Thahbib Rahman

Research Analyst

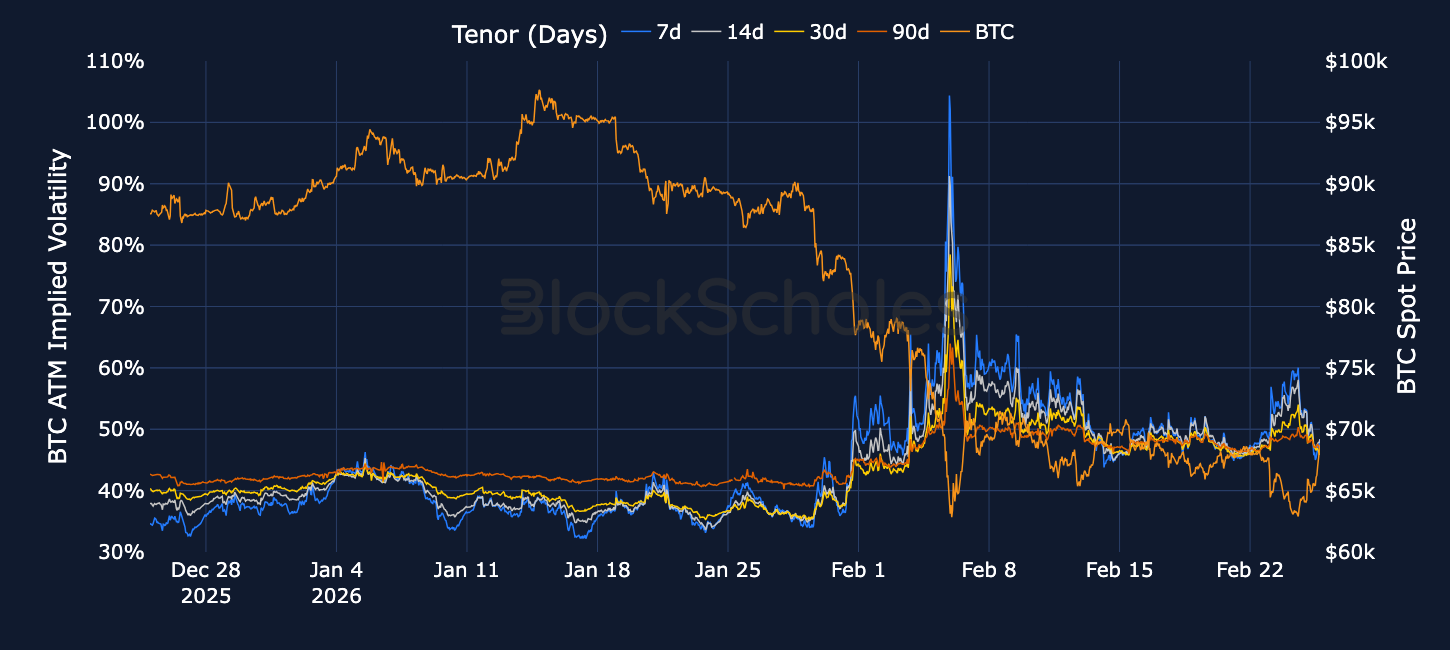

While BTC previously traded in a tight range, the low level of realized volatility broke this week when the price briefly fell to $62K. The move coincided with a weakening in risk appetite across broader markets, and options pricing responded quickly with a strong increase in demand for downside protection. However, a sharp correction back to the $68K levels at the time of writing, after a brief stint at the $70k handle, lost in the sell-off has not seen the same response in volatility markets.

While BTC previously traded in a tight range, the low level of realized volatility broke this week when the price briefly fell to $62K. The move coincided with a weakening in risk appetite across broader markets, and options pricing responded quickly with a strong increase in demand for downside protection.

However, a sharp correction back to the $68K levels at the time of writing, after a brief stint at the $70k handle, lost in the sell-off has not seen the same response in volatility markets.

While the skew of volatility smiles towards OTM puts has recovered, the snap back higher did not see ATM implied volatility levels jump to the same extremes. While traders are now pricing in larger near-term moves, with one-week implied volatility jumping, the front end of the volatility curve is only mildly inverted.

The bearish tone is not limited to options markets.

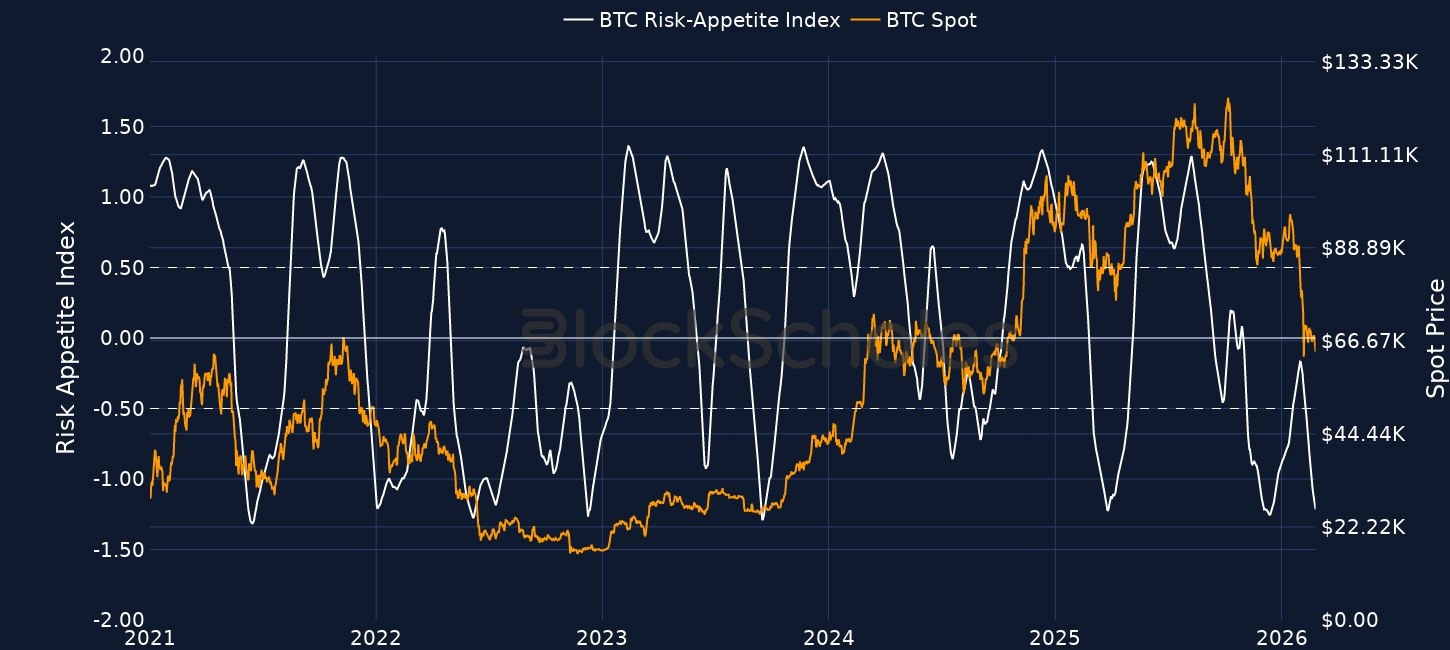

Block Scholes’ Risk Appetite Index measures the level of euphoria (above 1) or panic (below -1) in the spot market. Momentum in this index shows a strong relationship to spot returns.

The past two weeks of sideways consolidation were sharply interrupted this week as BTC fell to $62K. Risk appetite dampened across both crypto markets and broader macro asset classes, after President Trump vowed not to let the Supreme Court’s ruling on tariffs affect his signature economic policy.

However, the last 24 hours have seen BTC recover to around the $68K level that it last held in a single-minded rally higher.

While the initial sharp breakout to the downside in spot price resulted in options traders pricing optionality higher, the recovery of the lost spot levels has not. BTC’s term structure of volatility is still in a mild inversion after 7-day ATM IV jumped a full 10 percentage points to 60%, coinciding with a nearly 10-point jump in 7-day delivered volatility, but short-dated optionality is still far lower on the way up in spot than it was on the way down.

That quick repricing in implied volatility was largely driven by traders willing to pay a higher premium for insurance against further downside risk. While options prices have not yet fallen to their previous levels, the correction to the upside has not spiked options pricing in the same way.

In short, options prices remain lower than during the height of the sell-off.

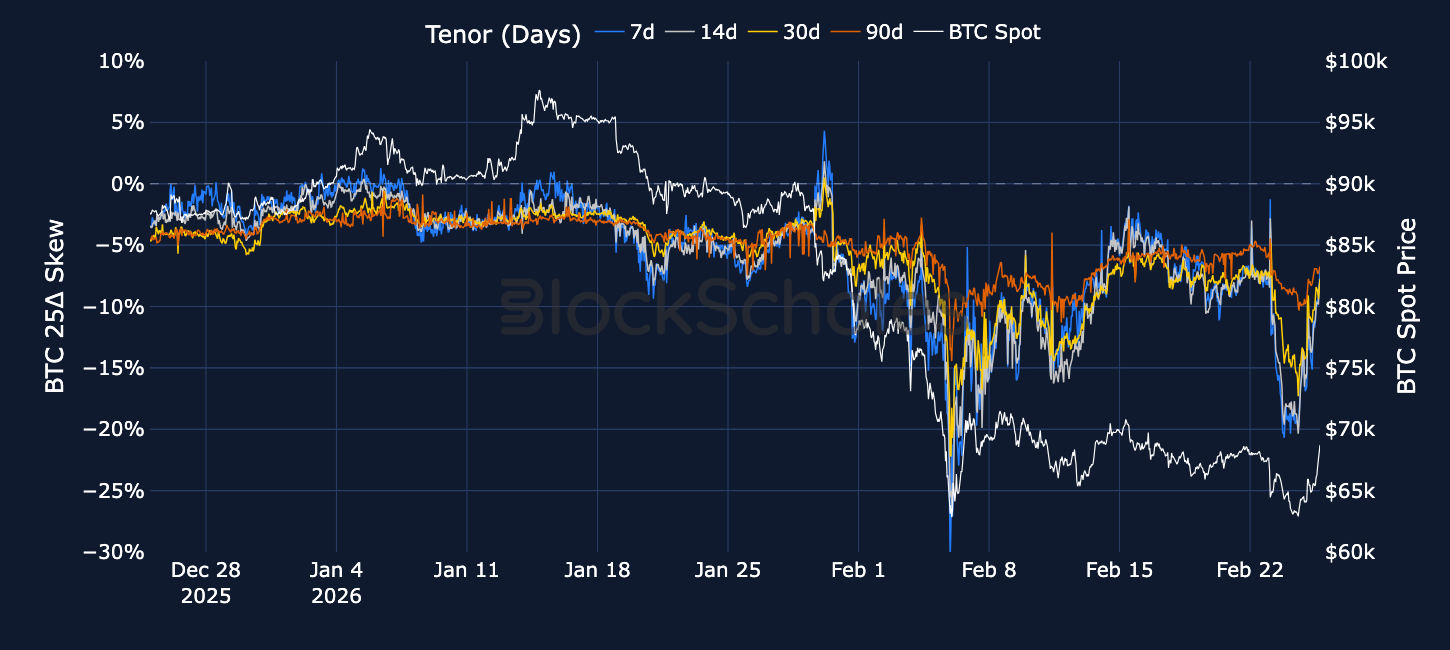

The impact of the recovery rally is more obvious in its impact on the skew of volatility smiles. In response to the sell-off on Feb 23, 2026, the relative preference for put options rather than call options fell back to the lows Feb 6 selloff, when BTC last traded at its 2026 lower bound.

However, since the recovery of the $68K level, put options no longer trade with as much of an extreme premium as they did.

This does not mean that options markets are now bullish – far from it.

Derivatives markets are still (in aggregate) looking for protection against a further selloff.

But while this slightly heavier positioning in short positions is bearish, it could see some traders caught offside and forced to close bearish positions in the case that the current rally in spot continues.

With Bitcoin now down about 46% from its all-time high, we see signs of bearish sentiment from all angles, not just in options markets.

Factors that had previously supported price action are now all working in the opposite direction.

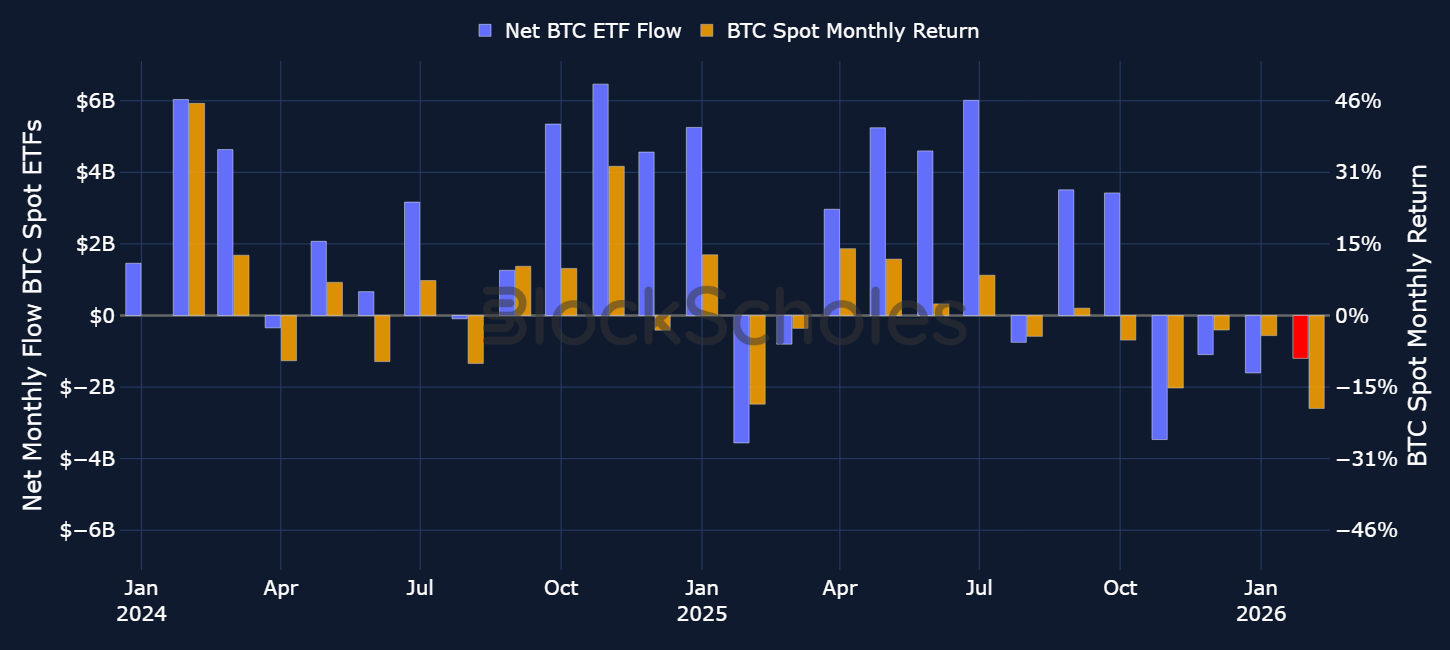

Firstly, Spot exchange-traded funds tracking Bitcoin are on track for their fourth consecutive month of outflows — the longest streak of net selling we’ve observed since their launch. Through the use of Spot ETFs, institutional investors had provided a consistent structural bid that had supported much of the bullish run in Q1 2024 as well as the post-Liberation Day recovery rally of 2025. As institutions continue to actively reduce their exposure, the demand cushion they had provided spot markets with continues to get weaker, reducing the likelihood of a sustained spot price recovery until institutional appetite returns.

The current four-month outflow streak of Spot Bitcoin ETFs also coincides with BTC spot returns on track for their fifth month of losses. The last time we saw a five-month losing streak was during the bear market that followed the 2018 ICO boom.

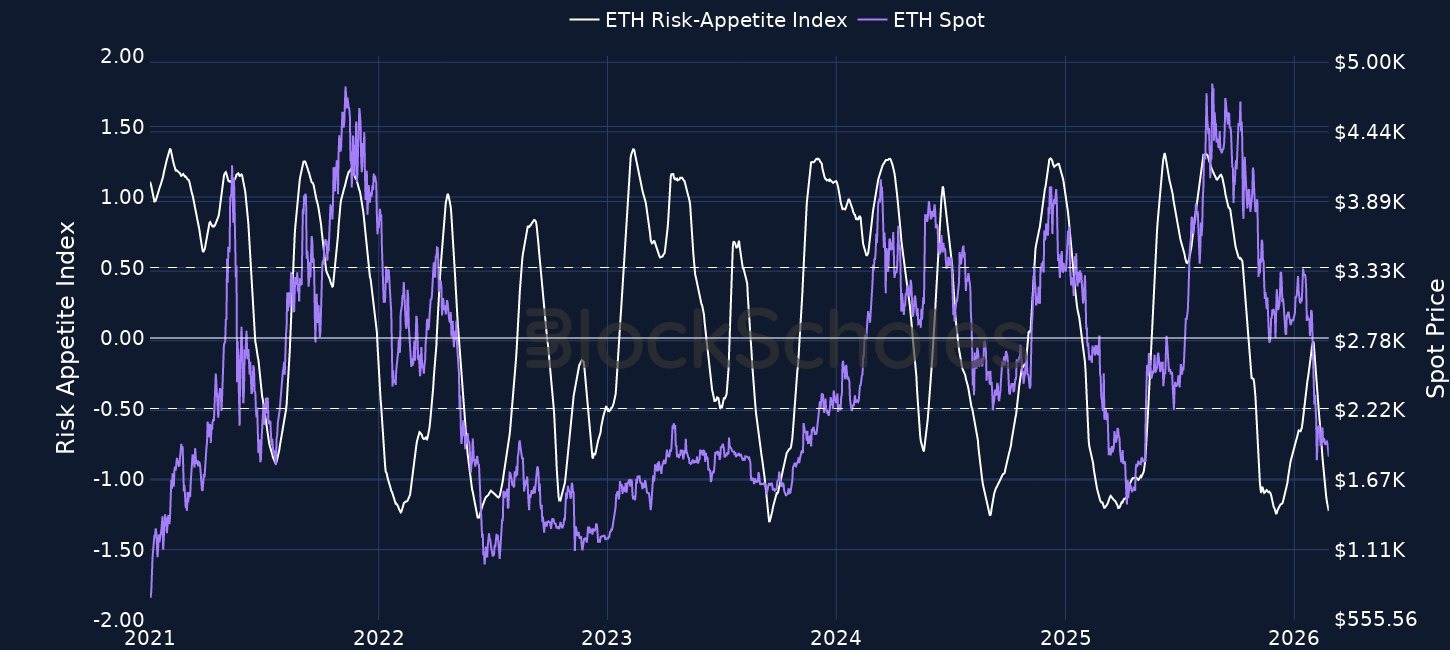

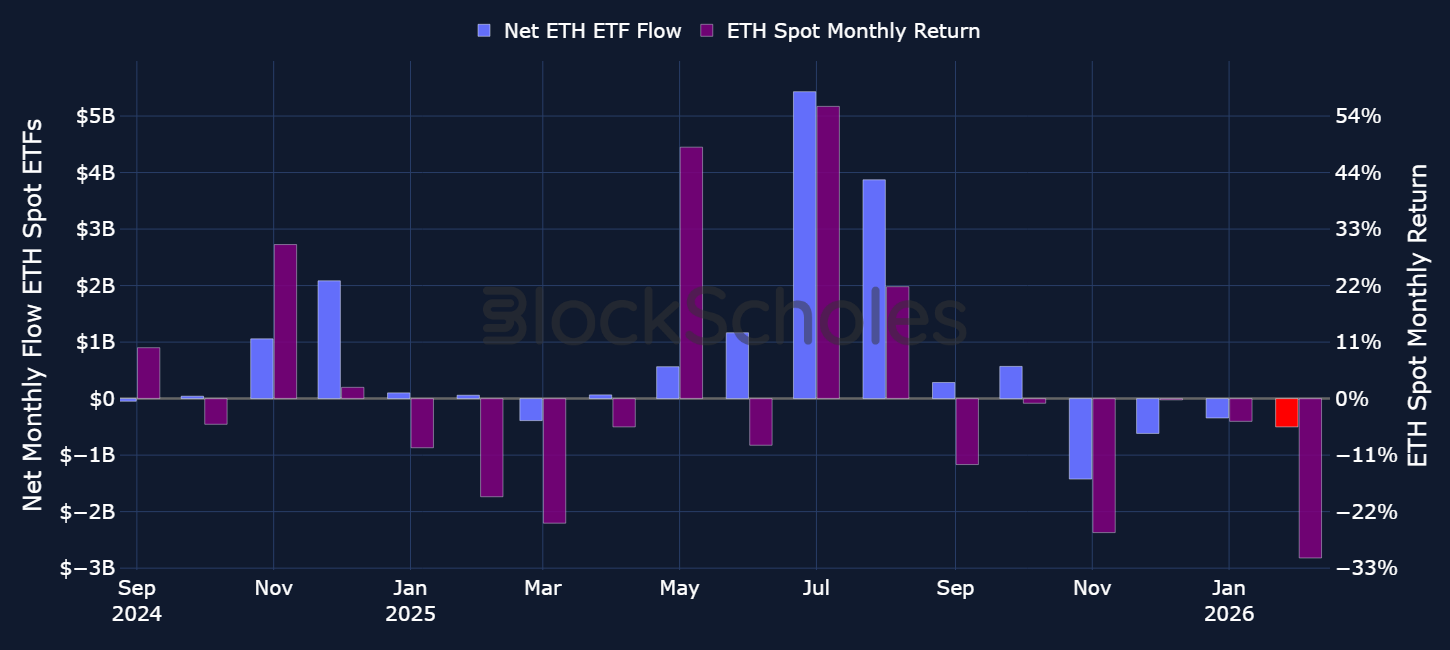

The story is equally bearish in ETH too — Spot ETFs are also on track for a fourth month of outflows (the longest since their respective launch in July 2024).

Spot ETFs are not the only vehicle through which we can measure the strength of the institutional bid on Bitcoin. Another is through digital asset treasury (DAT) firms. Several are showing the same lack of conviction as Spot ETFs. The most recent example is the case of Bitcoin mining and AI infrastructure company, Bitdeer Technologies (BTDR), which announced earlier this week that it had sold the entirety of its bitcoin holdings. Despite the company’s chairman and CEO, Jihan Wu, responding that “Holding zero shares [of BTC] now does not mean it will always be this way”, the switch away from Bitcoin accumulation towards land acquisitions for AI data-center expansion is at least an empirical instance of a short-term pivot away from crypto markets by institutions.

While the Oct 10th liquidation event saw the notional dollar amount of open interest in perpetual futures contracts more than halved, the most recent recovery in spot indicates that perpetual swap markets are backing the rally. After steadily declining for most of the remainder of Q4 2025 and since the new year, open interest levels in perpetual swaps of major tokens has reached its highest level since late January in the last 24 hours. Net open interest over 9 key token pairs now totals back above $6B.

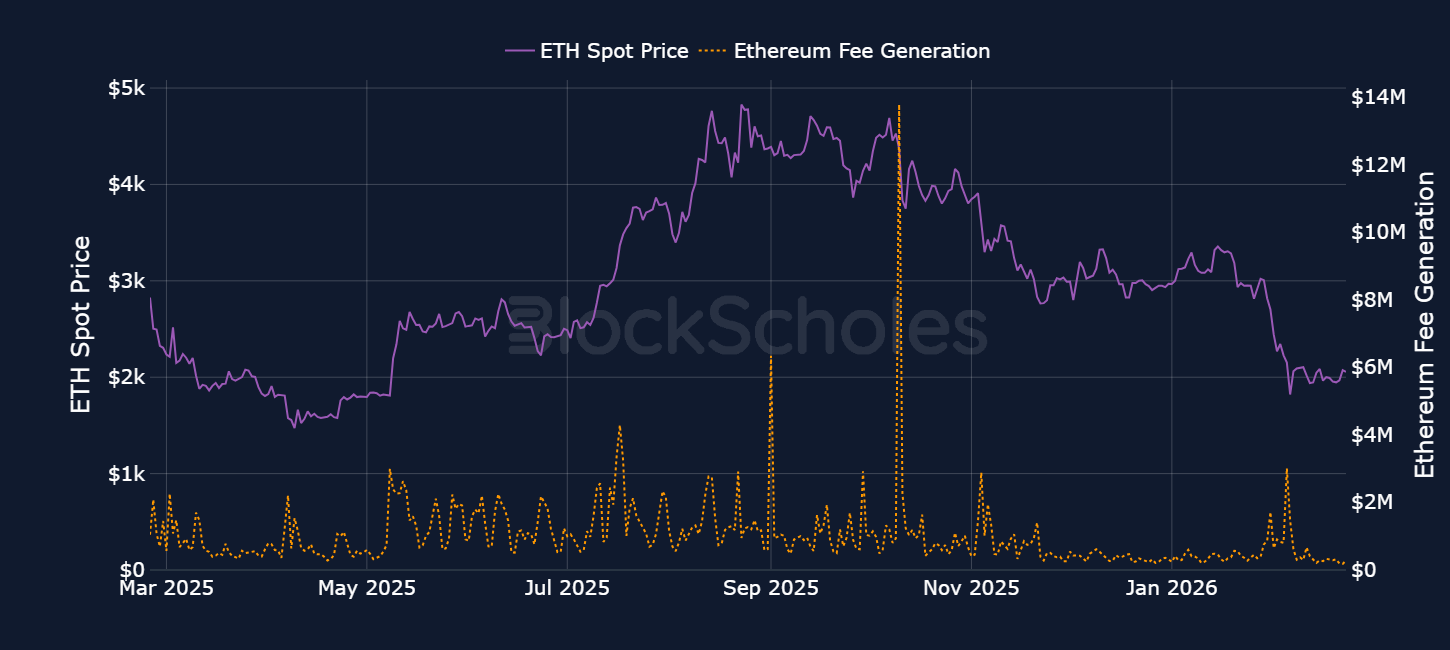

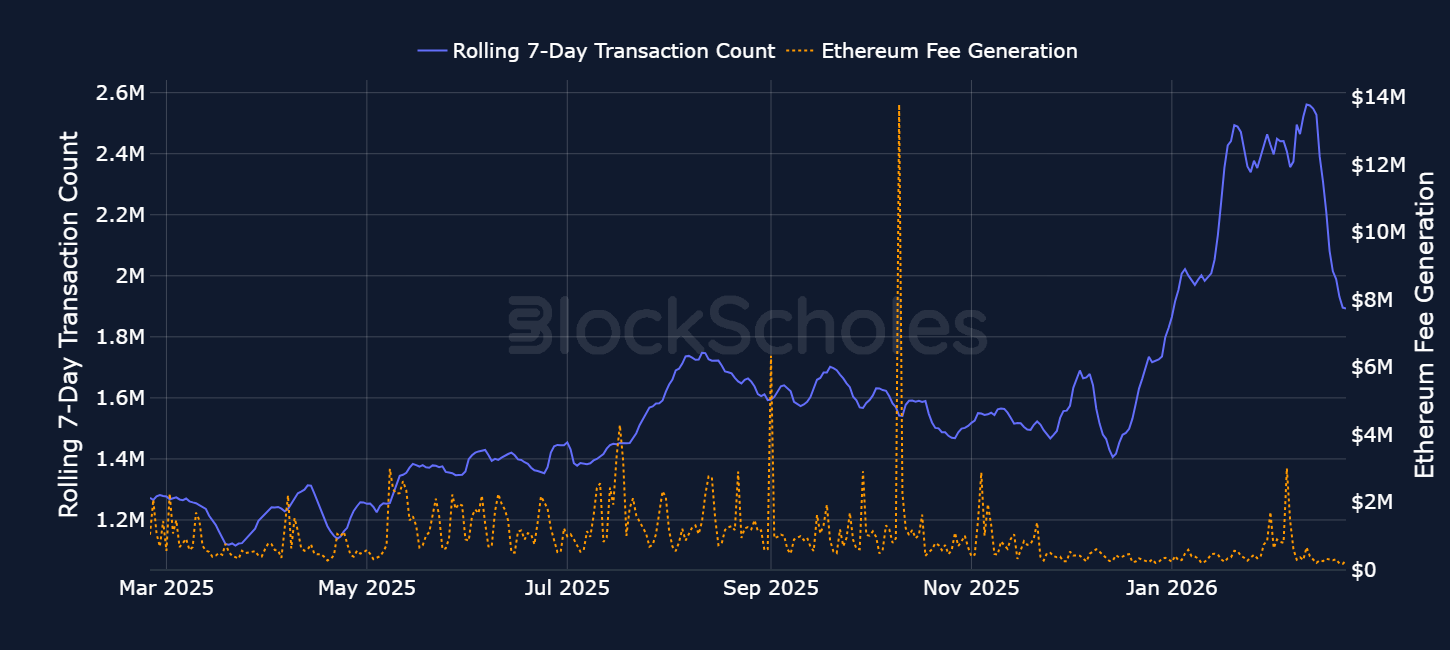

Ethereum Chain Fee generation has reached local lows, coinciding with a major crash in the spot price.

ETH fees represent both the revenue the network generates and the level of on-chain usage. On Ethereum, every transaction includes a base fee, which is permanently burned, reducing total ETH supply — this is why ETH can at times become deflationary, when more ETH is burned than is issued to validators.

Currently, ETH is on an extremely slow deflationary trend, which over the past year has had a negligible impact on overall supply dynamics.

The chart below shows that the rolling 7-day transaction count (and therefore usage) of the Ethereum blockchain has dropped significantly. Lower transaction fee revenue directly affects validator income from staking yields: fewer transactions mean fewer tips when placing an order, as there is less incentive to pay for priority inclusion when there are fewer transactions in the queue. This also implies fewer MEV (Maximum Extractable Value) opportunities – the extra tips paid to validators to order transactions within blocks to maximise a user’s arbitrage opportunities. Although one might expect more transactions to result in more fees, the correlation is not clear-cut.

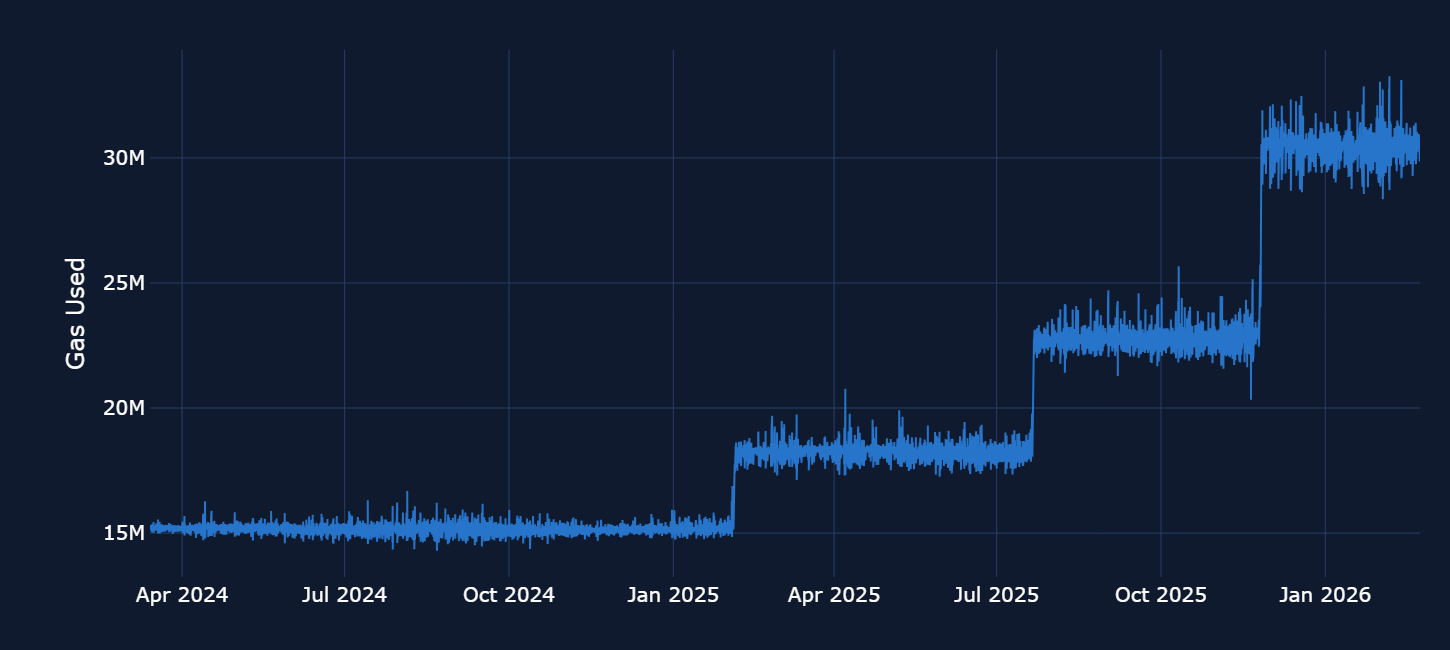

Ethereum's base fee charge is algorithmically adjusted based on network congestion. The decoupling between transaction count and fees generated by the Ethereum network results from increases in the gas limit per block. Gas in Ethereum is the unit of measurement for the computational work required to execute transactions and smart contract operations on the network. Gas limits per block increased from ~30M per block to ~36M in February 2025, then to 45 million on July 22, 2025, and finally to 60M in late November 2025, after a majority of Ethereum validators, more than 50% of staked validators proposing blocks, signalled support for a higher block gas limit.

Ethereum’s gas usage per block has increased, meaning each block now processes more computational work than before. However, demand for blockspace has not risen in line with this higher capacity, so blocks have been less congested, and the base fee has adjusted downward. As a result, overall fee generation has declined: with lower base fees under EIP-1559, average transaction costs have fallen, and less ETH is being burned per block.

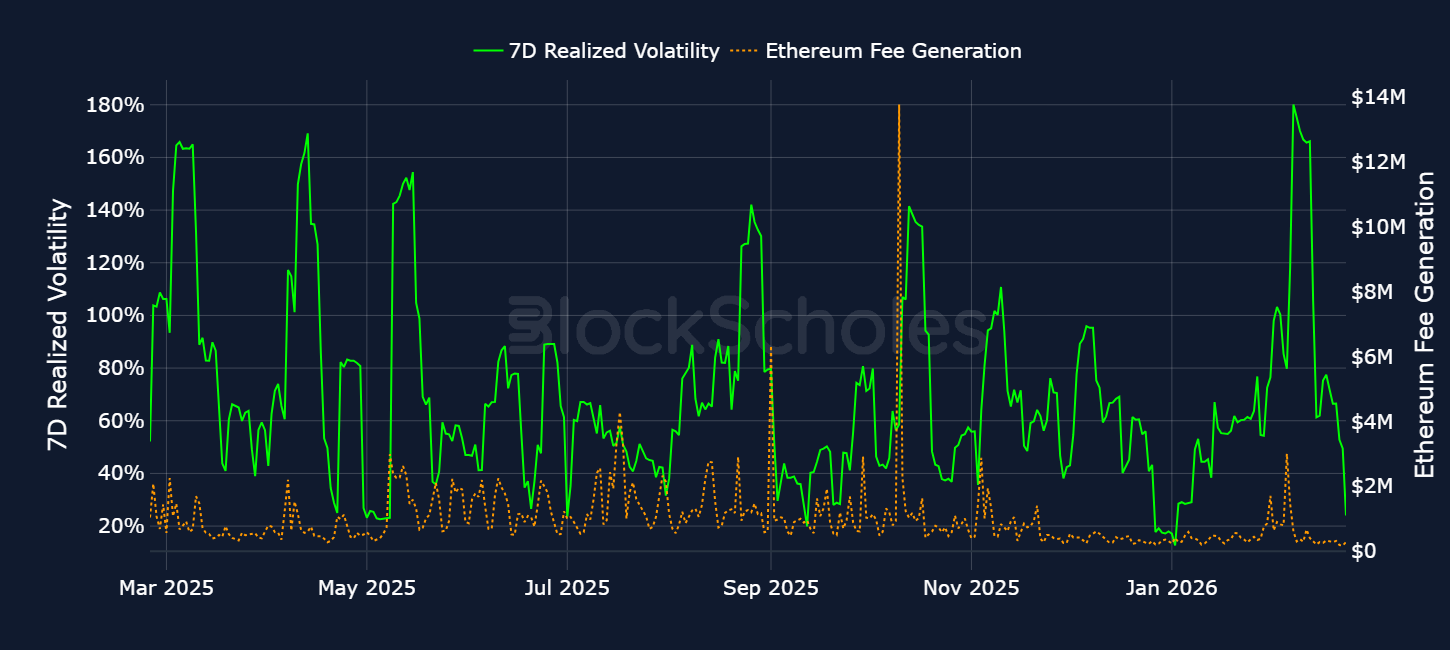

One of the strongest current drivers of fee generation is the relationship between Ethereum’s realized volatility and network fees.

This is because large price movements trigger bursts of trading activity, as market participants rush to reposition or manage risk simultaneously. The resulting surge in transaction demand pushes up congestion, and under Ethereum’s supply–demand–based base fee mechanism, this translates directly into spikes in fee generation.

Alongside, Coinbase has partnered with Yahoo Finance to enable users to move directly from researching an asset on Yahoo Finance to executing a trade on Coinbase, while also providing integrated tools within Yahoo Finance for asset discovery and tracking.

The idea is to partner with a third-party vendor to run dollar-pegged token payments and launch a new wallet, rather than building the full stack internally.

The initiative starts with a 2,016 ETH deposit and targets around 70,000 ETH staked in total, with rewards flowing back into the EF treasury.

This brings its crypto, total cash, and “moonshots” holdings to $9.6B, including 4,422,659 ETH valued at $1,958 per ETH, representing 3.66% of the total ETH supply (over 73% toward its “Alchemy of 5%” goal), 193 BTC, $691M in cash, a $200M stake in Beast Industries, and a $17M stake in Eightco Holdings.

As of February 22, 2026, Bitmine has staked 3,040,483 ETH worth $6.0B, generating $171M in annualized staking revenue, and is on track to launch its MAVAN staking solution in Q1 2026.

The transition will happen in two stages: new CNH₮ issuance will stop immediately (no more tokens will be minted), and redemptions will remain available for one year, after which Tether will end redemption support, with a reminder notice to follow closer to the deadline.

The move follows a $325M convertible notes offering and a $43.5M equity raise, suggesting the liquidation may be aimed at boosting cash as it expands data centers and pivots toward AI.

Trading will run continuously on CME Globex, with a minimum two-hour maintenance window each weekend, and any positions traded from Friday evening through Sunday evening will be dated and processed on the next business day for clearing, settlement, and regulatory reporting.

He said all major transactions were announced promptly, arguing critics are misreading financial statements and misunderstanding accounting-driven losses.

EVMbench draws on 120 curated vulnerabilities from 40 audits, including sponsored open-code audit competitions and security reviews for Tempo, the Layer 1 blockchain co-developed by Paradigm and Stripe, and tests AI agents’ capability modes like vulnerability detection, contract modification, exploit mitigation, and end-to-end fund-draining attacks in a sandboxed blockchain environment.

This is an expansion to their previous offering, which only allowed BTC and ETH as collateral, allowing loans of up to $5M and $1M, respectively.

The goal is to give the Hyperliquid community a presence in Washington and push for clearer, more workable regulations for DeFi, particularly around perpetual derivatives and decentralized markets via research, policy engagement, and direct outreach to lawmakers, serving as a resource for informed policymaking.

The key change is access control, which is now a “permissioned domain” that allows the venue operator to define which approved entities can place orders and which can fill them, enabling participation to be linked to KYC/AML and other compliance requirements.

The feature is designed for regulated institutions, such as banks and brokers, that want on-chain settlement and liquidity but cannot interact with fully open DeFi markets.

The ROBO token is the native cryptocurrency of the Fabric Foundation, an initiative established by OpenMind.

The project describes itself as infrastructure for coordinating intelligent machines and robotics in a way that can be shared across many participants, with rules that are transparent and enforceable. The underlying premise, as stated in its public materials, is that as autonomous systems become economically active in the real world, coordination problems expand into identity, permissions, accountability, settlement, and incentive alignment between humans, organisations, and machines.

Fabric is designed as a blockchain network. It relies on an on-chain ledger and smart-contract rules so participants can share the same system of record for coordination and settlement without a single central operator. In practical terms, the chain is meant to be where network state is recorded and where economic activity is settled, so that permissions, transactions, and incentive flows are all handled in one consistent framework.

On the technical side, the architecture is described as a base layer that provides settlement and security, with the option to run more specialised execution environments on top of it, framed as robot sub-networks in an L2-style model. The idea is that robotics-related activity can run in environments tailored to those needs, while still anchoring outcomes to a common settlement layer.

Within that design, ROBO is positioned as the economic unit of the network. It is intended to be used for fees and settlement, and it is also tied to incentive mechanisms such as staking, delegation, and bond-like structures that are meant to coordinate participants and align behaviour over time.

The main differences compared to other tokens that are close to the AI narrative are that Fabric places the emphasis more directly on machines acting in the physical world, which naturally shifts attention toward settlement, accountability, and governance around actions that have real-world consequences. It also sits close to DePIN and the broader “machine economy” theme, where blockchains are used to coordinate real-world devices and services with token incentives. The difference here is that the focus is not mainly on getting device data on-chain, but on setting up a wider set of rules and payments for how autonomous machines interact and get coordinated, potentially across several environments that still settle back to the same base layer.

Bybit announced that ROBOUSDT is listed on Perpetual Pre-Market Trading from 25 Feb 2026.

Open interest and trading volume data are sourced “as is” from the Bybit exchange platform API exclusively, and as such do not represent a comprehensive picture of the sum of trading activity across all derivatives markets or exchanges. The data visualized in this report consists of hourly and daily snapshots, recorded over the previous 30 days. Daily (hourly) snapshots of trade volume record the total sum of the notional value of trades recorded in the 24H (1 hour) period, beginning with the snapshot timestamp.

If not explicitly labeled as derived from another exchange, the input instrument prices to all derivatives analytics metrics in this report are sourced from the appropriate endpoints of Bybit’s public exchange platform API. In the event that data is labeled or referred to as representing the market on another exchange source, that data is sourced from the appropriate endpoint of each respective exchange’s public API.

Macroeconomic charts and data are sourced “as is” from the Bloomberg Terminal. Exchange data is sourced “as is” from publicly available exchange APIs. Block Scholes makes no claims about the veracity of public third-party data.

After acquisition of underlying-denominated raw data for open interest and trading volume on the Bybit exchange platform from Bybit’s API endpoint, equivalent dollar-denominated figures are calculated using the concurrent value of Block Scholes’s Spot Index for the relevant underlying asset.

Block Scholes’s Spot Index represents the aggregate Spot mid-price for a given currency across the top five CEXs by volume (with USD-quoted markets). It considers the proportion of total volume in the instrument on the exchange, as well as the deviation of a data point from those on other exchanges.

Futures prices are used for Block Scholes’s futures-implied yields calculation services in order to derive the constant-tenor annualized yields displayed in the Futures section of this report.

Options prices are used for Block Scholes’s implied volatility calculation services in order to calibrate volatility surfaces, from which all derivatives volatility analytics displayed in the BTC Options and ETH Options sections of this report are calculated. Volatility smiles are constructed by calibrating to mid-market prices observed in Bybit options markets. As part of the calibration process, prices go through rigorous filtration and cleaning steps, which ensures that the resulting volatility surface is arbitrage-free and has exceptional fit to the market observables.

.jpg)

.jpg)