Thahbib Rahman

Research Analyst

The previous time we evaluated the potential for a crypto altseason, we defined it as a period of significant and sustained outperformance by altcoins (cryptocurrencies other than Bitcoin). Such market regimes have historically begun when Bitcoin dominance reaches a local peak, leading to evidence of capital rotation from Bitcoin into Ethereum, and subsequently into smaller, riskier altcoin projects. This rotation results in rapid price appreciation across altcoins, with many surpassing their previous cycle highs. Altseason ends when the total market capitalization of all altcoins reaches a new all-time high (ATH), often just prior to the broader market peak.

The previous time we evaluated the potential for a crypto altseason, we defined it as a period of significant and sustained outperformance by altcoins (cryptocurrencies other than Bitcoin). Such market regimes have historically begun when Bitcoin dominance reaches a local peak, leading to evidence of capital rotation from Bitcoin into Ethereum, and subsequently into smaller, riskier altcoin projects. This rotation results in rapid price appreciation across altcoins, with many surpassing their previous cycle highs. Altseason ends when the total market capitalization of all altcoins reaches a new all-time high (ATH), often just prior to the broader market peak.

In our previous analysis of altseason conditions, we identified three distinct historical crypto bull runs: 2012–2014, 2015–2018 and 2019–2022. Each of these cycles followed a similar rally-crash-recovery structure, with Bitcoin leading the rallies and reaching new ATHs, with the first two cycles exhibiting distinct altseason periods during which capital flowed out of Bitcoin and into altcoins.

However, the current cycle (2022–present) has delivered multiple new Bitcoin ATHs without a subsequent outperformance in altcoins. The anticipated capital rotation hasn’t occurred in either the same manner or post-halving time period seen in past cycles.

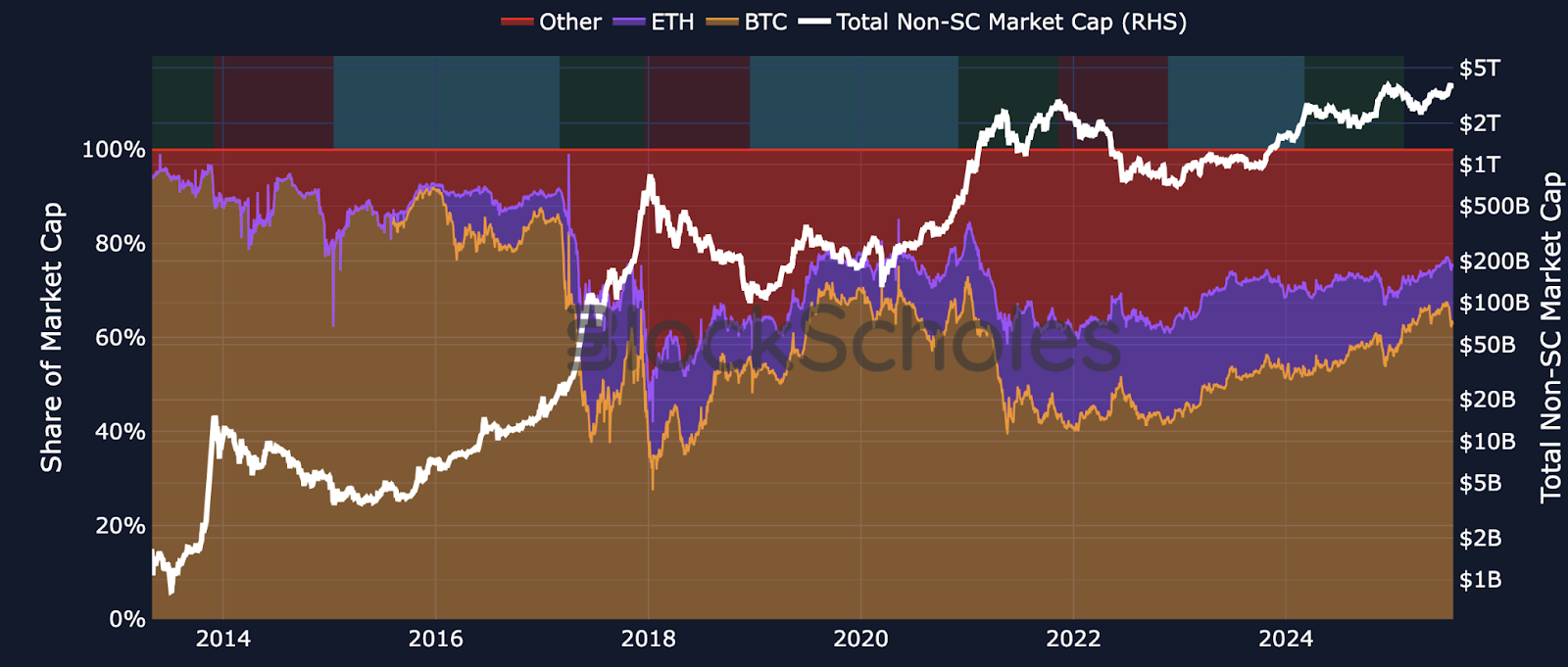

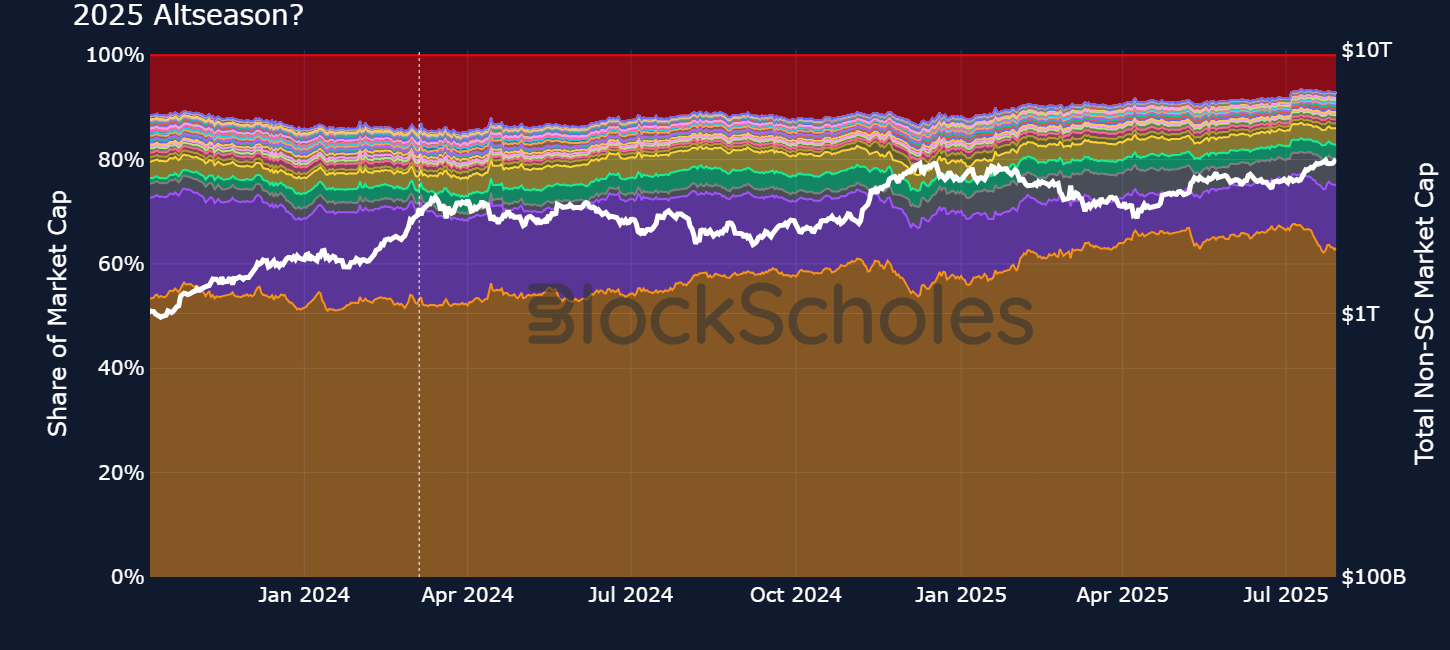

As indicated in the chart below, the market began this current cycle by following historical patterns, moving from a recovery period into new ATHs. However, the duration of new ATHs set by BTC is longer than any seen in prior cycles. Bitcoin is achieving new ATHs and overall crypto market cap is rising in parallel, and yet the sharp drop in BTC dominance, a characteristic typical of altseason, is notably absent in this cycle.

Figure 1. Percentage of total non-stablecoin market capitalization of cryptocurrencies by BTC (orange), ETH (purple) and all other cryptocurrencies (red) from 2013 to July 2025, with total non-stablecoin market capitalization on log scale (white, right-hand axis). Recovery (blue), New ATH (green) and Crash (red) periods are indicated by the color bar at the top of the chart. Sources: CoinGecko, Block Scholes

While the possibility of a delayed altseason remains, it’s certain that this cycle hasn't replicated the timing of previous cycles. Here, we aim to find answers. Is the altcoin season just delayed, or is there something fundamentally different about this cycle?

Far from tumbling in favor of altcoins, Bitcoin’s dominance of total, non-stablecoin market capitalization is currently continuing a strong, steady and upward trajectory. A pronounced decline in Bitcoin dominance has historically been a hallmark of altseason, typically unfolding approximately 230 days post-halving, a point we passed on Dec 5, 2024.

We’ve observed several temporary pullbacks in BTC dominance, however, most notably during a post–US election (on Nov 5, 2024) rally that triggered a market-wide uptick in crypto assets, followed by a relative outperformance in altcoins and a meme coin surge. During this period, Bitcoin’s market share briefly declined by around 6%, which appeared to hint at the early stages of altseason. However, the decline was neither large enough nor sustained to confirm the switch in market regime.

We are now witnessing yet another pullback in BTC dominance — but is the 4% decline simply another short-lived retracement, or does it herald an emerging altseason?

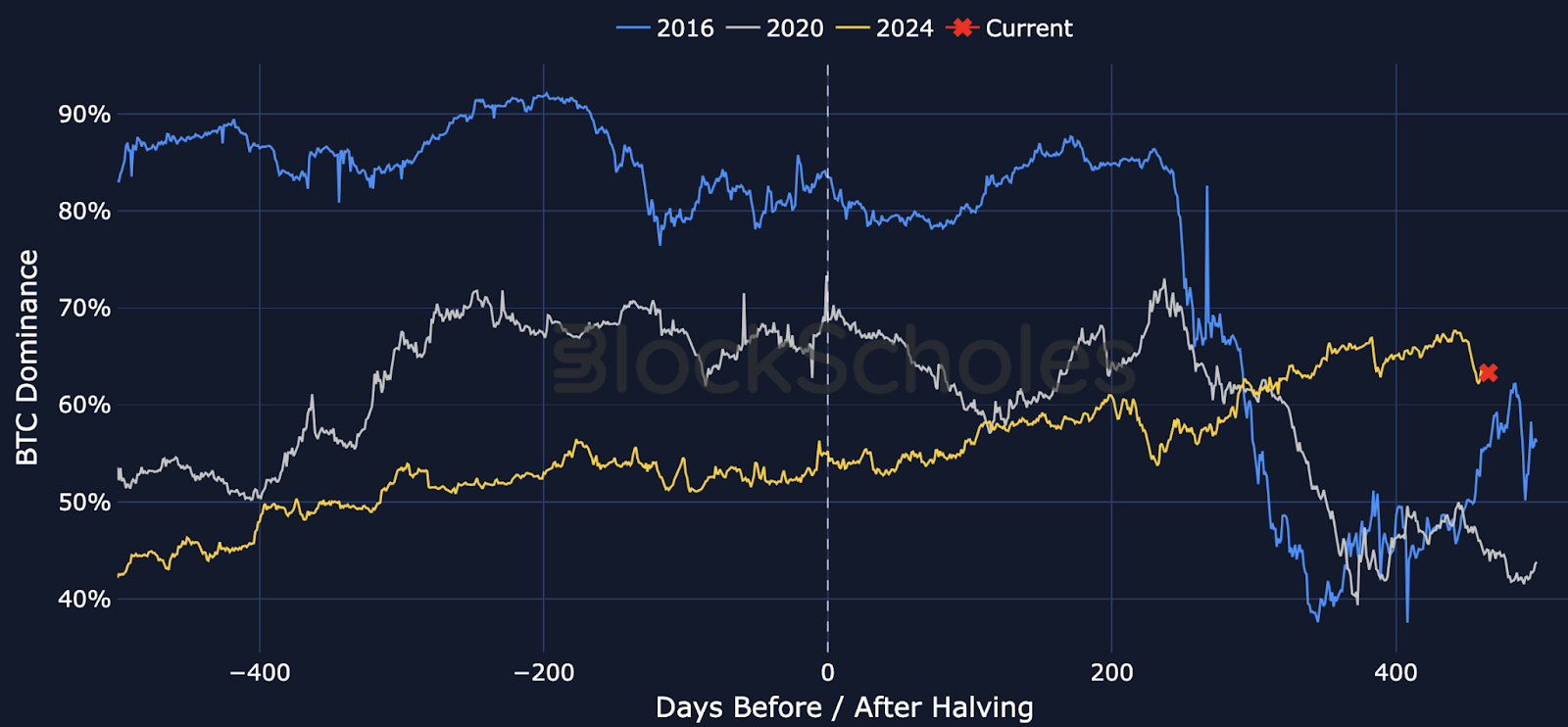

Figure 2. BTC dominance before and after historical halving events (excluding 2012). Sources: CoinGecko, Block Scholes

In previous cycles, BTC dominance was much higher at the time of halving (at over 80% and around 70% in 2016 and 2020, respectively). Interestingly, despite starting from different levels, both the 2016 and 2020 cycles saw dominance fall to roughly 40% before rebounding. Unlike previous cycles, the 2024 halving came with BTC dominance already below 55%, yet it's been climbing steadily, undisturbed. This hints that the so-called four-year cycle might be an illusion of pattern — because as they say, two points make a line, not a trend.

BTC keeps on giving

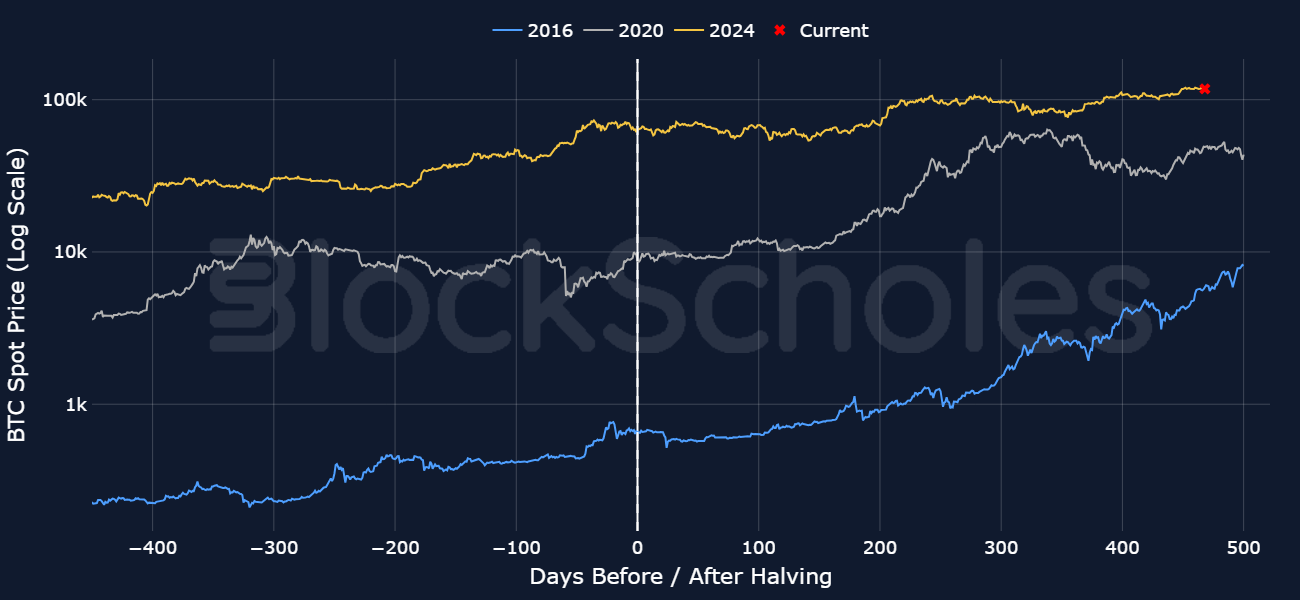

If the altseason is simply delayed, then Bitcoin’s continued delivery of positive returns may be the reason why. Otherwise, why bother rotating capital into other coins when BTC returns are still positive and strong? The asset’s trailing one-year return stands at approximately 79%, significantly outperforming the S&P 500’s 16%. While Bitcoin continues to deliver compelling returns and maintains its lead over traditional benchmarks, the incentive to shift capital into more speculative altcoins remains limited.

Figure 3. BTC spot price returns (log scale) before and after historical halving events (excluding 2012). Sources: CoinGecko, Block Scholes

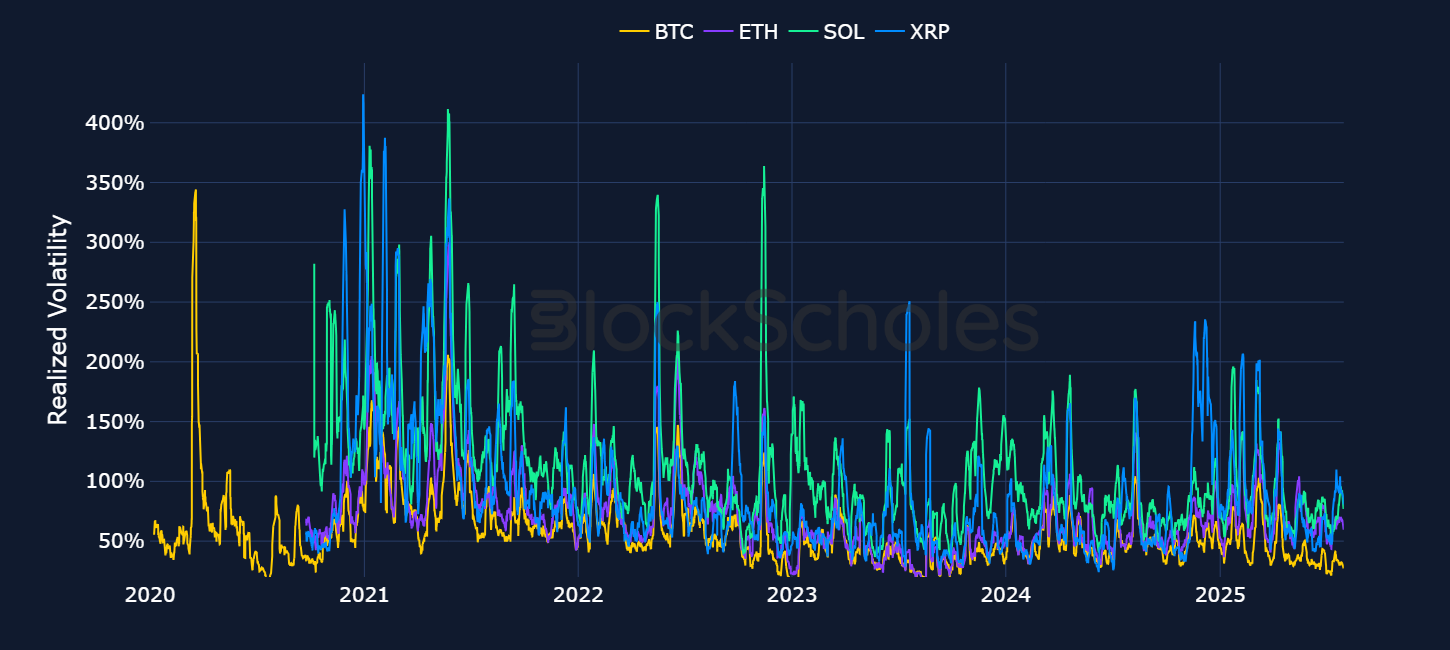

Institutional adoption of Bitcoin is fundamentally reshaping market behavior. Previous analysis suggests that a shift in investor profile has been a key factor in the recent decline of Bitcoin’s realized volatility. The accumulation and persistent demand for Bitcoin reduces abrupt price swings, effectively stabilizing market dynamics through longer-term holding strategies. This includes everything from explicit treasury accumulation strategies from corporate treasuries and governments to more implicit, longer-term holders, such as pension funds and asset managers (also known as “sticky money”).

Figure 4. BTC (orange), ETH (purple), SOL (green) and XRP (blue) realized volatility (7-day lookback window on 60-minute returns). Source: Block Scholes

Rather than being drawn to Bitcoin because of its reduced volatility, these institutional players actually appear to be actively driving that change. This structural influence contrasts with previous cycles, such as in 2020, when demand was more speculative and volatility was exacerbated by macroeconomic uncertainty and monetary tightening. Therefore, the institutional nature of this rally may also be the cause of the delay in the “traditional” capital rotation that we’ve come to expect from crypto rallies.

Figure 5. BTC (orange), ETH (purple), SOL (green) and XRP (blue) normalized returns from April 1, 2025. Sources: CoinGecko, Block Scholes

While the “sticky-money” effect in BTC may be holding back liquidity from flowing into other crypto assets, ETH may still be the first beneficiary if investors decide to rotate to other crypto assets. Indeed, we’ve recently noted that Ethereum has vastly outperformed all large-cap tokens. Since its April lows, ETH has delivered nearly a 100% return, over double BTC’s 40% and a large margin above SOL’s and XRP’s approximately 60% returns. If this is ETH’s moment, it too is over 100 days later than historical precedence would suggest.

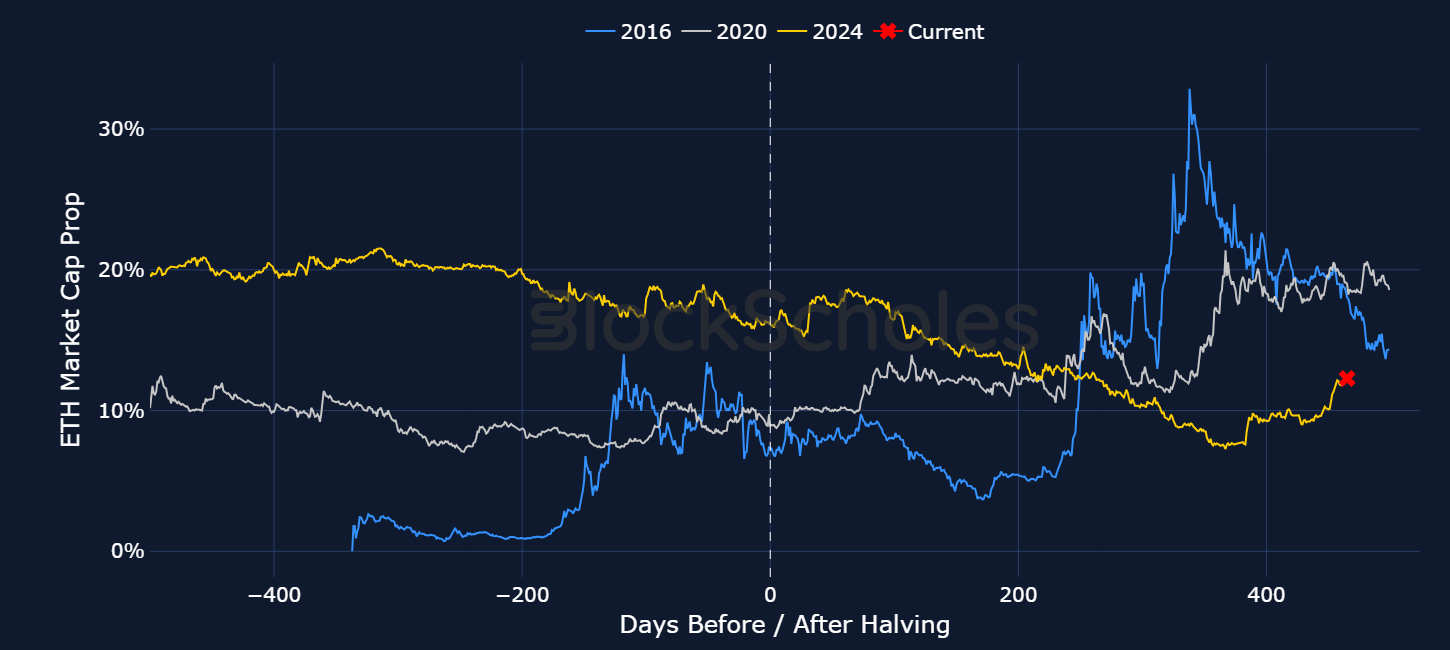

Figure 6. ETH’s proportion of total non-stablecoin crypto market-cap before and after historical halving events (excluding 2012). Sources: CoinGecko, Block Scholes

In isolation, Ethereum’s recent outperformance may appear to fit the textbook definition of an “altseason”: a period marked by sustained and significant gains in altcoins relative to Bitcoin, typically accompanied by broad-based price appreciation across the altcoin market. However, this narrative doesn’t fully align with current market dynamics. Despite ETH’s strength, its price remains well below previous ATHs, and the broader altcoin market hasn’t demonstrated the widespread speculative momentum that’s characteristic of sustained altcoin outperformance.

And yet, when analyzing ETH’s market share as a proportion of Bitcoin and ETH’s combined market cap, we can in fact see that this is not an ETH rally, but instead a recovery.

Figure 7. ETH (blue) and BTC (orange) relative market-cap share. Sources: CoinGecko, Block Scholes

During the April 2025 market downturn, it became clear that Ether’s ability to outperform was contingent on the alignment of key fundamentals, including network optimization and regulatory clarity for the token. As those conditions materialized, ETH’s spot price responded accordingly.

Network optimization was delivered via the successful deployment of the Pectra upgrade to the Ethereum Mainnet on May 7, 2025. Additionally, investor confidence has been supported by the Ethereum Foundation’s ongoing internal restructuring, which is aimed at aligning its operational focus. The renewed strategic direction of focusing on three core network goals — scaling the base layer, advancing Layer 2 infrastructure and enhancing user experience — reinforces Ethereum’s long-term value proposition.

Long-awaited legal clarity was also delivered in late May 2025, when the US Securities and Exchange Commission (SEC) clarified that certain proof of stake (PoS) staking activities do not constitute securities transactions under federal law. This reduces regulatory risk for institutional holders while enhancing the appeal of PoS token investments (such as ETH) by offering higher yields.

Therefore, while the institutional nature of this rally may be holding capital back from entering other assets, it may well be institutional interest in Ethereum and other Layer 1s that’s driving the beginning of an “institutional altseason.”

We’ve already seen the impact that ETF buying activity has had since its adoption on BTC’s volatility levels. It’s also possible that trading behavior via ETFs will impact the typical market flow of capital as it has in the past. Has institutional interest changed Bitcoin’s role in the market in this cycle?

Besides macro factors, every crypto altseason has had idiosyncratic drivers and/or new participants to ignite it. In 2017, it was the prospect of PoS blockchains and initial coin offerings (ICOs) of various different types of crypto tokens that set off the altseason. In 2021, it was the promise of DeFi and, within that, specific subcategories, such as interest in the metaverse and NFTs. It’s obvious that this cycle is different, since BTC’s price rally this time around began with the entrance of spot ETFs (or institutional buyers), and has been extended by continued positive developments in the regulatory environment.

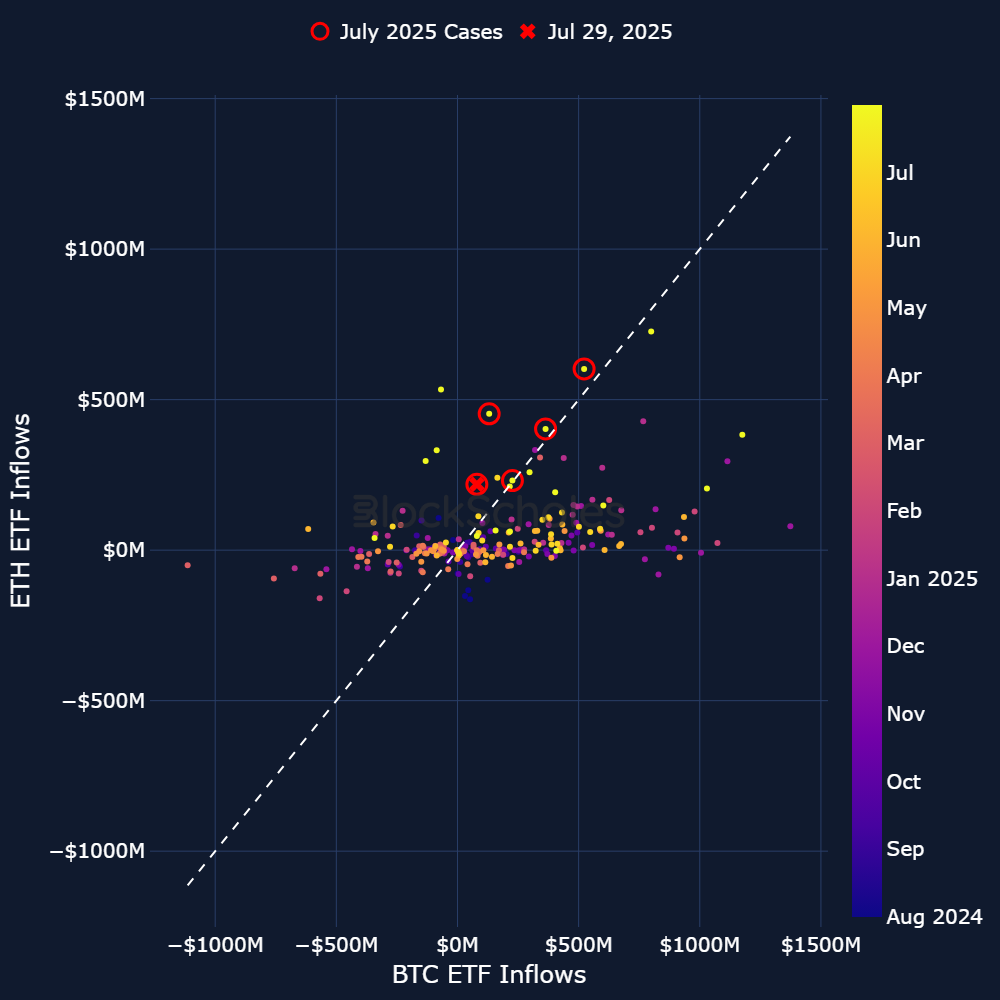

So if institutions are a big cause for the rally, could we see spot ETF investors switching to ETH ETFs to kick-start the capital rotation needed for an altseason? If so, we may have seen the beginning signs already. ETH Spot ETFs recently began to overtake BTC Spot ETFs in daily inflows. Since the launch of both products, there have only been nine trading days when ETH Spot ETFs outperformed BTC Spot ETFs on days when both products had positive net flows. Of those nine days, five occurred in July 2025 alone.

Figure 8. Scatter plot of Spot BTC ETF inflows and Spot ETH ETF inflows. Sources: Farside Investors, Block Scholes

Should that trend continue, it could be an early sign that the walled garden of Spot BTC ETFs is perhaps not as isolated as many expected would be the case — and that institutional investors are willing to rotate their capital away from BTC and into ETH.

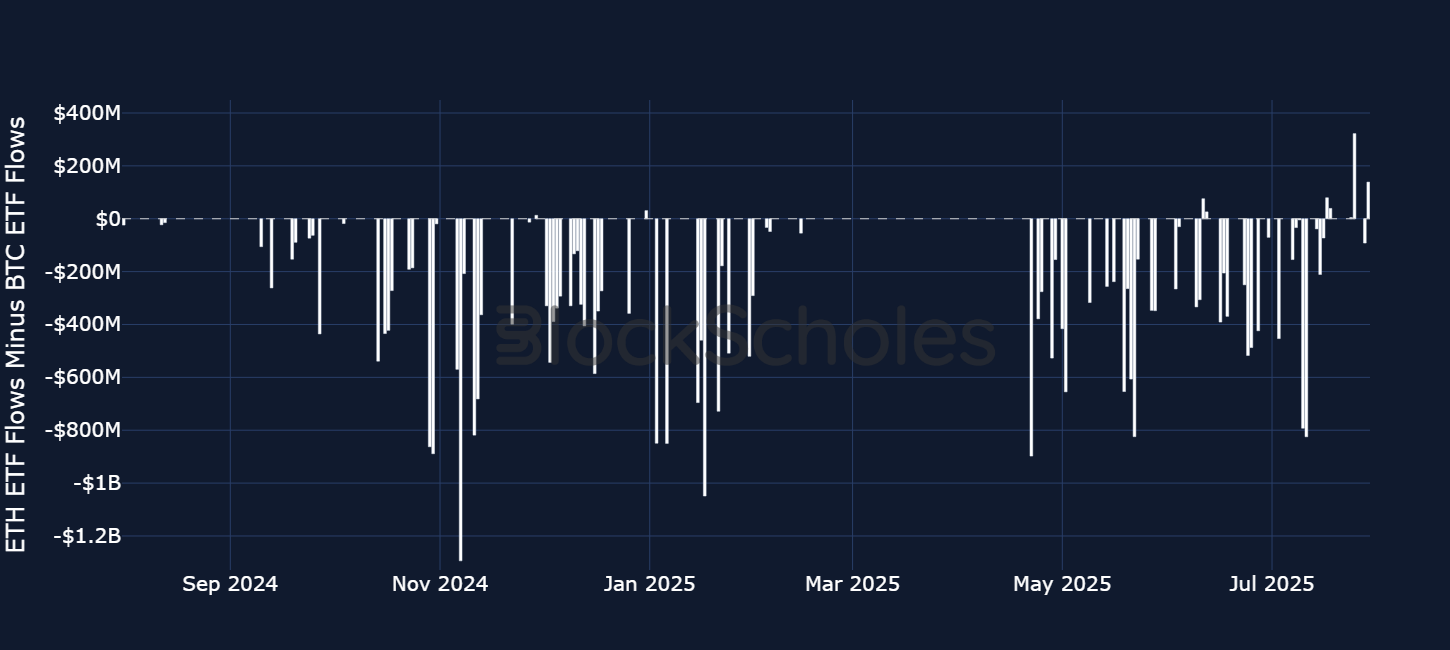

Figure 9. Net Spot ETH ETF flows minus net Spot BTC ETF flows since launch. Sources: Farside Investors, Block Scholes

Initially, when BTC and ETH Spot ETFs were first launched, institutions showed a strong preference for BTC. The ETH ETF products had very little to distinguish themselves from the most well-known cryptocurrency, Bitcoin; and institutional traders who (for the first time) had the opportunity to get exposure to the crypto market largely chose to do so via Bitcoin. However, huge changes in the regulatory landscape have now set the stage for investors to find a unique distinguishing reason to get exposure to Ether, either alongside or instead of Bitcoin.

First, the passing of the GENIUS Act, which we covered here, provides the first proper guardrails for stablecoins in the US, an industry with a market cap of $250B. Half of that supply is in the Ethereum network alone, as more institutions look to build on Ethereum or launch stablecoins, it provides an obvious demand reason to hold Ether — it’s the gas token that powers transactions on the Ethereum network. Secondly, the SEC’s continued push toward tokenization — most recently via Chair Paul Atkin’s announcement of “Project Crypto,” defined as “a Commission-wide initiative to modernize the securities rules and regulations to enable America’s financial markets to move on-chain” — will also likely take place on Ethereum. We find signs that it already has.

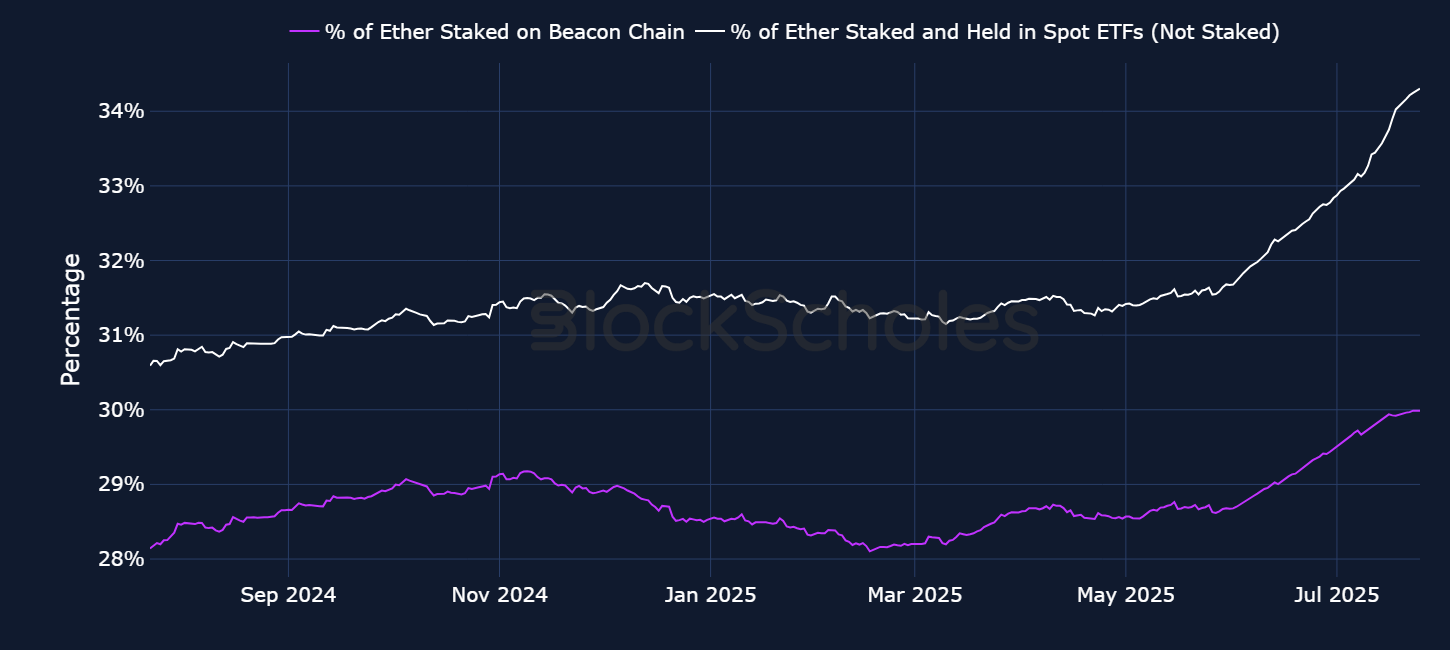

Finally — and perhaps one of the biggest catalysts for a potential capital rotation out of BTC and into ETH — is the growing confidence that the SEC will approve staking-enabled Spot ETH ETFs, which will then provide investors a staking yield on top of spot exposure. That confidence is supported by the fact that the SEC has already approved a staking-enabled ETF for Solana.

Figure 10. Percentage of Ether staked on the beacon chain relative to circulating Ether supply (purple) and sum of Ether staked and Ether held in Spot ETH ETFs (not staked) relative to circulating Ether supply (white). Sources: Artemis, Block Scholes

We’ve been strong proponents of the view that Bitcoin is driven by three fundamental drivers: the macro environment, regulatory developments and supply-and-demand factors. The confluence of these drivers has already pushed BTC to highs of $123K, setting the scene for traders to take their profits from BTC and push that capital further along the risk curve into other altcoins.

However, we expect that in order for traders to continue pushing their capital into riskier assets (altcoins or meme coins) in search of further returns, a wider risk-on sentiment across financial markets is needed. Without that confidence, it’s difficult to see an aggressive capital rotation out of BTC into riskier altcoins.

So, what exactly are the conditions needed for risk-on sentiment, and a potential altseason — and how close are we to those conditions? We expect that the macro conditions supportive of an altcoin season or prolonged period of altcoin outperformance are as follows:

That in mind, let’s ask: What are current macroeconomic conditions suggesting?

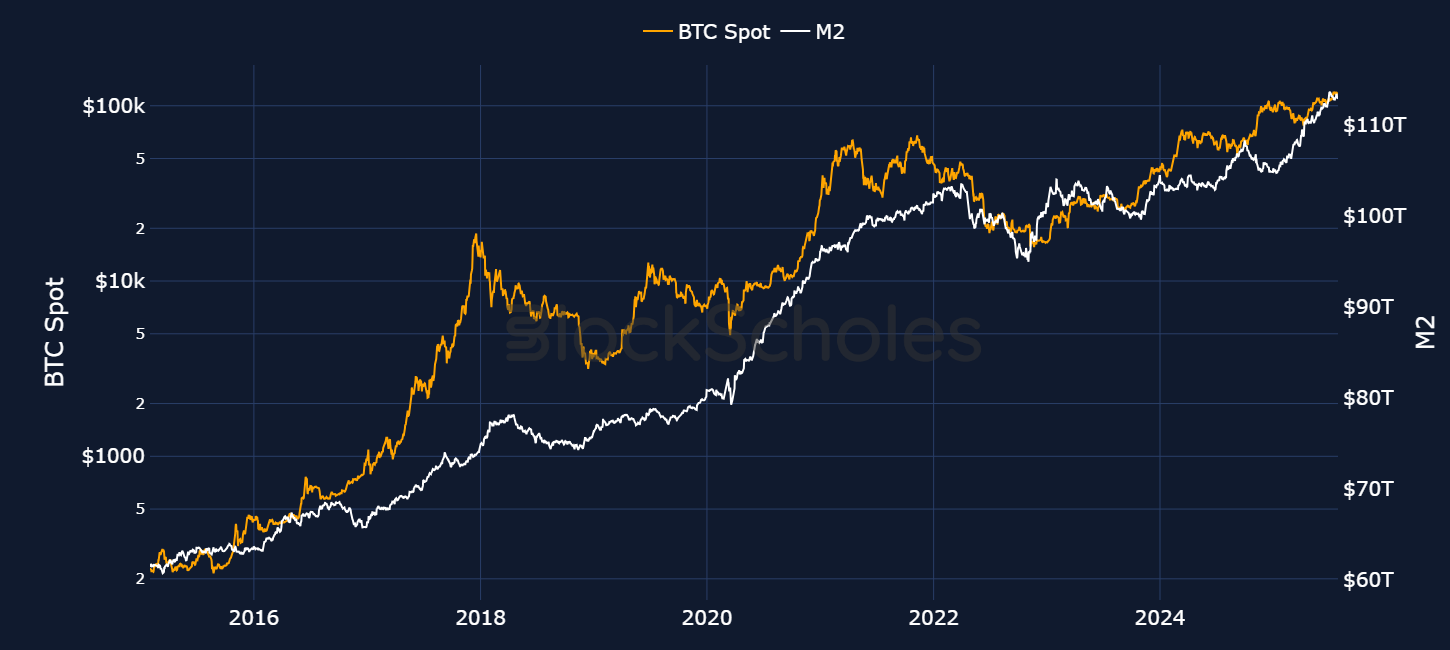

Higher global liquidity levels provide a favorable macro backdrop for risk appetite, because the more liquidity sloshing around in the financial system, the greater the opportunity for that liquidity to be parked into different assets or asset classes. However, higher liquidity levels alongside an environment of lower interest rates mean that more capital finds itself spreading into risk-on assets that provide a larger rate of return than, for example, the “risk-free rate” provided by US treasuries.

One case study of how a confluence of these two factors supported a major altcoin season was during the 2020–2021 crypto cycle, when an easing of monetary conditions and an increase in global liquidity pushed prices to several new highs. Subsequent tapering in the increase of global liquidity aligned broadly with the tops of Bitcoin price cycles.

Figure 11. BTC daily spot price, log-scale (orange, left-hand axis) and global liquidity levels measured in USD (white, right-hand axis). Sources: Block Scholes, Bloomberg

Since late 2024, we’ve seen global liquidity levels increase once again. We can measure these levels using M2 money supply — defined as a broad measure of liquidity that includes cash, checking deposits, savings accounts, and money market funds denominated in US dollars across the largest economies in the world. The M2 metric is at an ATH and growing, although it has risen at a moderately slower pace than four years ago.

In the chart below, we’ve plotted global liquidity levels as before, but this time alongside BTC dominance. What we find is that sharp moves downward in BTC dominance have also occurred during times of accelerating liquidity levels. For example, take 2017–2018, when a $10T increase in M2 was met with a more than 40% drop in BTC dominance. The 2020–21 period followed a similar pattern. Unlike both of these cases, the current cycle has yet to see that same downward crash in BTC dominance.

Figure 12. BTC dominance, log-scale (orange, left-hand axis) and global liquidity levels measured in USD (white, right-hand axis). Sources: Block Scholes, Bloomberg

However, assuming the Fed eventually resumes its cutting cycle, we may see the opportunity for an acceleration in easier liquidity conditions. Despite the fact that Fed Chair Jerome Powell’s FOMC committee voted on Jul 30, 2025 to keep interest rates on hold for a fifth consecutive meeting, citing uncertainty over the extent of tariff-induced inflation, markets are still pricing for a resumption of rate cuts before the end of the year. According to 30-day Fed funds futures, the probability of a September cut increased to 78.7% on Aug 1, 2025 from 37.7% a day earlier, as significantly weaker-than-expected jobs data was released in the US.

Therefore, the market is once more pricing in for two more cuts in the remaining three meetings for the year. As monetary policy moves interest rates lower, these easier capital conditions and increased liquidity will act as a net positive for risk-on assets.

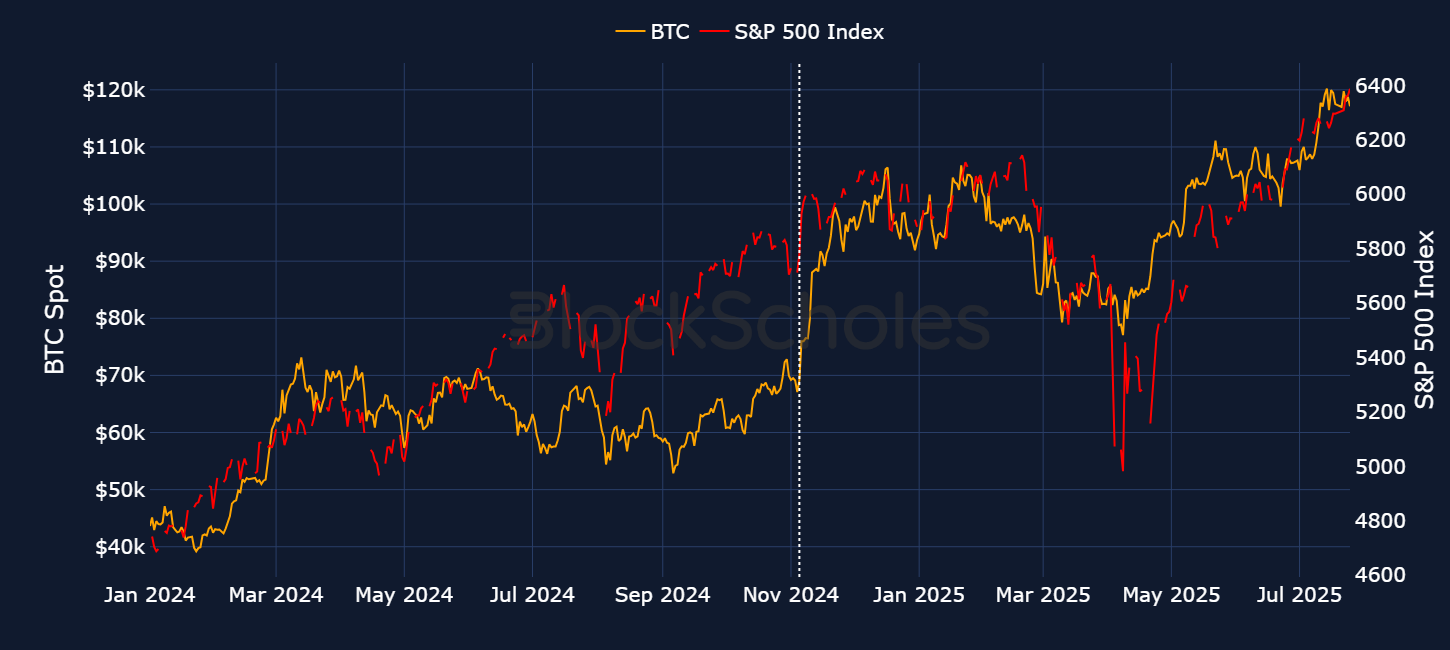

Has the increase in global liquidity translated into a measurable change in risk appetite in other markets? Despite navigating many ups and downs between Trump’s election victory and the present day, the S&P 500 is now trading close to ATHs, and is up more than 8% year-to-date.

Figure 13. BTC spot price (orange, left-hand axis) and S&P 500 (red, right-hand axis) since January 2024, with vertical dotted line marking the US 2024 November election. Sources: Block Scholes, Bloomberg

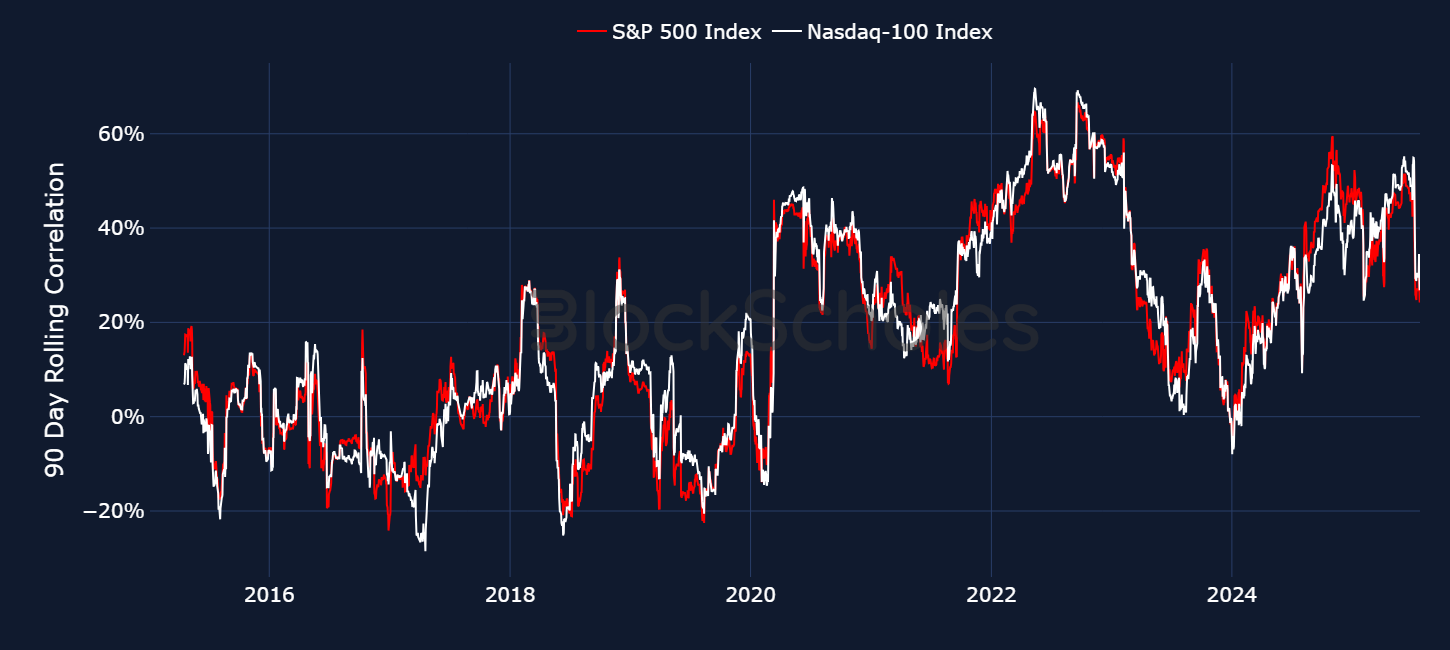

That move higher in US equities is taking place while BTC’s correlation with risk-on US stocks is still close to its ATH. The 90-day rolling correlation of BTC returns with both the S&P 500 and Nasdaq-100 is above 0.5.

Figure 14. 90-day rolling correlation between BTC daily returns and SPX daily returns (red) and BTC daily returns and NDX daily returns (white). Sources: Block Scholes, Bloomberg

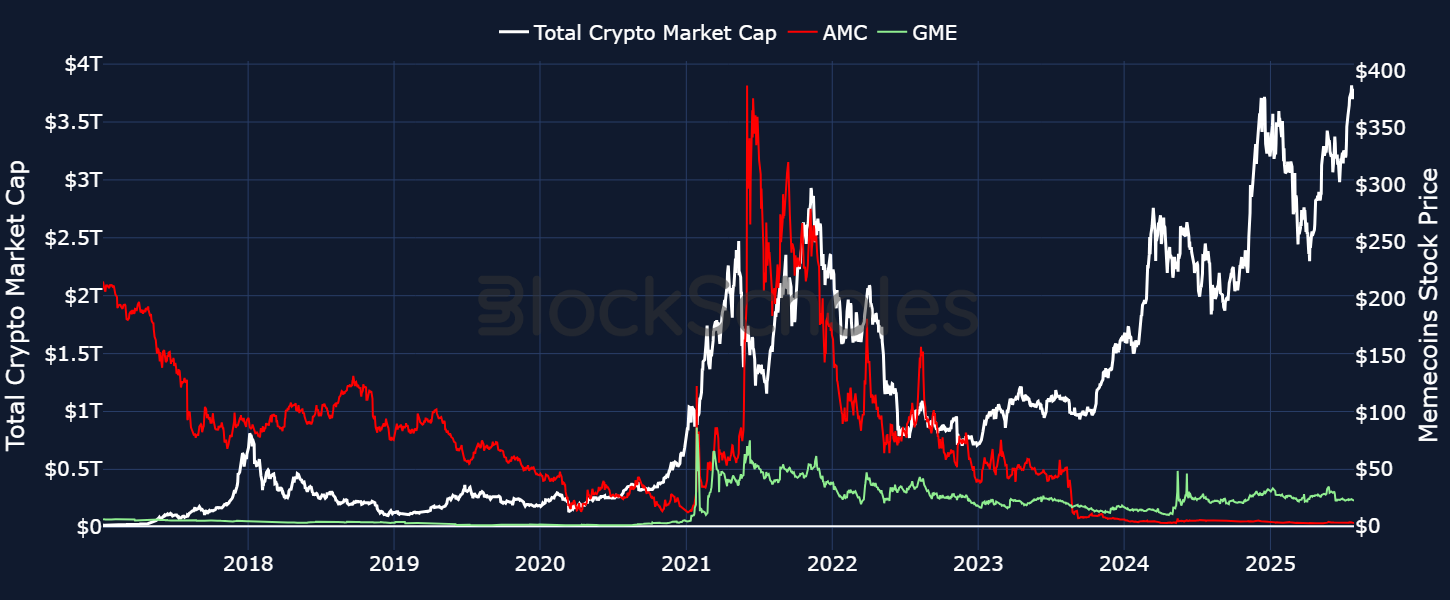

Additionally, we’re seeing glimmers of the resurgence of another indicator of markets championing risk-on sentiment — a rally in meme stocks. In 2021, meme-stock mania took place as traders on forums such as WallStreetBets (WSB) on Reddit piled into various equity tickers in the hopes of driving them higher. Among the most well-known meme stocks were AMC Entertainment Holdings Inc (AMC) and GameStop Corp (GME). In fact, in that period of 2021, we found evidence that capital rotated out of BTC and into profitable meme stocks, with the two categories of assets recording peaks in cycles distinct to BTC.

Figure 15. BTC spot price (orange, left-hand axis) and select meme stock prices, AMC (red, right-hand axis) and GME (green, right-hand axis). Sources: Block Scholes, Bloomberg

The multiple peaks in GME and AMC in 2021 actually took place around the same period when altcoins reached their first peak in total market capitalization (in May of that year), although we also saw evidence of capital rotating back and forth between meme stocks and meme coins.

Figure 16. Total non-stablecoin crypto market-cap (white, left-hand axis) and select meme stock prices, AMC (red, right-hand axis) and GME (green, right-hand axis). Sources: Block Scholes, Bloomberg

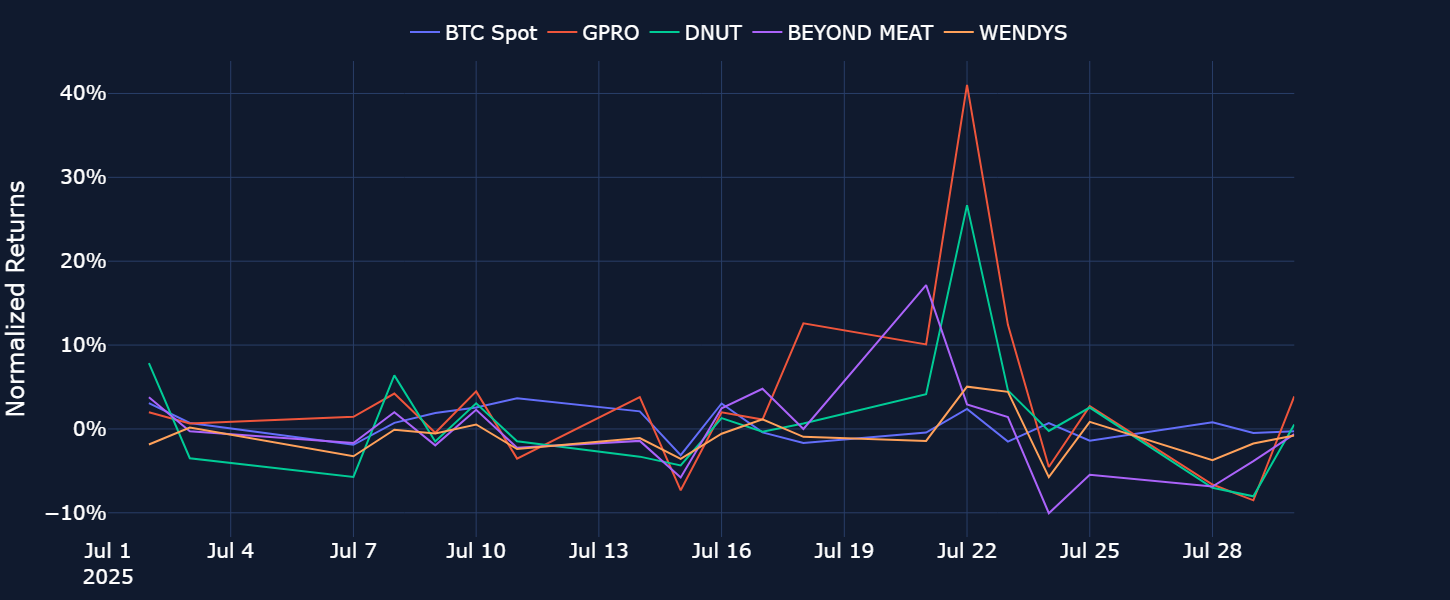

Fast-forward to the present day — and we find that a frenzy of meme stocks recently erupted in mid-July 2025, fueled by the same category of retail participants on Reddit and other online chat forums as four years ago. As shown below, a basket of meme equities — including GoPro Inc (GPRO), Krispy Kreme Inc (DNUT) and Beyond Meat Inc (BYND) — all broke out at once, despite little if any change to their underlying business. That’s another indication from markets that sentiment is very much on the upper boundaries of speculation.

Figure 17. Normalized returns of BTC and select meme stocks from July 2025. Sources: Block Scholes, Bloomberg

There’s one elephant room that needs to be addressed when it comes to the macro set-up — the US president’s favorite word, tariffs. The initial impact of tariffs on crypto and risk assets alike was extraordinary. BTC dropped to levels as low as $75K, while the S&P 500 recorded some of its biggest intraday losses since the 2008 and 2020 market crashes. This was largely due to the uncertainty around exactly what the impact of tariffs would be on the economy, as well as the erratic nature of Trump’s policymaking when it comes to setting the tariff rates.

However, over time, the uncertainty that was negatively impacting risk-on sentiment has started to wane as Trump continues to sign new trade deals with US partners. As such, both BTC and the S&P 500 are back trading close to their record highs, with the latter rallying nearly 30% from its April lows.

Figure 18. BTC spot price (orange, left-hand axis) and ETH spot price (purple, right-hand axis), with select macro-related events marked as vertical dotted lines. Source: Block Scholes

In the above chart, the vertical dotted lines correspond with the following tariff- or macro-related events, presented here in chronological order:

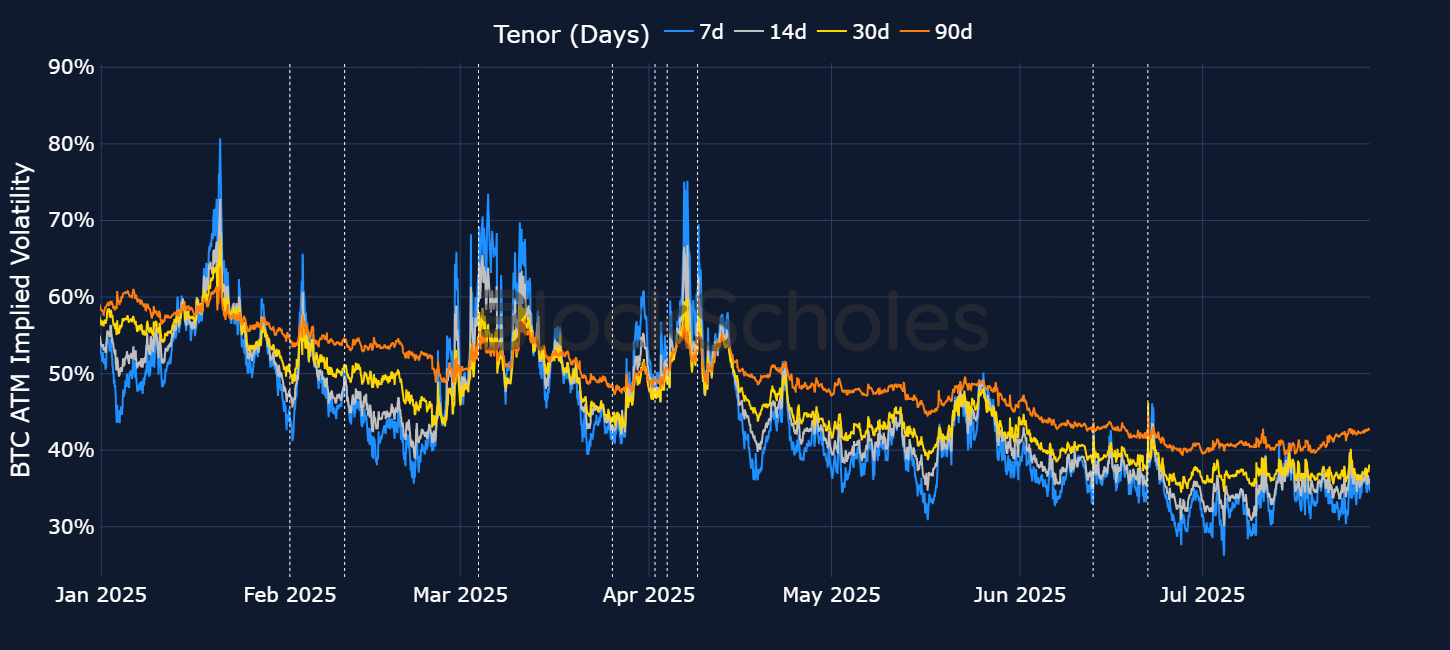

We can see that BTC and ETH fell lower (alongside other risk-on assets such as US equities) with each and every tariff announcement. Below, we plot the implied volatility of at-the-money BTC options at several constant tenors, marked with the same tariff announcements, as this is a key indicator of the uncertainty faced by the market over this period.

Interestingly, that measure of uncertainty or risk has been falling over the same period. Earlier in the year, tariff announcements would sharply invert BTC’s term structure of volatility; short-tenor IV would trade much higher than long-tenor options, as investors rush to options markets for protection against market moves. Those inversions have abated over time. During the peak of the Iran-Israel conflict (itself a major macro development), even as the US struck three key Iranian nuclear sites, BTC’s term structure failed to invert.

Figure 19. BTC at-the-money options’ implied volatility at several constant tenors, with select macro-related events marked as vertical dotted lines. Source: Block Scholes

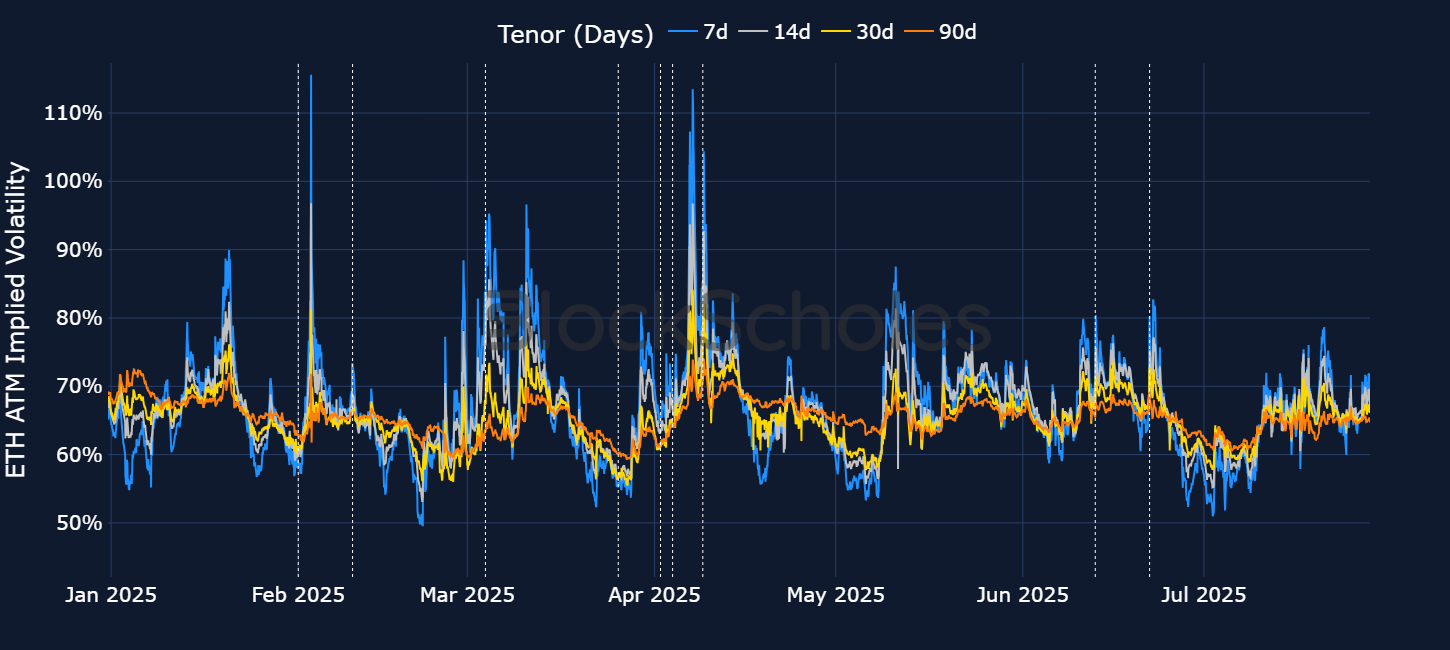

While term structure inversions for BTC have become rarer with tariff-induced volatility in the markets, for ETH such term structure inversions are common. However, the intensity of those inversions has eased over time — again an indication that tariffs, at least, may be having a smaller effect on implied volatility.

Figure 20. ETH at-the-money options’ implied volatility at several constant tenors, with select macro-related events marked as vertical dotted lines. Source: Block Scholes

The president himself perhaps knows the impact his tariff policies can have on the market, telling the market to buy stocks ahead of positive tariff announcements (such as a pause or willingness to negotiate). As such, these events have marked perfect local bottoms.

Figure 21. BTC spot price (orange, left-hand axis) and S&P 500 (red, right-hand axis) since January 2025, with vertical dotted lines corresponding to market-related comments from President Trump. Source: Block Scholes

Nonetheless, while tariffs have had minimal impact so far on the US economy (or namely, on inflation), the signs are emerging. Various Fed members, including Chair Powell, have been vocal that recent increases in core goods inflation — an aspect of the inflation basket that just a few years ago was “well behaved,” according to Powell — is likely to continue to move higher. That, in turn, may further slow down the cutting cycle of the Fed and delay any easing of financial conditions.

Ultimately, despite the initial signs of an altcoin season on the horizon, this wouldn’t be the first time in the current crypto cycle that BTC dominance initially has fallen before quickly recovering and stopping an altcoin rally (to the extent we’ve previously seen). For now, the major drop in BTC’s market cap share — and its subsequent aggressive increase in total non-stablecoin market cap — have yet to materialize.

Figure 22. Percentage of total non-stablecoin market capitalization of cryptocurrencies by BTC (orange), ETH (purple) and all other cryptocurrencies (red) from November 2023 to February 2025, with total non-stablecoin market capitalization on log scale (white, right-hand axis). Sources: CoinGecko, Block Scholes

So how are derivatives markets positioned currently — and what indicators can we watch to stay attentive to a prolonged period of altcoin outperformance?

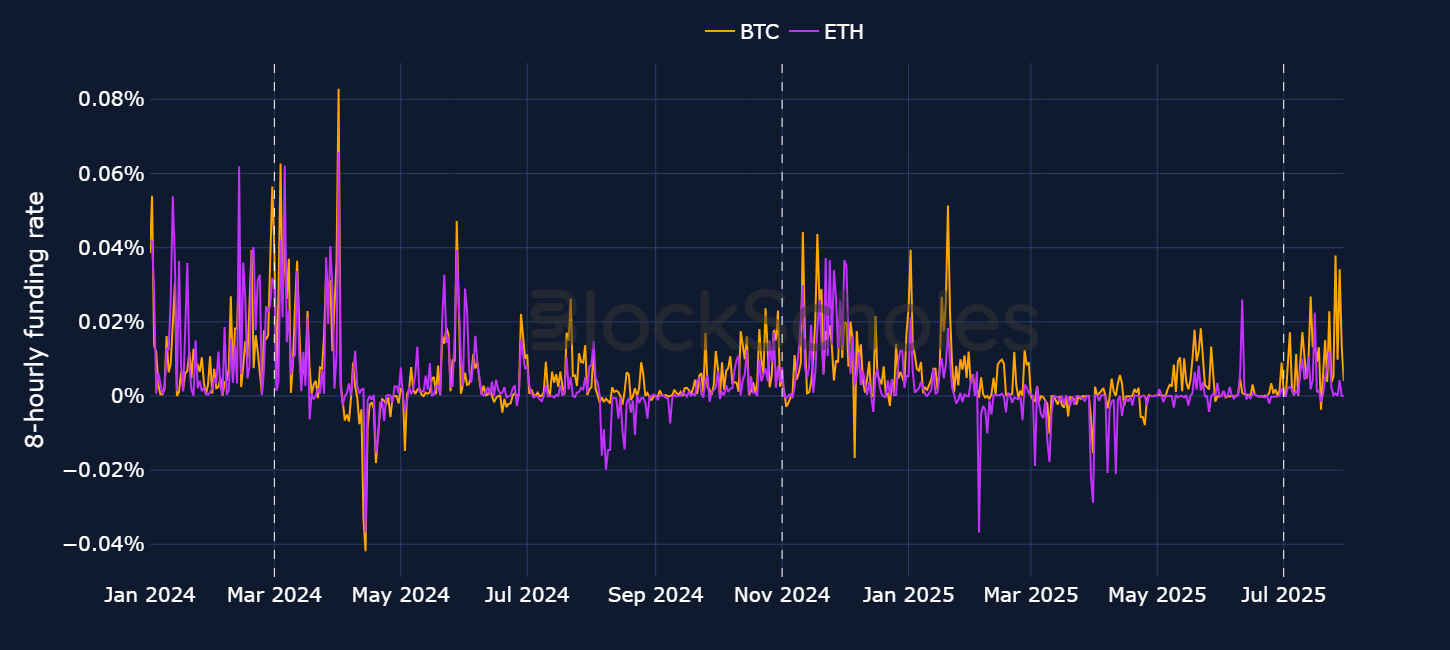

In the chart below, we plot BTC funding rates (a key indicator of leveraged bullish positioning in perpetual swap markets) on an hourly basis since January 2024, when BTC Spot ETFs were launched. Also marked on the chart are two dates since that period when markets began to heat up, and clamors of altseason were circulating, as well as a third date for July 2025, the most recent period of altcoin outperformance.

Figure 23. BTC (orange) and ETH (purple) hourly perpetual swap funding rates since January 2024, with vertical dotted lines marked on select periods of altcoins outperformance. Source: Block Scholes

It’s quite clear that the euphoric sentiment in ETH funding rates — both in the March and November 2024 rallies — have yet to be revisited. Funding rates reached a July peak of 0.02% as ETH’s spot price surged through $3,000, but remained far below the levels in Q1 2024 when ETH rallied to $4,000. Interestingly, while ETH funding rates have yet to match exuberant highs, the same cannot be said for BTC. Perp funding rates for BTC contracts have come close to both their March and November 2024 highs.

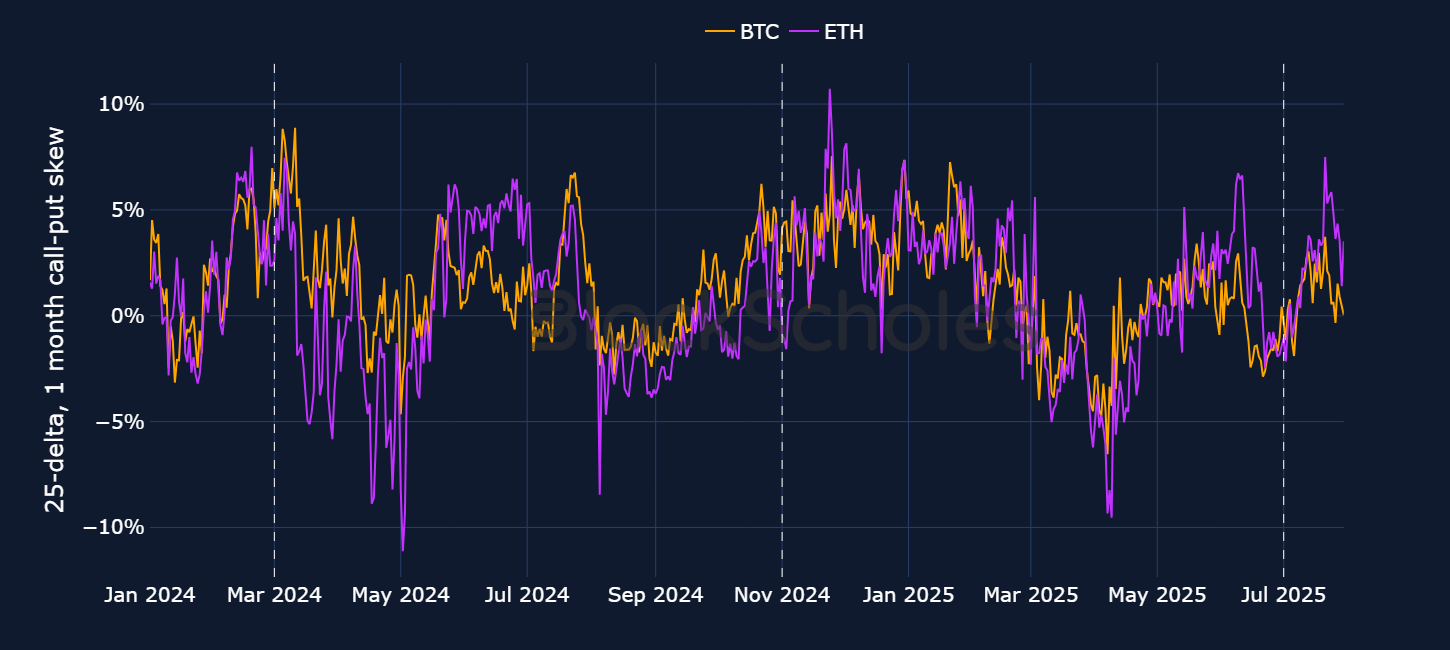

Another metric we can consider is the difference in the implied volatility of a 25-delta call option and 25-delta put option of 30 days for both BTC and ETH. Higher smile skew values indicate a market-assigned premium to OTM call options — or, in other words, a bullish market outlook. July 2025 has seen levels close to — though still not as high as — that reached in the post-election period. However, volatility skew has matched levels reached earlier in March.

Figure 24. BTC (orange) and ETH (purple) 25-delta 30-day volatility smile skew since January 2024, with vertical dotted lines marked on select periods of altcoins outperformance. Source: Block Scholes

Derivatives markets are therefore painting an unclear picture: sentiment remains bullish in both BTC and ETH, but hasn’t reached the exuberant highs seen several times before in this cycle. However, previous extremes in market positioning have resulted in sharp pullbacks as liquidations of long positions exacerbate downside volatility, such as those following the launch of ETFs in January 2024 and the post-election rally in December 2024. A lack of extreme bullish positioning is suggestive of a more healthy environment for fundamentals to win out over flows.

Throughout this report, we’ve analyzed various metrics and signals across market structure, macro conditions, institutional flows and options markets positioning. One theme stands out: the ignition of the next altseason is well overdue. While isolated bursts of altcoin outperformance have occurred, they’ve lacked the sustained momentum, depth and capital rotation that have characterized prior cycles. The persistence of elevated Bitcoin dominance suggests that this cycle might see the fruition of an altseason slightly later — or perhaps not to the extremes we’ve seen previously.

That isn’t to say the ingredients for altseason are absent. Liquidity is expanding, ETH Spot ETF inflows have caught up and (more recently) outpaced BTC, and macro conditions are still supportive, on the whole. Furthermore, regulatory clarity around Ethereum’s role in tokenization, potential staking-enabled ETFs and stablecoin issuance could all serve as powerful catalysts for capital rotation. The same institutional behavior patterns that may have delayed the transition of capital out of BTC and into riskier altcoins (including ETH) may also be responsible for the subsequent rotation, as more assets receive ETF approvals and benefit from increased regulatory clarity in the US.

.jpg)

.jpg)