Thahbib Rahman

Research Analyst

Premia, a decentralized derivatives exchange, first launched in 2021 on the Ethereum mainnet with the goal to “bring options trading onchain”. In this report we will cover the design choices across the entire protocol and evaluate whether those choices achieve two overarching goals of Kyan.

Premia, a decentralized derivatives exchange, first launched in 2021 on the Ethereum mainnet with the goal to “bring options trading onchain”. Its v1 was a peer-to-peer order book. Its v2 developed this further into an automated market maker (AMM) based options exchange, while v3 was a concentrated AMM. Now, the team behind Premia is set to launch Kyan on Arbitrum — an orderbook-based, decentralized crypto derivatives exchange that will initially support options and perpetual futures (perps) on BTC, ETH and ARB, providing traders with customizable multi-leg strategies with portfolio margin (additional assets will be introduced for trading via a listing process post-launch).

In this report we will cover the design choices across the entire protocol and evaluate whether those choices achieve two overarching goals of Kyan:

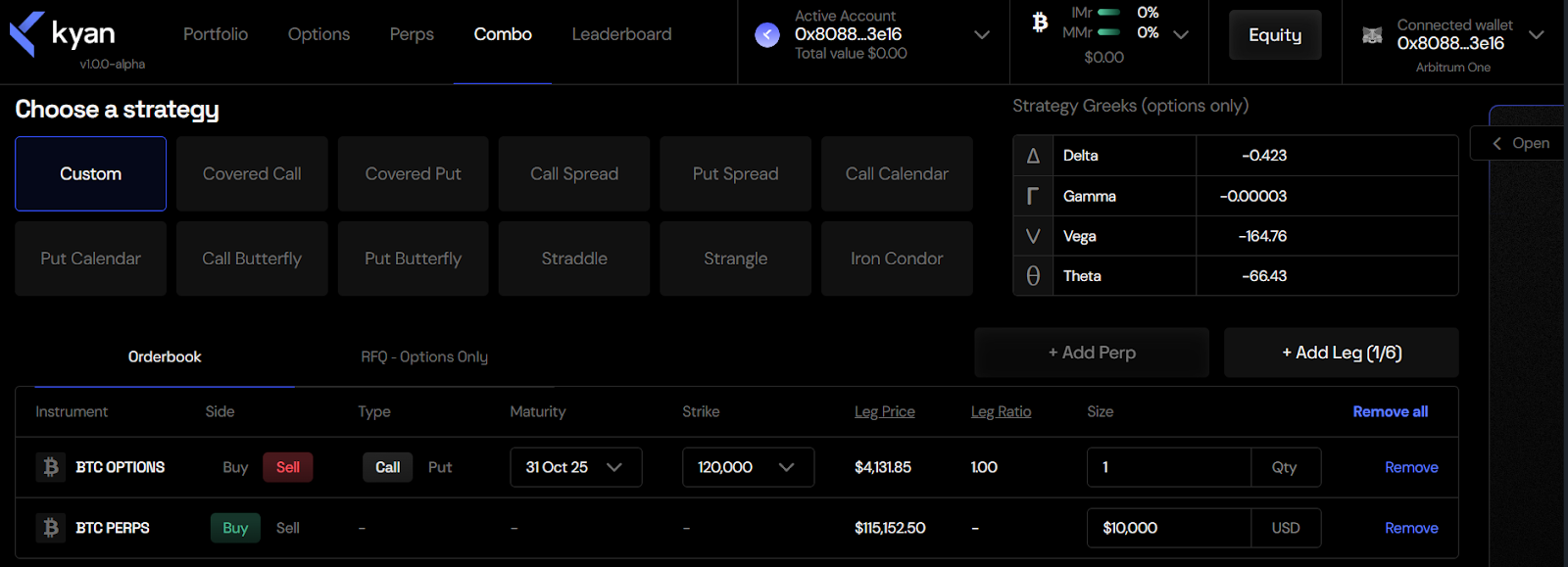

At the heart of Kyan is the implementation of portfolio margin and a risk engine that is designed to support ‘Combo’ trading and multi-leg strategies. A trader can devise a strategy that has up to six different legs at once, and have the ability to hedge the net delta of the position with a perp contract. Instead of having to place orders for those different legs one by one, Kyan provides users with two choices.

The first is the ability to choose from an array of preset strategies, including: butterflies, strangles, straddles and more. This will prepopulate the relevant legs of the trade, after which the user can change the strike prices, expiration dates and the ratios of the legs. Preset multi-leg strategies are executed in an atomic manner on Kyan (referred to as transaction bundling) — this means in the back-end, when a user chooses any of the preset strategies, each leg of their combo is independently routed to that particular instrument’s order book and executed as a Fill-Or-Kill (FOK) order. If any leg of the combo does not get successfully matched to an open order in that leg’s orderbook, the entire combo order does not get executed. Note that the orderbook itself is hosted offchain, with trades also being settled offchain. The exchange state is posted on-chain periodically.

The second option that traders have available to them is the full flexibility to leg in and out of trades via custom strategies. For example, a trader may have the view that the long-term trend for BTC is to the downside and therefore shorts a call option to earn a premium. A few days later, the trader’s view of the market evolves: they still believe their call option will expire out-the-money, but they anticipate a certain macro event may temporarily result in a bounce upwards. Therefore, the user wishes to cover some of their delta exposure, via a long perp contract.

The perp will offset some of the losses in the short call during the move higher in spot price. Kyan’s margin engine takes note of the fact that the trader is hedging their position, and therefore the risk in their portfolio is now partly offset. As such, it will release some collateral back to the trader. The initial short call may have required a margin of $1,000, however, the long perp position reduces that margin to $500, giving the trader the most capital efficient experience.

When trading naked options, losses can (theoretically) be infinitely large. For example, a trader selling a call option by itself can face an ‘infinite’ loss as the spot price of the underlying asset has no ceiling. With portfolio margin in Kyan, options strategies that have a predefined risk portfolio (such as a call spread or those that are used in conjunction with perps to reduce the delta exposure) allow the trader to access more leverage on Kyan.

The above is an example of one beneficial use case of portfolio margin on Kyan. Another benefit of having a full suite of options and perps with portfolio margin is the ability to create synthetic spot exposures.

One way that a trader can create a synthetic position that simulates the same exposure as being long spot BTC is by leveraging put-call parity: taking a long position in 1 BTC call option and a short position in 1 BTC put option at the same strike and expiration date. If a trader then adds an additional short perp position, the portfolio margin on Kyan would recognise that the synthetic position offsets the short perp position, leading to a lower margin requirement for the positions.

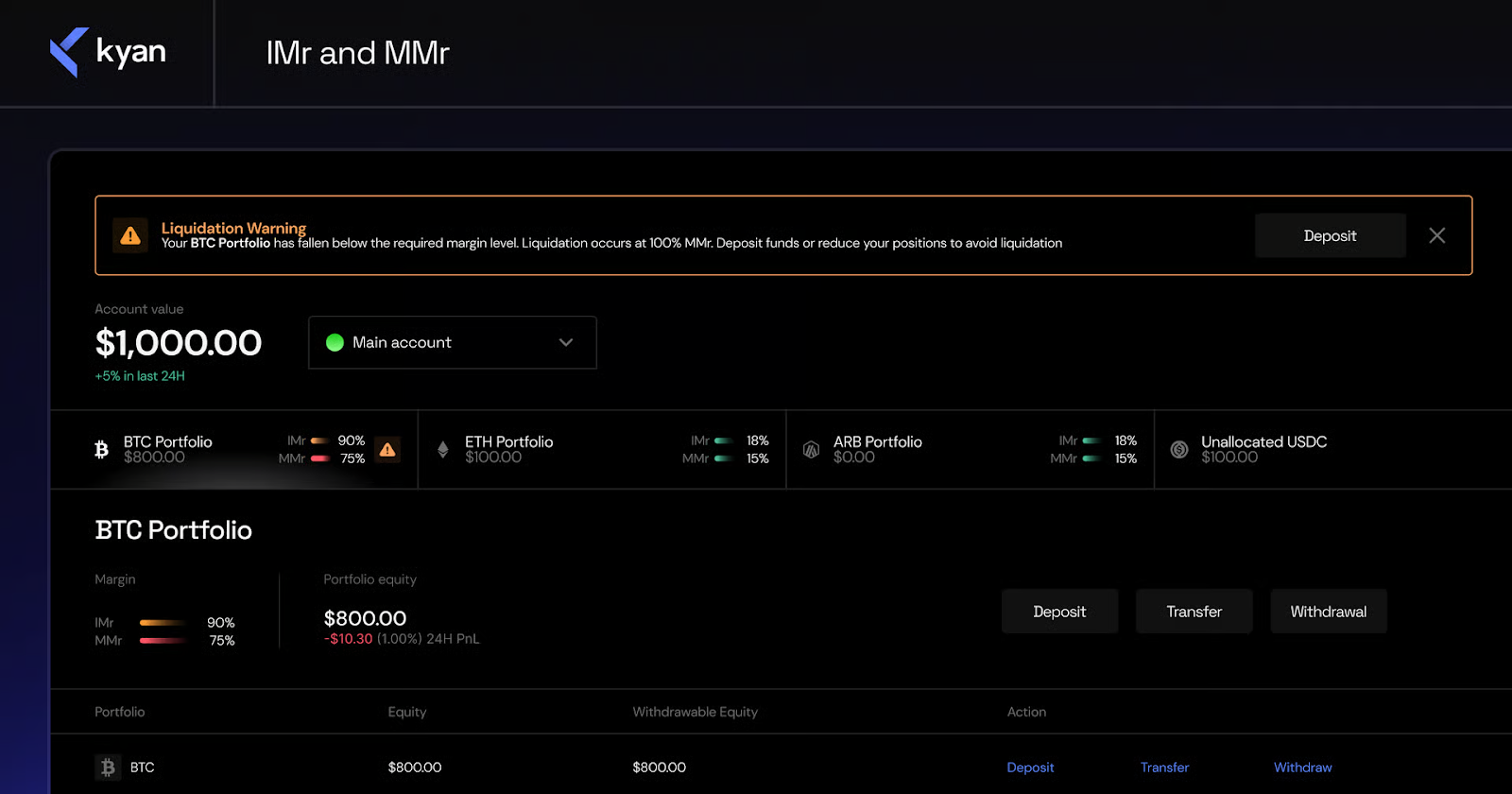

When trading on exchanges, there are generally two types of margin: standard margin and portfolio margin. Portfolio margin (PM) is the dynamic risk-based system Kyan uses when calculating the margin required to enter a position – this is the default option for all traders on Kyan, with standard margin scheduled to be added later. When a trader connects their wallet application to Kyan, it will automatically create separate ‘Portfolios’for the user. Each ‘Portfolio’ contains three separate margin accounts for the three tradeable markets on Kyan: BTC, ETH, ARB. That allows traders to segregate strategies based on the underlying asset being traded (known as Isolated Portfolio Margin).

Standard margin considers each position in a portfolio in isolation. The total margin requirement is simply the sum of each position — and therefore will increase with every new trade, even if some of the new positions offset the total risk of the portfolio. This structure therefore often requires the trader to post a greater total margin.

Portfolio margin, on the other hand, does not silo each position in a portfolio. Instead, it considers the totality of the portfolio: if certain positions act as hedges, or offset the risks of other positions, traders are required to post a lower amount as margin, avoiding overcollateralization. Directional trades on Kyan will still allow traders to get leverage (often 5-8x), but portfolios that are delta neutral (and therefore have overall reduced risk exposure) can get up to 40x leverage.

Through sub accounts and portfolio margin, a user can separate their portfolios based on the underlying, such that liquidation in an ETH perpetual position has no impact on the margin requirement on a BTC options position. Profit and loss and margin are all separate across sub accounts, though users can send funds between accounts.

Liquidations are a natural byproduct of trading with margin – insolvent positions must be closed before they incur a loss that they cannot fund, avoiding a shortfall to the exchange and its users. Aiming to make the switching cost from CEX to DEX as frictionless as possible via a liquidation model that traders on CEX’s may be familiar with, Kyan’s risk engine replicates many of the capital efficiency and modelling properties of Deribit’s risk engine. It also means that liquidations are performed incrementally, to preserve a trader’s capital and not wipe out an account in one go.

Kyan’s risk engine determines when to liquidate a portfolio by calculating two margin requirement ratios. The first ratio, initial margin, is defined as the minimum amount of capital required to enter a derivatives position. The initial margin ratio, IMr, is the ratio between the capital needed for a position and the capital a trader has in their account that is not being used to back other trades. A trader is able to add more risk to their portfolio as long as the new trades they put on keep the initial margin ratio below 100%. However, when it reaches 100%, a trader cannot open any new trades that increase their directional exposure (offsetting positions that reduce risk are allowed).

The second ratio is maintenance margin – the capital needed to keep a position open. When this reaches 100%, Kyan will take over a user’s account completely, and will begin the liquidation process. Both of these metrics are real-time ratios the trader can track while trading at all times — and traders are able to see how a new position will change their margin ratios before executing an order.

The risk engine is constantly evaluating the risk of every trader’s portfolio to determine the initial and maintenance margin requirements. The total risk of a portfolio is a function of 7 different variables: portfolio risk = systematic risk + spot shock + IV shock + vega risk + fat tails risk + delta shock + roll risk – variables of similar type to Deribit’s. Systematic risk refers to the overall risk exposure of the entire protocol across users and assets.

For example, there are 9 simulated shock scenarios on the spot price of the underlying asset in the portfolio. These shocks range from a -24% drop in spot price to a +24% gain in spot price (-24%, -18%, -12%, -6%, 0%, 6%, 12%, 18%, 24%). For each spot price shock, Kyan also evaluates a shock to the implied volatility of the instruments in the portfolio. Three different IV scenarios are tested: a downward shock to volatility, no shock to volatility and an upward shock to volatility. This means there are 27 scenarios across the spot and volatility matrix under which the platform estimates the value of a portfolio. The loss incurred in the worst performing scenario is then used as the required margin amount.

There are also 16 other shock scenarios (referred to as extended scenarios). These model larger moves in spot price and are designed to capture vega risk and edge cases — including price moves of -66%, -33%, +50%, +100%, +200%, +300%, +400%, +500%. Together, the portfolio is tested against 43 different scenarios.

The two additional risks are delta risk and roll risk. Delta risk relates to the directionality of the portfolio. In scenarios where implied volatility is very high, it may be difficult for Kyan to liquidate a trader’s positions as the underlying spot price may see big swings. Therefore, position sizes on Kyan that have a large directional exposure require higher margin requirements. Roll risk refers to the impact on a portfolio consisting of options with different maturity dates. If one leg of a multi-leg strategy expires, it may change the entire risk profile of the portfolio. That risk is considered and may result in an increase in margin requirement close to when one of the legs expire, in order to make a trader aware of the roll risk.

We note however that the risk calculations used by Kyan to determine margin ratios are all computed offchain. An API is used to display those risk metrics on screen so traders can see their margin in real-time and trades placed by a user are accepted or rejected based on these off-chain margin computations. Therefore, while smart contracts enforce the execution of trades, they are not used for risk calculations — this is due to the heavy computation that would be required to maintain a live-update for the IMr and MMr of a strategy with six different legs for example.

When Kyan takes control of a trader’s portfolio, it follows a three-stage process to liquidate the user. Firstly, similar to Deribit, Kyan carries out liquidations incrementally. This means a user’s position is liquidated by just enough to make the position’s margin requirement lower than the posted collateral. Relative to previous iterations of Premia’s DEX such as its v3 model where positions were fully collateralized, the mechanism in Kyan is designed to be far more user-friendly and improve capital efficiency.

The first step in the process is analyzing the portfolio’s delta exposure. Kyan will attempt to use a trader’s remaining collateral to open a position in a perpetual futures contract to hedge the exposure of the portfolio and lower the MMr. If it can lower the MMR enough, this will end the liquidation process, with minimal damage. It does however mean that portfolios with perp exposure only are liquidated in one go.

If delta hedging alone does not reduce the MMr enough, or the portfolio was delta hedged to begin with, Kyan breaks the overall portfolio into three segments:

Decomposing the portfolio allows Kyan to look at each leg in the portfolio, and identify whether there are any offsetting legs to that position. Suppose a portfolio of five different positions: a vertical spread, a long synthetic, and a naked call option. Decomposing the portfolio in this manner allows Kyan to rank the legs or positions contributing most to the margin requirements, e.g., perhaps it is the naked call option due to it not being hedged by any other legs. The liquidation process will begin by unwinding that position first. This can often make the account healthy again, foregoing the need for further liquidations. If that is not the case, additional positions are liquidated until the margin level is healthy again.

If the portfolio contains any vertical spreads, Kyan will, on behalf of the trader, open an opposing position to unwind it. Similarly, synthetic positions are also unwound by opening an opposing order. To encourage liquidators to take on these liquidation orders, a liquidation incentive is added incrementally to the order, and it is then reposted to the order book.

The initial incentive will be to price the order at a 1% more attractive price relative to the mark price of the position. That incentive will then increase over time by a fixed amount.. As the incentive increases, it is likely that the liquidation order crosses an existing bid or ask in the order book, either from a market maker providing liquidity on Kyan, or simply another trader with a limit order. This may provide the taker of a liquidated position with a more attractive price and trading opportunity, particularly as the incentive increases.

From a more user-friendly approach to liquidations, the ability to trade up to 6 different options legs at once, and the inclusion of perpetual futures contracts as a built-in mechanism for portfolio hedging, Kyan has many features that may appeal to options traders. Its focus on designing a risk engine that closely matches Deribit is a design choice in order to prioritize the main goal of the protocol: reducing the switching cost as much as possible for traders coming from centralized exchanges into the DeFi space.

The focus on the ‘CEX in a DEX’ goal however does come with its tradeoffs: the margin computations required to be calculated before opening and closing positions would be gas-incentive if done on-chain, given that 43 different market scenarios are evaluated per portfolio. This means Kyan has opted to do these calculations offchain, and they are displayed on a user’s account via an API. It also means that trades are accepted or rejected based on these computations and users are forced to trust the calculations without the same transparency as they otherwise would have with on-chain computation.

For those who are interested in testing Kyan, a public beta launch is expected in October 2025.

.jpg)

.jpg)