Thahbib Rahman

Research Analyst

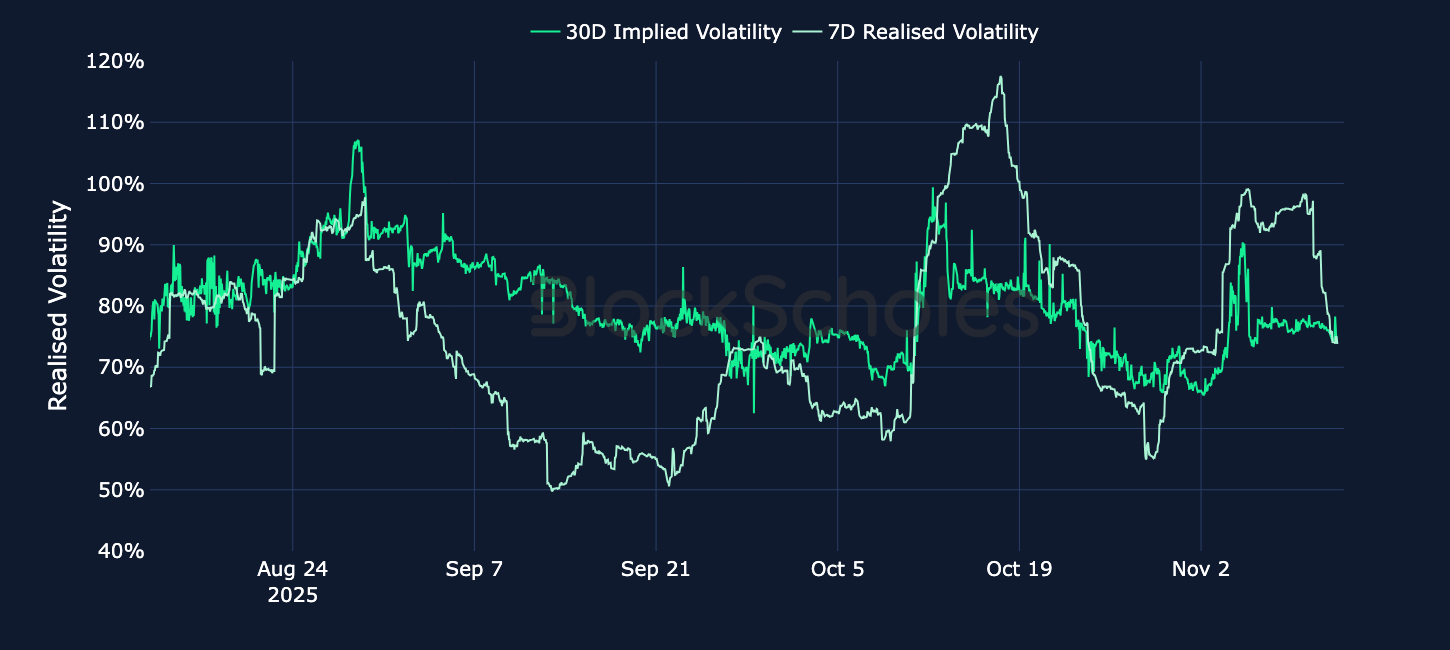

U.S. equities continue to scrape against all-time highs, buoyed by signs that the government shut-down is nearing an end. However, crypto-assets have failed to enjoy the same positive sentiment, with every attempt by spot prices to re-rally back to the levels lost in successive October and November sell-offs met with resistance. The bearish slog in spot markets is marked by signs of bearish position-taking in derivatives markets, as implied volatility levels refuse to return to the lower levels that they traded at in September and volatility smiles price-in a relative premium for protective puts.

U.S. equities continue to scrape against all-time highs, buoyed by signs that the government shut-down is nearing an end. However, crypto-assets have failed to enjoy the same positive sentiment, with every attempt by spot prices to re-rally back to the levels lost in successive October and November sell-offs met with resistance. The bearish slog in spot markets is marked by signs of bearish position-taking in derivatives markets, as implied volatility levels refuse to return to the lower levels that they traded at in September and volatility smiles price-in a relative premium for protective puts.

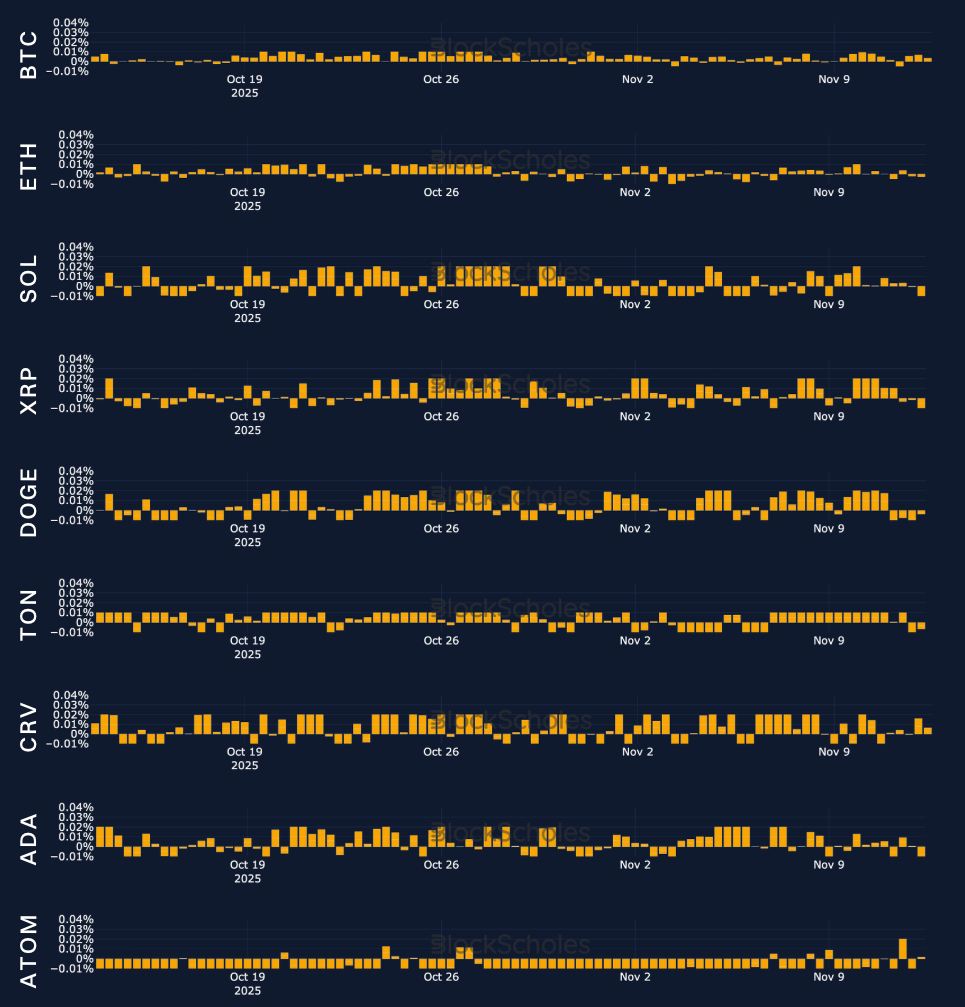

Perpetuals: Funding rates in majors present a mixed picture of sentiment, while those of altcoins are titled bearishly in a reflection of their underperformance relative to spot.

Options: Volatility expectations implied by the price of options remain elevated, with a strong skew towards bearish put contracts.

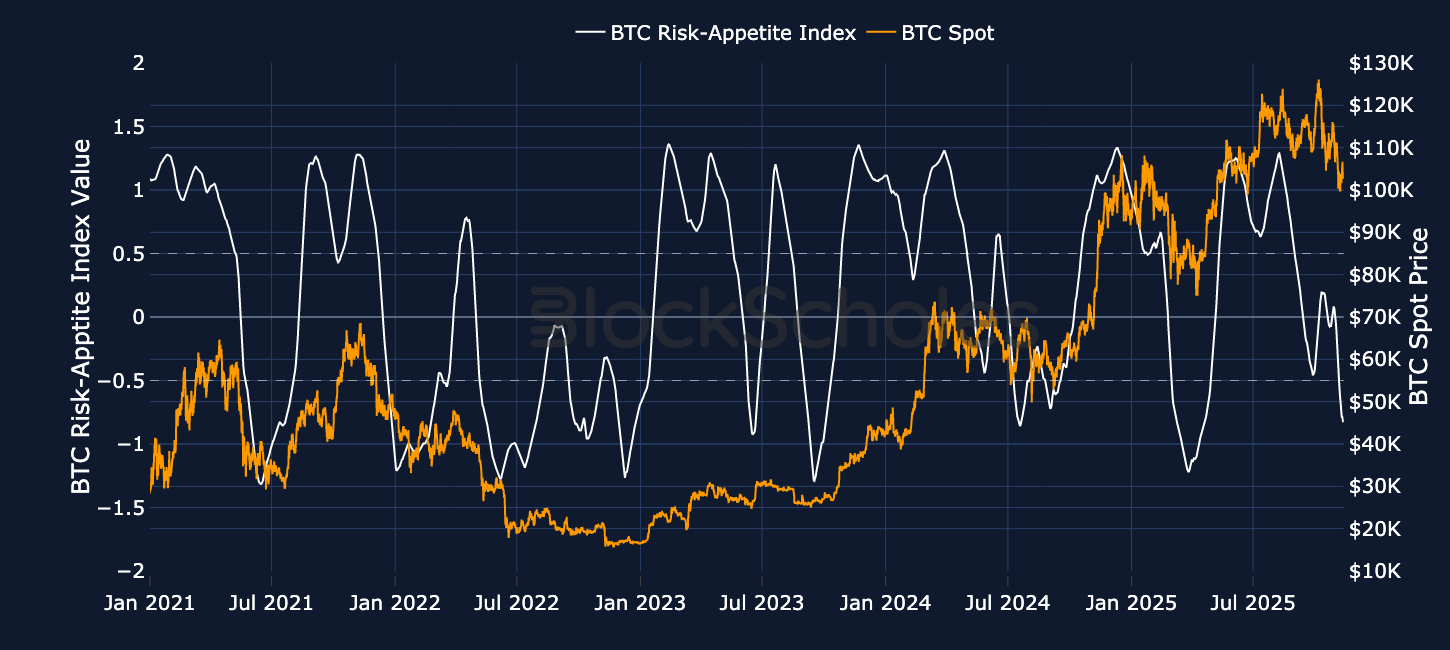

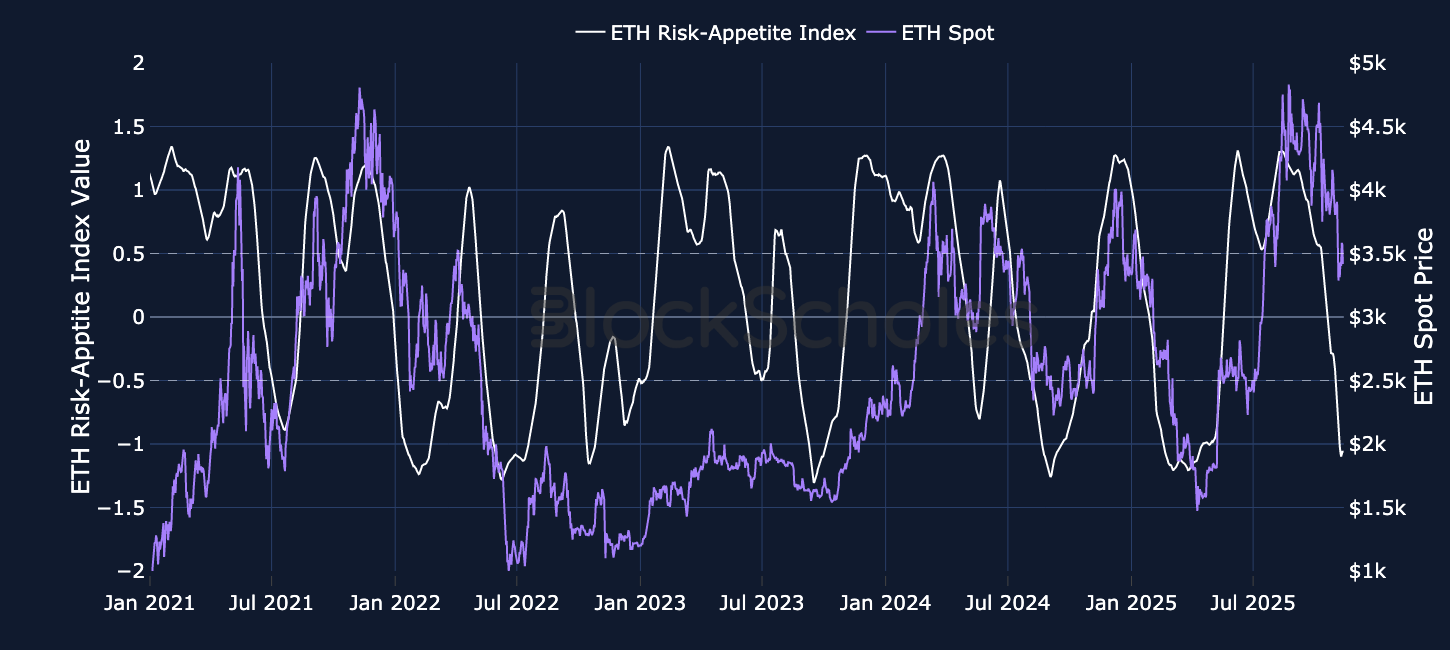

Block Scholes’s Senti-Meter Index aggregates the funding rate, future-implied yield and volatility smile skew into a single expression of sentiment in derivatives markets. See more in the methodology article here.

Canton Coin (ticker CC) is one of the newest tokens on Bybit, with the CC/USDT market introduced on Nov 10, 2025. Canton Coin serves as the native utility token of Canton Network, a Layer 1 public and permissionless blockchain tailored for institutional financial use.

Introduced in May 2023, the Canton Network emerged from a collective industry effort aimed at modernizing global capital market infrastructures, particularly in post-trade and settlement processes. Its development was driven by collaboration among prominent institutions including BNP Paribas, Capgemini, CBOE, Deloitte, Deutsche Börse, Digital Asset, Goldman Sachs, Microsoft, Moody’s and Paxos.

The Canton Coin itself is used to cover transaction fees on the network, to incentivize and reward ecosystem participants such as validators, developers, and users on the network and can also be used by application providers to charge for their services.

The network aims for its token supply to be in “equilibrium” with all Canton network fees paid in CC burned while new coins are minted as rewards to be distributed to validators based on activity and to application creators building on the Canton Network, particularly those working on institutional projects such as tokenizing real-world assets (RWAs). Canton estimates an issuance and burning of roughly 2.5B coins annually to maintain a balanced supply over time.

Institutional adoption for Canton appears robust – institutional asset manager Franklin Templeton has connected its blockchain infrastructure to allow for its “Benji” token, which tokenizes shares in a yield-bearing money market fund to be traded on the network. Sandy Kaulm, Head of innovation at Franklin Templeton, said that institutions “wanted the ability to have privacy around trades, they did not want their trades to be recorded across public blockchains.” as its ecosystem webpage highlights participation from entities such as 21Shares, Bank of China, Bybit, and various banks. However, many of these major banks listed engage indirectly through third-party integrations; for instance, Bank of America, Barclays, and Citi interact with the Canton Network via Versana, a platform that digitizes syndicated loan data and portfolio positions.

Canton token (ticker CC), rallied upon listing and continues to hold value:

On November 6, Nasdaq-listed biotech firm Tharimmune Inc. (NASDAQ: THAR) announced the completion of a $545M private placement to create a Canton Coin digital asset treasury. Tharimmune announced they will use the money to purchase CC, set up a Canton Network “Super Validator,” operate and deploy additional validators across the network, and invest in Canton-based applications that advance institutional adoption within capital markets with remaining funds used for general corporate operations.

Markets Pivot to 12-15 Nov — In October, markets saw higher chance of a shutdown after 16 Nov, mostly mid-40s to low-50s and briefly above 60 in early November. On 9 Nov, that reversed: the 12–15 Nov window rose to 98%, while 16+ fell to near zero.

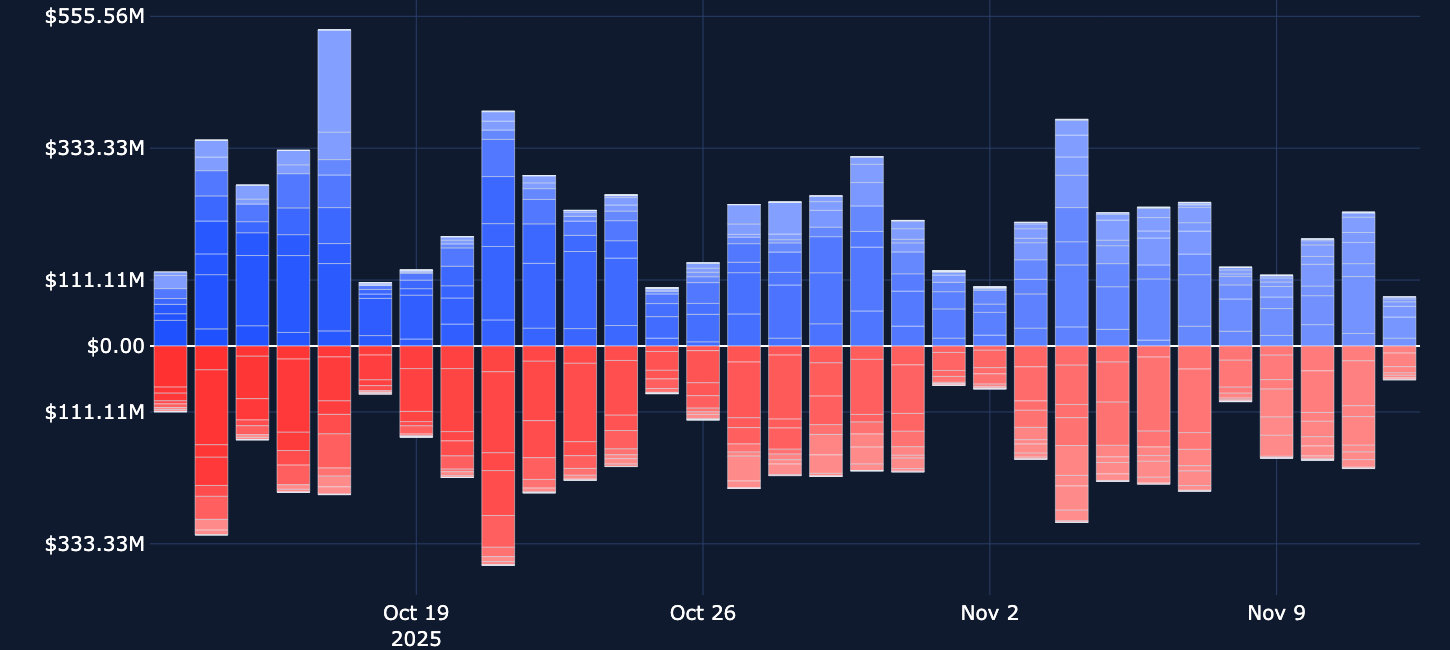

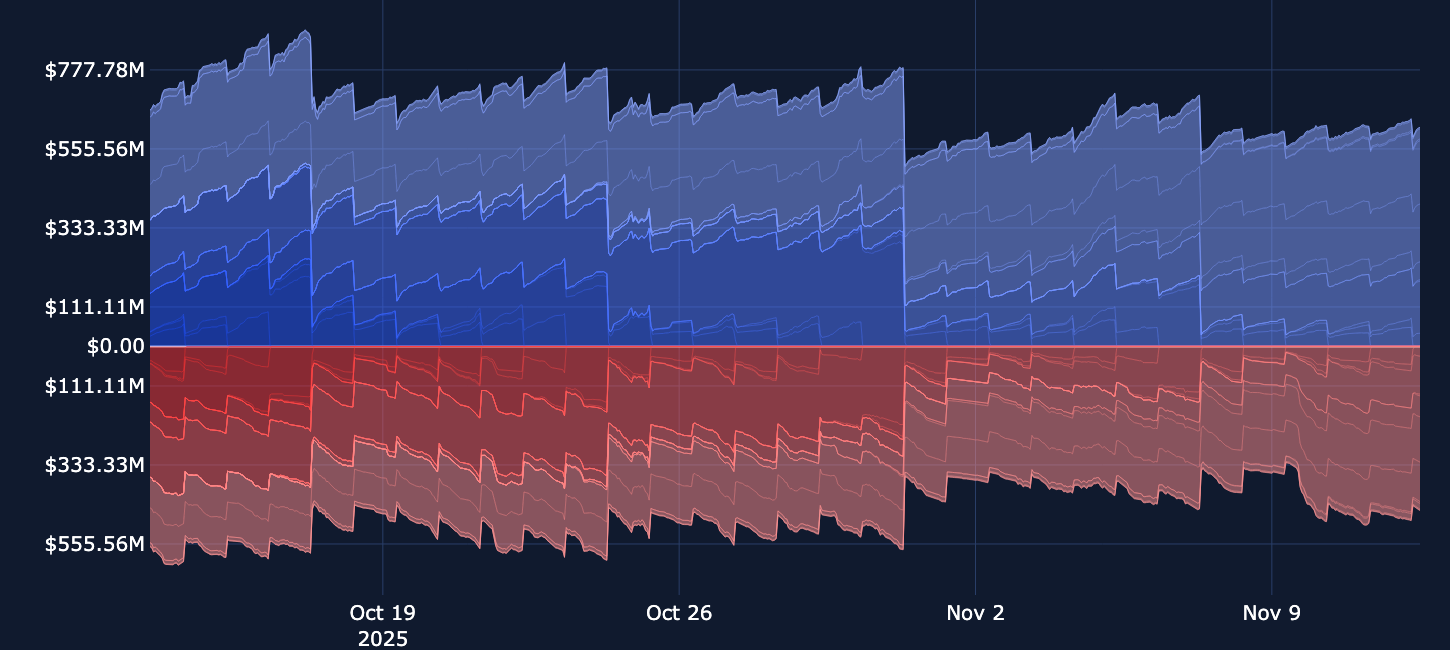

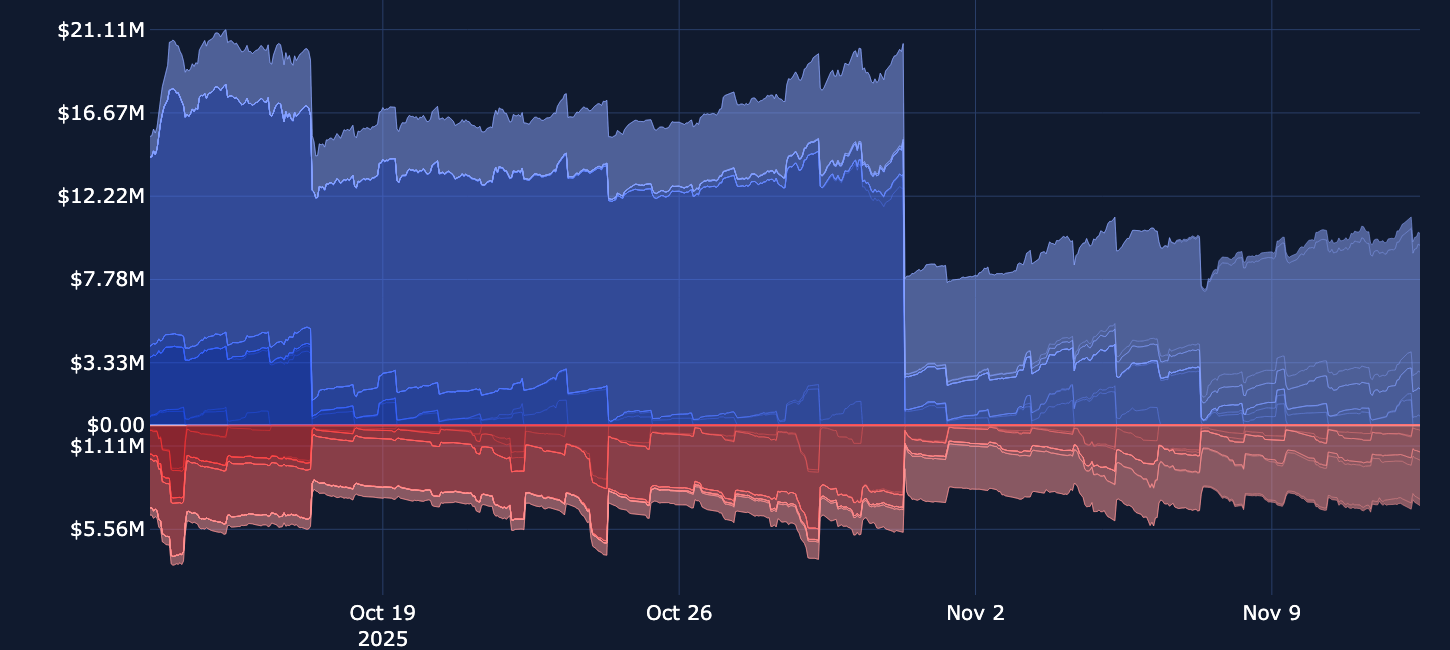

Bearish price action since the beginning of October 2025 has seen the open interest of large-cap perpetual swaps fall to almost half of their previous rates. The initial reversal from BTC’s all-time high in the first week of October triggered one of the largest liquidation events in crypto history. Far from recovering from that crash, the now lower levels of open interest indicate a reluctance to reopen those lost long positions.

That reluctance to open new perpetual swap positions has continued as spot prices (particularly those of altcoins, but also of majors like BTC and ETH) have since struggled to maintain any sort of momentum higher and back to the levels they lost. However, the sell-off in early November did not leave the same footprint on open interest, suggesting a lower level of leverage in the system at that time and therefore a lower level of liquidated positions.

Altcoins’ continued underperformance relative to majors like BTC and ETH is reflected in the funding rates of those tokens’ perpetual swaps. The funding rate of SOL, which is down 1% over the last 7 days in comparison to BTC’s +0.44% return, has struggled to remain persistently positive, an indication that short-exposure via the perp has frequently outweighed demand for long exposure. The same pattern of behaviour is seen in other large-cap altcoins, many of which have recorded their strongest bearish rates on Wednesday, November 12, 2025.

Despite U.S. equity markets appearing to shrug off much of the macroeconomic uncertainty triggered by the U.S. government’s shutdown, BTC leads other crypto-assets in a sluggish, pained attempt to re-rally following the spot price crash in early-November. Even though spot BTC managed to spike to a one-week high above $107,500 after the Nov 10 developments in the Senate, which ultimately paved the way for the shutdown’s end, the first-born crypto was unable to sustain such gains and duly faltered back into sub-$105k territory. At the time of writing, Bitcoin has so far merely offered a muted reaction to President Trump’s signing of the legislation that reopens the US government.

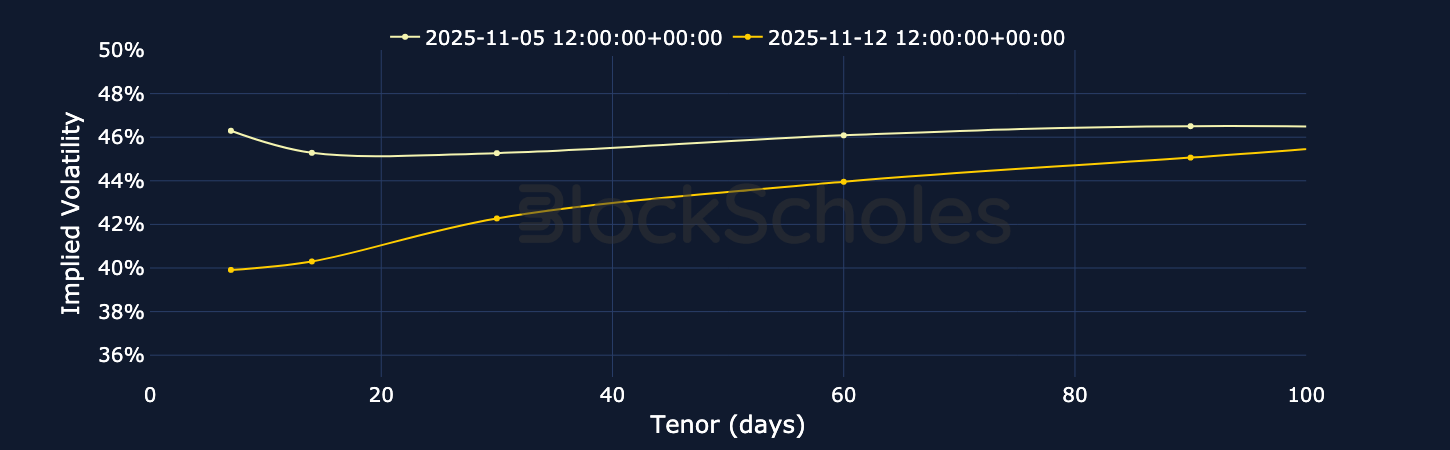

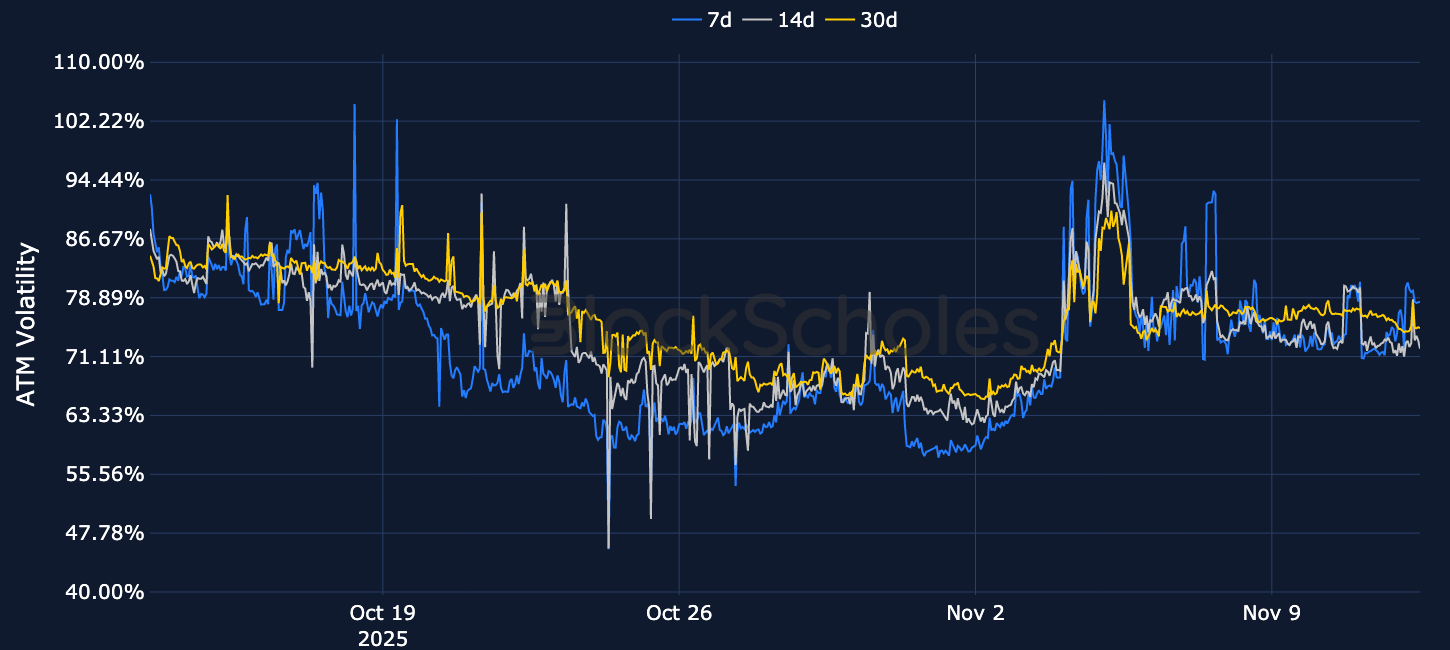

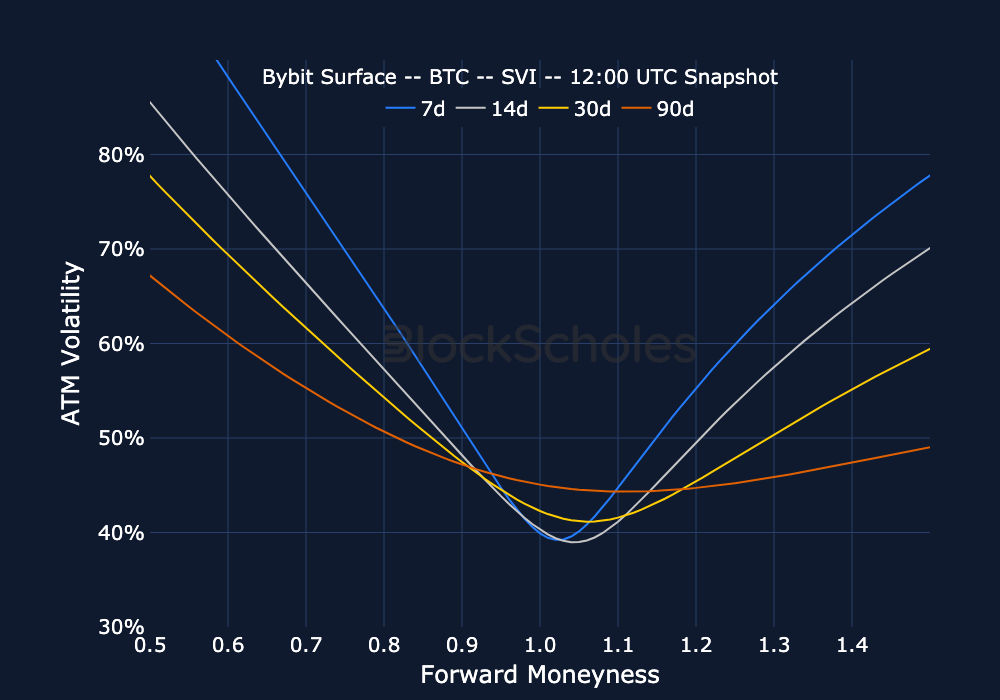

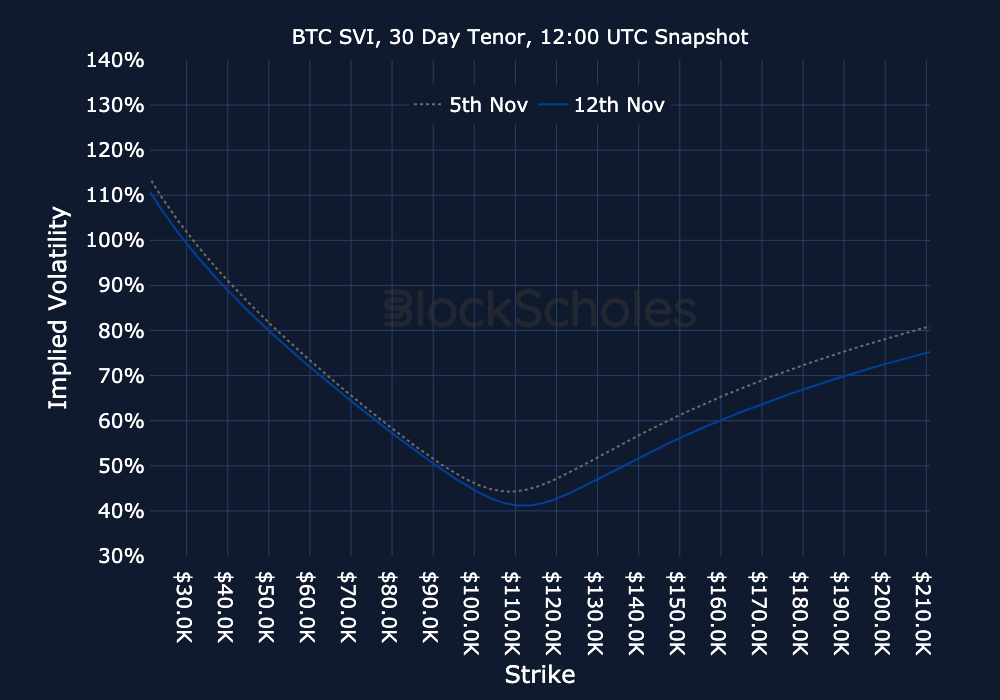

BTC options markets, unlike the perpetual swap funding rates of both BTC and ETH, suggest a strongly bearish tilt over short horizons. Volatility smiles are skewed towards puts, optionality is priced at a premium relative to the new-found low levels that we had become accustomed to over the Summer and activity (as indicated by the trade volumes or both puts and calls) has fallen in November relative to October.

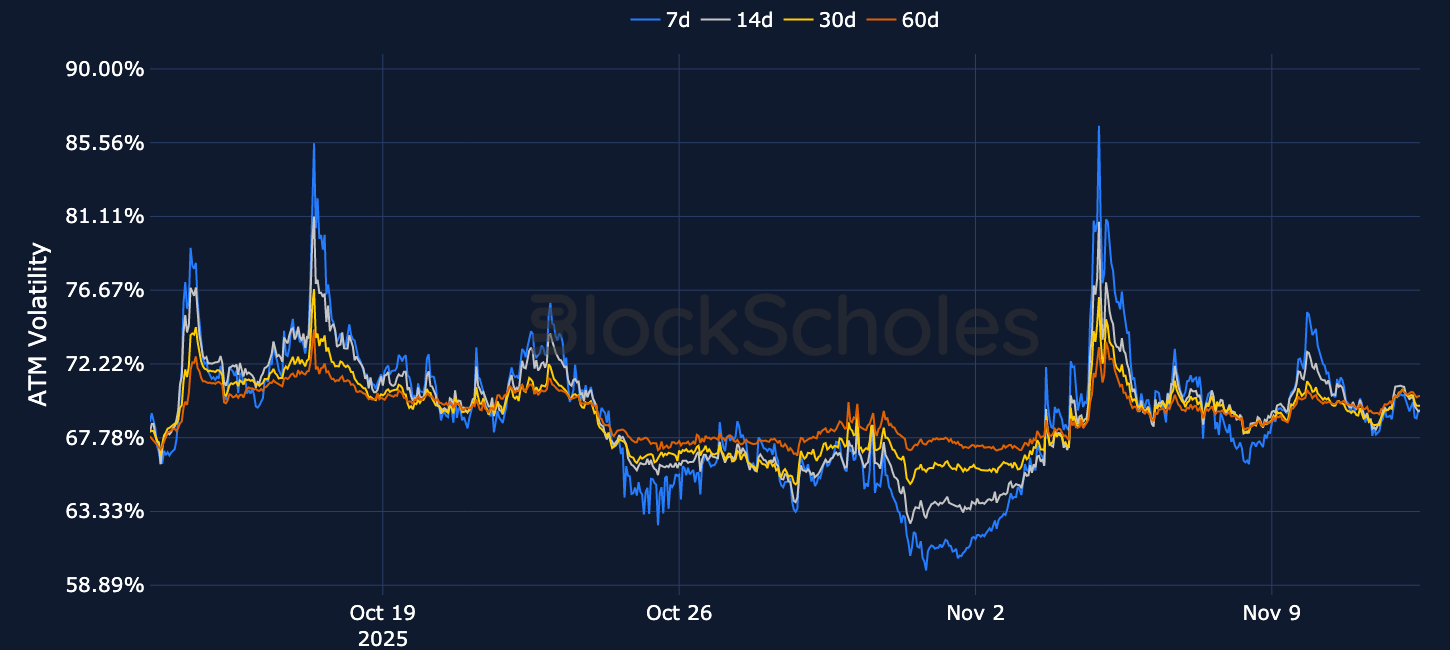

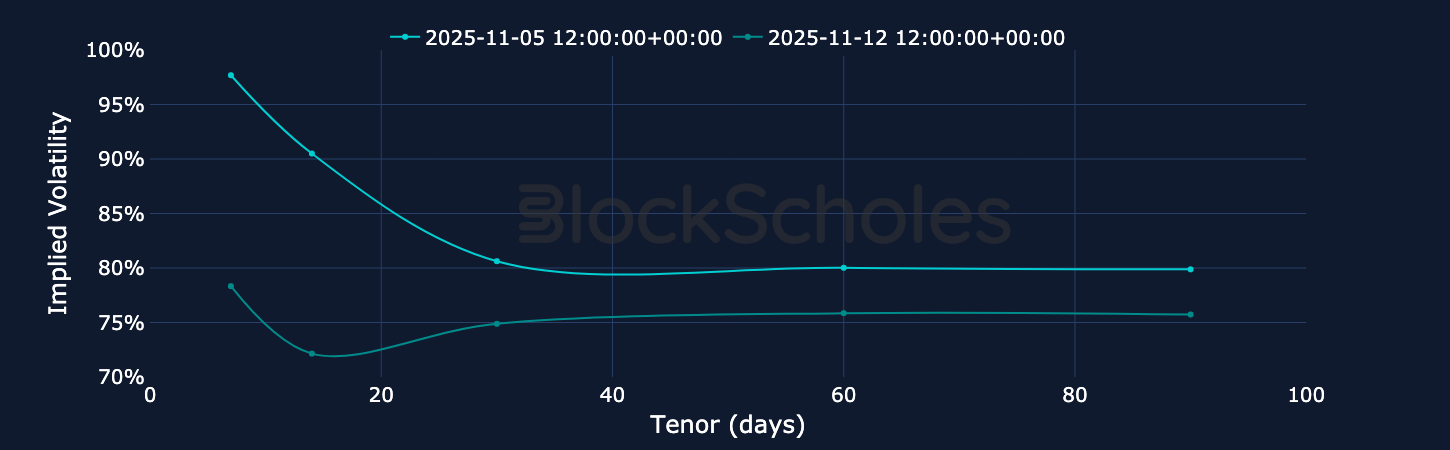

Realized volatility of ETH’s spot price has fallen, as there has been a distinct lack of further downside price action since the early November crash, as spot finds support around its 200-day simple moving average for much of November so far. However, volatility expectations remain high and sentiment remains bearish. This is clear from both trade volume data and the volatility surface, which both show that trading is focused on short-dated downside protection against further sell-offs. While nowhere near the levels of inversion that we saw during the height of the early-November panic, short-dated optionality continues to trade several volatility points above the back-end of the term structure. In addition, volatility at all tenors is priced in a tight range between 70% and 75%, some 10 percentage points higher than its levels at the turn of the month.

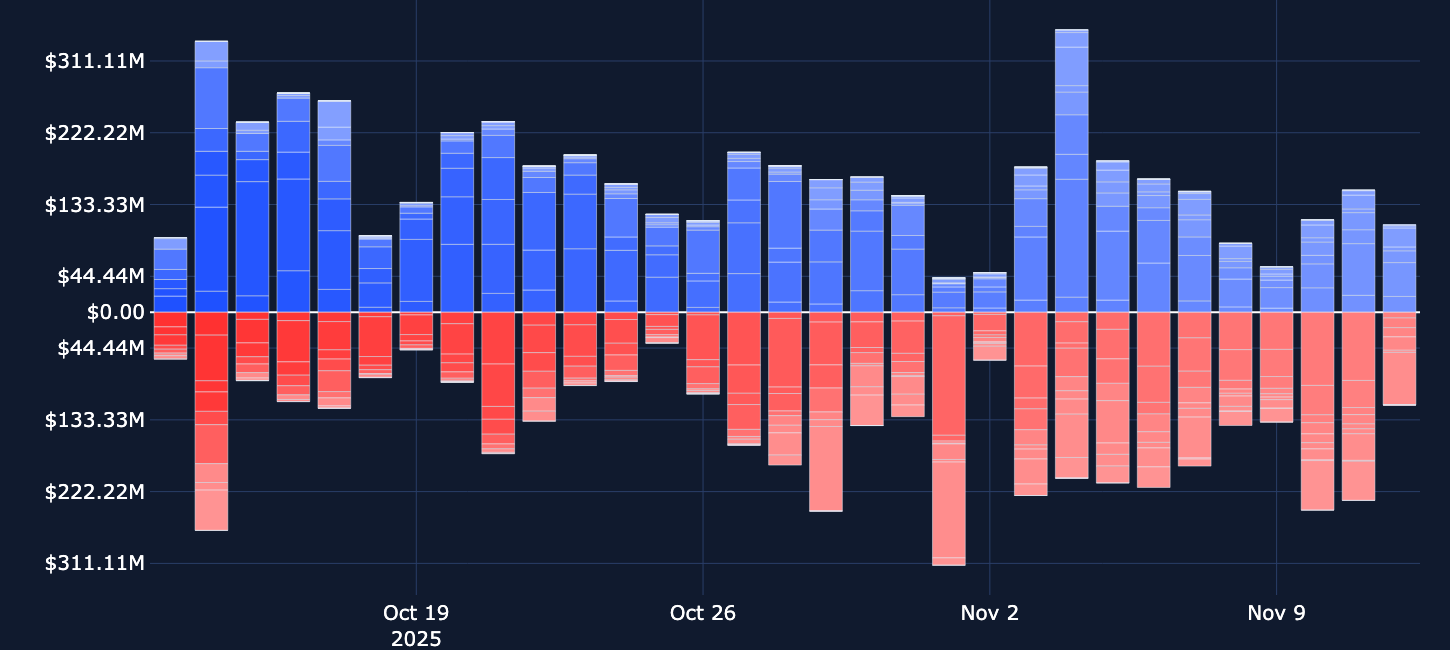

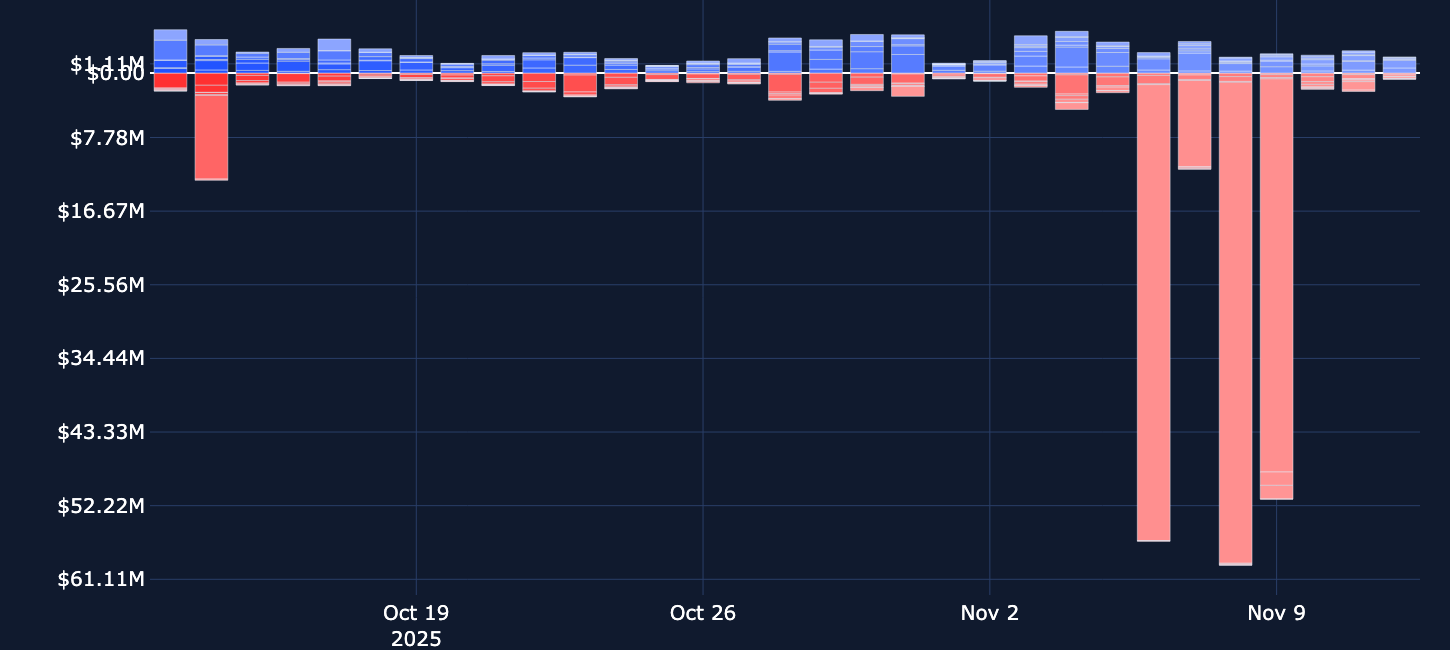

SOL options have recorded several days of trade volumes dominated trading in bearish put options. More than $150M of longer-dated put contracts changed hands between Nov 6 and Nov 9, 2025. However, as this occurred after the large sell-off in SOL spot price at the beginning of November and does not appear to have had a lasting impact on open interest, we cannot conclude there has been a lasting shift towards further bearish positioning.

That’s not to say that sentiment among SOL option traders has recovered from the spot move lower, as volatility expectations remain elevated and the price of optionality remains high. Short-dated optionality is in increased demand, resulting in the distinctive inversion of the term structure of implied volatility that we also see in ETH options markets. While realized volatility has fallen back below the level implied by options expiring in one month, it remains elevated relative to its Summer levels.

Several attempts in spot markets to sustain a rally back into late-October levels have failed. As a result, options markets remain bearish about sustained positive price action in the short term, with a strong skew towards OTM puts in both BTC and ETH that indicates a preference for downside protection. Interestingly, BTC options markets are assigning a stronger bearish skew, assigning a 6%+ implied volatility premium to put options expiring in the next 7 days. In contrast, ETH options at the same tenor assign less than a 3% premium to downside protection, despite pricing-in a higher level of volatility outright. However, while the perpetual swap funding rates of many altcoins show a persistent demand for short exposure, the funding rates in BTC and ETH markets do not show as strong a bearish sentiment as their volatility smiles.

Open interest and trading volume data are sourced “as is” from the Bybit exchange platform API exclusively, and as such do not represent a comprehensive picture of the sum of trading activity across all derivatives markets or exchanges. The data visualized in this report consists of hourly and daily snapshots, recorded over the previous 30 days. Daily (hourly) snapshots of trade volume record the total sum of the notional value of trades recorded in the 24H (1 hour) period, beginning with the snapshot timestamp.

If not explicitly labeled as derived from another exchange, the input instrument prices to all derivatives analytics metrics in this report are sourced from the appropriate endpoints of Bybit’s public exchange platform API. In the event that data is labeled or referred to as representing the market on another exchange source, that data is sourced from the appropriate endpoint of each respective exchange’s public API.

Macroeconomic charts and data are sourced “as is” from the Bloomberg Terminal. Exchange data is sourced “as is” from publicly available exchange APIs. Block Scholes makes no claims about the veracity of public third-party data.

After acquisition of underlying-denominated raw data for open interest and trading volume on the Bybit exchange platform from Bybit’s API endpoint, equivalent dollar-denominated figures are calculated using the concurrent value of Block Scholes’s Spot Index for the relevant underlying asset.

Block Scholes’s Spot Index represents the aggregate Spot mid-price for a given currency across the top five CEXs by volume (with USD-quoted markets). It considers the proportion of total volume in the instrument on the exchange, as well as the deviation of a data point from those on other exchanges.

Futures prices are used for Block Scholes’s futures-implied yields calculation services in order to derive the constant-tenor annualized yields displayed in the Futures section of this report.

Options prices are used for Block Scholes’s implied volatility calculation services in order to calibrate volatility surfaces, from which all derivatives volatility analytics displayed in the BTC Options and ETH Options sections of this report are calculated. Volatility smiles are constructed by calibrating to mid-market prices observed in Bybit options markets. As part of the calibration process, prices go through rigorous filtration and cleaning steps, which ensures that the resulting volatility surface is arbitrage-free and has exceptional fit to the market observables.

.jpg)

.jpg)