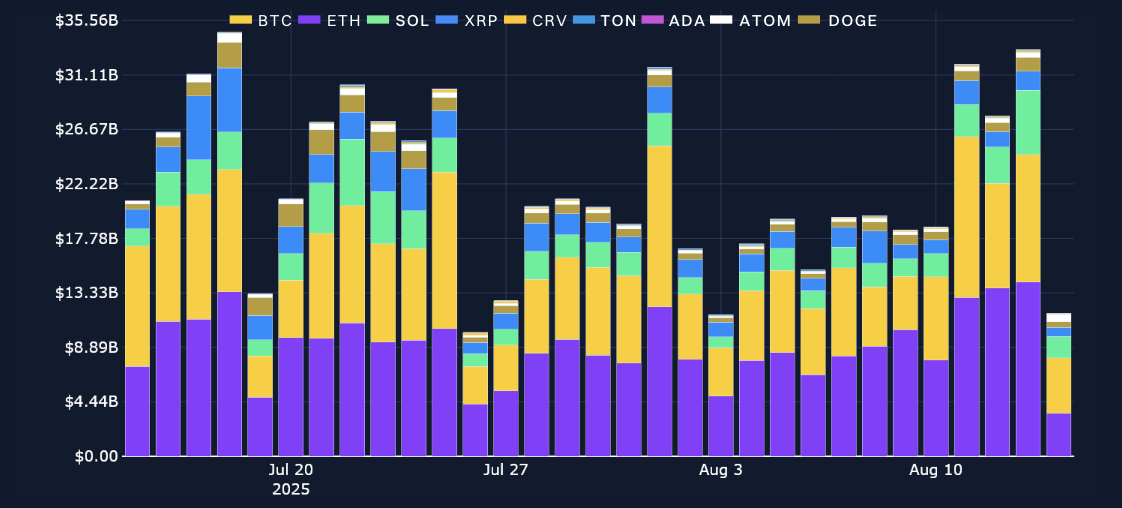

Trade volumes have been consistently above $15B so far in August (on most days, excluding weekends). However, more recently within the week, we’ve seen volumes that have more than doubled, reaching levels closer to the end of July, when BTC initially rallied to $123K.

In line with the current rally in spot prices and the growth of crypto’s total market cap to $4.1T, funding rates across most of the observed tokens are positive. That’s a bullish signal — suggesting that traders believe prices will rise, and are willing to pay a premium to keep their long positions in order to capitalize on that price rise.

At the end of the first week of August, US equity markets were still reacting from the curve ball thrown at them as the US employment report came in weaker than expected, with significant job revisions over the months of May and June. The sinking of US equities took BTC down, too, as its price fell to $112K. However, despite this decline in spot price, funding rates have remained positive. Since then, BTC has made a new ATH and for most of the week has seen consistent positive funding rates. The same can be seen for ETH, which has been bolstered by insatiable demand from digital asset treasury firms and ETH Spot ETFs.

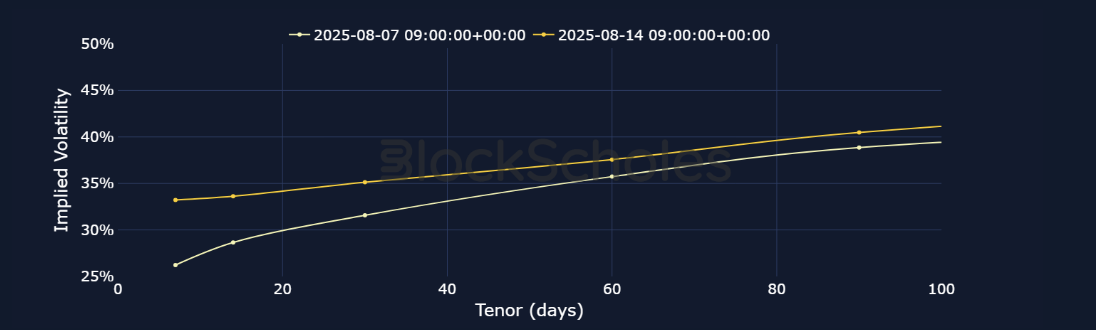

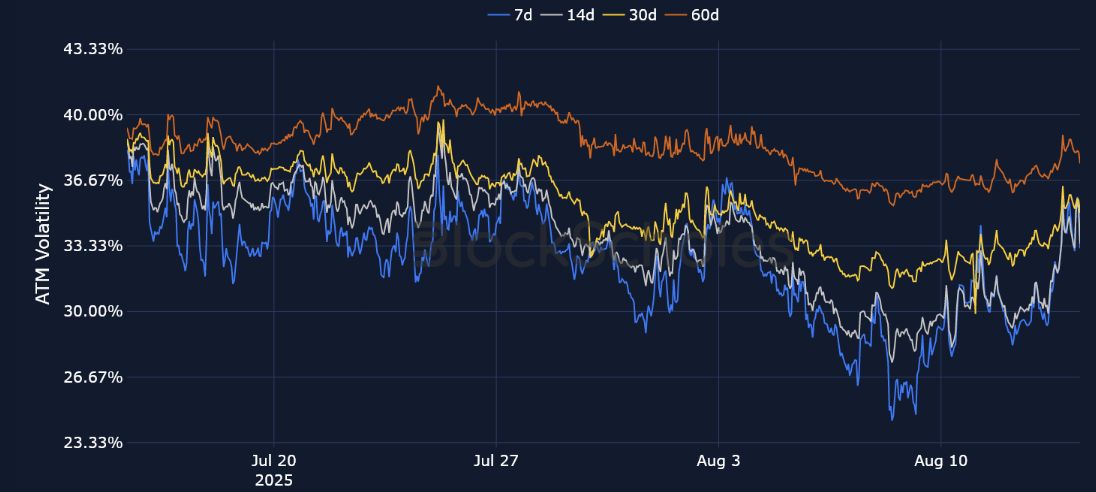

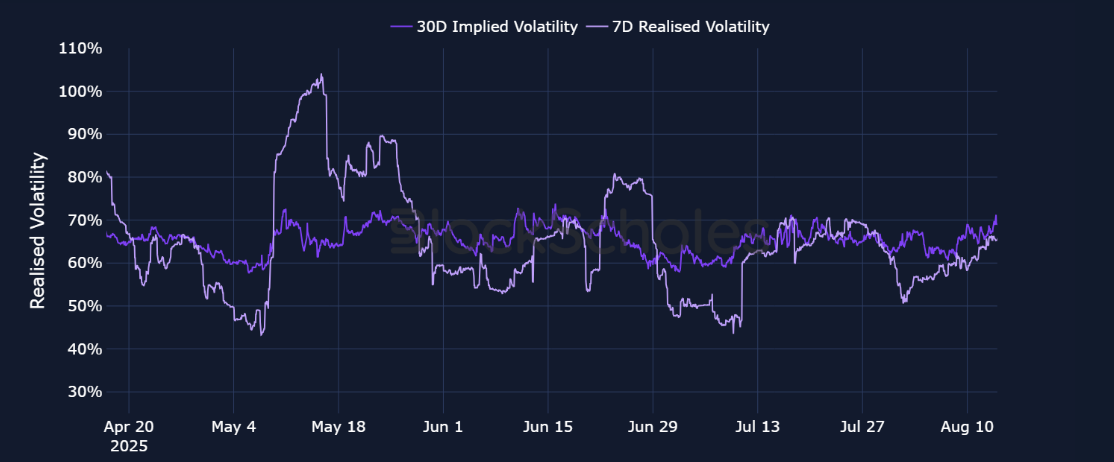

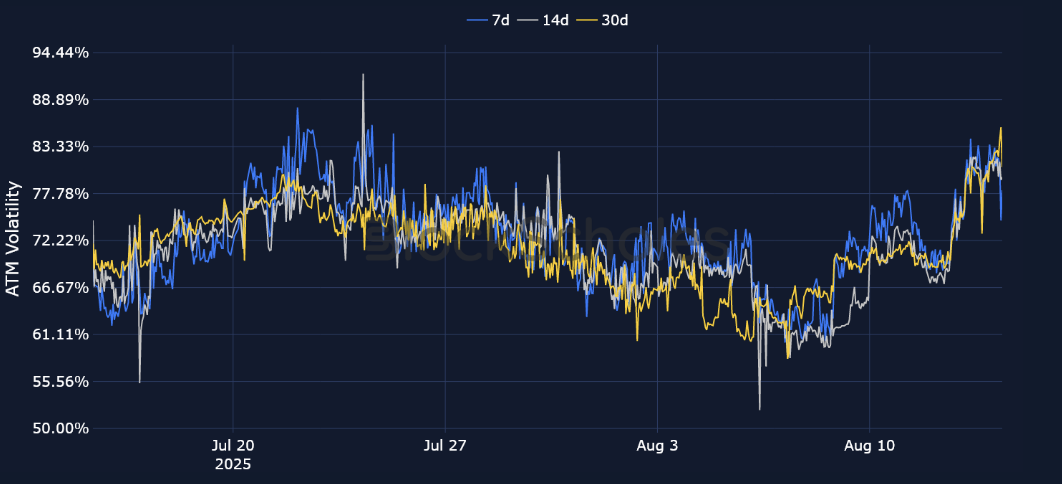

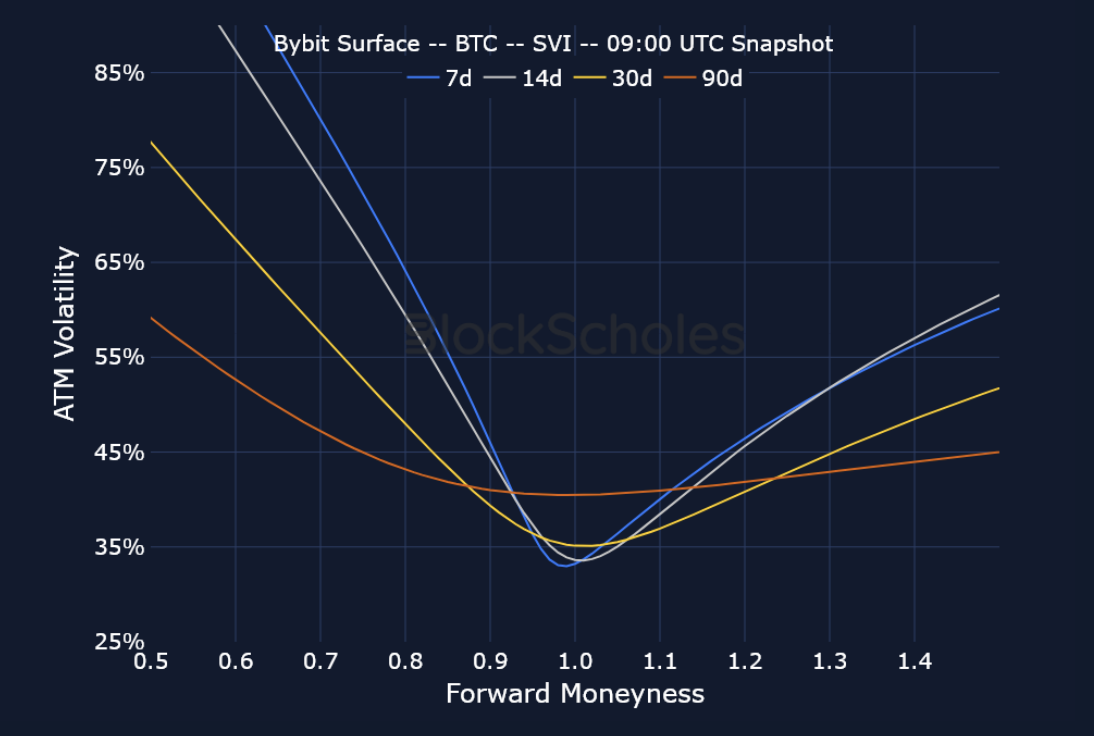

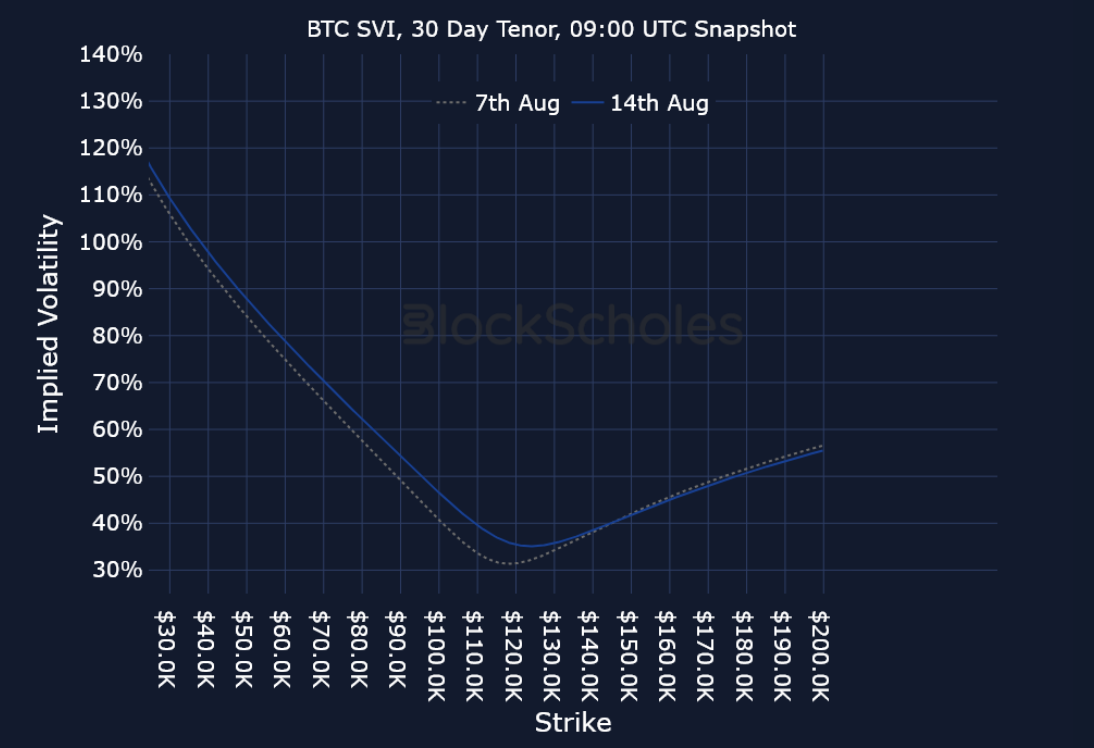

This week, BTC options reversed their downward trend in at-the-money (ATM) implied volatility since the start of August — but not until volatility had hit its lowest levels all month, at 24% on Aug 8, 2025. However, as BTC’s spot price broke through $116K (a level at which it had been trading sideways earlier in the week) and surged to $122K, short-tenor IV spiked higher to 34%. As has often been the case, that jump in short-tenor volatility wasn’t nearly enough to invert the term structure of volatility, and short-tenor IV fell back below 30%.

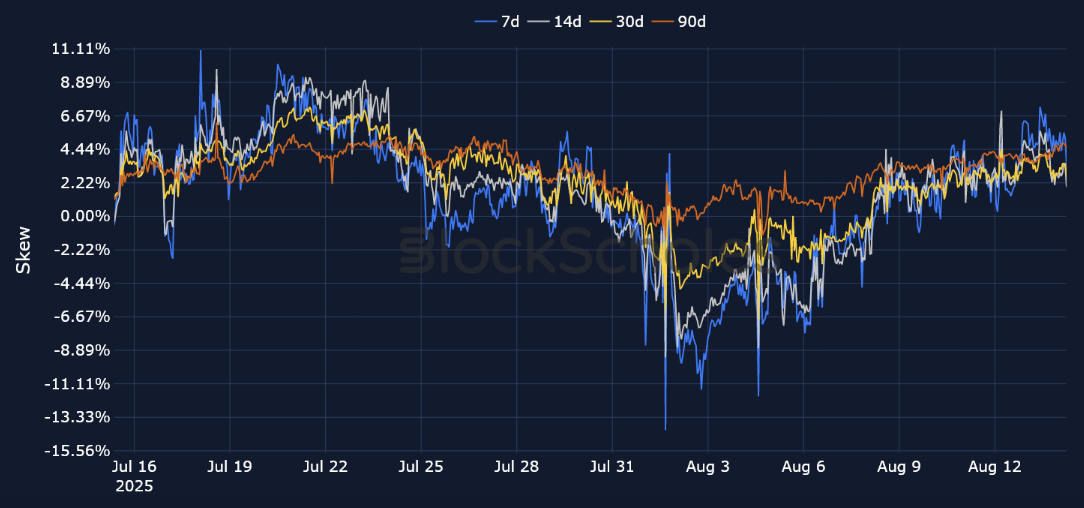

Shortly after, we saw a second spike in front-end volatility as BTC exceeded its July ATH. Volatility smiles skewed toward OTM call options during the rally to $122K, but as BTC failed to hold at these higher levels, markets quickly reversed in their sentiment. Meanwhile, the 7-day put-call skew fell to −2.2% as traders bought up downside protection, though spot price didn’t fall drastically from $122K. Since BTC reached a new ATH, sentiment has once more shifted toward call options for 7-day tenors.

The biggest news so far this week for BTC was President Trump’s signing of an executive order that will allow US retirement plans to invest in alternative assets, including digital assets such as BTC. That opens the digital assets sector to a roughly $8.7T market.

This week, the spotlight in crypto has been on Ether. For much of this cycle, we’ve commented on ETH’s lagging moves and underperformance relative to BTC. However, this week it’s rallied 23% — and, over the past 30 days, a whopping 55%. This means that, year-to-date, ETH has outperformed BTC, and is now trading within a hair of its November 2021 ATH. Compared to that date — and despite being at almost the same price now — this time, the ETH rally has been supported by institutional interest via digital asset treasuries, Spot ETH ETF inflows (which had their first $1B inflow day on Aug 11, 2025) and government regulation, which is pushing stablecoin interest and tokenization toward the Ethereum network.

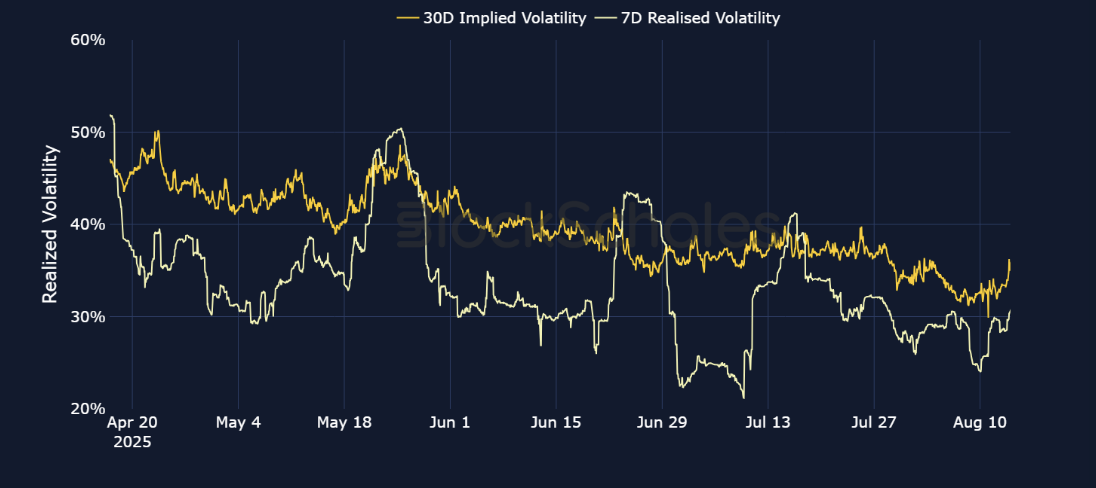

As we commented last week, traders in ETH options are still far more willing to push the front end of the term structure higher during periods of spot market rallies (we saw evidence of this on Aug 10, 2025, as ETH’s term structure briefly inverted). Interestingly, despite huge moves in ETH’s spot price, we haven’t seen a major increase in options volumes, which have averaged $200 million per day this past week.

The typical cycle of capital rotation in previous crypto bull runs has followed a path in which BTC rallies first, and then capital is rotated into ETH and other large-cap altcoins (such as SOL). Recently, the Solana network’s native token has caught a major bid, and is trading 23% higher over the past seven days (and 15% higher in the past 24 hours alone). As such, implied volatility across SOL options has rocketed higher, with 7-day SOL options trading with an IV of 76%.

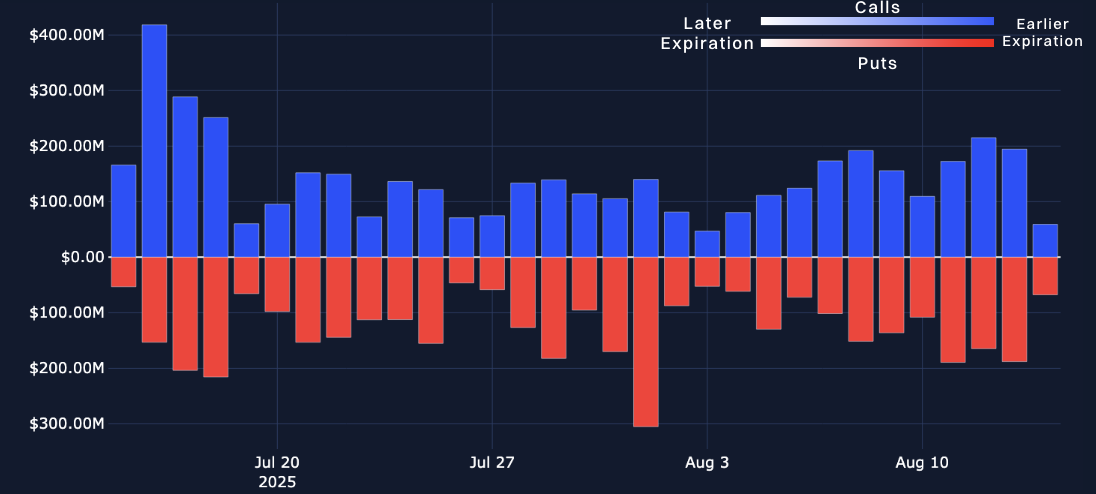

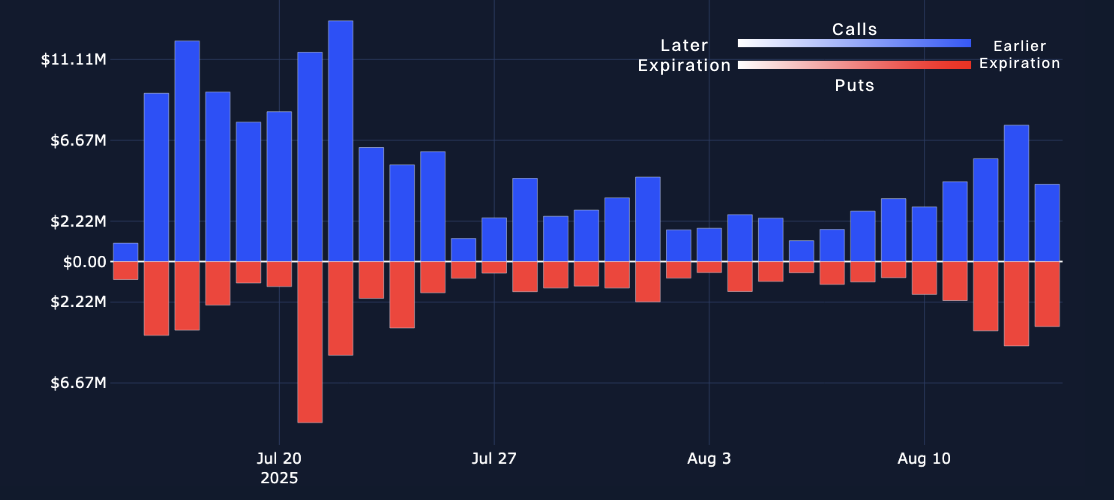

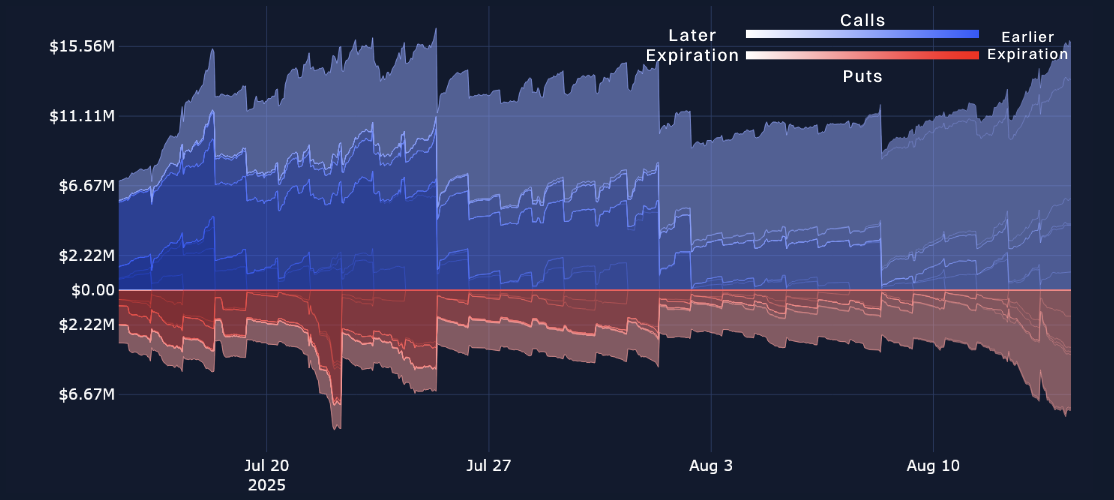

Similar to ETH, however, this rally in spot price hasn’t been met with a major increase in options volumes to the levels seen in late July — a month when SOL and most altcoins also rallied significantly. Open interest for SOL continues to be dominated heavily in call options, as has now become the norm.

ETH’s options market sentiment has turned around completely since the beginning of August 2025. At the start of the month, ETH skew fell to lows of −11% in the aftermath of the weak US jobs report. That meant short-tenor OTM put options carried an 11 percentage-point implied volatility premium over OTM calls of similar maturity. Since then, ETH’s spot price has rallied significantly, and now looks poised to touch its November 2021 ATH of $4,878.

That rally has been strongly supported by institutional appetite for ETH: BitMine, a Bitcoin mining firm–turned–digital asset treasury for ETH, has become the largest holder of the token, with over 1 million Ether held in its reserves. More recently, the firm filed with the SEC to expand its ATM equity program of $4.5B by another $20B to fund further ETH purchases. Other corporate treasuries such as SharpLink Gaming raised $900M in capital over the past week to buy more ETH. This demand crunch is being further amplified by Spot ETH ETFs, which purchased $1B worth of ETH in a single day on Aug 11, 2025.

This strong demand has helped support ETH’s rally to $4,700 and pushed ETH skew to 4.8% in favor of calls for short-tenor options — a strong bullish signal. The same bullish flick is apparent for BTC, too: During the most recent run to a new ATH of $124K, put-call skew sharply shifted from its −1.89% levels, assigning as much as a 3.85% volatility premium to out-of-the-money call options.

Open interest and trading volume data are sourced “as is” from the Bybit exchange platform API exclusively, and as such do not represent a comprehensive picture of the sum of trading activity across all derivatives markets or exchanges. The data visualized in this report consists of hourly and daily snapshots, recorded over the previous 30 days. Daily (hourly) snapshots of trade volume record the total sum of the notional value of trades recorded in the 24H (1 hour) period, beginning with the snapshot timestamp.

If not explicitly labeled as derived from another exchange, the input instrument prices to all derivatives analytics metrics in this report are sourced from the appropriate endpoints of Bybit’s public exchange platform API. In the event that data is labeled or referred to as representing the market on another exchange source, that data is sourced from the appropriate endpoint of each respective exchange’s public API.

Macroeconomic charts and data are sourced “as is” from the Bloomberg Terminal. Exchange data is sourced “as is” from publicly available exchange APIs. Block Scholes makes no claims about the veracity of public third-party data.

After acquisition of underlying-denominated raw data for open interest and trading volume on the Bybit exchange platform from Bybit’s API endpoint, equivalent dollar-denominated figures are calculated using the concurrent value of Block Scholes’s Spot Index for the relevant underlying asset.

Block Scholes’s Spot Index represents the aggregate Spot mid-price for a given currency across the top five CEXs by volume (with USD-quoted markets). It considers the proportion of total volume in the instrument on the exchange, as well as the deviation of a data point from those on other exchanges.

Futures prices are used for Block Scholes’s futures-implied yields calculation services in order to derive the constant-tenor annualized yields displayed in the Futures section of this report.

Options prices are used for Block Scholes’s implied volatility calculation services in order to calibrate volatility surfaces, from which all derivatives volatility analytics displayed in the BTC Options and ETH Options sections of this report are calculated. Volatility smiles are constructed by calibrating to mid-market prices observed in Bybit options markets. As part of the calibration process, prices go through rigorous filtration and cleaning steps, which ensures that the resulting volatility surface is arbitrage-free and has exceptional fit to the market observables.

.jpg)

.jpg)