Thahbib Rahman

Research Analyst

Sideways trading in the final stretch of 2025 was upended by a sharp and aggressive move higher this week in BTC spot price to a two-month high, nearly touching $98K. That move dragged the rest of the spot market up with it, and has had a strong effect on derivatives markets. Funding rates for select altcoins have shot higher, while open interest in perpetual futures contracts has increased, signalling new longs entering the market in hope of capturing any further upside moves in spot price. Volatility smiles have priced out their bearish put premium and now trade close to neutral for BTC and ETH. Additionally, spot ETFs for both majors show positive inflows year-to-date. ETH has also benefitted from idiosyncratic, on-chain tailwinds: demand for staking continues to soar, with 30% of the total ether circulating supply currently being staked. Despite the breakout from a month-long period of consolidation and various macro risks in the form of US-Iran tensions, December’s NFP release, December’s CPI report, a grand jury subpoena issued to the Federal Reserve, volatility has continued to trend lower.

Sideways trading in the final stretch of 2025 was upended by a sharp and aggressive move higher this week in BTC spot price to a two-month high, nearly touching $98K. That move dragged the rest of the spot market up with it, and has had a strong effect on derivatives markets.

Funding rates for select altcoins have shot higher, while open interest in perpetual futures contracts has increased, signalling new longs entering the market in hope of capturing any further upside moves in spot price. Volatility smiles have priced out their bearish put premium and now trade close to neutral for BTC and ETH.

Additionally, spot ETFs for both majors show positive inflows year-to-date. ETH has also benefitted from idiosyncratic, on-chain tailwinds: demand for staking continues to soar, with 30% of the total ether circulating supply currently being staked. Despite the breakout from a month-long period of consolidation and various macro risks in the form of US-Iran tensions, December’s NFP release, December’s CPI report, a grand jury subpoena issued to the Federal Reserve, volatility has continued to trend lower.

Perpetuals: Open interest has ticked up coinciding with the breakout in spot price, with funding rates for altcoins showing signs of optimism.

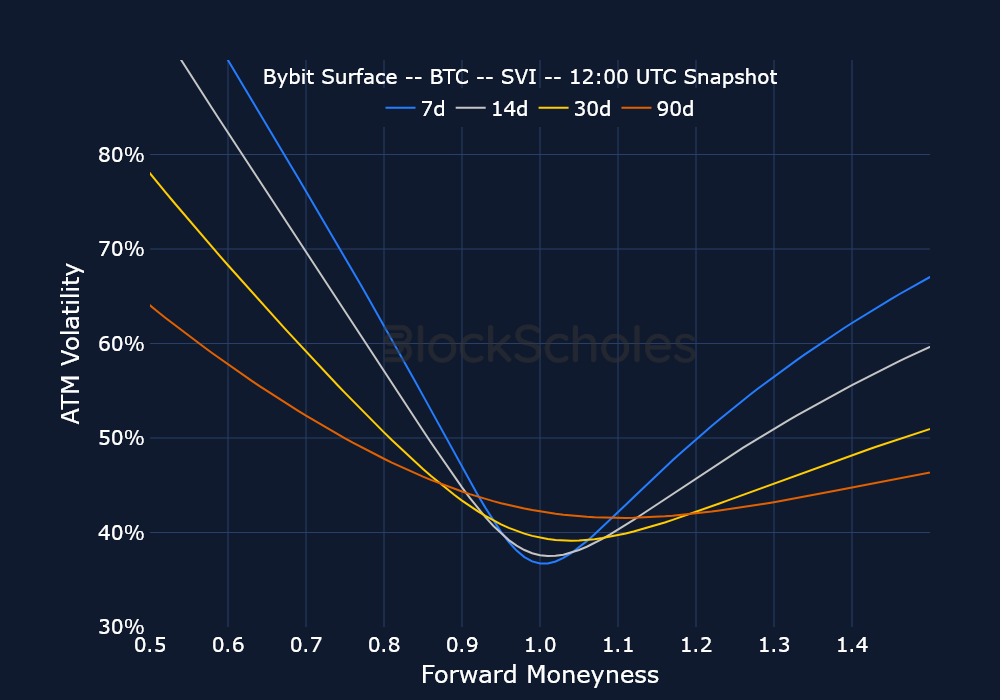

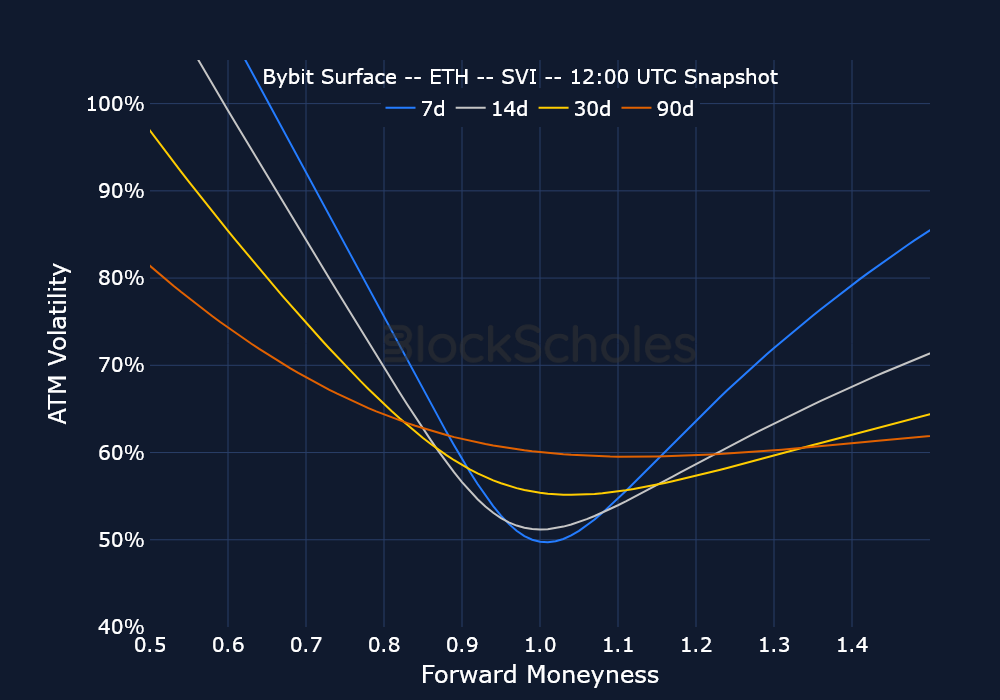

Options: BTC and ETH volatility smiles are now pricing in a neutral skew for short-dated optionality – a shift from the previously bearish put-skew. We’ve seen that before already this year however, when the move to $94K in early January saw a neutral skew that eventually reverted back to puts as BTC failed to hold that price level.

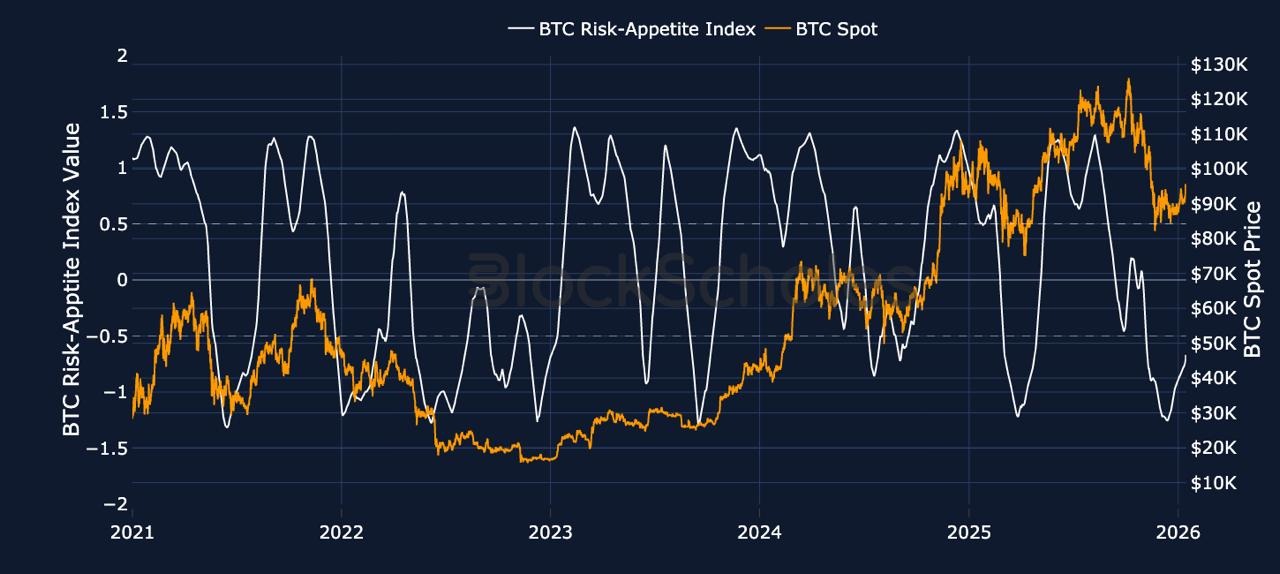

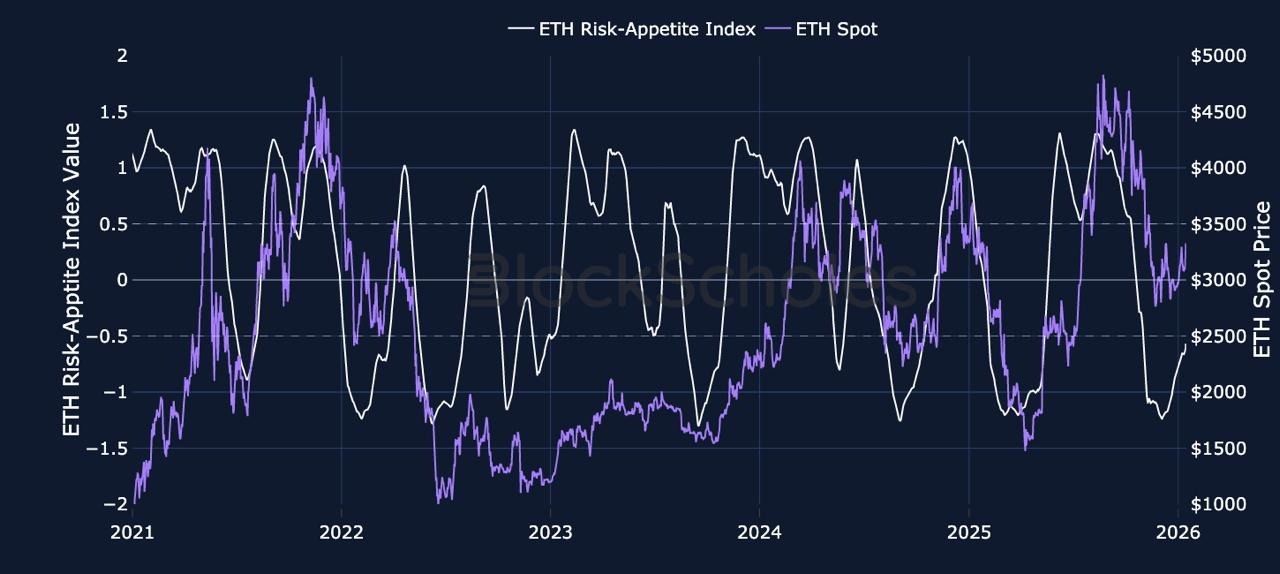

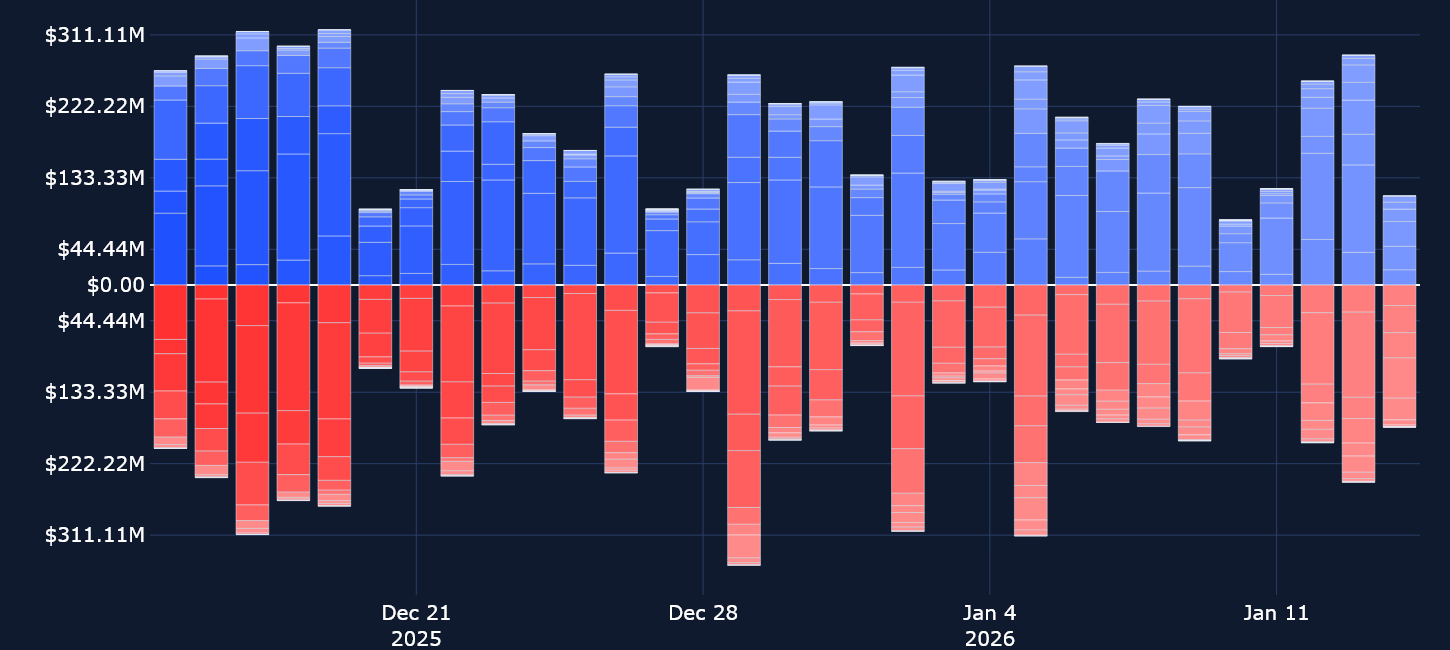

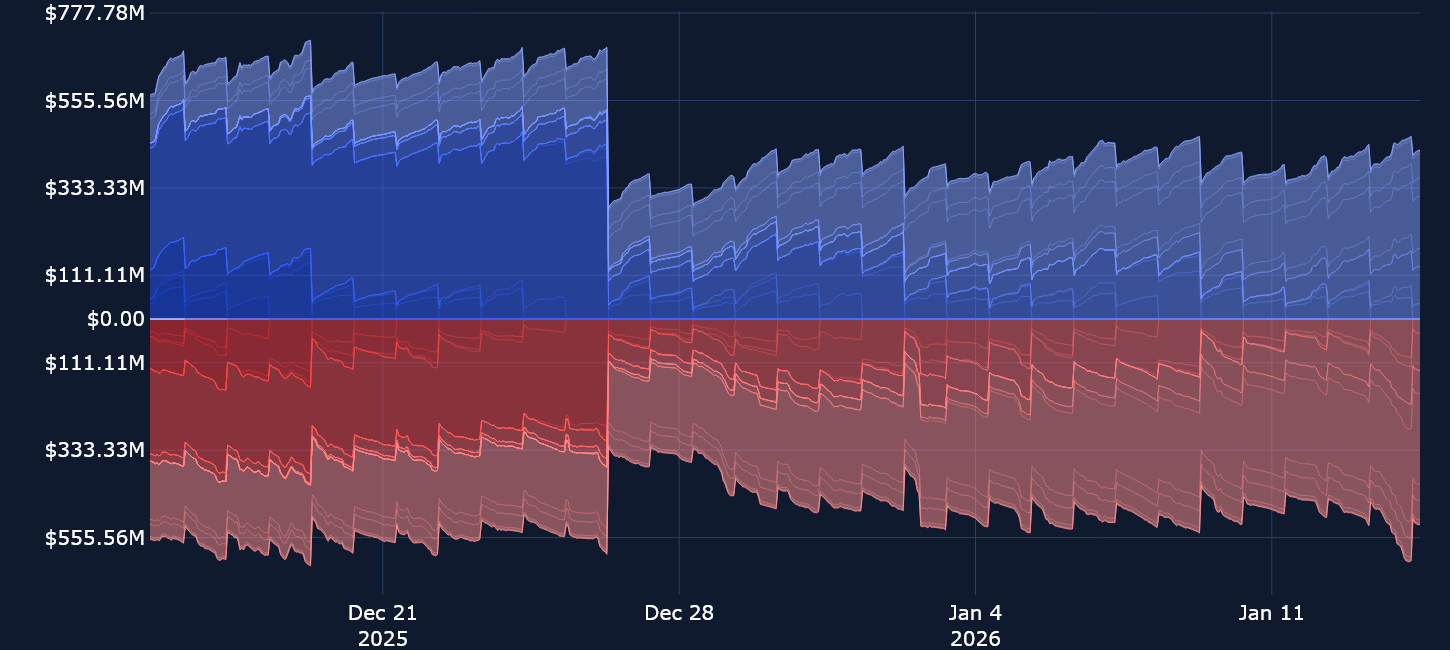

Block Scholes’ Risk Appetite Index measures the level of euphoria (above 1) or panic (below -1) in the spot market. Momentum in this index shows a strong relationship to spot returns.

Dash is an open-source cryptocurrency that runs on its own Layer-1 blockchain. It was launched in 2014 under the name XCoin, but was later renamed to Darkcoin, and rebranded as Dash (“digital cash”) in March 2015.

The protocol is Bitcoin-derived in its UTXO design and general architecture, but it diverges meaningfully in how it targets payments performance and user experience: Dash uses Proof-of-Work (PoW) secured mining with the X11 hashing algorithm and pairs that with a second, incentivised node layer (“masternodes”) that provides higher-level services and governance.

Dash positions itself explicitly as “digital cash” built for everyday spending, with the message on its website that businesses are encouraged to add Dash payments so customers can pay by scanning a QR code (or via gift-card rails), with the network marketed around near-instant settlement. The typical performance is usually one second per transaction at a cost of less than one cent. On their website, a “safety first” posture in custody terms is emphasised, stating that Dash secures the wallet experience while users retain control of their private keys and recovery phrase.

What differentiates Dash technically is its two-tier architecture and the way it tries to deliver speed and finality on top of a Proof-of-Work base. Beyond standard miners, Dash’s network relies on an incentivised set of collateralised nodes called masternodes – a standard masternode requires 1,000 DASH locked as collateral, aligning operator incentives while enabling additional network services. This masternode layer underpins "InstantSend", which uses quorum-based signing to typically confirm within seconds, and it also supports "ChainLocks", a mechanism designed to reduce the practical risk of chain reorganisations by having masternode quorums attest to blocks.

For privacy, Dash offers an optional mixing feature commonly described as CoinJoin (historically branded as “PrivateSend”), which aims to make transaction link analysis more difficult. It is best characterised as a privacy enhancement tool rather than a guarantee of absolute anonymity.

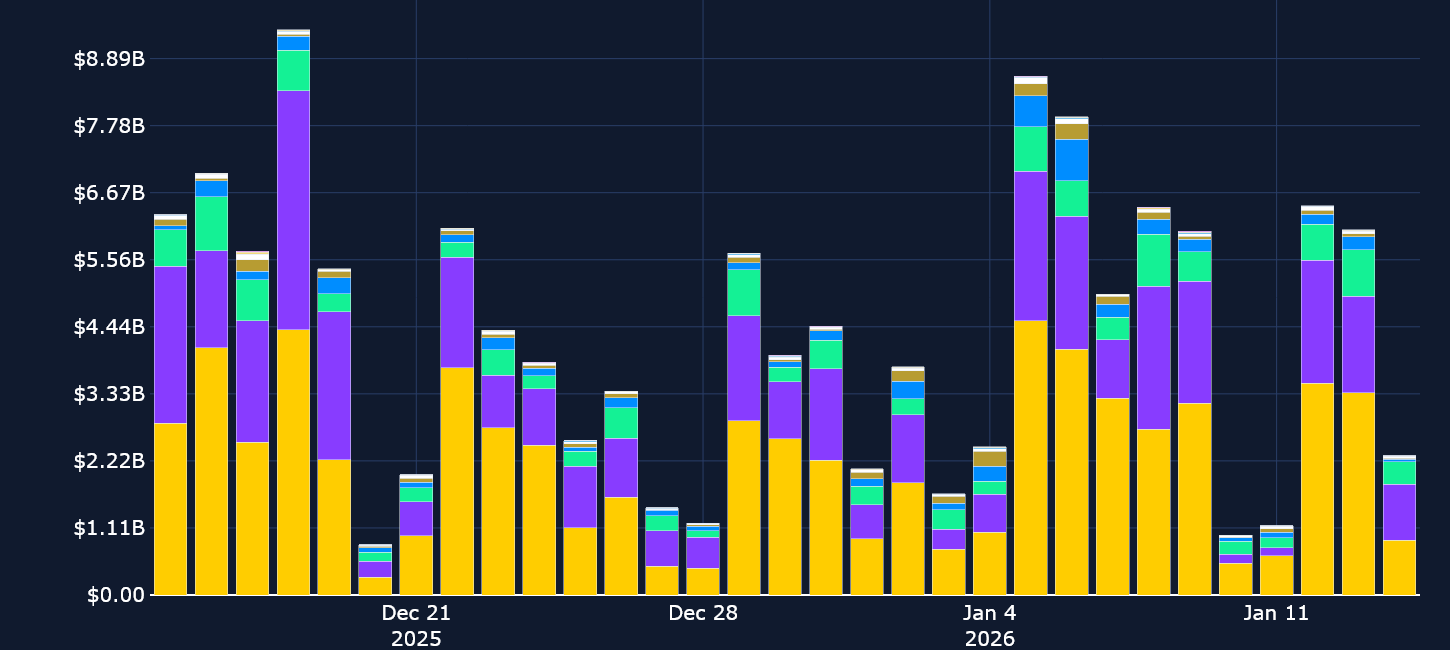

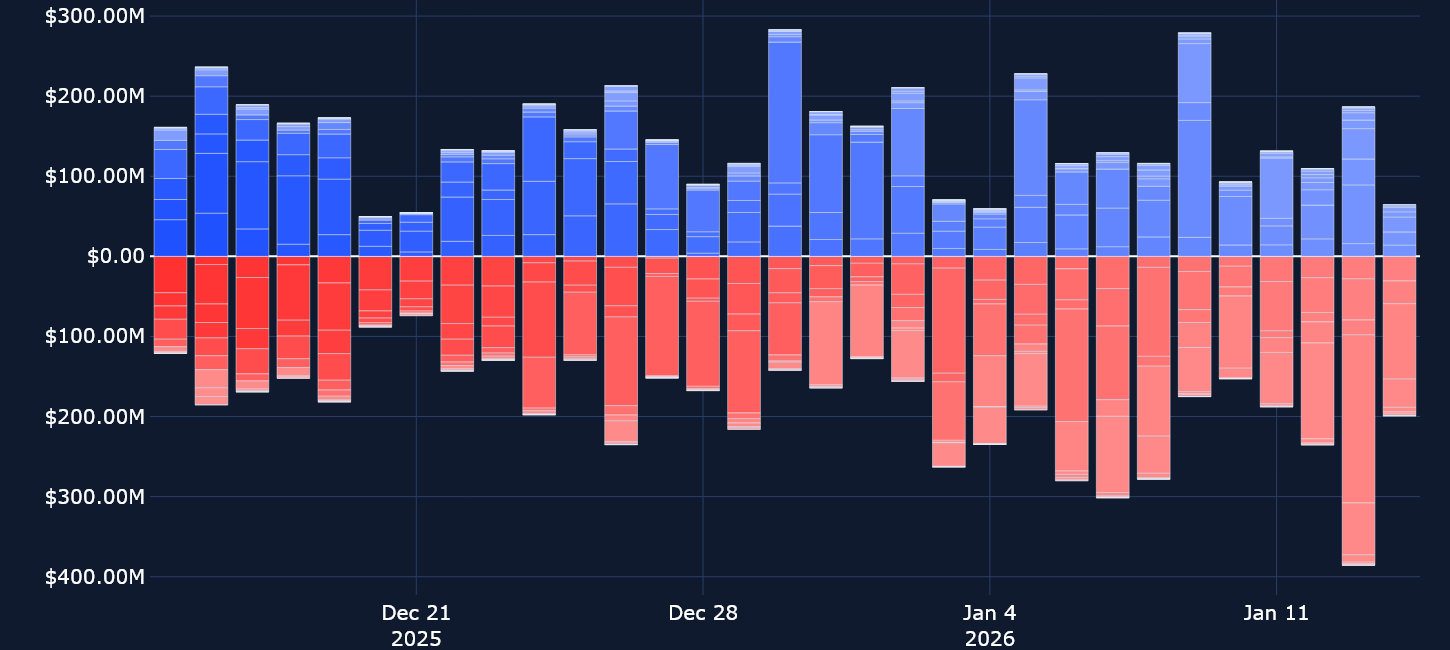

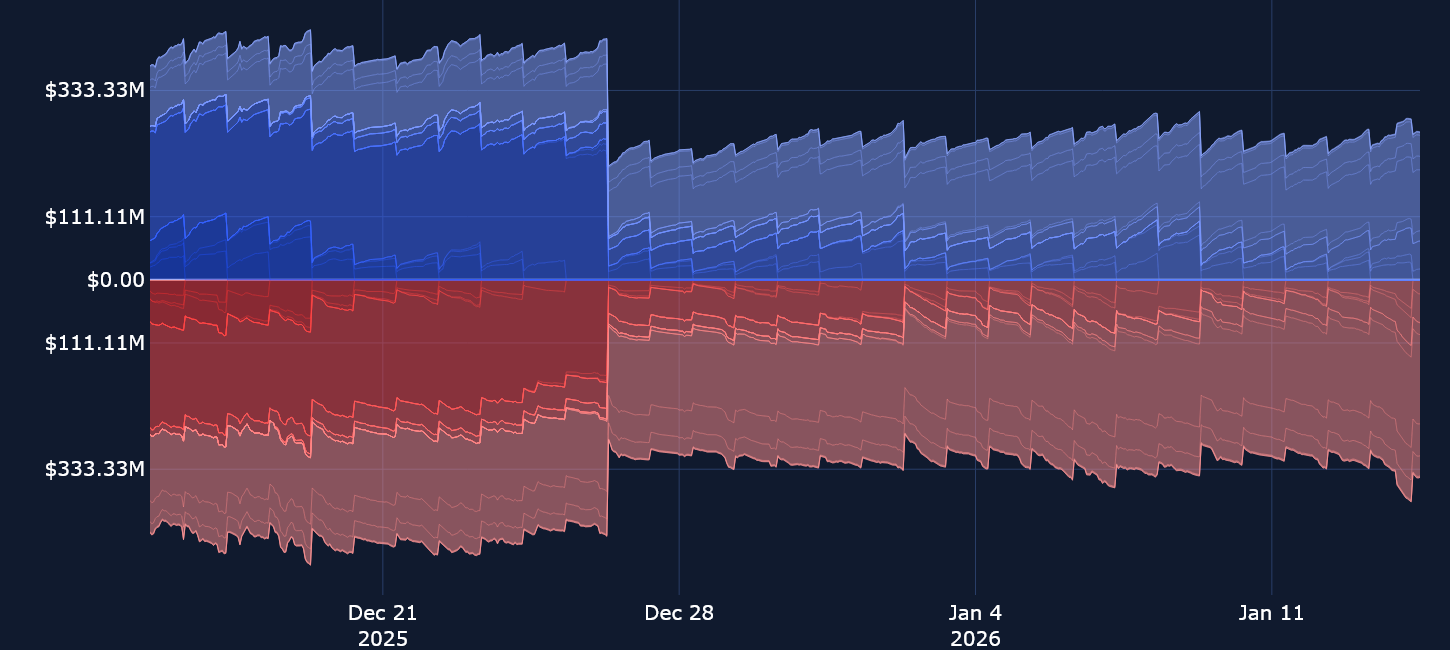

After more than a month of rangebound trading between $85K and $95K, BTC has now broken out into the upper-$90k region,lifting the rest of the altcoin market up in tandem. The impact on perpetual swap markets is quite apparent – open interest shot up past $8B across the 9 major tokens we are tracking, returning back to levels we saw at the start of the year, when BTC rallied to $94K.

Coupled alongside a vertical move higher in our Risk-Appetite Index, it suggests that the upward trend in spot price momentum is causing some traders to open perp positions in order to capture any further upside moves in spot prices. ETH and other altcoins have also benefited from inflows into their respective Spot ETFs. Ethereum Spot ETFs purchased $130M of Ether on Jan 13, 2025, while XRP and SOL have seen multiple consecutive days of inflows, further supporting the turn in spot price momentum.

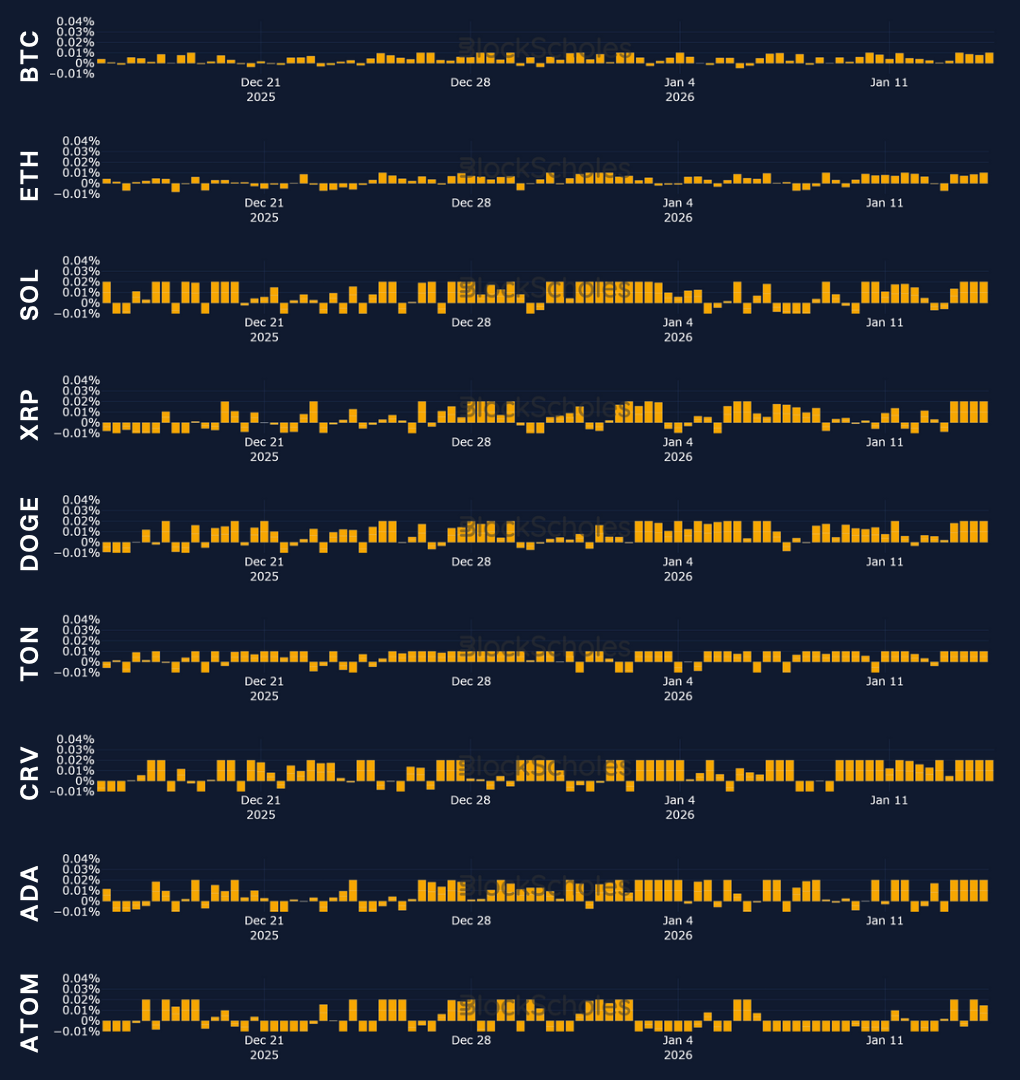

Perpetual swap funding rates also show tentative signs of a potential change in market sentiment.

For BTC and ETH we see modestly positive funding rates, however for altcoins further up the risk curve we see stronger signs of traders showing conviction that they expect the rally to continue. SOL, XRP and (still the premier memecoin of the crypto market) DOGE have all seen funding rates around 0.02% on an eight-hourly basis. Taken alongside the increase in open interest, that suggests traders are entering into long positions in perps, and are willing to pay a premium for leveraged upside exposure.

SOL in particular has benefited from another of token/chain specific tailwinds: Solana mobile, which is linked to the Solana network via the Solana Mobile Stack announced it will airdrop 20% of its native SRK token on Jan 21, 2025, while DEX volumes on Solana recently surged higher, driven by increased trading activity on Pump.fun and Meteora.

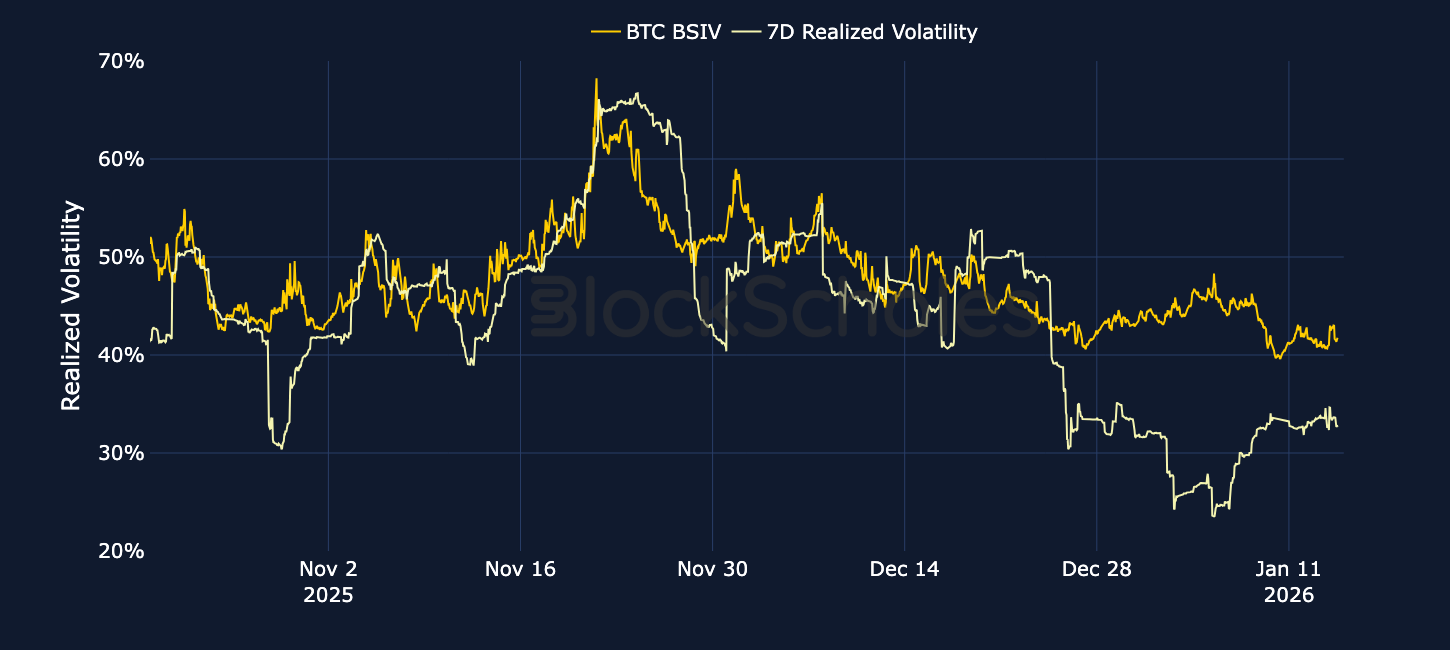

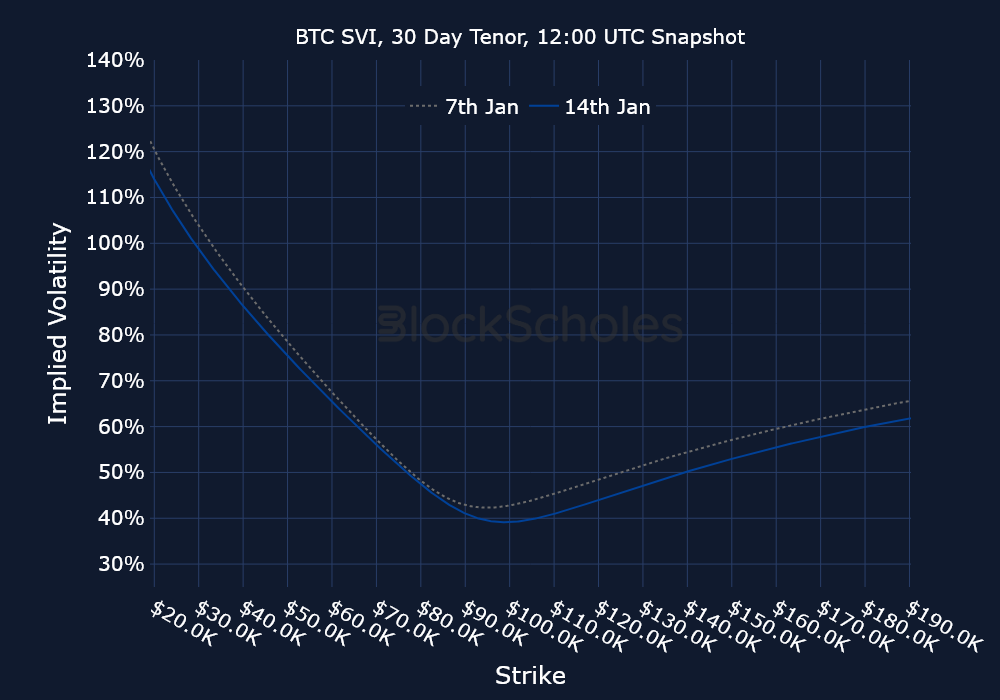

The past month of BTC spot price could be described as ‘chop-solidation’ – a continued sideways chop between $85K and $95K, with few breakouts (neither up nor down) from those bounds. It is unsurprising, then, that options markets expectations for volatility have continued their downward trend.

What’s more surprising is that the eventual breakout from that range to a two-month high of $96K has had very little impact on outright ATM implied volatility levels. Realized volatility ticked up towards the end of last week before now moving sideways at 38%, while short-tenor IV has only been lower around 22% of the time since January 2024.

BTC’s spot price rally has been supported by Spot ETF inflows, however. Year-to-date, BTC Spot ETFs have seen net inflows of $660M, with $760M in net inflows on Jan 13, 2026 - the biggest one-day haul since the 10/10 (Oct 10th) historic liquidation event.

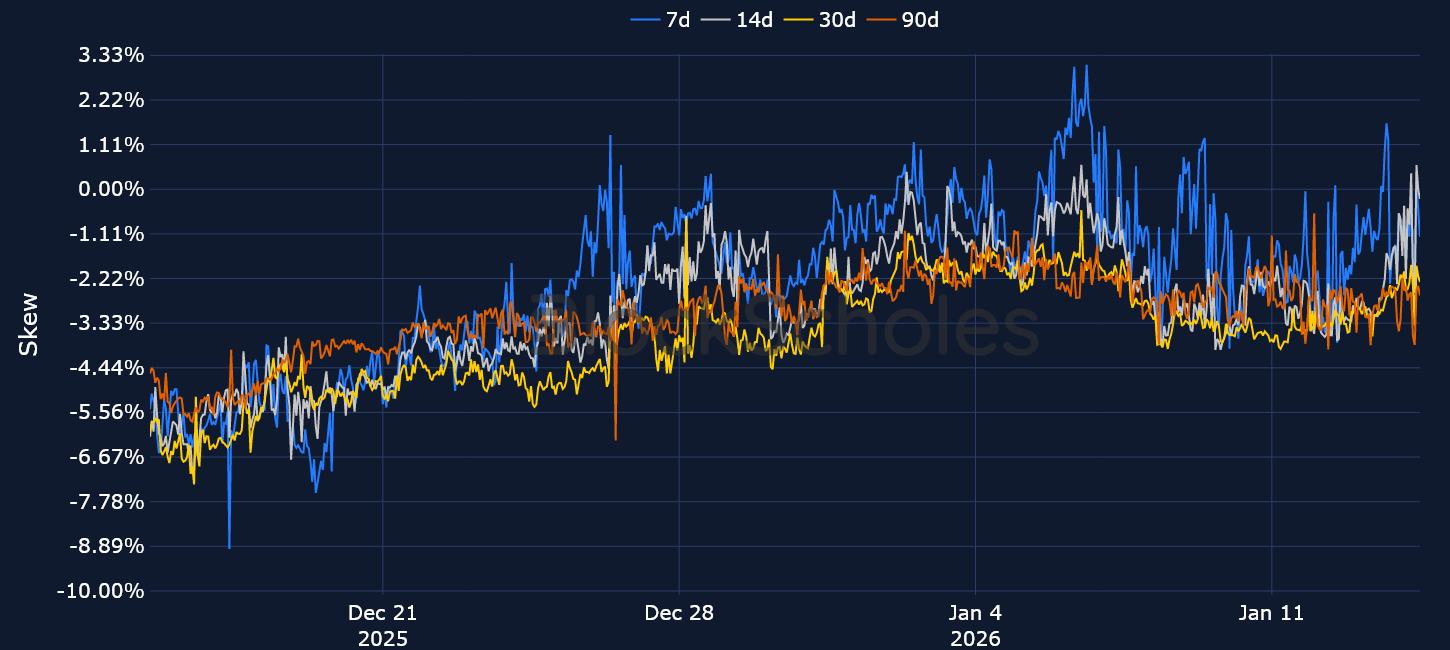

Additionally, we see signs that derivatives markets are supporting a continuation of the rally. Volatility smiles for shorter-dated options have moved towards neutral skew (from previously bearish positions) and 7-day futures trade with a 10% premium over spot price, a sign of a strong willingness for leveraged exposure.

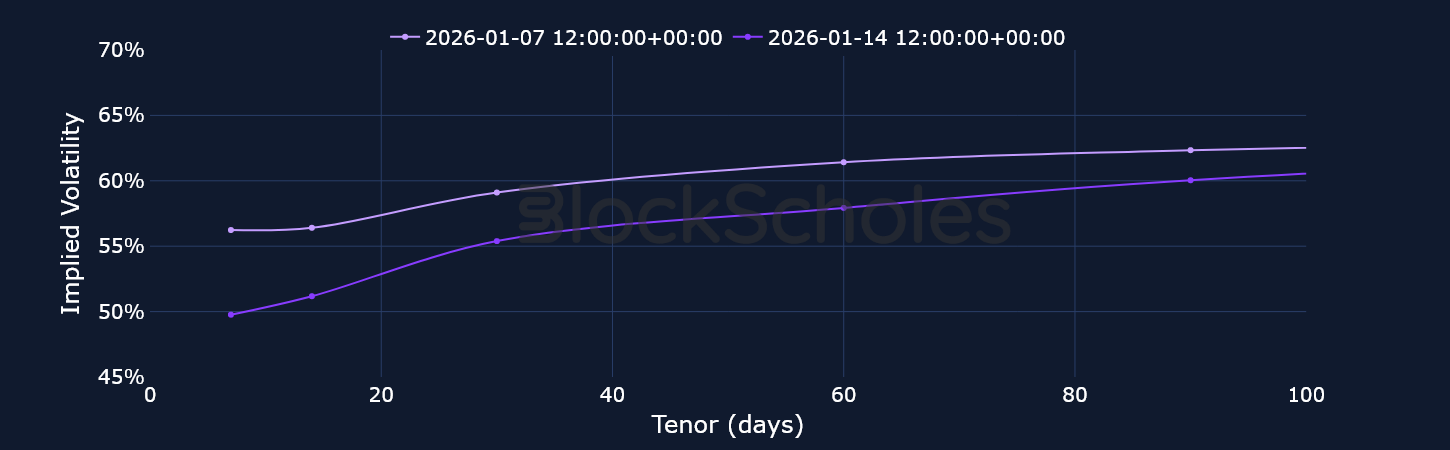

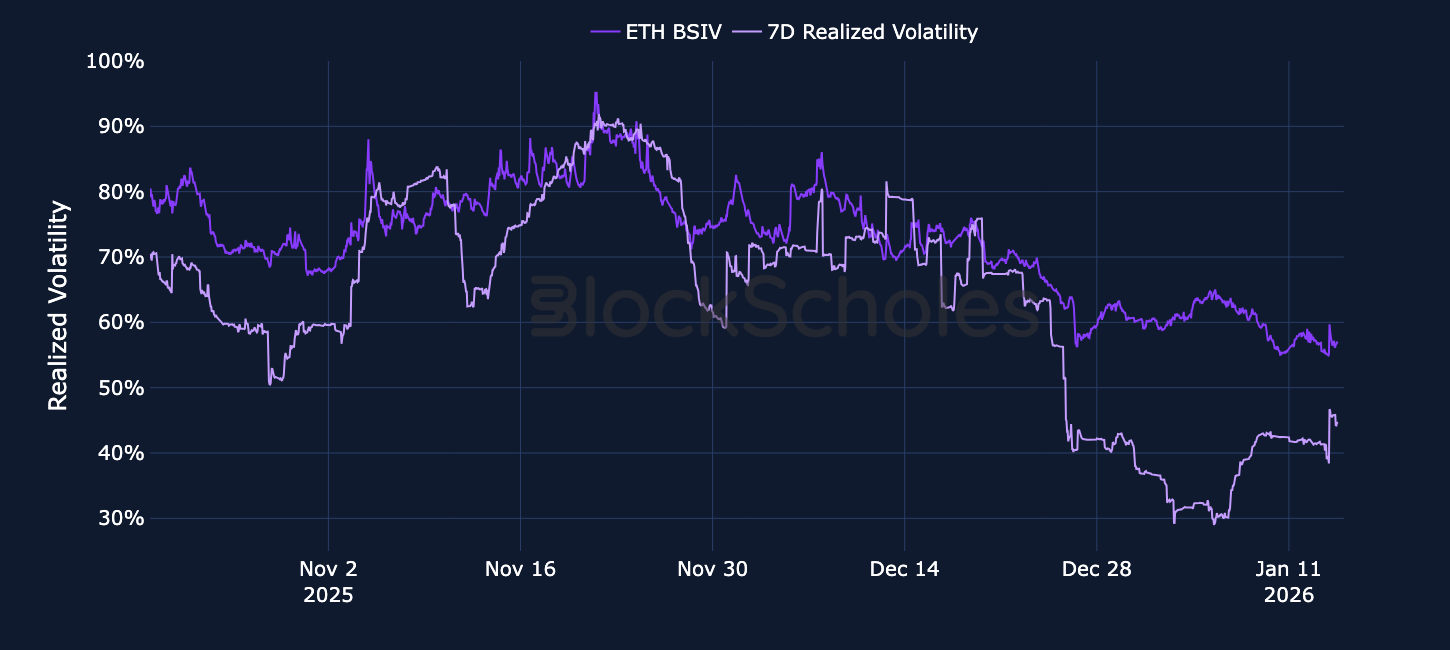

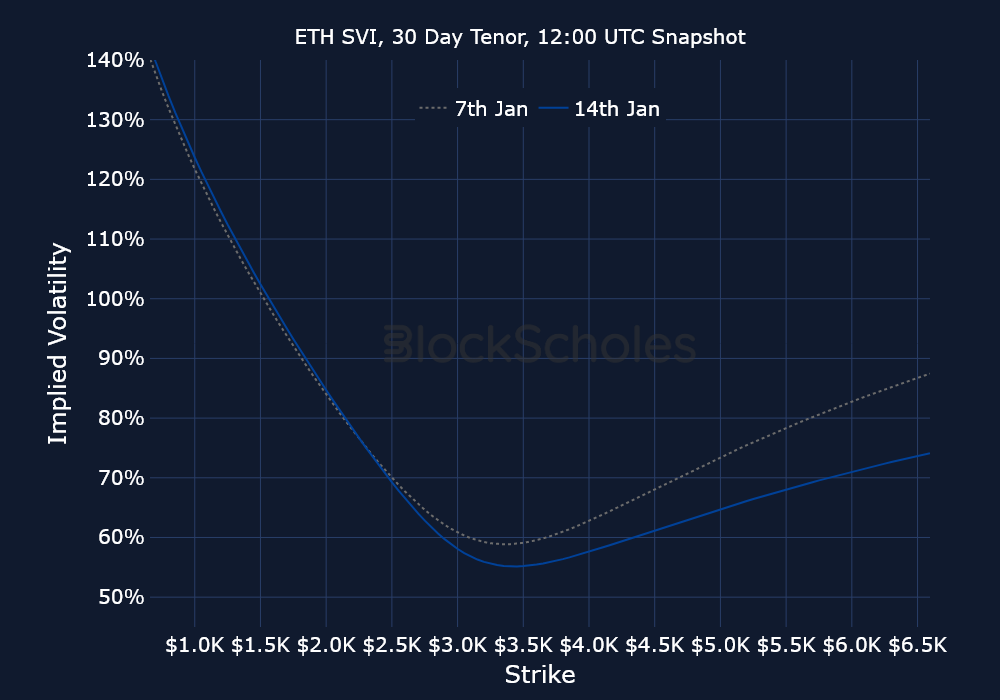

Just like BTC, ETH has spent the past month trapped in sideways trading around the psychological $3K mark. The recent breakout past $3.3K, however, has seen it move to its highest levels so far this year – supported by modestly strong Spot ETF inflows that have accumulated a net $241M year-to-date.

That move in the spot price has had some impact on realized volatility, which trades above the extreme lows we saw during the Christmas break, but still far lower relative to ETH’s history than we are used to. The current 50% realized volatility is the lowest level since before the US election in November 2024.

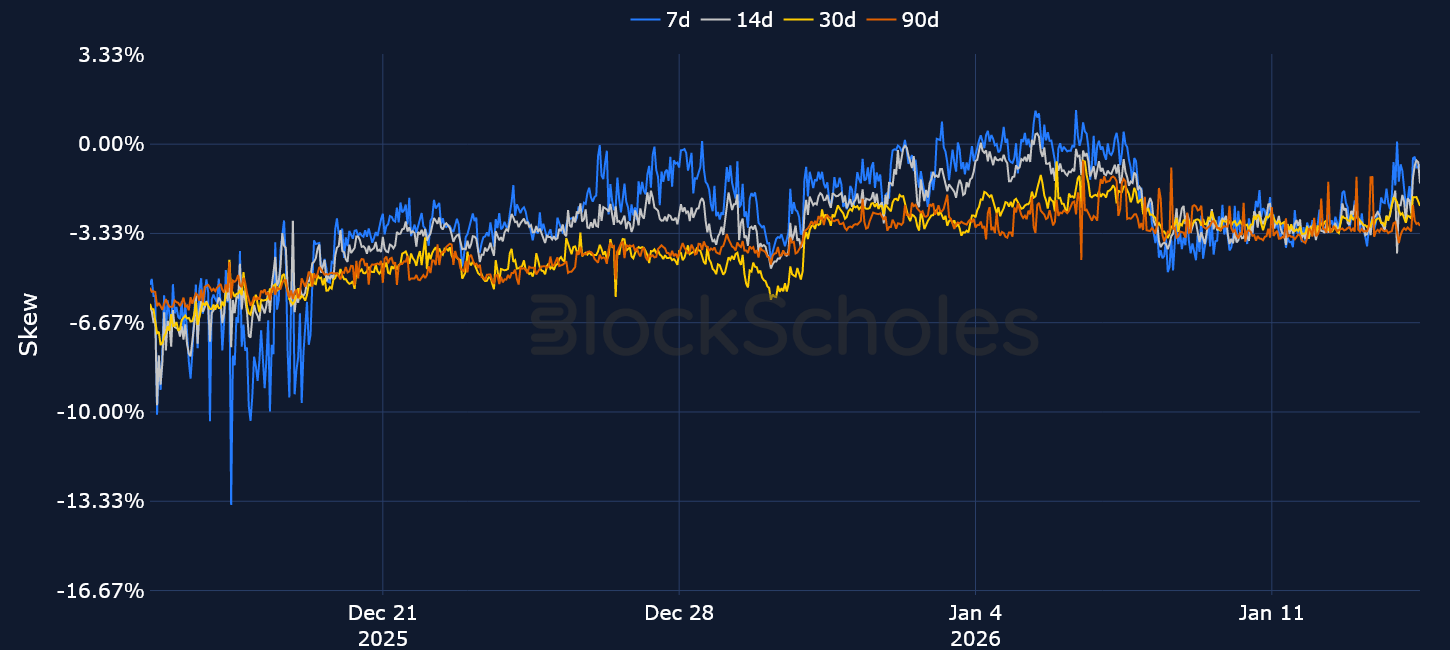

Despite the spot price rally, options volumes and open interest are both skewed towards put contracts. Take Jan 13, 2026 for example: options volumes were nearly twice as large in put contracts than in calls, while open interest was also slightly higher in puts.

ETH is also benefitting from a surge in staking demand. Currently over 36M ETH is now staked on the Beacon chain, nearly 30% of the network’s circulating supply – a high last seen in July 2025. There’s also 2,403,590 ETH in the validator queue waiting to be staked – a level last seen in August 2023.

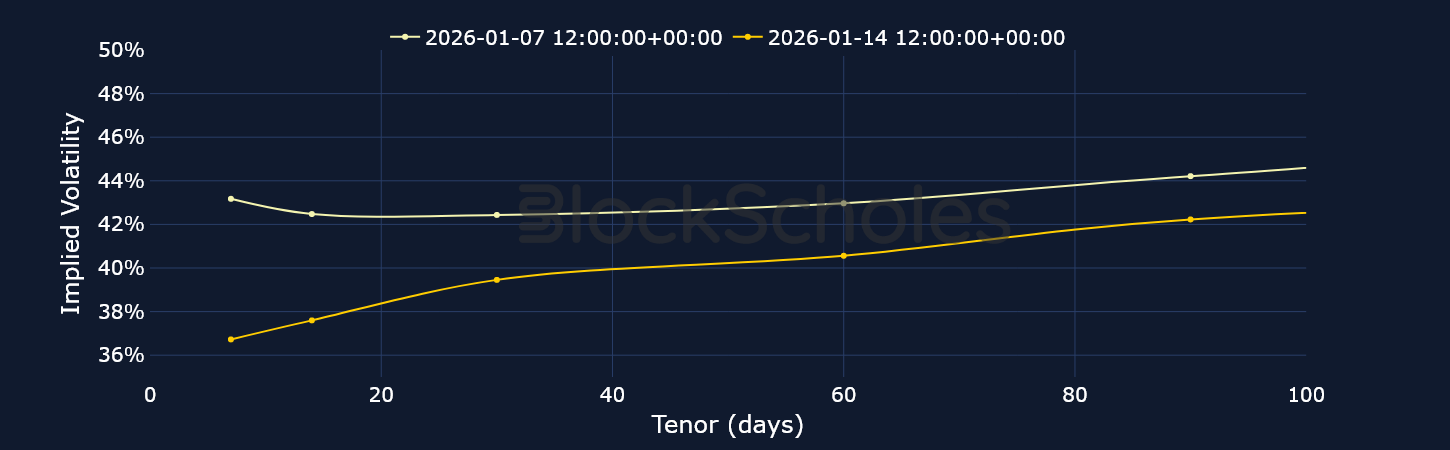

When BTC surpassed $94K earlier this month, we saw a change in the skew of volatility smiles from a bearish put premium to a neutral skew. When that level did not hold, traders once more assigned a volatility premium for OTM puts. Now, a similar region of $94-96K has proven to be a trigger for another change in sentiment from bearish to neutral.

While we are yet to see short-dated volatility smiles fully skew towards calls, taking history as a guide suggests that if BTC fails to hold $95K, we may see a return back to the put premium.

Ultimately, what that suggests is that derivatives markets, particularly options, look seemingly willing to back the move higher in spot price, but a failure to hold at those levels is resulting in a return back to bearish protection.

What’s also interesting is the clustering of the term structure for both BTC and ETH at the same values. For much of the past week, all tenors have traded with a -3% skew for BTC and -3-4% skew for ETH. That’s interesting given that the shorter end of the term structure tends to be more reactive to volatile moves in the short term.

Open interest and trading volume data are sourced “as is” from the Bybit exchange platform API exclusively, and as such do not represent a comprehensive picture of the sum of trading activity across all derivatives markets or exchanges. The data visualized in this report consists of hourly and daily snapshots, recorded over the previous 30 days. Daily (hourly) snapshots of trade volume record the total sum of the notional value of trades recorded in the 24H (1 hour) period, beginning with the snapshot timestamp.

If not explicitly labeled as derived from another exchange, the input instrument prices to all derivatives analytics metrics in this report are sourced from the appropriate endpoints of Bybit’s public exchange platform API. In the event that data is labeled or referred to as representing the market on another exchange source, that data is sourced from the appropriate endpoint of each respective exchange’s public API.

Macroeconomic charts and data are sourced “as is” from the Bloomberg Terminal. Exchange data is sourced “as is” from publicly available exchange APIs. Block Scholes makes no claims about the veracity of public third-party data.

After acquisition of underlying-denominated raw data for open interest and trading volume on the Bybit exchange platform from Bybit’s API endpoint, equivalent dollar-denominated figures are calculated using the concurrent value of Block Scholes’s Spot Index for the relevant underlying asset.

Block Scholes’s Spot Index represents the aggregate Spot mid-price for a given currency across the top five CEXs by volume (with USD-quoted markets). It considers the proportion of total volume in the instrument on the exchange, as well as the deviation of a data point from those on other exchanges.

Futures prices are used for Block Scholes’s futures-implied yields calculation services in order to derive the constant-tenor annualized yields displayed in the Futures section of this report.

Options prices are used for Block Scholes’s implied volatility calculation services in order to calibrate volatility surfaces, from which all derivatives volatility analytics displayed in the BTC Options and ETH Options sections of this report are calculated. Volatility smiles are constructed by calibrating to mid-market prices observed in Bybit options markets. As part of the calibration process, prices go through rigorous filtration and cleaning steps, which ensures that the resulting volatility surface is arbitrage-free and has exceptional fit to the market observables.

.jpg)

.jpg)