Andrew Melville

Head of Research

The month of August has started in a far more bearish manner than the month that came before it. Positioning in derivatives markets suggest that market participants were anticipating a bigger downside move than what has so far materialized and that, despite the pullback in spot prices abating, sentiment has yet to fully recover. The past week has not been short of narratives for crypto traders: President Trump extended his reciprocal tariff program as his self-imposed Aug 1, 2025 deadline was reached, weaker-than-expected US jobs data has reignited uncertainty over the Fed’s monetary policy path and the SEC’s “Project Crypto” provided some bullish news for the advancement of tokenization in the US and Layer 1 blockchains that stand to benefit from the regulatory positivity.

The month of August has started in a far more bearish manner than the month that came before it. Positioning in derivatives markets suggest that market participants were anticipating a bigger downside move than what has so far materialized and that, despite the pullback in spot prices abating, sentiment has yet to fully recover. The past week has not been short of narratives for crypto traders: President Trump extended his reciprocal tariff program as his self-imposed Aug 1, 2025 deadline was reached, weaker-than-expected US jobs data has reignited uncertainty over the Fed’s monetary policy path and the SEC’s “Project Crypto” provided some bullish news for the advancement of tokenization in the US and Layer 1 blockchains that stand to benefit from the regulatory positivity.

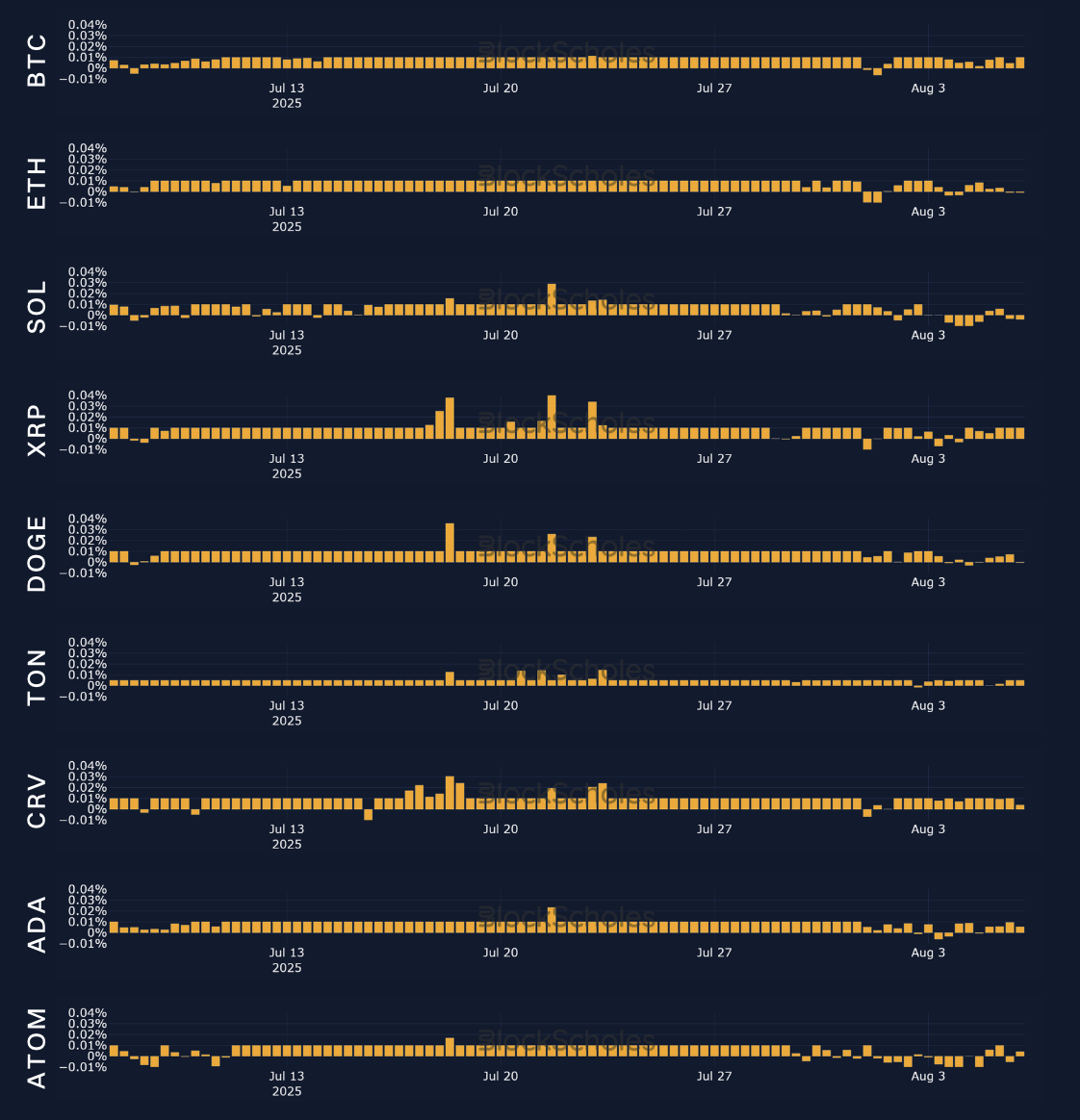

Perpetuals: Funding rates declined across a slew of tokens as spot prices fell following the disappointing July jobs report in the US.

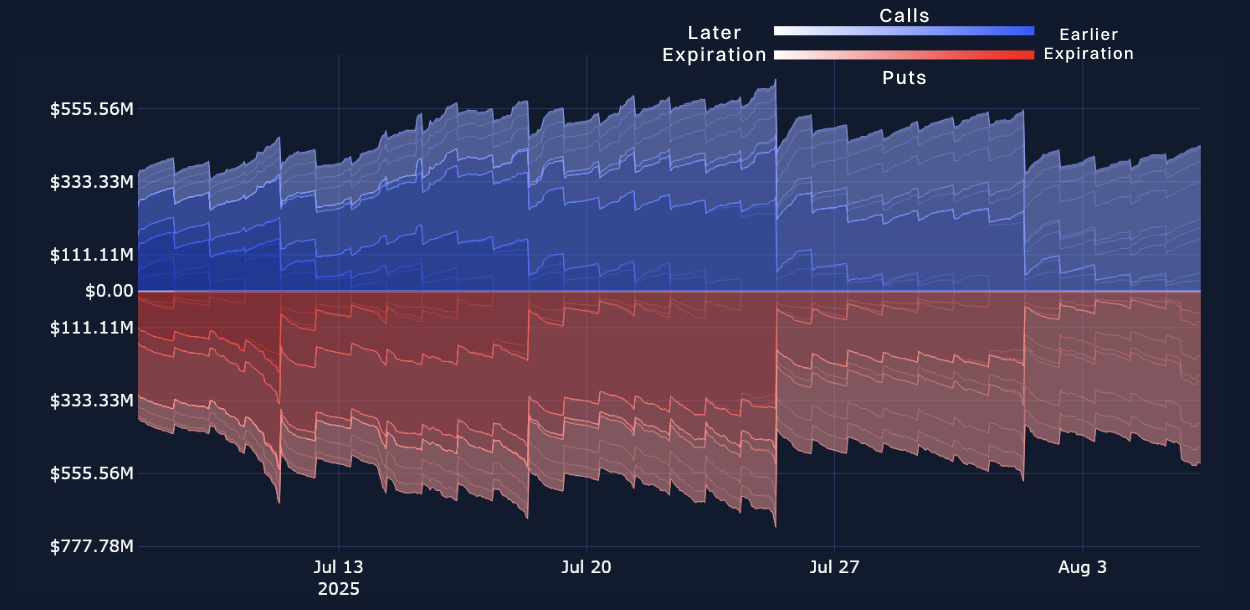

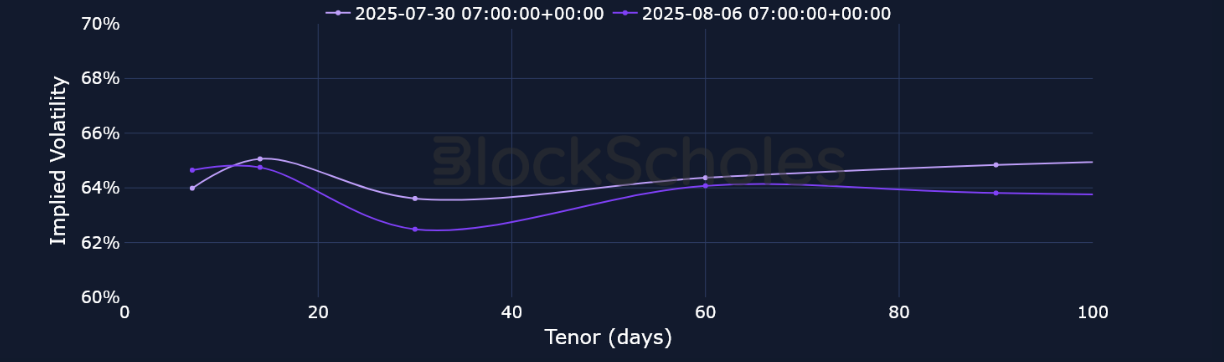

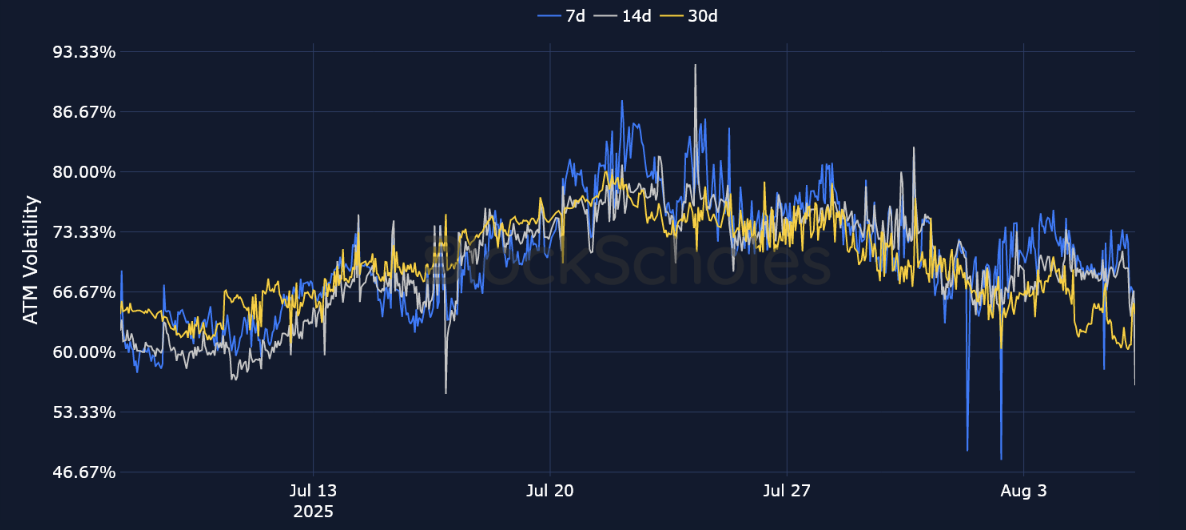

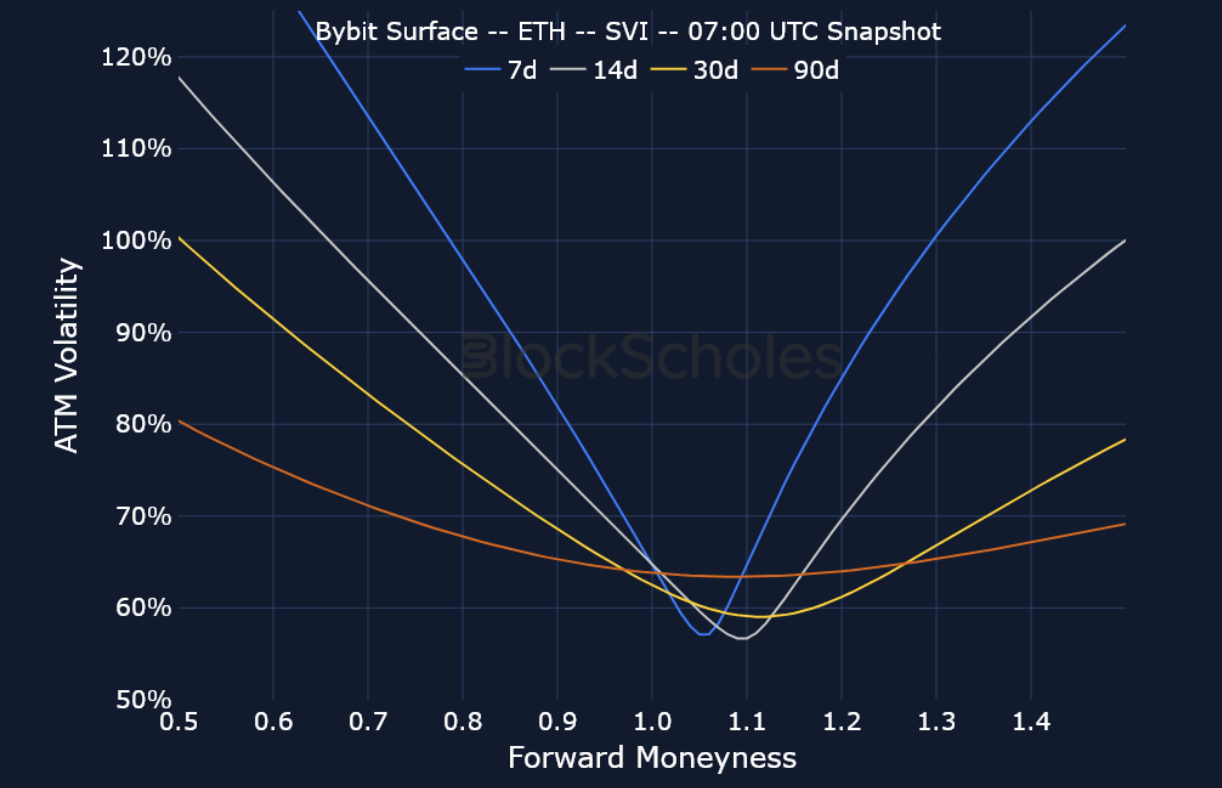

Options: ETH options continue to trade with close to a 2x premium to BTC options, and show a far stronger willingness to invert the term structure of volatility during big market moves. The weekend inversion in ETH’s term structure after the US jobs report and the failure of an inversion in BTC’s term structure provide ideal examples.

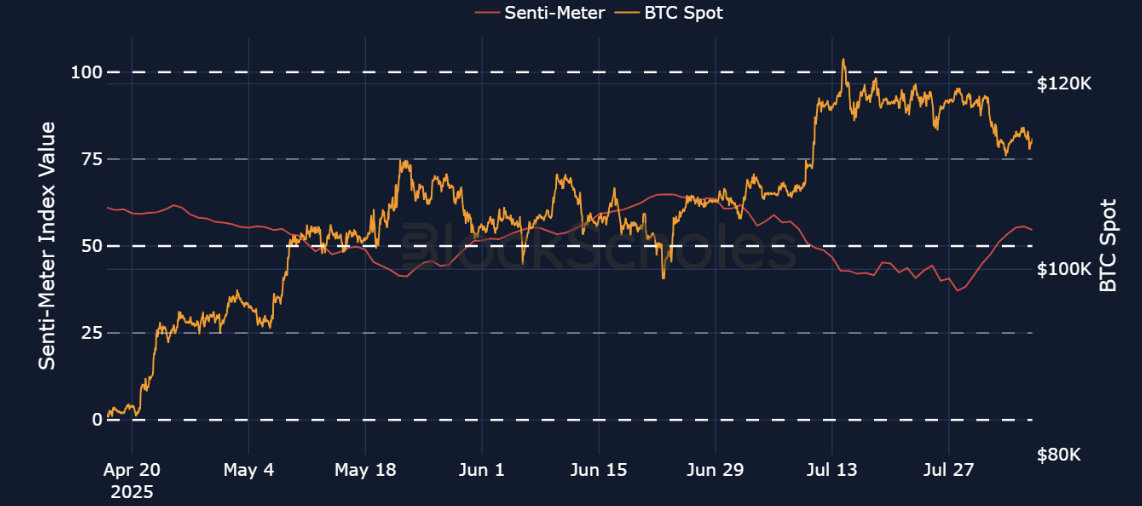

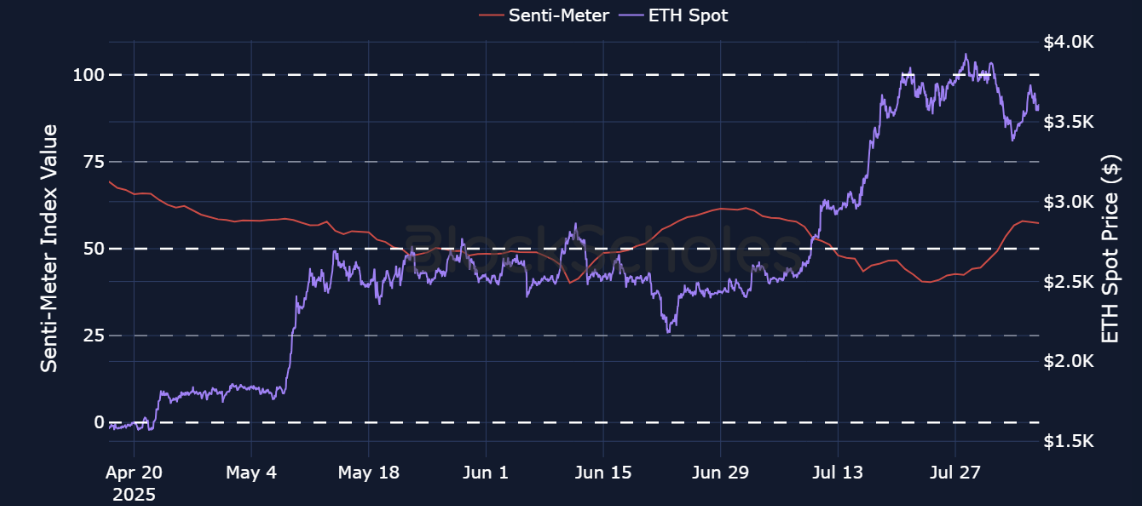

Block Scholes’s Senti-Meter Index aggregates the funding rate, future-implied yield and volatility smile skew into a single expression of sentiment in derivatives markets. See more in the methodology article here.

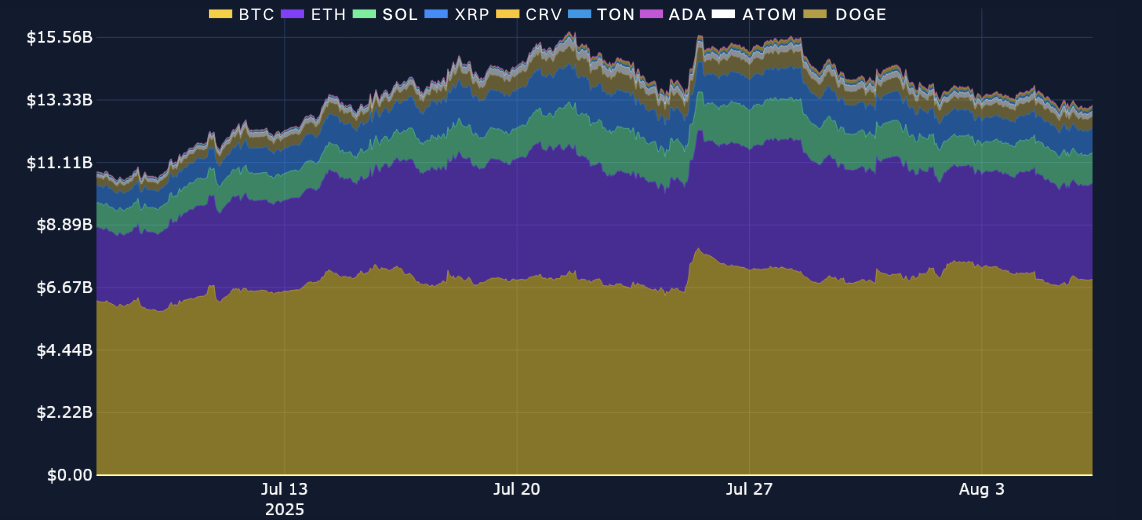

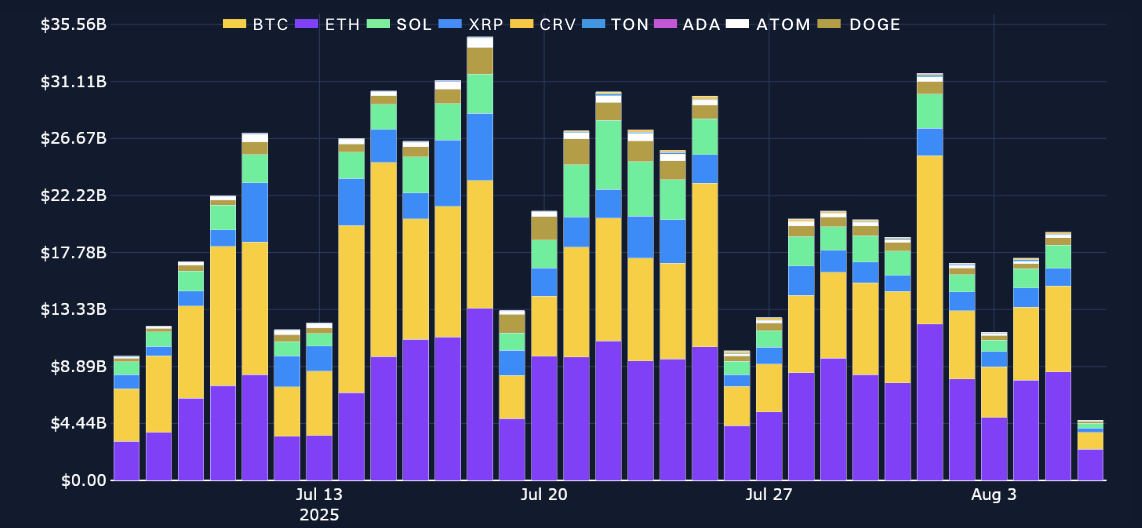

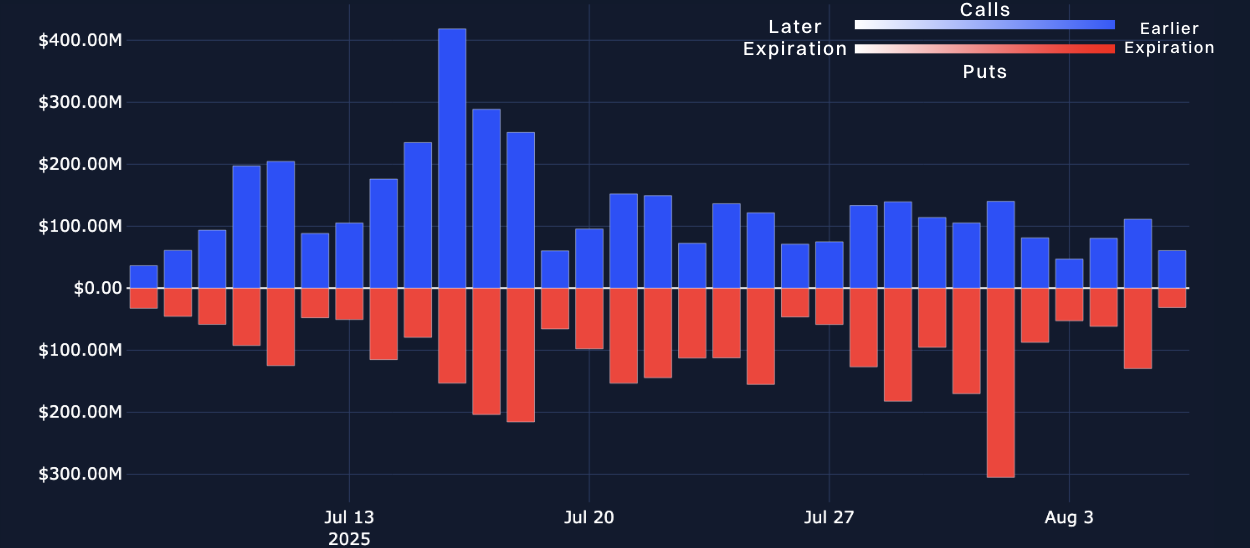

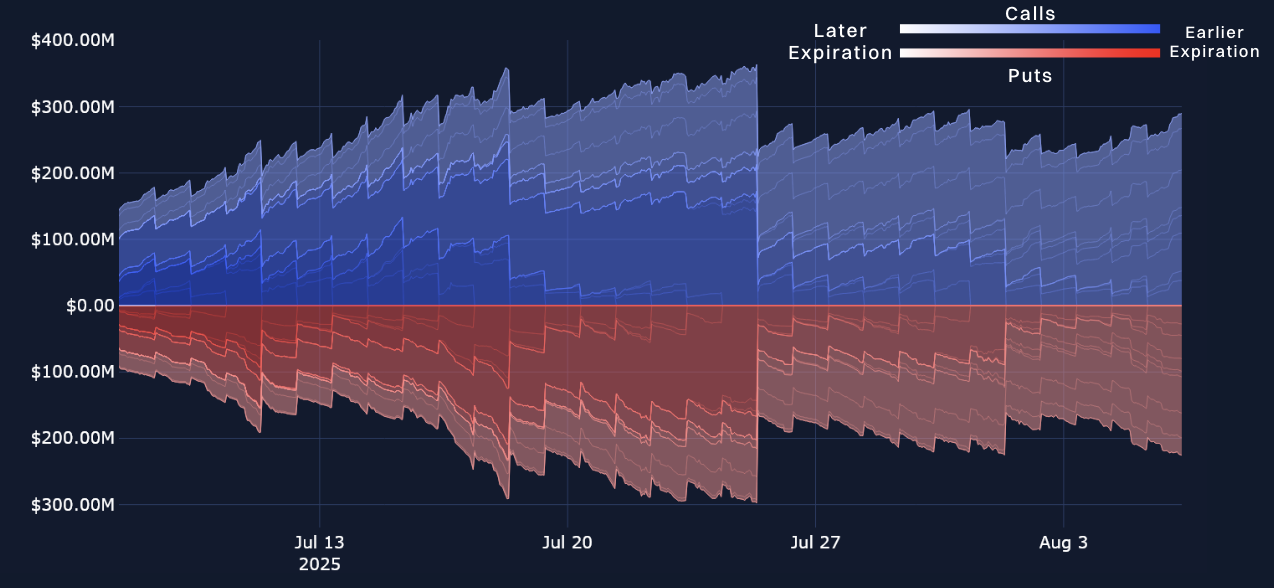

After rising through most of July from $10B to $15.5B, open interest in perpetual futures contracts began to descend from Jul 28, 2025. That decline has been broad-based across the tracked assets. For BTC, perp open interest has declined by $1B since late July, while open interest for ETH has dropped by slightly more than $1B. That coincides with a falling spot price in both major crypto assets over the same period of time. On Jul 31, 2025, BTC was trading at $118K, but since then has fallen to trade within a range of $112K–$115K. That move lower began before the US employment report was released on Aug 1, 2025, as President Trump announced a slew of new extended reciprocal tariff rates, but was exacerbated as the weaker-than-expected employment figures brought down US equities and risk-on assets alike.

Aug 1, 2025 also featured the highest daily perp trading volume, reaching more than $31B, and trade volumes on the following Saturday (Aug 2, 2025) were nearly double the volume typically seen over the weekend.

This week marked a break in the exuberant funding rates across BTC and altcoins that characterized last week. Throughout, crypto markets were subject to a multitude of different narratives:

None of these events, however, had as great an impact as the US jobs report. On Aug 1, 2025, the day of the release, funding rates across a multitude of assets — including BTC, ETH and XRP — all fell to below 0%. Since then, funding rates have been mixed, marking at least a temporary end to the persistent bullishness that marked the end of July. While BTC shows recovery in leveraged long exposure, SOL is seeing continued negative funding rates.

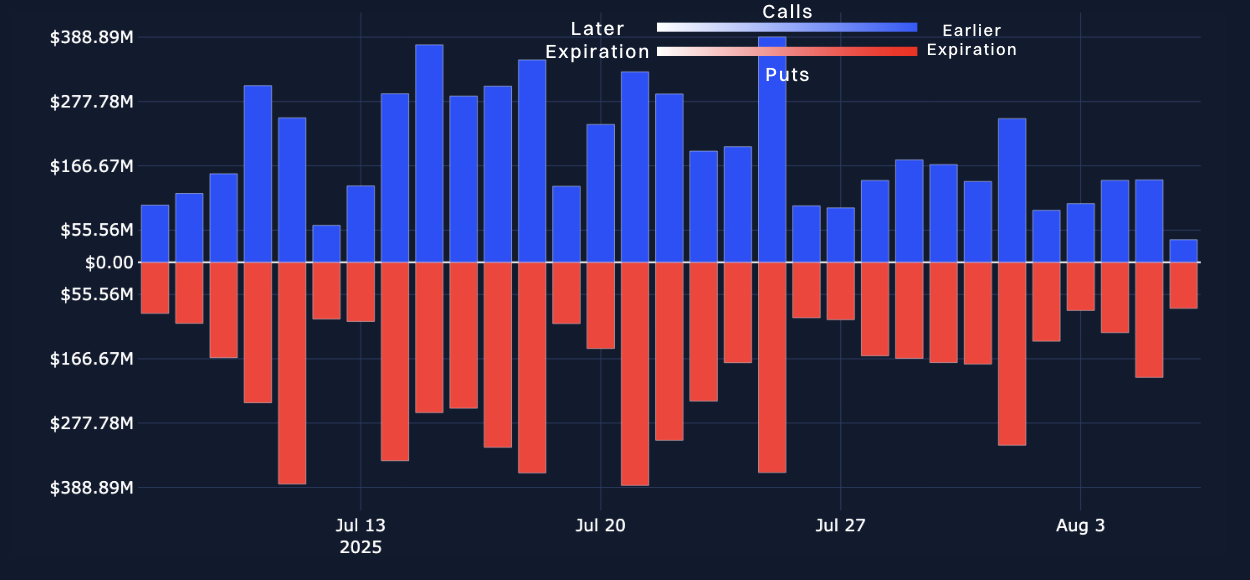

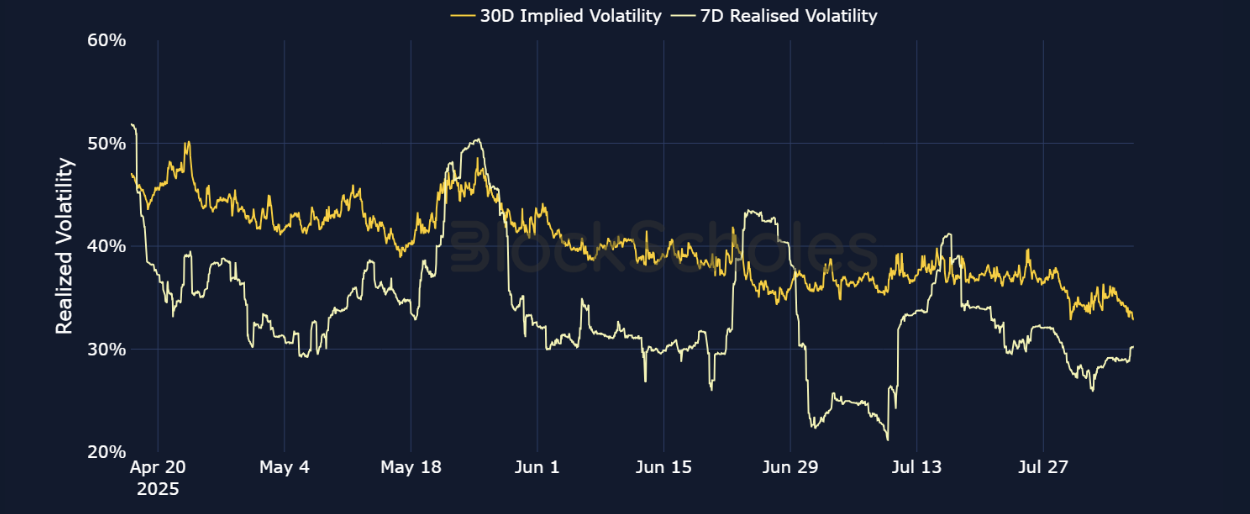

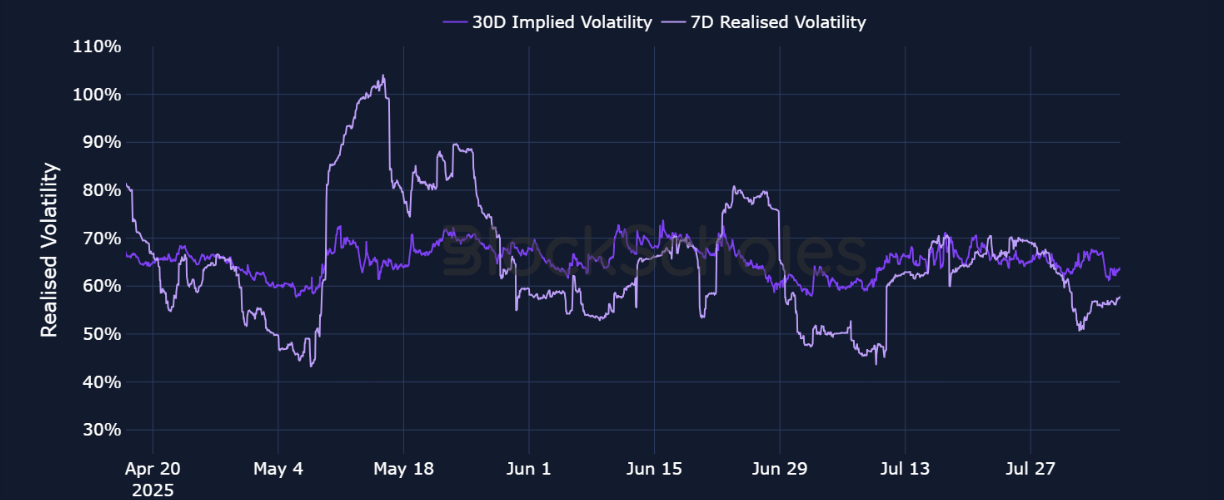

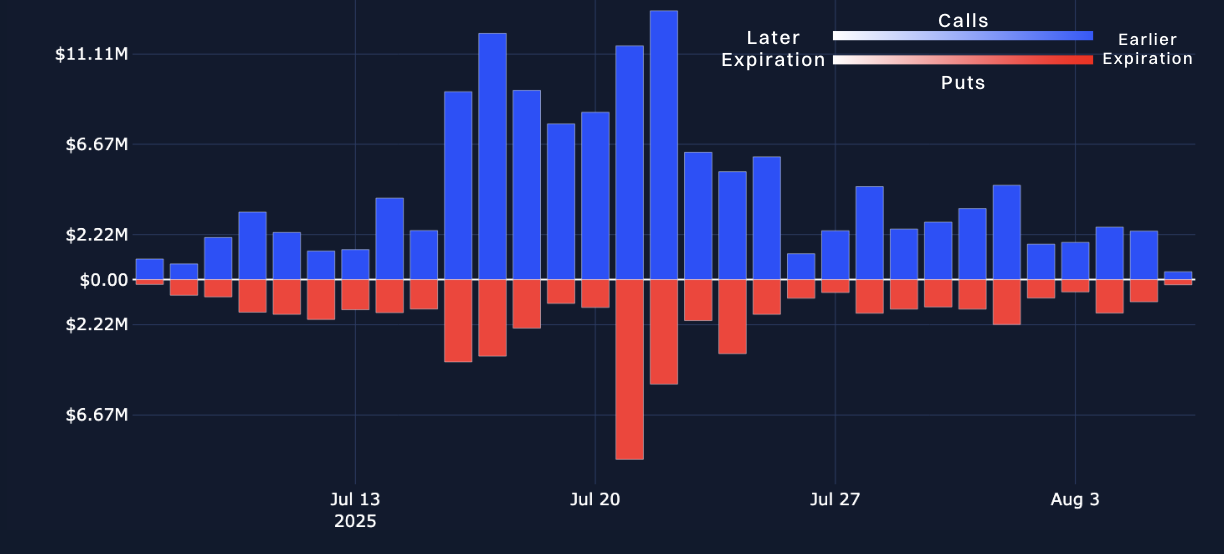

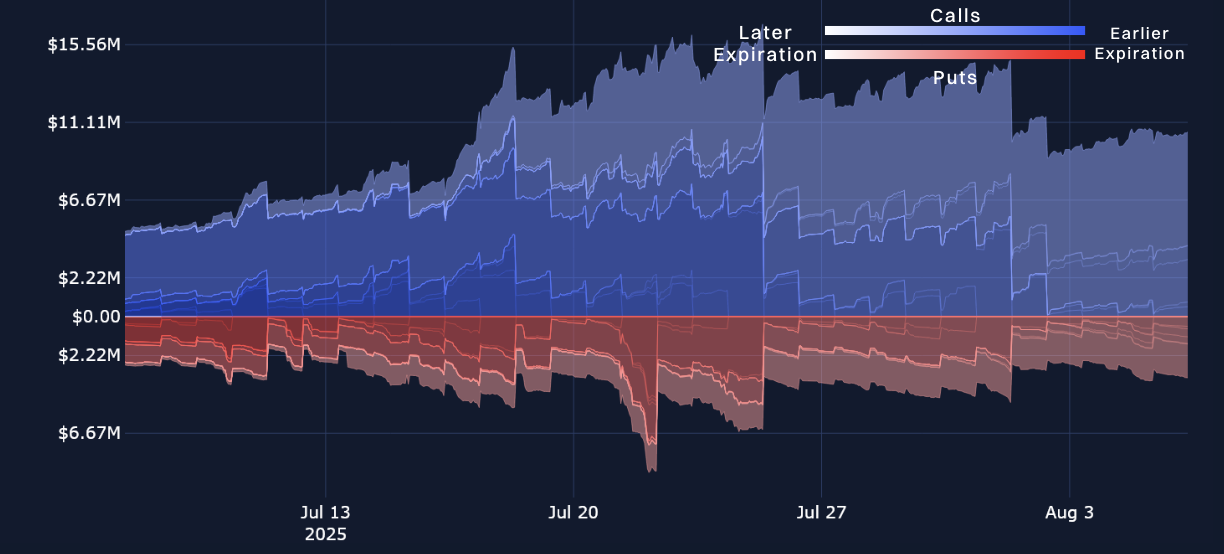

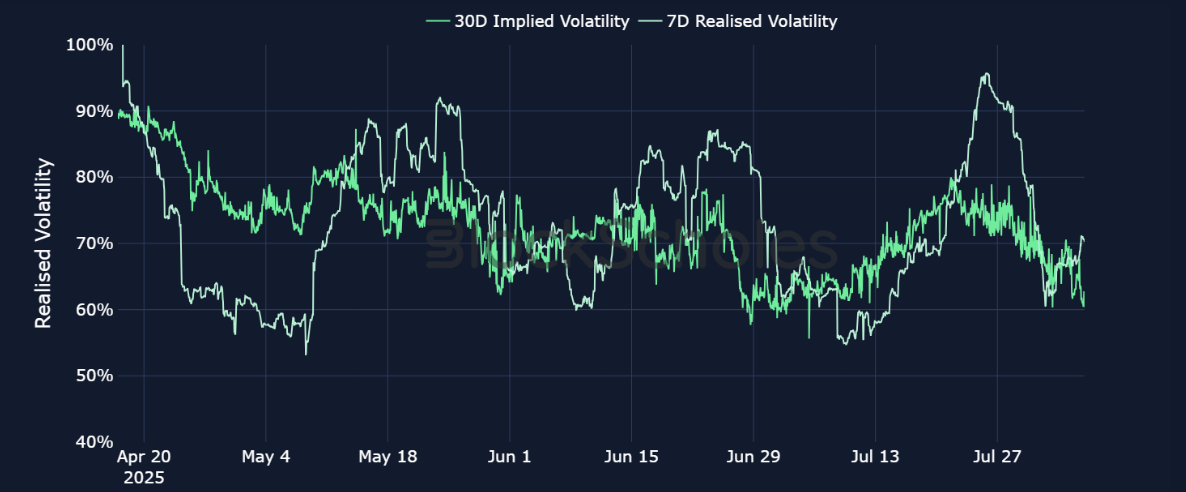

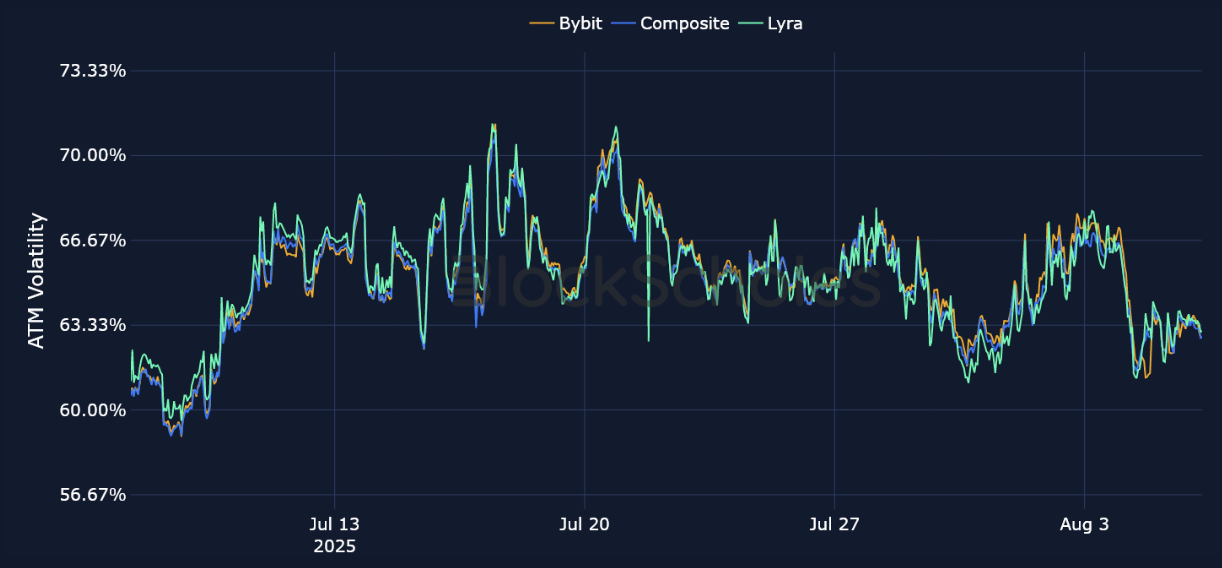

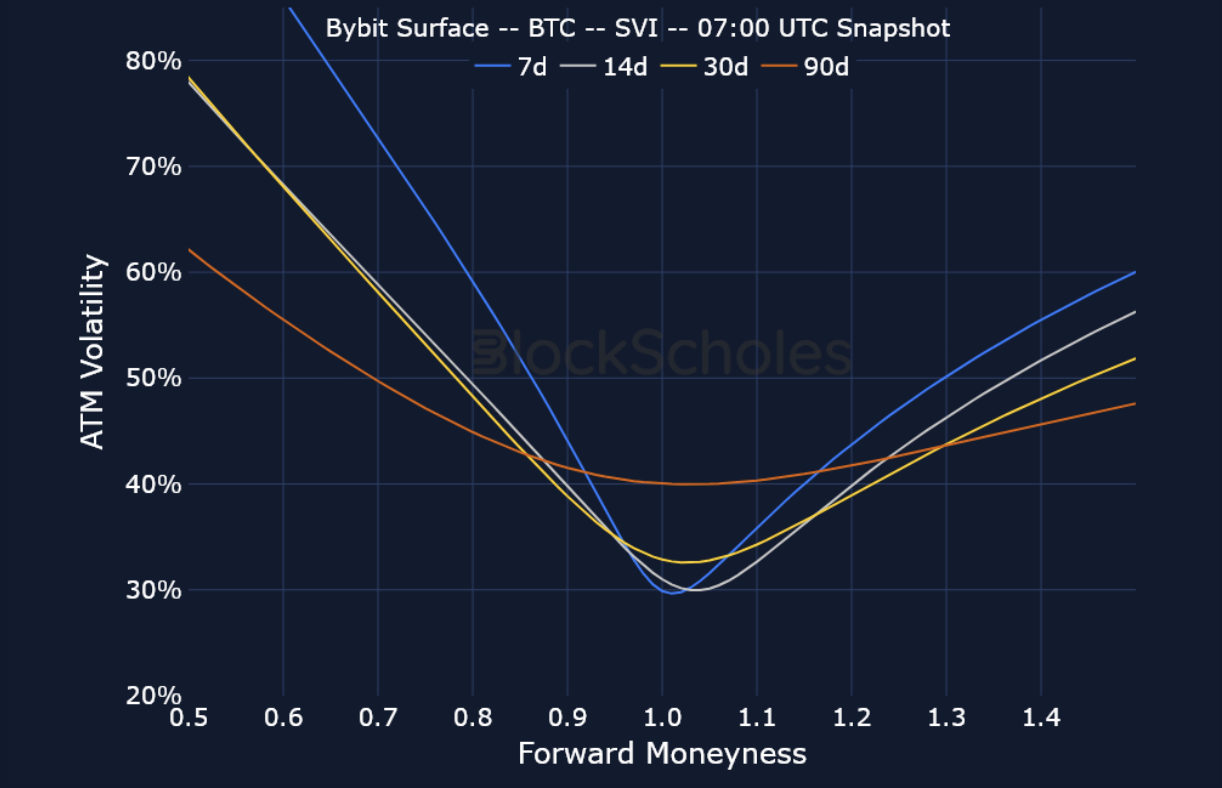

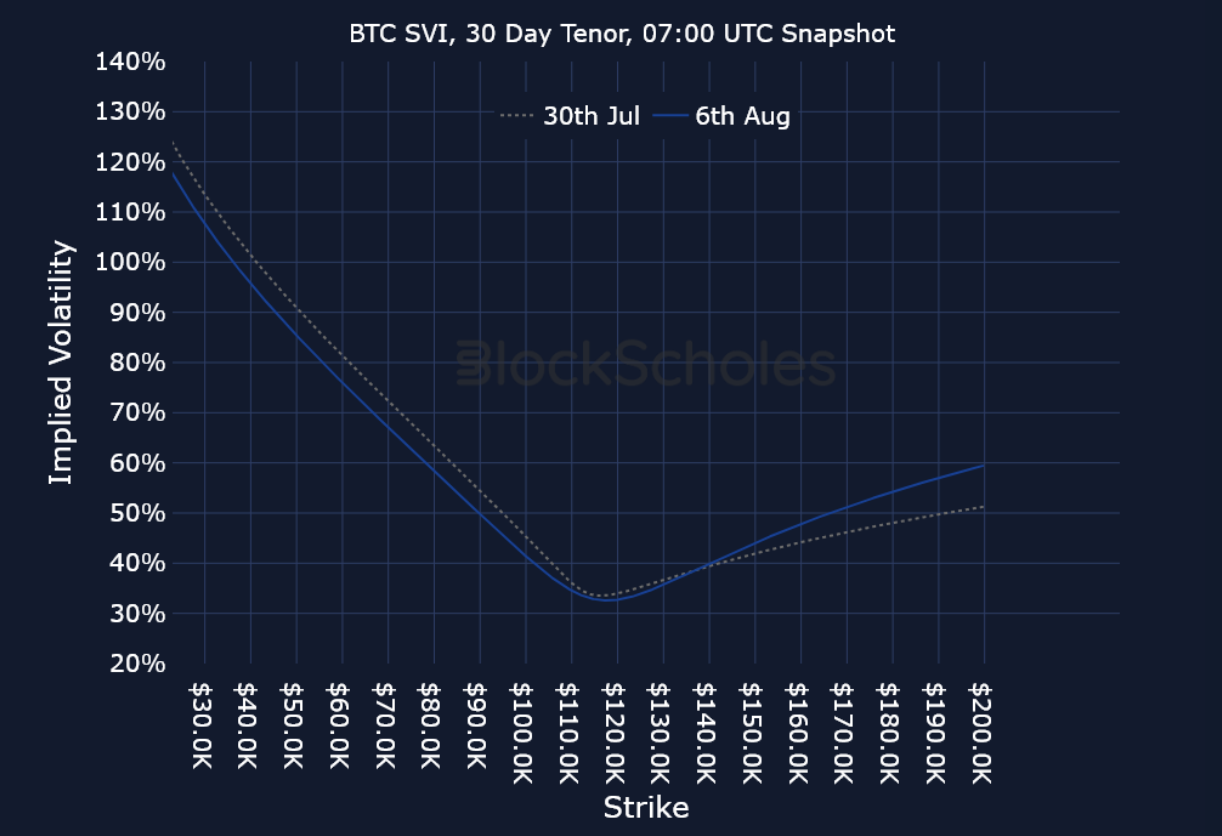

At-the-money (ATM) implied volatility for BTC options has continued to fall, despite the pullback in BTC’s rally over the past week from above $118K to $112K. Perhaps this doesn’t come as a surprise, however, given that realized volatility has also dropped since late July and is now sideways at around 30%, suggesting that the pullback in BTC’s spot price wasn’t such an extreme move. Meanwhile, positioning in puts and calls doesn’t reveal too much about market sentiment, as put options volumes and open interest continue to dominate as they did last week, despite the moves in spot price.

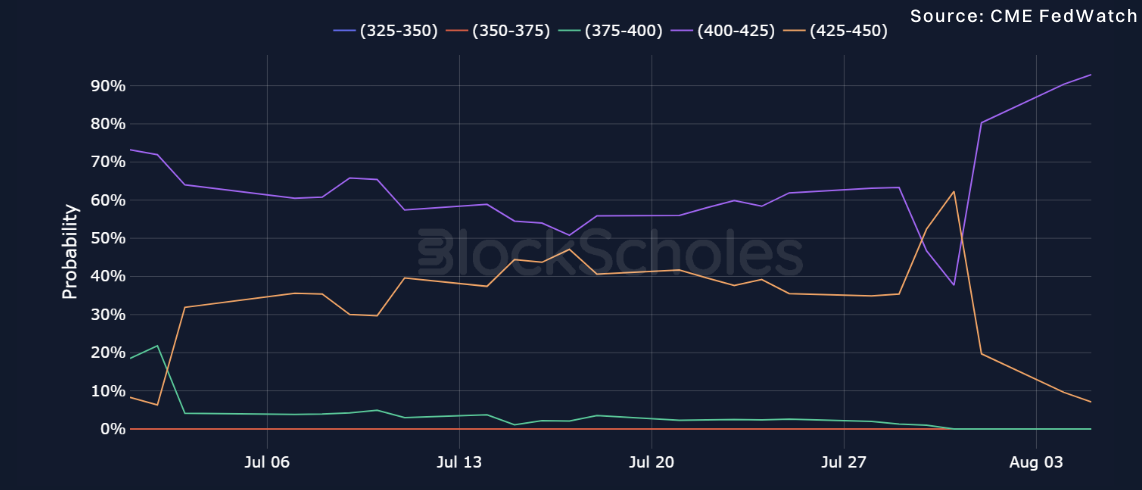

Macro conditions are once more providing an uncertain backdrop for BTC and crypto assets. President Trump’s self-imposed Aug 1, 2025 tariff deadline has passed, and he has since announced a slew of new extended reciprocal tariffs, including 15% levies on nations that have a trade surplus with the US. That’s also coupled with an unexpected weakening in the labor market, following major revisions to jobs data in the US, which is calling into question how quick and how much the FOMC is likely to cut interest rates before the end of the year.

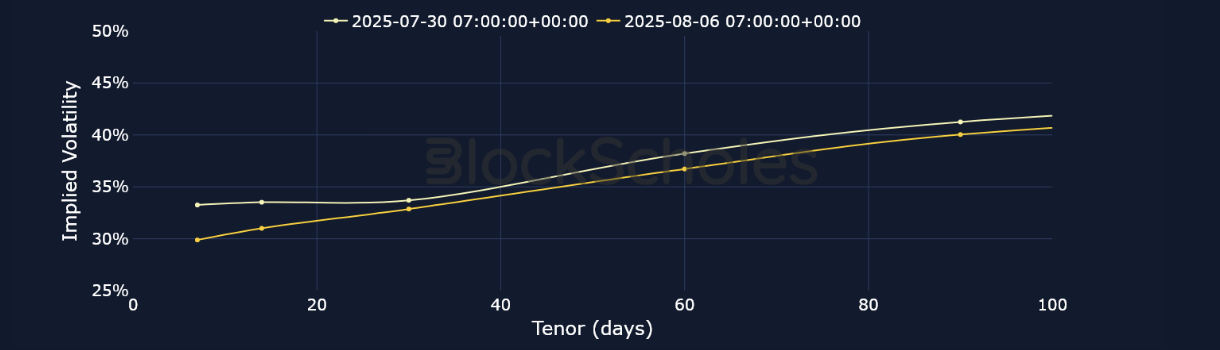

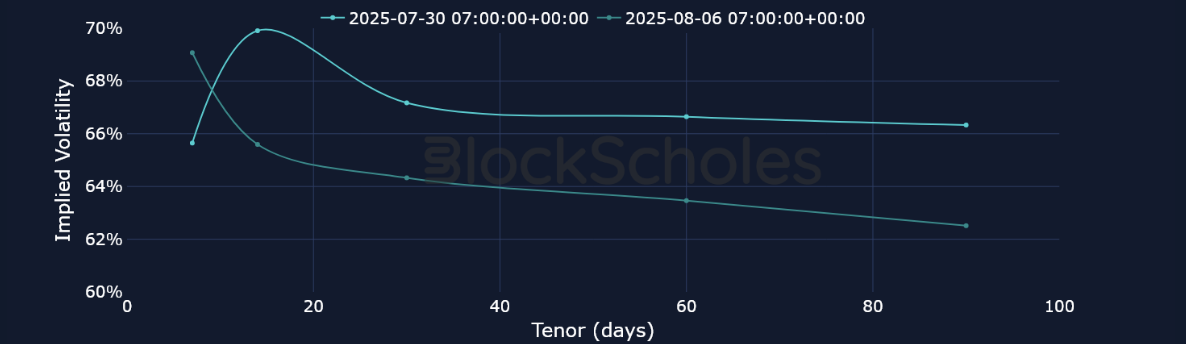

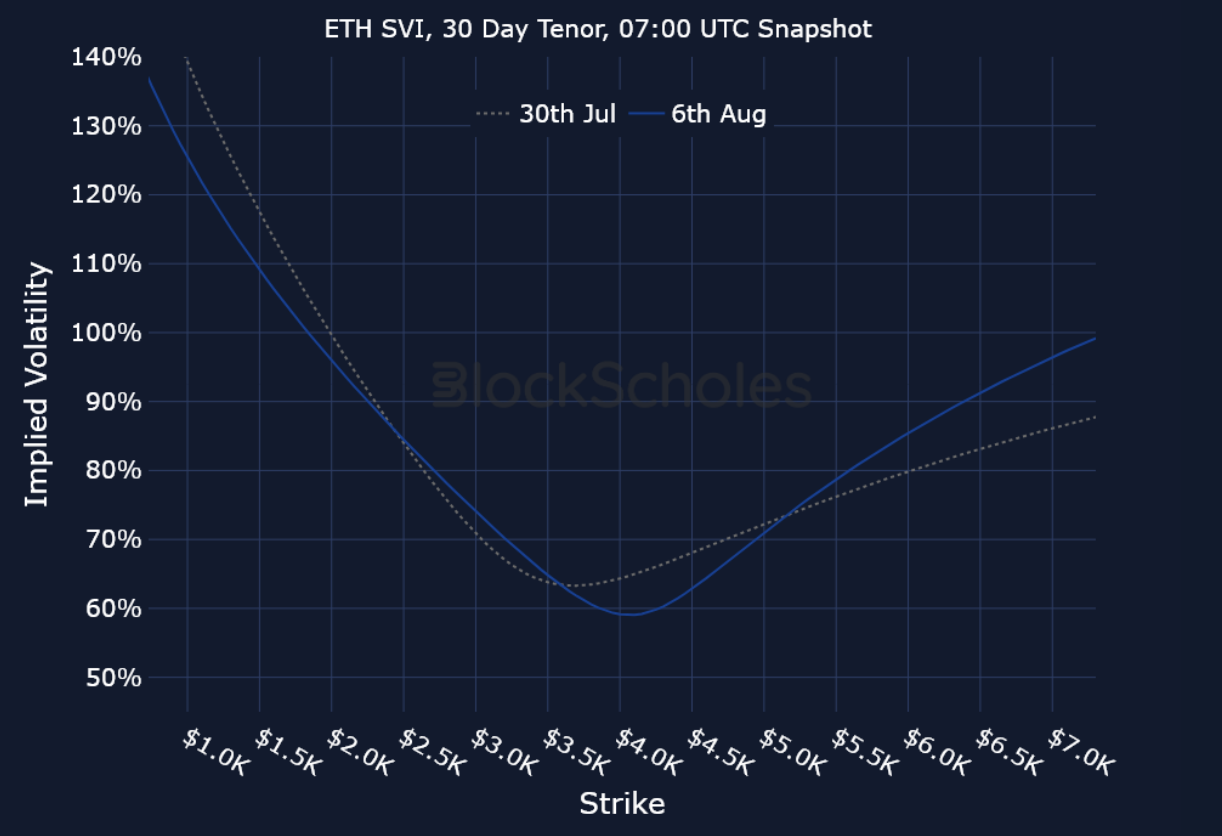

As we’ve come to expect, ETH’s short-tenor implied volatility continues to trade with nearly a 2x premium relative to BTC options at an equivalent maturity. Traders in ETH options are also far more willing to push the front end of the term structure higher during periods of spot market declines or major rallies, unlike BTC’s term structure, which has been far more stable during similar market moves.

Following the NFP report in the US and into the weekend, ETH’s front-end volatility shot up to 73%, while 60-day implied volatility traded closer to 67%, a swift inversion in the term structure. IV has since dropped off for ETH options as last week’s rally has come to a stop, and ETH is trading 4% lower over the past seven days. Interestingly, that pullback in spot price resulted in a large skew toward put options, indicating that put skew was driven up by traders purchasing put options for downside protection during the dip, rather than merely a drop in demand for upside exposure in calls.

Realized volatility for SOL has seen a major spike in both directions over the past week. As SOL’s spot price rallied into the end of July, delivered volatility surged past 90%. However, since late July, SOL has dropped from $204, and is down more than 7% over the past week. Just as significant, its 7-day realized volatility has also dropped from those 90% highs. At the same time, SOL options markets have been subdued in their response to the recent pullback, with options volumes more than 5x lower than mid-July, when altcoins were outperforming BTC. Open interest for SOL continues to be dominated heavily in call options, as we’ve often found to be the case.

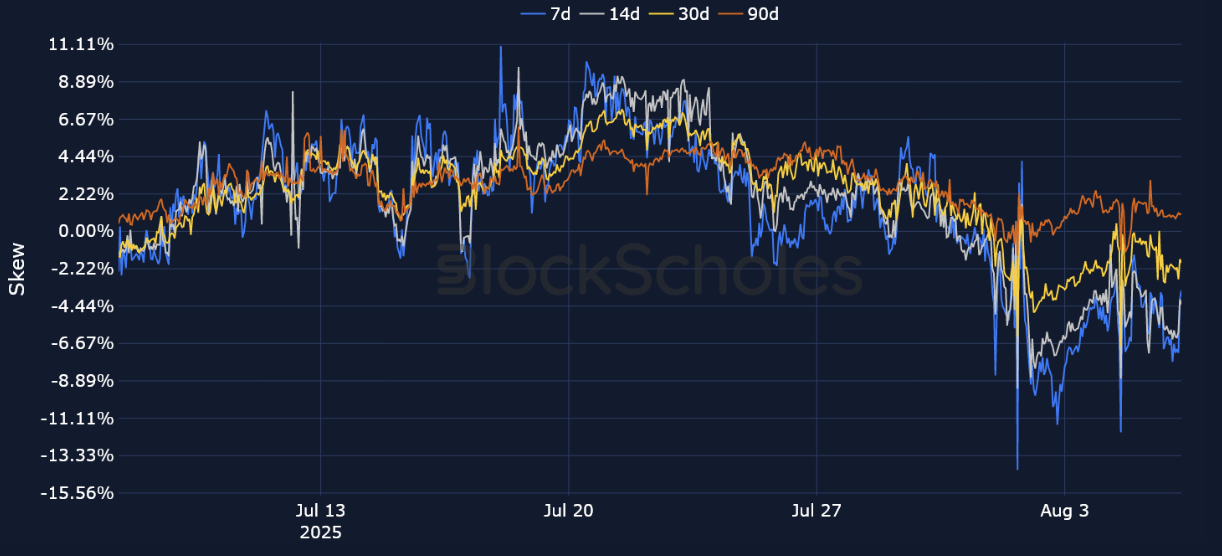

The month of August has started in a far more bearish manner than July, which saw BTC reach a new all-time high and ETH return more than 50%. As such, we see a major bearish slide in sentiment since the start of the month, as BTC’s put-call skew dropped to −7% earlier this week. That sentiment has yet to recover, despite the pullback in spot prices abating. Ultimately, the pullback in BTC’s spot price is modest, as a move from $118K to $112K is by no means the largest pullback so far this year. That may suggest traders’ positioning is more proactive than reactive. Positioning in ETH is more bearish than for BTC, something that’s unsurprising since altcoins typically perform worse during market sell-offs. This week has been a demonstration that ETH reacts more strongly than BTC in all directions — in spot markets, it’s fallen harder than BTC, and in derivatives markets ETH’s skew briefly dropped below −10%.

Open interest and trading volume data are sourced “as is” from the Bybit exchange platform API exclusively, and as such do not represent a comprehensive picture of the sum of trading activity across all derivatives markets or exchanges. The data visualized in this report consists of hourly and daily snapshots, recorded over the previous 30 days. Daily (hourly) snapshots of trade volume record the total sum of the notional value of trades recorded in the 24H (1 hour) period, beginning with the snapshot timestamp.

If not explicitly labeled as derived from another exchange, the input instrument prices to all derivatives analytics metrics in this report are sourced from the appropriate endpoints of Bybit’s public exchange platform API. In the event that data is labeled or referred to as representing the market on another exchange source, that data is sourced from the appropriate endpoint of each respective exchange’s public API.

Macroeconomic charts and data are sourced “as is” from the Bloomberg Terminal. Exchange data is sourced “as is” from publicly available exchange APIs. Block Scholes makes no claims about the veracity of public third-party data.

After acquisition of underlying-denominated raw data for open interest and trading volume on the Bybit exchange platform from Bybit’s API endpoint, equivalent dollar-denominated figures are calculated using the concurrent value of Block Scholes’s Spot Index for the relevant underlying asset.

Block Scholes’s Spot Index represents the aggregate Spot mid-price for a given currency across the top five CEXs by volume (with USD-quoted markets). It considers the proportion of total volume in the instrument on the exchange, as well as the deviation of a data point from those on other exchanges.

Futures prices are used for Block Scholes’s futures-implied yields calculation services in order to derive the constant-tenor annualized yields displayed in the Futures section of this report.

Options prices are used for Block Scholes’s implied volatility calculation services in order to calibrate volatility surfaces, from which all derivatives volatility analytics displayed in the BTC Options and ETH Options sections of this report are calculated. Volatility smiles are constructed by calibrating to mid-market prices observed in Bybit options markets. As part of the calibration process, prices go through rigorous filtration and cleaning steps, which ensures that the resulting volatility surface is arbitrage-free and has exceptional fit to the market observables.

.jpg)

.jpg)