Thahbib Rahman

Research Analyst

Bitget has unveiled its Universal Exchange (UEX) model, the platform’s vision of a unified trading hub that brings together the experience of centralized exchanges (CEXs), decentralized exchanges (DEXs), and traditional finance (TradFi). For users, that means the ability to trade a wide variety of asset types in one place, adding tokenized stocks of ETFs, gold, and equities to Bitgets’s crypto offering.Bitget will initially onboard tokenized stocks offered by Xstocks and Ondo Finance’s Global Markets. This will allow traders to trade a wide range of real-world assets, from equity tickers such as Tesla (TSLA) and Nvidia (NVDA), as well as ETF funds that track equity indices, for example SPYon or QQQon (which track the S&P 500 and Nasdaq-100, respectively). Tokenized stocks maintain their value because each digital token is backed one-to-one by the real asset, safeguarded by a regulated brokerage entity. This structure mirrors how regulated stablecoins such as USDC maintain value by holding equivalent reserves, where 1 USDC on-chain is backed by the equivalent of $1 off-chain held by Circle.

Bitget has unveiled its Universal Exchange (UEX) model, the platform’s vision of a unified trading hub that brings together the experience of centralized exchanges (CEXs), decentralized exchanges (DEXs), and traditional finance (TradFi). For users, that means the ability to trade a wide variety of asset types in one place, adding tokenized stocks of ETFs, gold, and equities to Bitgets’s crypto offering.

Bitget will initially onboard tokenized stocks offered by Xstocks and Ondo Finance’s Global Markets. This will allow traders to trade a wide range of real-world assets, from equity tickers such as Tesla (TSLA) and Nvidia (NVDA), as well as ETF funds that track equity indices, for example SPYon or QQQon (which track the S&P 500 and Nasdaq-100, respectively). Tokenized stocks maintain their value because each digital token is backed one-to-one by the real asset, safeguarded by a regulated brokerage entity. This structure mirrors how regulated stablecoins such as USDC maintain value by holding equivalent reserves, where 1 USDC on-chain is backed by the equivalent of $1 off-chain held by Circle.

Tokenized assets are real-world assets, such as equities (Tesla, Apple, Nvidia, etc.), bonds, commodities, currencies, or even physical items such as real estate, represented as digital tokens on a blockchain. Each token reflects ownership of, or exposure to, the underlying asset -allowing it to be traded within crypto ecosystems. The blockchain enables 24/7 markets and faster settlement of these assets, removing the limitations of “opening times” that exist in traditional finance (TradFi).

Ondo’s tokenized stocks are all issued by the Ondo Global Markets platform and are designed to give their holders the same economic exposure as if they owned the actual underlying asset(s) including any dividends. The difference is that, while the tokenized stock can be redeemed “for cash or stablecoins for the then-value of the underlying assets”, holders do not receive the “shareholder voting rights, statutory information rights or other shareholder rights from the issuer of those securities” as they would if they held the off-chain asset itself.

For users, the introduction of tokenized assets on Bitget allows them to buy these shares through digital tokens such as USDC and hold their positions in Bitget Wallet, a single place for easier management. For example, integration with Ondo means traders can choose from over 100 tokenized stocks. Similar to other platforms, Bitget has also now integrated with xStocks, allowing users to trade both equities provided by Ondo, as well as tokenized stocks provided by xStocks. Relative to other exchanges however, Bitget does not require users to pay extra, or have a ‘Pro’ account for example, in order to access its array of tokenized stocks. Additionally, it is one of the first exchanges to offer tokenized stocks to both users in the US and outside of the US.

Our report highlights that tokenized real-world assets are in a growth stage, from stablecoins to a new wave of tokenized stocks now making their way on-chain. We compare the market moves of tokenized assets with their off-chain equivalents during regular market hours, with bigger gaps mainly showing up overnight or on weekends when traditional markets are closed. We also look at how Bitget’s Universal Exchange (UEX) and Bitget Wallet bring all these assets together on one platform, creating a single environment for holding and trading “everything you own.”

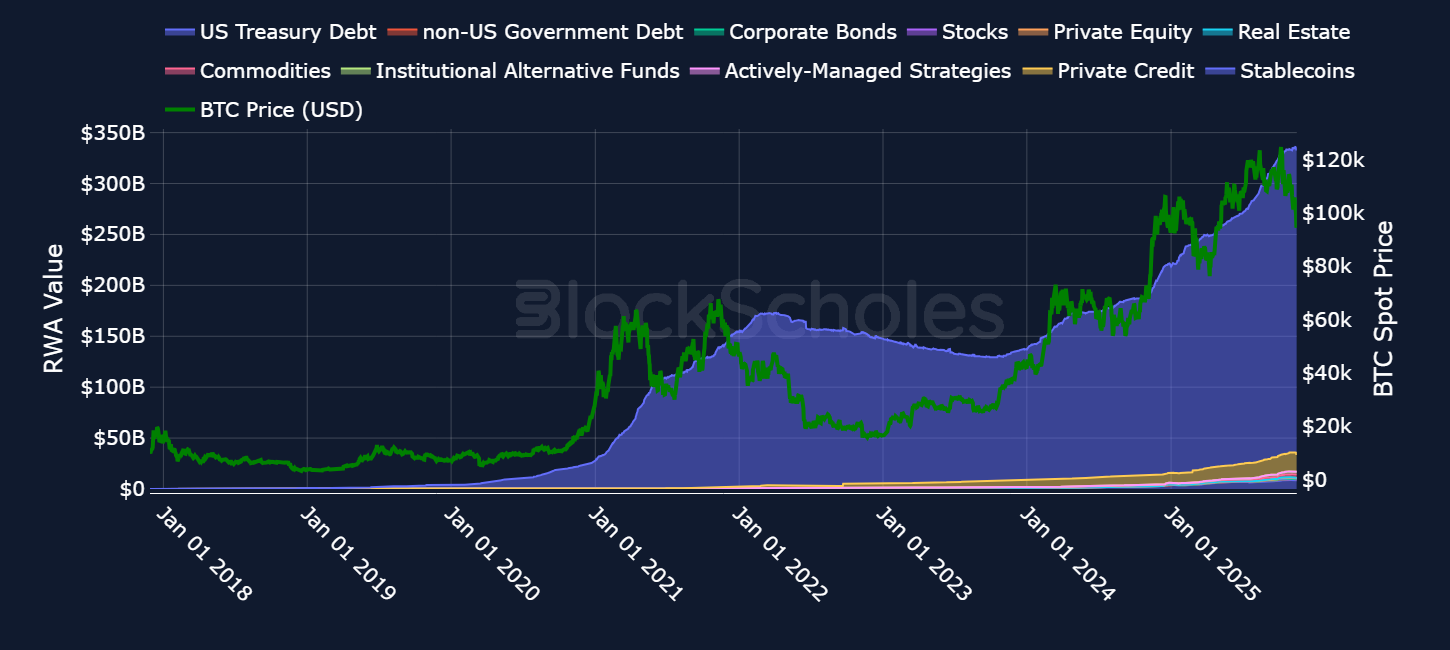

Onchain tokenization of real-world assets (RWAs) has been growing exponentially, with all major categories of RWA constituents expanding. The most common and widely adopted form of RWA is stablecoins, assets many people use without consciously categorizing them as tokenized instruments, even though fundamentally, they are: a U.S. dollar (or any other fiat currency) represented on-chain as a token backed by an off-chain underlying. Bitget is entering this market at a moment of rising supply, allowing users to gain access via UEX.

Including stablecoins, the broader RWA sector has seen a substantial rise in market cap that began around the 2020-21 Bitcoin bullrun and has continued to grow broadly in line with rising demand for their most popular use case: stablecoins facilitating the trading of digital assets.

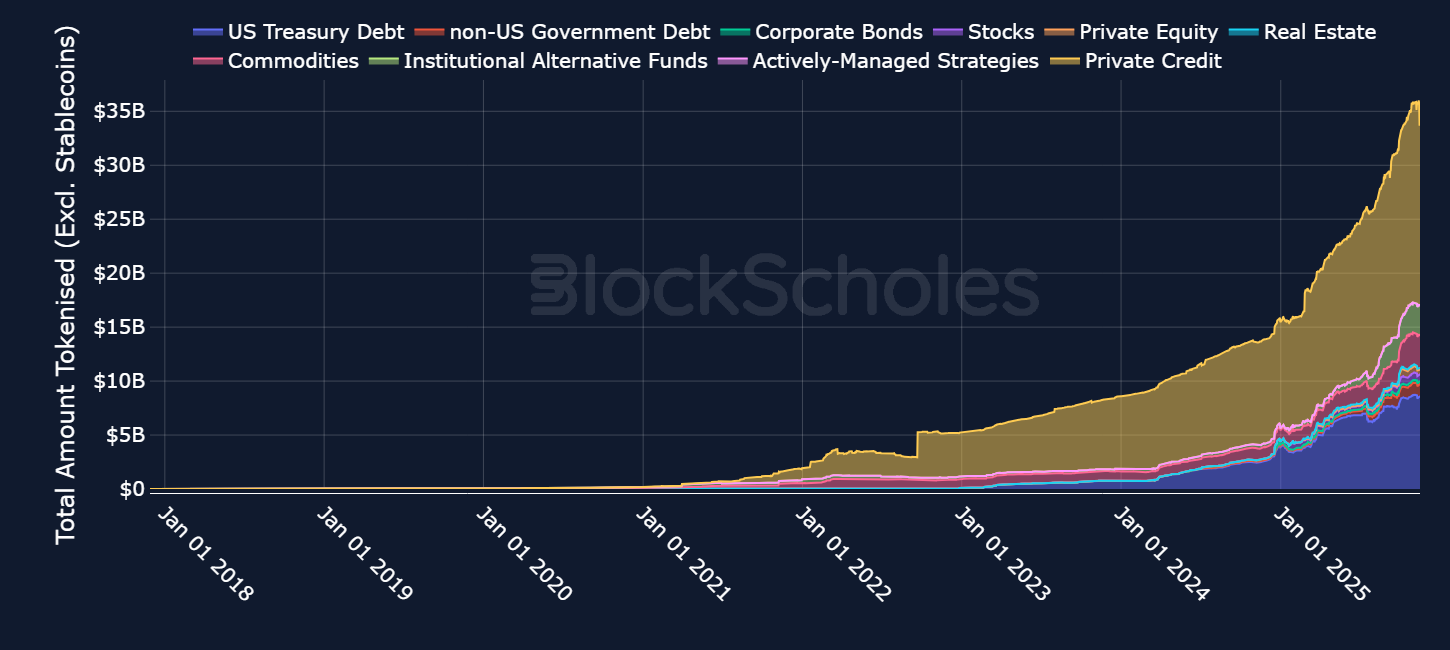

Away from stablecoins, the 2021-2022 period also marked the emergence of new asset classes being tokenized on-chain. This trend is now growing at its fastest rate since the concept began. As the data shows, a large majority of non-stablecoin tokenized assets falls under institutional offerings such as private-market instruments and U.S. Treasury debt. This momentum is driven by institutional demand — which has been bolstered by the current U.S. administration’s championing of digital assets. As such, firms are increasingly recognising the advantages of on-chain custody, particularly immediate settlement and rapid transferability, which in turn significantly reduces the need for traditional back-office processes.

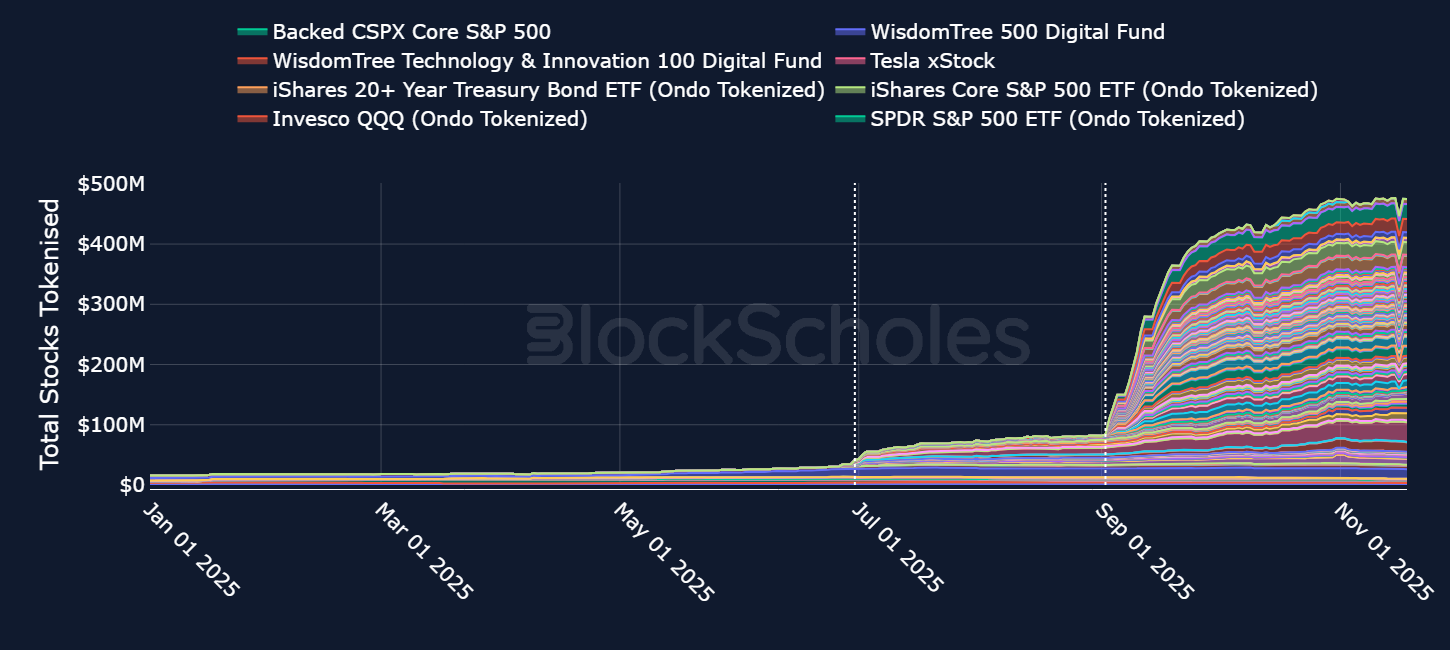

The growth of tokenized stocks is far more recent, with meaningful expansion only beginning to appear in Q3 2025. Tokenized equities at this stage are primarily aimed at retail users, with major centralized exchanges such as Bitget integrating access to these traditional finance instruments into their platforms. The increases observed in market metrics are closely linked to the timing and availability of new products.

The initial major driver of on-chain equities was the launch of xStocks by Backed Finance on Jun 30, 2025, which introduced more than sixty tokenized U.S. equities to the on-chain ecosystem. A further acceleration occurred on Sep 2, 2025, when xStocks expanded to the Ethereum mainnet. Prior to its Ethereum deployment, xStocks was already live on Solana, BNB Chain, and Tron. This broader growth alongside cross chain availability indicates that demand exists in the market, but easier access is needed to capture it.

Current trading volumes for tokenized stocks are largely concentrated between xStocks and Ondo Finance, the two providers that Bitget has integrated.

We’re seeing exponential growth in tokenized assets on-chain and a recent trend towards tokenized equities. But how well do these assets reflect their offchain counterparts, which already trade on centralised exchanges?

SPYon is Ondo Finance’s tokenized version of the SPDR S&P 500 ETF, an ETF designed to track the price of the S&P 500 Index — an index of the largest 500 publicly traded companies in the US. Given that SPYon and SPY are one of the most liquid and traded assets both on-chain and off-chain, we can take SPYon and its relationship to SPY as a proxy for understanding how well tokenized assets reflect the offchain price of the asset they are designed to track.

In Figure 4 above, we plot the hourly price of SPYon alongside the hourly price of SPY, which trades in US market hours only.

While the two look to track each other quite closely, given the fact that SPY trades only in US market hours — 09:30-16:00 ET (or 14:30-21:00 UTC), Monday-Friday, compared to the 24-7 nature of SPYon, a clearer visualization of how well the two track one another is by looking at their intraday spread. We measure the spread as how far the tokenized asset (SPYon) trades above or below the SPY ETF, expressed as a percentage of the SPY ETF price. In other words, when the spread is negative, SPYon is cheaper than the off-chain SPY price and when the spread is positive, say 0.5%, it means SPYon is trading 0.5% above the real SPY ETF price.

Excluding an early September spike, the spread between SPYon and SPY has generally been between -0.2% and +0.2%, indicating that the two assets do not track one another in an entirely perfect manner.

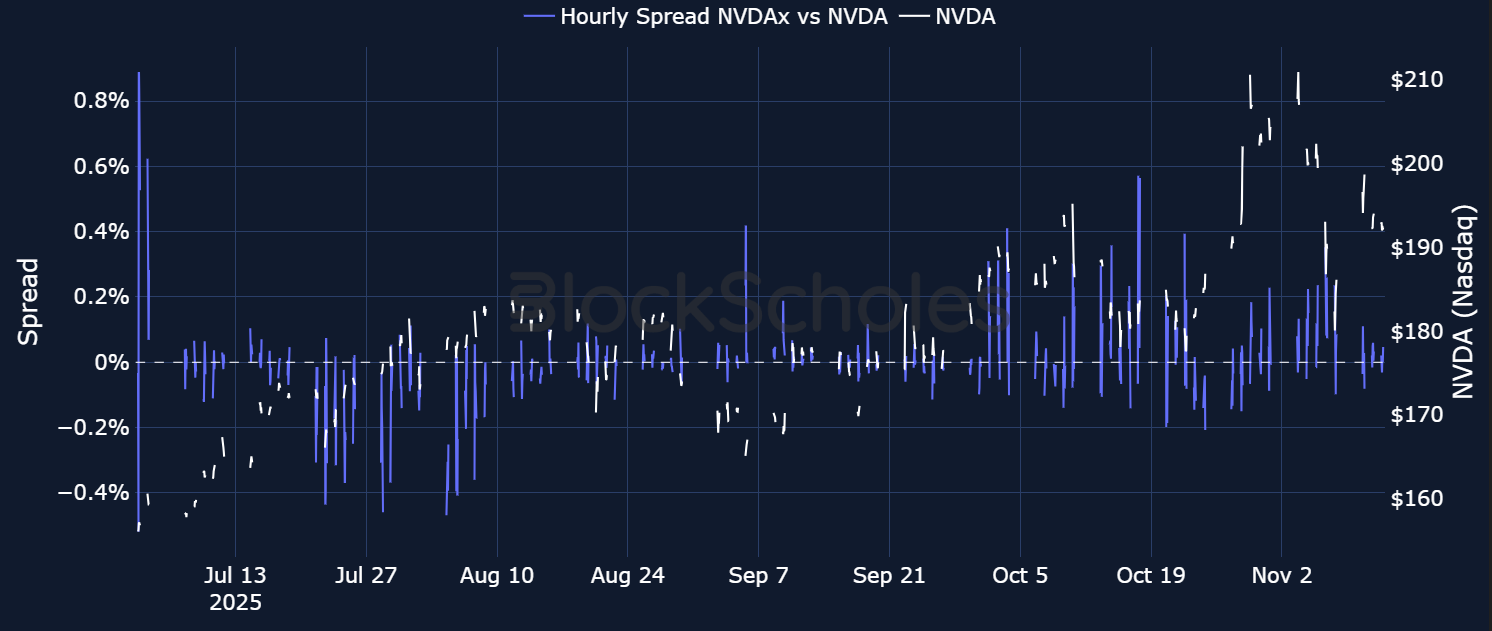

We can do a similar analysis on NVDAx and NVDA. The former is a tokenized asset issued by Backed, designed to track the latter, the stock of Nvidia — the world’s largest publicly traded company. Similar to Ondo, Backed guarantees that its “tokens are 1 to 1 backed by underlying securities”. Interestingly, the spreads appear to be wider between NVDAx and NVDA than they are for SPYon and SPY. Still, excluding a temporary deviation at the launch of NVDAx, the spreads have never exceeded more than a full percentage point in either direction — suggesting a relatively tight relationship between the on-chain and off-chain asset intraday.

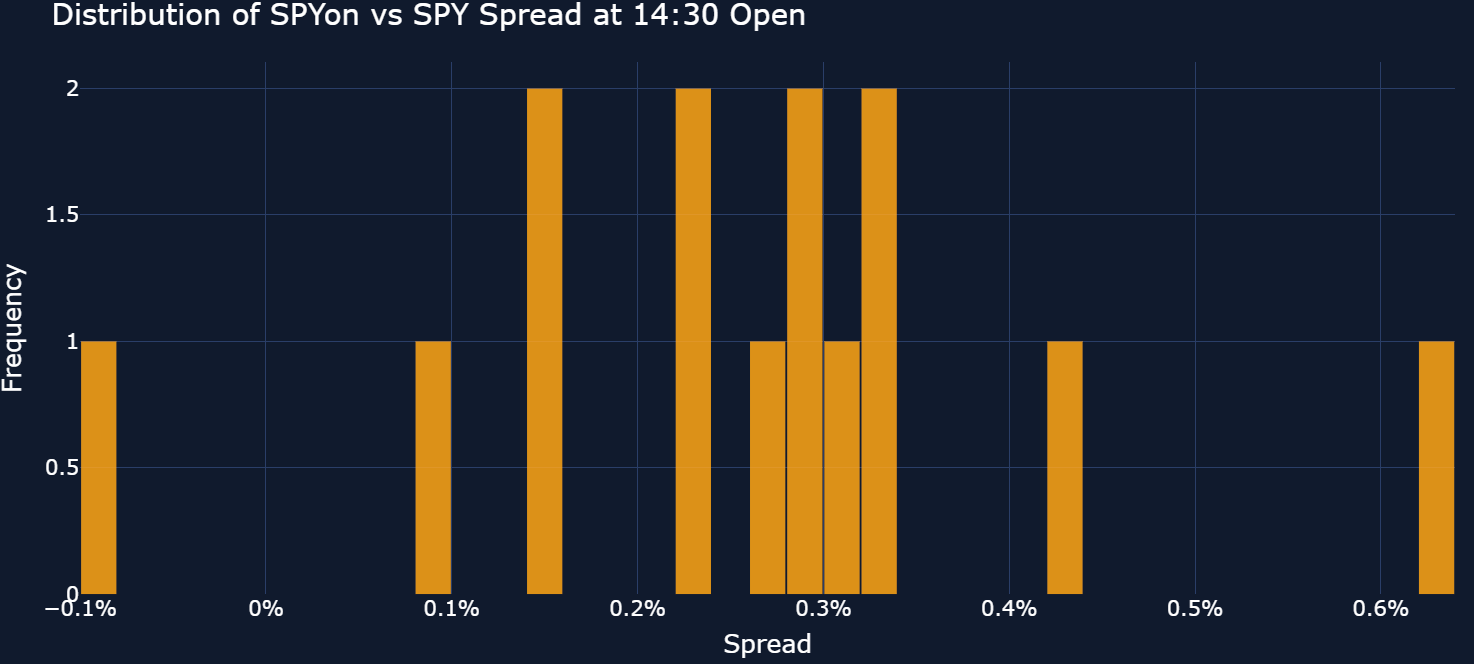

We’ve looked at how the spreads compare during the regular tradeable hours of the traditional equity tickers, but how do the spreads compare when the traditional US equity market opens? By isolating the opening price at the 14:30 UTC timestamp for both SPYon and SPY, we can compare how much the tokenized SPYon deviates from the off-chain New York Stock Exchange's (NYSE) Arca exchange’s SPY.

As seen below, between Oct 21, 2025 and Nov 18, 2025, the price of SPYon tends to be slightly higher than the price of SPY during its open, but that spread for the most part is clustered between 0.2% and 0.3%. Only once over the one month period did SPYon trade at a discounted price when the SPY market opened.

If the spreads are relatively small during market trading hours and when the US Trad-Fi market opens, how does the spread between the two assets look out of hours? To answer this, we extend the above analysis and compare the hourly SPYon price to the last recorded SPY close. Since SPY trades in US market hours, when the market is closed, we assume that the SPY price remains fixed at the last recorded close. This allows us to compute the spread outside of US market hours and measure how much the tokenized asset drifts during off-hours when the ETF is no longer trading.

Here it becomes clearer that the out-of-hours spreads are indeed much wider than both intraday and relative to the official market open of SPY. Take Sep 6, 2025 at 15:00: that timestamp corresponds to a weekend when SPY was not trading. The last recorded SPY price was on Friday, registering at $647.17. By 15:00 on the following day, SPYon had surged to as much as $671.95, resulting in an out-of-hours spread of as much as 3.83%.

To understand why these spreads are larger during off-hours, a slightly more detailed understanding of the minting and redemption process behind tokenized assets is required. Similar to stablecoins, the minting and redemption process is how tokenized stocks maintain their pegs to the off-chain asset. We will use Backed’s NVDAx as an example. NVDAx can be traded freely on exchanges such as Bitget or other decentralized exchanges (DEX’s). However, in order to mint or redeem NVDAx tokens, users must go through the Backed platform who will only execute your orders when the markets for the underlying asset are open.

Trading activity in tokenized US stock products is distributed across the 24-hour cycle: the core US session remains the most concentrated period, but the highest-volume window outside regular US hours occurs during the Asian afternoon, aligned with the US pre-market, with additional activity continuing after the US close.

Therefore, during the tradable Trad-Fi market hours, arbitrage arguments can explain why the two assets track one another with a relatively small spread. If NVDAx trades at a discount to the off-chain NVDA price (the price that redemption takes place at), traders can buy NVDAx tokens at the market price on an exchange or DEX, then redeem the NVDAx tokens on the Backed platform at the (higher) off-chain price. Therefore, when price deviates too far, during market hours, traders capturing the arbitrage will bring the prices back into line. However, in out-of-market-hours, since the off-chain NVDA stock does not trade at all, the on-chain market does not have a reference for the ‘true’ price of Nvidia stock. The lack of a reference price means traders or market makers hold the risk for quoting prices during this time period — a risk that holds until the off-chain market reopens again and minting and redeeming can take place at the off-chain price. These factors therefore can often result in wider price deviations and spreads when traders buy and sell tokenized assets in out-of-traditional-hours trading.

In the current market structure, digital assets and traditional securities are usually held and traded on separate platforms — crypto exchanges for spot and derivatives and brokerage accounts for stocks and ETFs. Tokenization is the mechanism that allows Bitget to bring these markets together, enabling the creation of a Universal Exchange (UEX) where both crypto and tokenized traditional assets can be accessed through a single integrated venue.

Bitget’s UEX lets users trade both crypto and tokenized RWAs from a single account, while Bitget Wallet provides a unified portfolio view. This setup allows tokenized stocks to be held alongside crypto assets and stablecoins in the same wallet, removing the need for a separate brokerage account. Tokenised RWAs still have regulatory and liquidity considerations, positioning that Bitget maintains risk management and compliance frameworks.

Beyond spot holdings, Bitget has introduced first-ever RWA contracts and index perpetuals that reference baskets of tokenized stocks. Bitget’s user base remains at around 120M users, with over 1M users having engaged with tokenized stock products, and that more than 95% of tokenised stock traders also hold crypto assets. On-chain RWA platforms now account for around $18.3B in tokenized assets, backed by approximately $391.6B of represented real-world assets and held by more than 550,00 unique RWA asset holders. This shows that RWA exposures are now used by a meaningful share of crypto market participants rather than a narrow niche. These instruments mirror the mechanics of crypto perpetuals and support leverage of up to 10x in isolated margin mode, allowing users to take both long and short positions on RWA indices.

Tokenized RWAs are in a growth phase across multiple segments, from established stablecoins to newer institutional products and tokenized equities. The broader RWA market has expanded alongside rising stablecoin demand since the 2020–21 period, with non-stablecoin RWAs, such as private-market instruments and U.S. Treasuries, increasingly focused on institutional offerings. Tokenized stocks are a more recent development, with meaningful growth only beginning in Q3 2025 and largely driven by products such as xStocks and Ondo.

At the same time, pricing data shows that tokenized assets generally track their off-chain counterparts closely during traditional market hours, with intraday spreads typically contained within tight bands. Wider deviations appear primarily during out-of-hours trading, reflecting limits on minting and redemption when underlying markets are closed and the absence of a live reference price. Overall, the combination of accelerating issuance, new product availability, and improving trading infrastructure suggests that the tokenized RWA market is still in an early but increasingly scalable phase, with growth coming from both institutional and retail channels.

Bitget UEX and Bitget Wallet are positioned on top of this trend by turning these separate developments into a unified user experience. By integrating tokenized stocks and ETFs from Ondo and xStocks, and allowing users to fund positions in stablecoins such as USDC and hold them in Bitget Wallet alongside crypto, Bitget creates a single environment for managing tokenized RWAs and digital assets. UEX then provides the trading layer, offering 24/7 access, extended-hours trading in tokenized S&P and Treasury-linked products, and RWA index perpetuals that follow familiar crypto-perpetual mechanics. Together, Bitget UEX and Bitget Wallet operationalise the idea of “everything you own” in one place.

.jpg)

.jpg)