Thahbib Rahman

Research Analyst

The demand for decentralized perpetual swap contract exchanges (perp DEXs) has emerged as a key narrative in crypto markets, particularly since September 2025. In this report we aim to understand exactly why perp DEXs are experiencing unprecedented growth in volumes and fees, what advantages (and disadvantages) they have over traditional centralized venues (CEXs) and whether metrics such as fee generation can provide insight into the value of a perp DEX’s native token.

The demand for decentralized perpetual swap contract exchanges (perp DEXs) has emerged as a key narrative in crypto markets, particularly since September 2025. In this report we aim to understand exactly why perp DEXs are experiencing unprecedented growth in volumes and fees, what advantages (and disadvantages) they have over traditional centralized venues (CEXs) and whether metrics such as fee generation can provide insight into the value of a perp DEX’s native token.

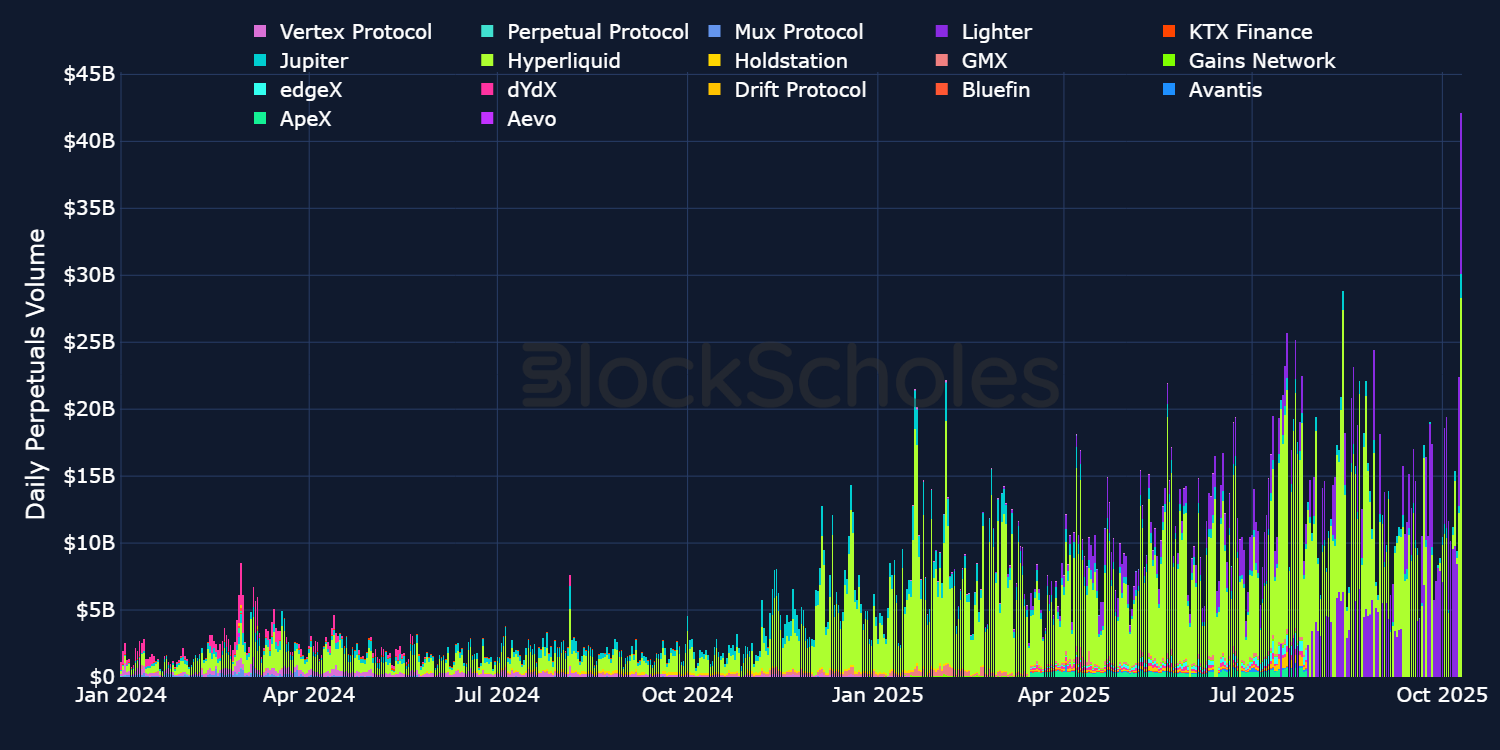

Decentralized venues that provide traders access to high leverage perpetual swap contracts really began to explode in trade volumes back in November 2024. That was following the election victory of US President Donald Trump, who has championed cryptocurrencies and the digital asset space.

Interestingly, that parabolic rally in the total daily perp trading volume was concentrated in just a few DEXs: Hyperliquid, edgeX Exchange and Lighter. When we exclude these, we find that perpetual swap volumes have for the most part actually been flat over the period between 2024 and 2025.

Hyperliquid has emerged as the new leader of the perp DEX space. Despite launching back in 2023, the perp DEX’s volumes first picked up momentum during the broad-based crypto rally that followed President Trump’s re-election, and then again following the launch of its native HYPE token on Nov 29, 2024. Since the start of 2024, 58% of the volume across the top eight perp DEXs has been routed through the Hyperliquid protocol alone.

The other two DEXs responsible for the exponential increase in perp activity are edgeX Exchange and Lighter, both launched slightly later. edgeX Exchange launched its mainnet in early 2025, while Lighter announced its mainnet on Oct 2, 2025, following eight months of a private beta.

However, the most recent parabolic ascent in interest toward these exchanges was ignited by the launch of Aster in Sep 17, 2025. Aster, a multichain DEX (backed by YZi Labs, the crypto investment firm of Changpeng “CZ” Zhao, co-founder of Binance), is looking to challenge Hyperliquid. (Due to the relatively new launch of Aster and the lack of available data, we’ve chosen to omit the exchange from our analysis in this report.)

Despite this explosion, volumes across all perps on DEXs are comparable to those on a single CEX, such as Bybit. At their peak, perp DEX volumes exceeded those on Bybit by around $10B. However, excluding the one-off high, volumes on perp DEXs tend to regularly trade above the $10B mark. While that is a major feat for these protocols from far lower levels earlier in 2024, it is still generally lower than those on Bybit, where volumes regularly exceed $20B.

Most cryptocurrency users are well versed with traditional decentralized exchanges (DEXs) such as Uniswap. These exchanges primarily focus on facilitating the trading of spot pairs (actual tokens), not perpetual contracts — which instead are derivatives that offer synthetic exposure to the underlying asset.

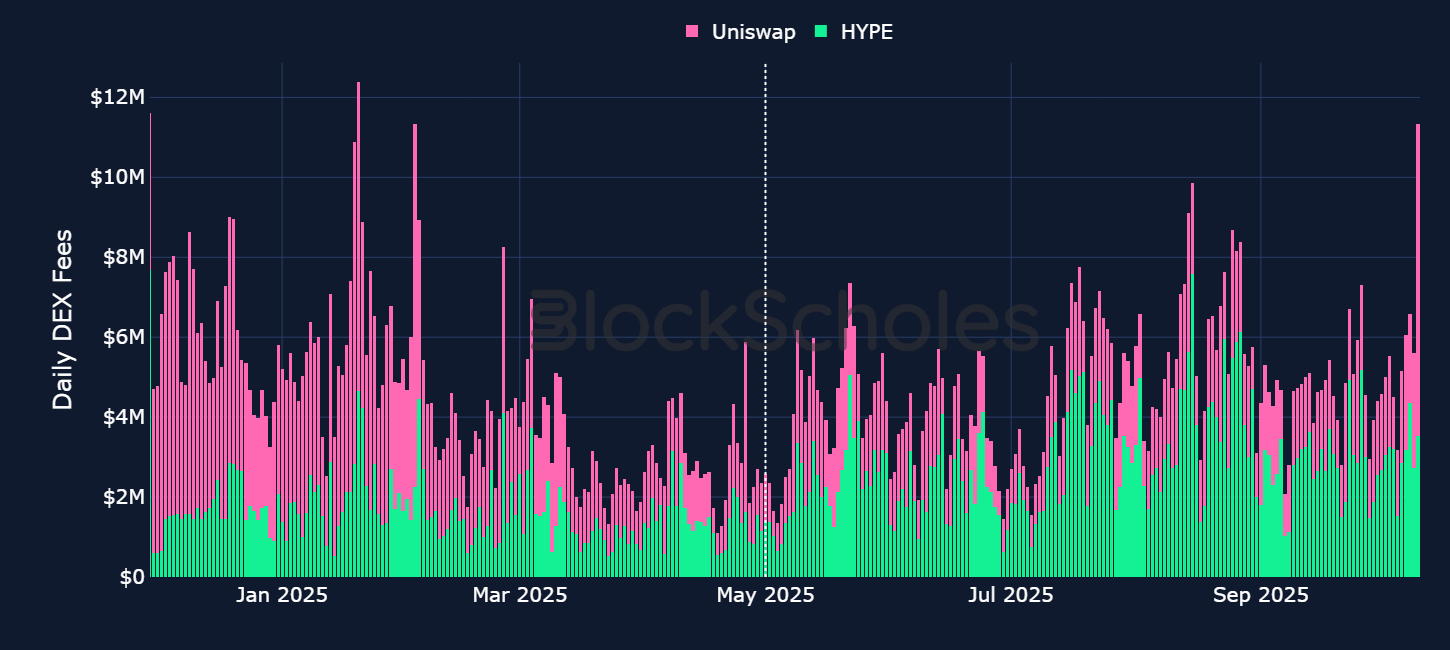

The recent explosion in perp DEXs has seen these perp DEXs generate more fees per day than traditional spot DEXs and contribute a greater proportion to the overall fees generated on the chain within which they operate.

According to CoinGecko data, Uniswap is the largest spot DEX on the Ethereum blockchain, accounting for 58% of the total volume on Ethereum-based DEXs (across all types of DEXs). Similarly, Orca accounts for 36% of total volumes on Solana. On Base (the popular, low-cost Ethereum Layer 2), spot DEX Aerodrome Finance accounts for 50% of the trading volume. Taking these three DEXs as a proxy for the total fees generated by spot DEXs across major blockchains since late January 2025, fees generated across major perp DEXs have far outweighed those generated by the largest spot DEXs on Solana, Ethereum and Base.

In fact, since May 2025, Hyperliquid has consistently generated higher fee revenues on a daily basis than Uniswap. From the beginning of the year, fees generated on Hyperliquid have on average exceeded Uniswap’s by 1.3x. The difference becomes even more apparent when we compare fees across both protocols. Hyperliquid fees range between 0.0150% and 0.0450%; compared to Uniswap, whose fees are between 0.01% and 1%. Therefore, volumes on Hyperliquid are magnitudes larger than Uniswap, such that — despite charging lower fees per trade — Hyperliquid still manages to generate a larger premium over Uniswap in protocol fees. A similar analysis relative to Orca and Aerodrome shows Hyperliquid’s fees have been 7.2x and 4.9x higher on average (per day), respectively, since 2025.

Two things are apparent: Despite charging lower fees per trade, the explosion in volumes on perp DEXs is so large that these protocols are contributing more to the total fees generated on the chains they operate than spot DEXs. Secondly, in the case of Hyperliquid, fees paid by users on the exchange now make up between 20% and 60% of the total fees generated across some of the largest blockchains.

If perp DEXs are now accounting for so much volume (and so many fees), can we point to some reasons why?

Perp DEXs offer a slightly different trading experience from both spot DEXs and perp CEXs. Following are some of the reasons why (or why not) trading perpetual swaps on DEXs has skyrocketed in popularity over the past 12 months.

Centralized exchanges (CEXs) commonly require users to adhere to strict regulatory standards. For individual traders, this typically requires a standard know your customer (KYC) process to verify identity. For institutions, onboarding extends to know your business (KYB) checks, which involve confirming the business entity and its ownership structure. Major CEX platforms enforce these checks before granting access to advanced trading products, such as futures and perpetual contracts. While these checks are important for CEXs in terms of security and compliance, traders who want to start immediately face delays and a lack of anonymity.

In contrast, many perpetual DEXs position themselves as operators or “facilitators” of trading, claiming that a trader using a perpetual DEX doesn’t create an account with a central entity or give custody of their assets to an operator but simply interacts with a smart contract. Since (in most cases) the smart contract custodies user assets (rather than the protocol operator), doesn’t store personal data and doesn’t process fiat money, there’s no regulatory obligation to verify identities in the same way that a traditional exchange must do. This means that many DEXs don’t implement mandatory checks.

However, this legal claim to autonomy is less clear when the operators run a centralized front end, earn fees from trading activity or retain control over protocol upgrades. In such situations, authorities may consider these entities to be providing a regulated service to users. As a result, organizations like Uniswap Labs and dYdX Trading Inc. have implemented geo-restrictions or partnered with KYC providers for certain users. These measures aren’t required by the underlying decentralized protocols themselves, but are instead designed to protect the legal entities that operate the user-facing interfaces.

Not all DEXs follow this model. Platforms such as GRVT are building hybrid approaches, whereby trading remains noncustodial but access is gated by identity checks or KYB procedures. As a result, while many DEXs still emphasize this frictionless onboarding, the perp DEX market is still split between fully permissionless platforms and regulated DEXs that trade some ease of access for credibility.

Faster listing of new tokens is one of the clearest advantages of DEXs. Because most decentralized platforms are permissionless, new tokens can be listed almost immediately once liquidity is provided or an oracle is configured.

In contrast, listings for many CEXs involve formal applications, legal checks and liquidity arrangements. For instance, Coinbase has an internal asset listing policy that requires compliance and legal review before approval, which in some cases may take some time. Coinbase states that their due diligence typically takes about a week, with trading enabled within two weeks of approval, though the full timeline can extend up to 30 days, depending upon an asset’s complexity and technical requirements.

In many cases, new token listings on DEXs are determined by governance proposals, tokenholder voting or liquidity bootstrapping pools, depending upon the protocol’s design. For bonding curve–based perpetual DEXs, the main technical requirement is sufficient liquidity secured by community liquidity deposit requirements.

In contrast, perp DEXs with central limit order book implementations must ensure that an oracle price feed is available, there’s enough liquidity provided by market makers and the smart contract setup is audited. Some DEXs streamline this process through community engagement, whereby these requirements can be proposed and voted on in community governance forums. This way, despite the extra steps, a token can go live within hours or days.

One of the clearest distinctions between DEXs and CEXs is in which trader assets are custodied. On a CEX, users must deposit funds into exchange-controlled wallets. This creates counterparty risk: if the platform fails, funds can be frozen or lost.

In contrast, most perp DEXs are self-custodial. Traders connect with their own wallets, and assets remain under their control until a transaction is executed. Settlement occurs directly on-chain via smart contracts, eliminating the need for an intermediary.

Perp DEXs also differ from CEXs in the way they structure trading costs and leverage. On Hyperliquid, for example, fees are based on a rolling 14-day volume and are assessed daily. Maker rebates are paid out continuously on each trade, directly to the trader’s connected trading wallet, and there are separate fee schedules for perpetuals and spot. At the base tier, taker fees start at 0.045% and maker fees at 0.015%, with the lowest available tier reducing taker fees to 0.024% and bringing maker fees down to 0% so that high-volume traders can effectively earn rebates by providing liquidity.

CEXs such as Deribit operate on a simpler structure, with nearly zero fees for makers. For example, on Bitcoin perpetuals, makers pay 0.00%, while takers pay 0.05%.

Leverage is another feature that differs between exchanges. Hyperliquid offers up to 40x leverage, while protocols such as GMX allow up to 100x. Bybit’s perpetual contracts support leverage of up to 100x on many pairs, although the exact maximum varies by asset, and certain products — such as Pre-Market Perpetuals — are capped at much lower levels, such as 5x. Meanwhile, Deribit offers perpetual and futures contracts with leverage of up to 50x.

In traditional CEXs, the exchange’s internal systems manage collateral, margin and liquidations entirely off-chain, requiring traders to deposit funds into the exchange’s custody and trust that the exchange handles funds and risk fairly. DEX perp protocols rely on oracle-fed margin calculations to calculate margin ratios, with the subsequent liquidation steps handled automatically by smart contracts.

Some DEXs — such as dYdX, Hyperliquid and Aevo — instead use auto-deleveraging (ADL) as a backup mechanism. If a liquidated position cannot fully be closed, the system automatically reduces the exposure of opposing traders, starting with those holding the highest leverage or largest profits, to restore balance. This process helps maintain overall system solvency, but can result in “unfair” closures for affected traders.

However, in extreme circumstances where losses outweigh recovery mechanism balances, the protocol will become insolvent. All open positions are automatically liquidated or frozen to prevent further losses. Since the protocol cannot fully repay what is owed, users incur losses and, depending upon the protocol’s design, this can result in either a partial loss — whereby users recover only a portion of their collateral — or a total loss. Since the perp DEX is a smart contract, no central authority will be held responsible for these losses.

However, these advantages come with important drawbacks. One significant disadvantage is privacy: on a DEX, every trade, position and liquidation is recorded on-chain and is visible to the public in real time. Although this transparency builds trust in how the protocol operates, it creates sensitivity for traders whose strategies, position sizes or order flows are effectively open to competitors. For institutions, this lack of confidentiality is an important obstacle.

One major drawback for many perpetual DEXs is in execution latency, particularly on AMM-based platforms. Because every trade must be processed and confirmed on-chain, execution speed is limited by block times. In practice, this can cause delays and slippage if markets move while a transaction is still pending. CEXs, in comparison, run high-performance matching engines that process trades in milliseconds and are supported by professional market makers to maintain depth.

More advanced perpetual DEXs have moved away from pure AMM designs toward central limit order book (CLOB) models. For example, dYdX v4 uses in-memory order books maintained by validators, allowing trades to be matched off-chain before settlement is finalized on-chain. This greatly reduces the issue of latency, though settlement is still tied to block confirmation and relies on validator or sequencer infrastructure.

CEXs and DEXs differ not only in regulation and onboarding, but also in how they source liquidity. CEXs usually require designated market makers to provide liquidity when a new asset is listed, which can delay trading until those arrangements are in place.

In contrast, there are three main ways that DEXs match orders and source liquidity:

AMM models like GMX’s allow anyone to supply liquidity by depositing tokens into a pool, so markets can launch almost instantly without relying on professional market makers.

That said, for order book–based DEXs, such as dYdX, Derive or GRVT, market makers are still necessary in order to maintain spreads and depth. Order book–based DEXs work by matching users in opposing positions, meaning a buy order will be matched with a sell order of the same amount, with the trade settled and executed on-chain. If a user's portfolio falls below margin requirements, the smart contract liquidates it automatically. Efficient liquidations are based on trustworthy data delivered by a trusted oracle, and are a key mechanism that oracle-based perp DEXs such as Hyperliquid and dYdX (v3 and v4) rely upon when offering high leverage.

Although DEXs could offer a fully on-chain order book or matching engine, allowing for complete transparency in terms of where transactions are processed and stored on the blockchain, most DEXs choose to keep this matching component off-chain for large cost-efficiency gains.

Other perp DEXs such as Perpetual Protocol (v2) use AMM-implied internal pricing to determine when to liquidate positions. In this model, the on-DEX price of an asset is used for margin calculations. The main advantage of this approach is that it operates entirely on-chain, making it faster and more transparent without relying upon external data feeds.

However, this price feed can be vulnerable to manipulation, since large trades relative to the liquidity available in the pool can distort the pool’s price. This creates a discrepancy between the real spot price of a token and the tradable price within the perp DEX’s liquidity pool, which results in incorrect liquidations of collateral. To mitigate this possibility, some protocols, including GMX (v1 & v2) and Drift Protocol (v1), adopt hybrid systems that combine AMM-implied and oracle-based pricing for greater accuracy.

HYPE has become the largest perp DEX by fees and volumes, and has taken a significant share of the market away from CEXs and traditional spot DEXs. How — if at all — has this translated to its spot price?

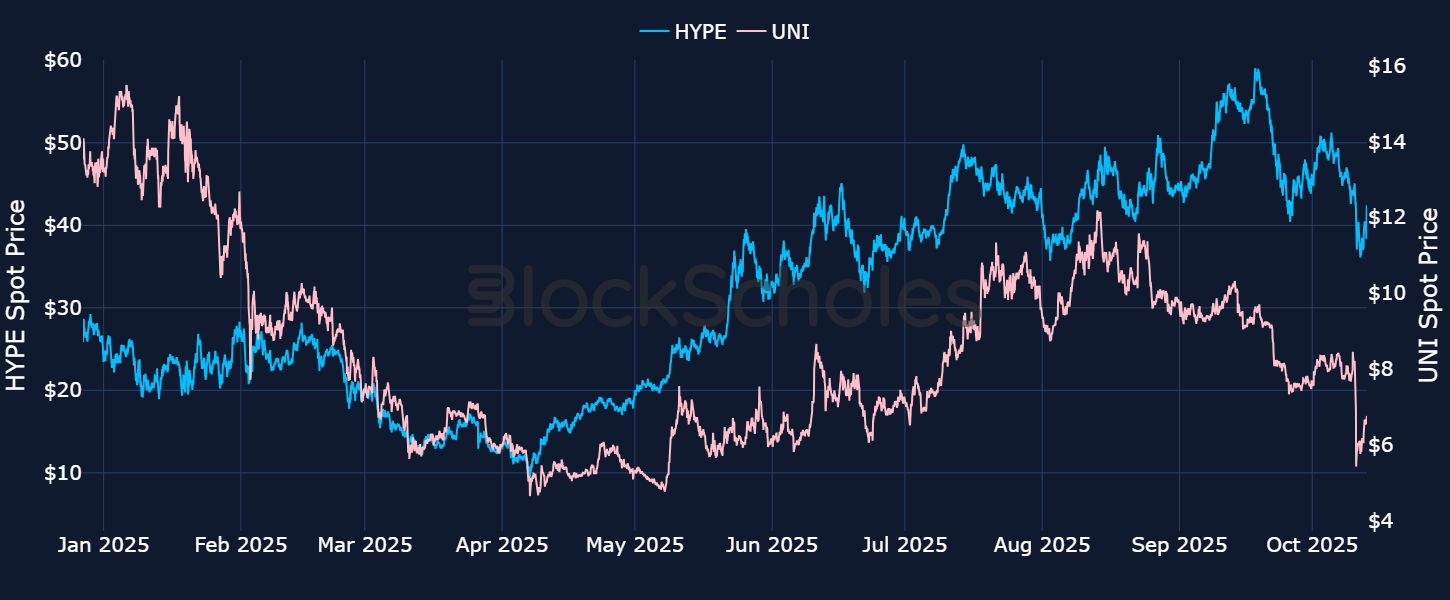

Below, we plot the HYPE token against UNI since January 2025. Both assets followed a similar Q1 trajectory, but after bottoming in April, a noticeable divergence played out. UNI only modestly rebounded, and has yet to reclaim even close to the $50 mark from which it fell. On the other hand, HYPE is up more than 6x from its April low, and 2x year-to-date.

The drop in spot prices in early 2025 was a broad-based crypto move based on changes in the macro environment. Risk-on assets — including crypto and US equities — saw sharp declines as President Trump began a flurry of tariff announcements. This suggested that even the explosion in on-chain metrics supporting the growth of Hyperliquid wasn’t enough to resist the gravitational pull of BTC and the broader macro-based slowdown.

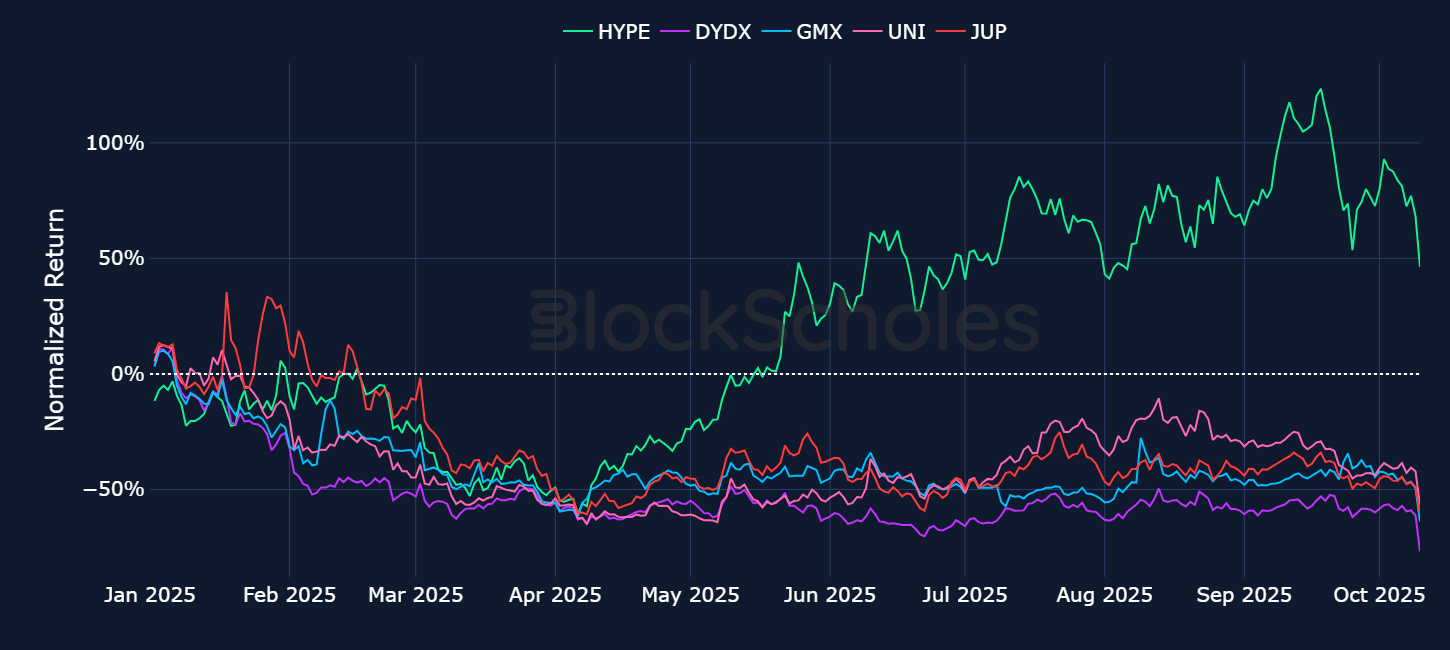

But what about the post-April rally? Is it reflective of all perp DEX tokens, or was it limited only to HYPE? When we compare the normalized returns of HYPE to those of JUP [the native token of the Jupiter perp (and spot) DEX], DYDX (the native token of the dYdX perp exchange) and GMX (the native token of the GMX exchange), we find that HYPE is clearly the outlier — as all of the aforementioned tokens’ prices are down close to 50% year-to-date, similar to spot DEX tokens such as UNI.

Could this reflect HYPE’s market share grab from the previous leaders in the DEX space? There is some evidence to support this assertion. At the beginning of this article, we explained that Hyperliquid began to overtake Uniswap in total daily DEX fees from May 2025. The almost vertical doubling in HYPE’s price from below $20 to upwards of $40 in May coincides with the period in which Hyperliquid began to outperform Uniswap in daily fee generation.

However, it’s equally difficult to contextualize all of HYPE’s rally relative to the performance of UNI alone. That’s because UNI (see below) has structurally been on a decline since its highs of the 2021 altcoin cycle.

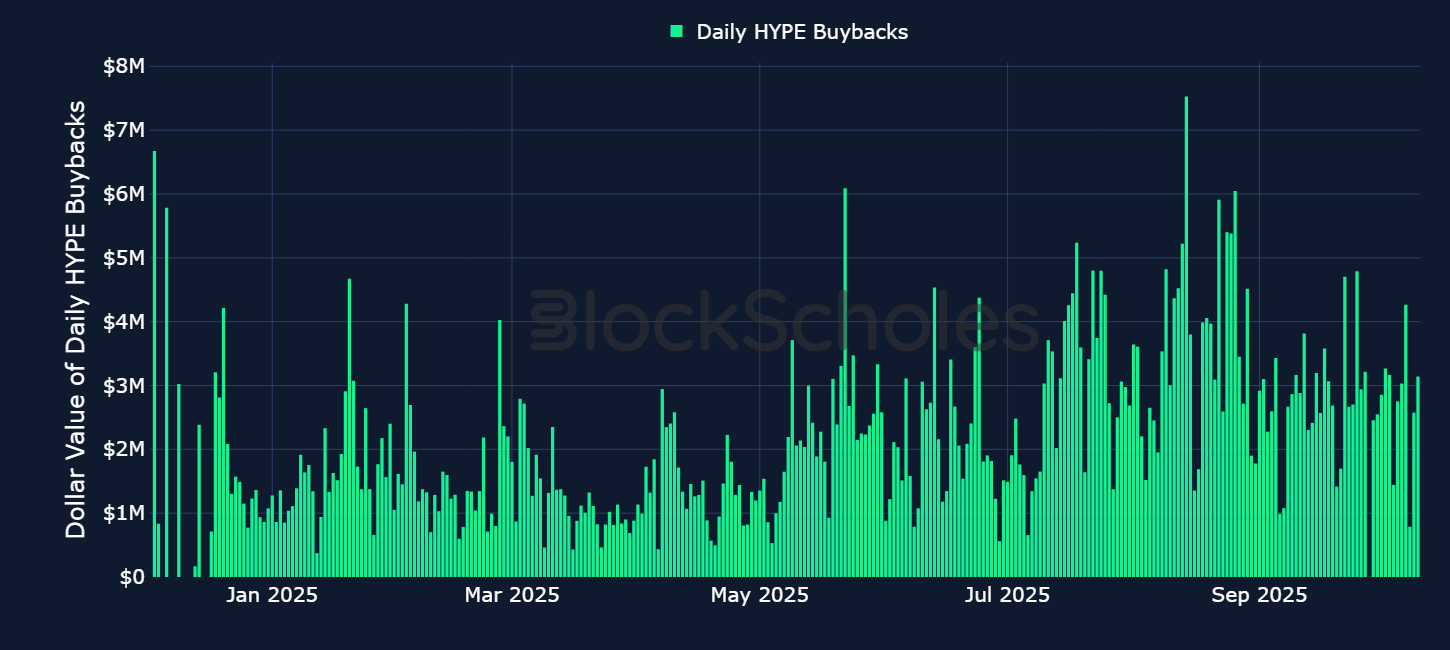

Another potential factor contributing to HYPE’s success is its buyback program. Ninety-seven percent of Hyperliquid’s revenues are allocated to an assistance fund that uses the funds to buy back HYPE tokens. This has a flywheel effect on the value of the HYPE token. The higher the volume of trades on the Hyperliquid platform, the more fees are generated on the protocol. This has two effects:

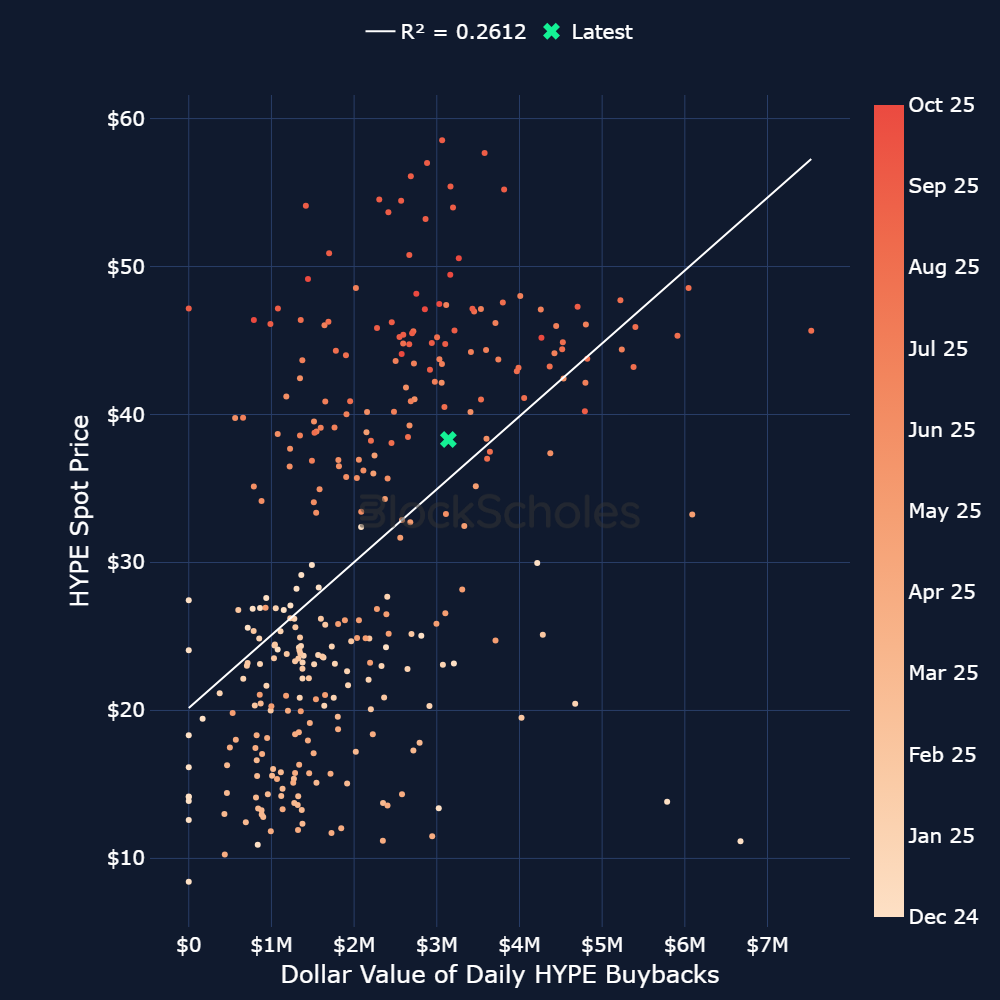

When we plot the dollar value of daily token buybacks, we find that — at times — Hyperliquid has purchased upwards of $6M worth of their native token, and that since May 2025, purchases above $2M have become the norm. Additionally, we find evidence that the buybacks do have a relationship with HYPE’s price. Below, we regress HYPE’s daily spot price against the dollar value of daily buybacks. According to this linear relationship, approximately 26% of the variation in HYPE’s price can be explained by token buybacks.

It’s important to note that other perp DEXs have also adopted such a strategy, likely after seeing Hyperliquid’s success. However, the buyback programs announced by Hyperliquid’s competitor DEXs allocate a smaller percentage of their revenues. For example, in late January 2025, the founder of Jupiter announced that its platform would allocate 50% of its fees to buybacks. And in March 2025, dYdX announced its first DYDX buyback program (“25% of net protocol fees will be allocated to monthly buybacks”).

One thing to watch for is an upcoming token unlock, scheduled to begin on Nov 29, 2025. Approximately 237.8M HYPE tokens will be vested over a period of 24 months. We can compare this increase in the supply of HYPE tokens relative to the buyback program in order to understand what impact it may have on the price of HYPE.

Since the launch of the token, the average number of daily HYPE tokens bought back by the assistance fund has been 75,888 tokens (equivalent to 2,227,652 tokens per month). Therefore, despite such an aggressive buyback strategy, at the current rate only 23% of the monthly issuance is likely to be absorbed by current buyback programs (assuming a linear token unlock). This could overpower the reduction in the supply of HYPE tokens from the buyback initiative.

The rise of perpetual decentralized exchanges (perp DEXs) since late 2024 has been driven by a surge in trading volumes following US president Donald Trump’s pro-crypto policies and the launch of high-performing platforms, such as Hyperliquid, edgeX Exchange and Lighter. Hyperliquid alone accounted for 58% of total volume across the top eight perp DEXs in 2025, with its growth accelerating further after the release of its native HYPE token. While perp DEX volumes occasionally match the levels of major centralized exchanges (such as Bybit) by around $10B at their peak, average daily volumes generally remain lower, despite the significant progress from early 2024 levels.

Perp DEXs have also overtaken traditional spot DEXs — such as Uniswap, Orca and Aerodrome — in terms of daily fee generation, with Hyperliquid consistently earning more fees than Uniswap since May 2025. The platform’s fee revenues, which make up 20–60% of the total fees across major blockchains, have also been linked to HYPE’s strong price performance, supported by its aggressive buyback program that allocates 97% of revenues to token repurchases. However, despite this support, upcoming token unlocks could offset some of the positive price effects from buybacks.

Overall, the rapid growth in volume, fees and token value illustrates how perp DEXs have become a central part of the crypto trading ecosystem during 2025.

.jpg)

.jpg)