Thahbib Rahman

Research Analyst

With spot prices now in a consolidation phase following the sharp and violent selloff in early February, traders in options markets are showing a lack of interest. BTC has spent the past two weeks rangebound between $65K and $70K, while ETH trades around the $2,000 mark. ATM implied volatility levels have plunged off from their extreme 2022-esque highs, with traders anticipating far less volatility in the short-to-mid term, compared to only two weeks ago. The term structure of volatility for all three majors, BTC, ETH and SOL, is flat and compressed, while (as expected in a ~50% drawdown from all-time highs), volatility smiles are still skewed towards put options.

With spot prices now in a consolidation phase following the sharp and violent selloff in early February, traders in options markets are showing a lack of interest. BTC has spent the past two weeks rangebound between $65K and $70K, while ETH trades around the $2,000 mark.

ATM implied volatility levels have plunged off from their extreme 2022-esque highs, with traders anticipating far less volatility in the short-to-mid term, compared to only two weeks ago. The term structure of volatility for all three majors, BTC, ETH and SOL, is flat and compressed, while (as expected in a ~50% drawdown from all-time highs), volatility smiles are still skewed towards put options.

In DeFi, one of the most interesting developments furthering the convergence between TradFi and Defi, is BlackRock’s announcement to list its BUIDL token on UniswapX. The collaboration will provide whitelisted holders of BUIDL with another avenue for trading the token. The news resulted in a sharp, but short-lived rally in Uniswap’s native UNI token, which petered out just as quick.

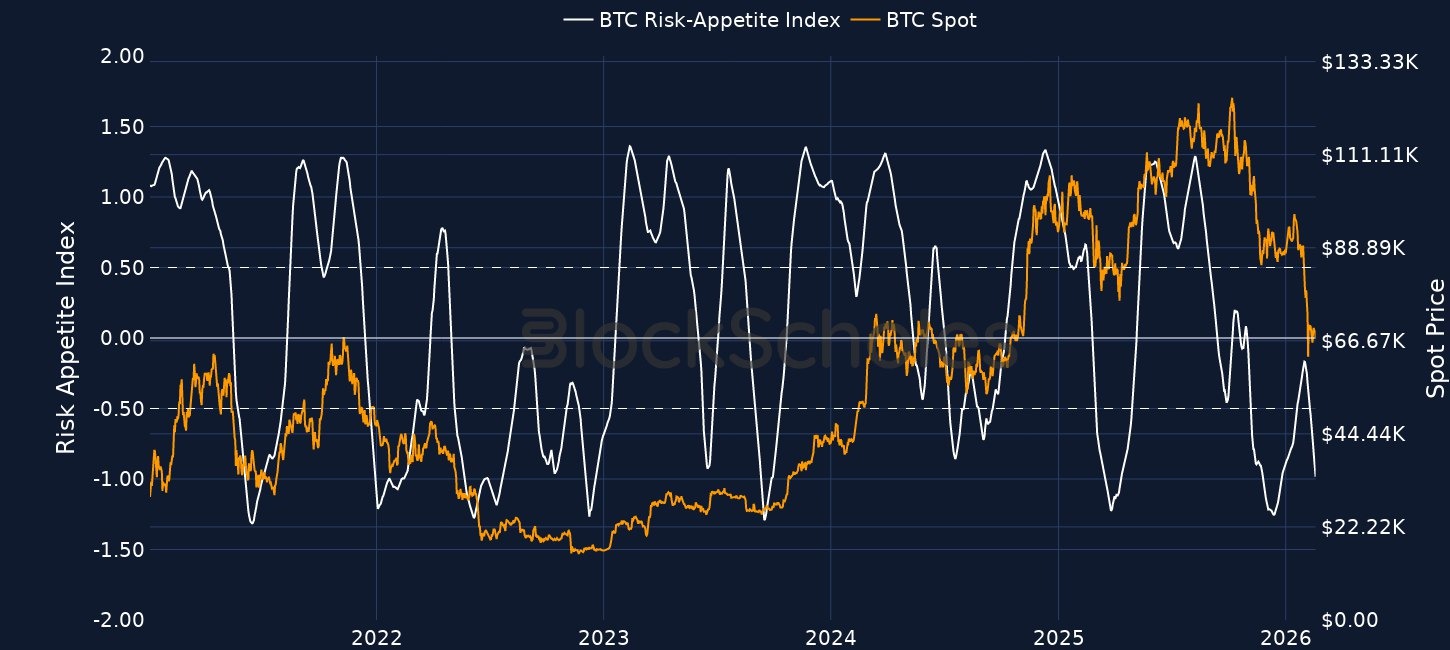

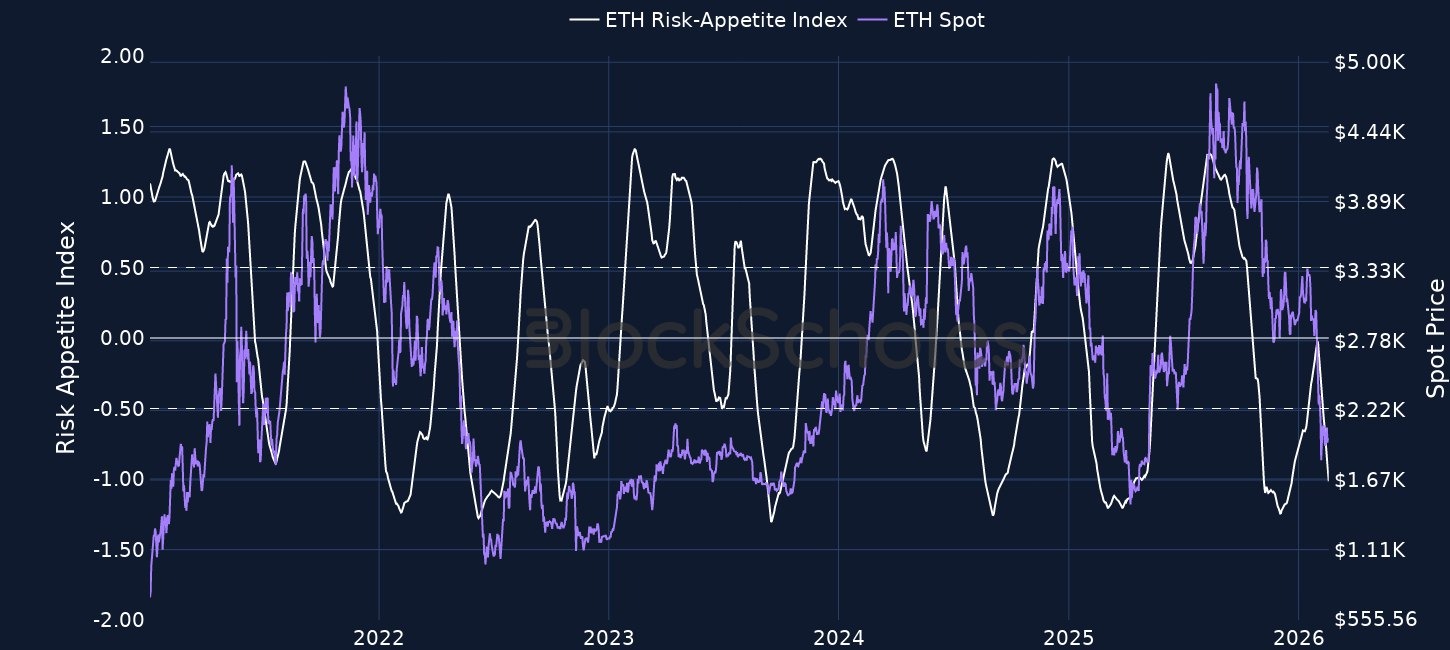

Block Scholes’ Risk Appetite Index measures the level of euphoria (above 1) or panic (below -1) in the spot market. Momentum in this index shows a strong relationship to spot returns.

After the Feb 5, 2026 brief crash below $60K, BTC quickly recovered back to $70K. That level soon proved to be a strong line of resistance for the time being, with spot price moving sideways between $65K and $70K in the two weeks since. Rangebound movements in both BTC spot and ETH spot (currently around $2,000) reflect a lack of catalysts in crypto markets that could push prices higher. One such potential catalyst is the passing of the CLARITY Act.

Treasury Secretary Scott Bessent recently told CNBC news that “in a time when we are having one of these historically volatile selloffs, I think some clarity on the CLARITY bill would give great comfort to the market, and we could move forward from there”.

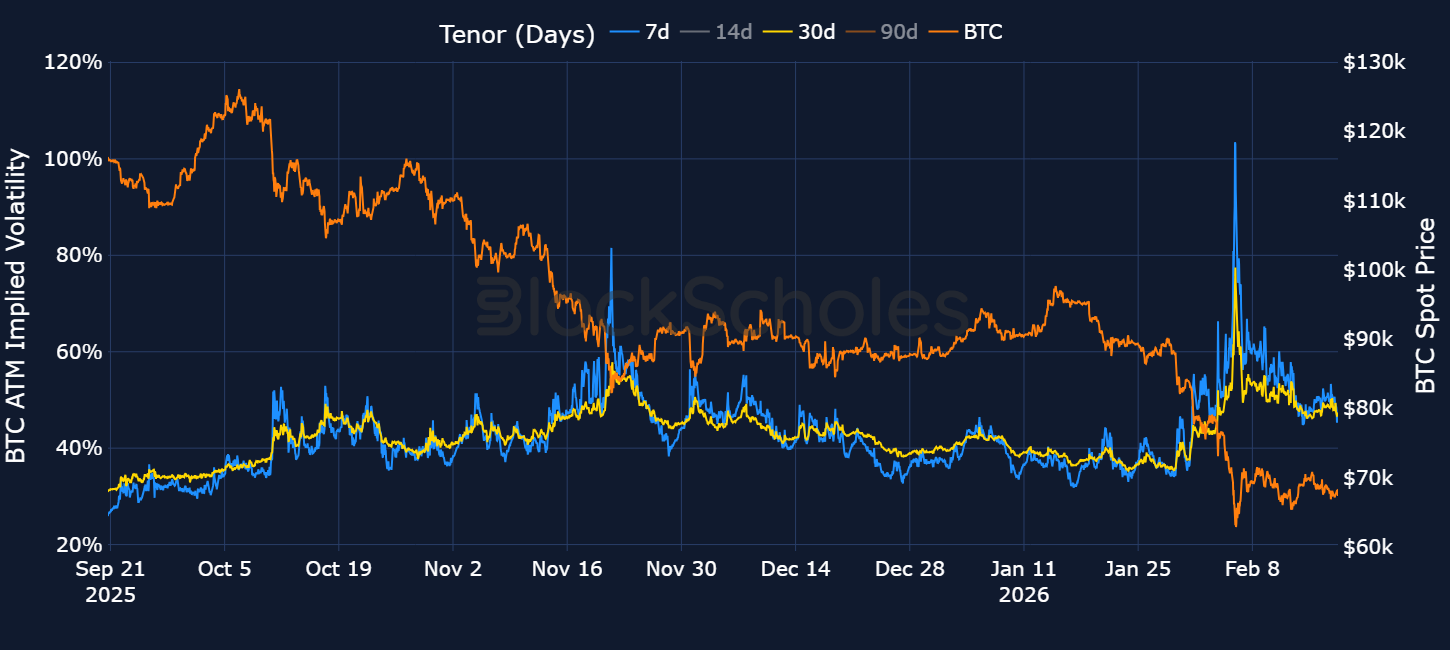

The lack of drivers to move spot price has taken its toll on derivative markets.

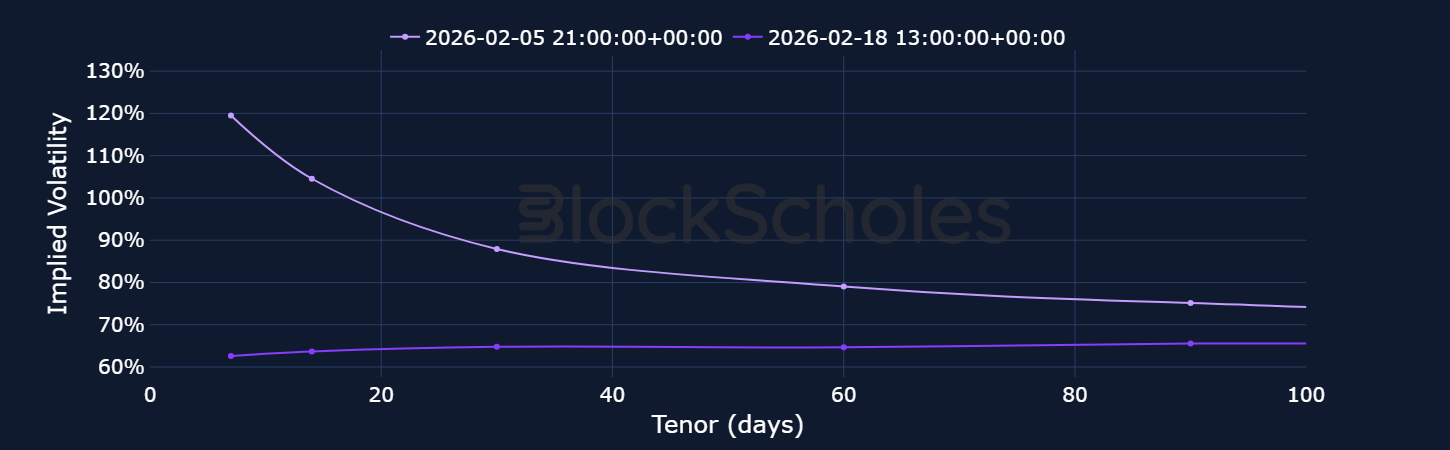

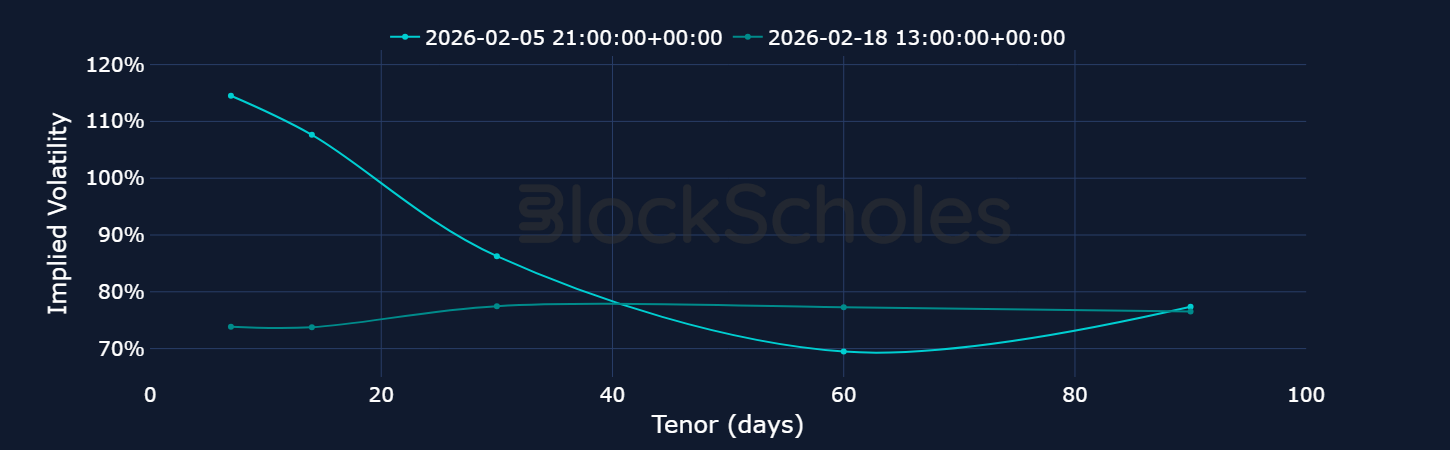

As shown below, after reaching highs last seen in 2022, short-dated BTC at-the-money implied volatility has now dropped by more than half, trading just shy of 50% for 7-day options. That’s even lower than the volatility realized by spot prices over the past 7 days, suggesting options traders were quick to give up the dramatic demand for downside protection they expressed just two weeks ago.

We see a similar decline in implied volatility beyond just BTC. The term structures of volatility for BTC, ETH and SOL are all currently compressed and flat, with traders pricing in minimal premiums for longer-dated options compared to near-term expiries. That significantly contrasts the positioning of two weeks ago, when short-dated volatility spiked across all assets on Feb 5, 2026, as BTC fell below $60K.

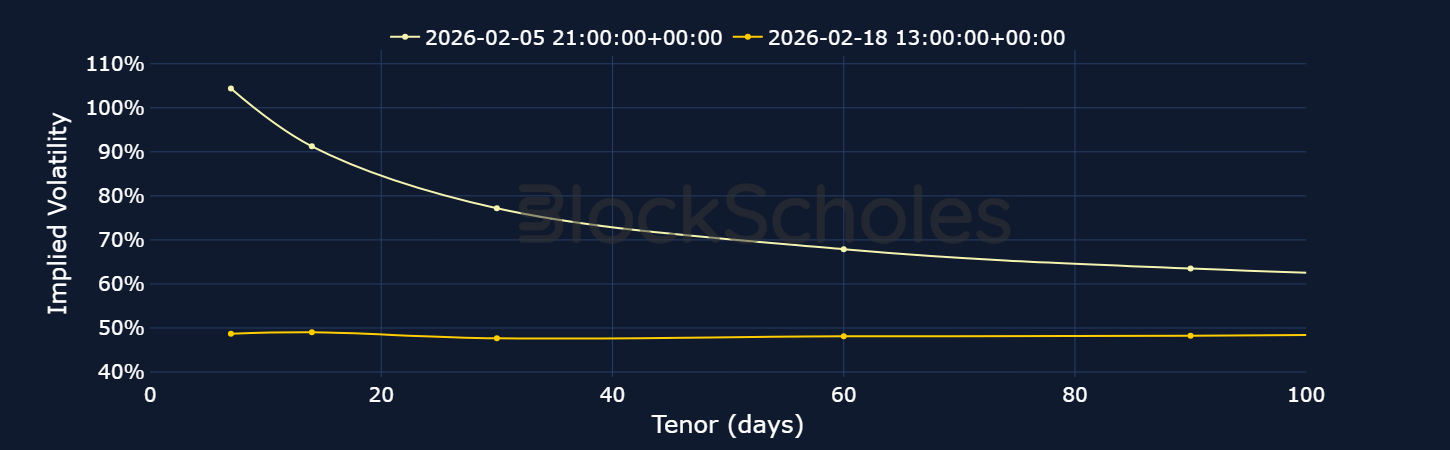

With risk-sentiment continuing to dwindle lower and spot prices close to (if not more than) 50% below their all-time high levels, it is unsurprising that volatility smiles continue to skew towards put options. BTC traders are still willing to pay a premium for protection against further downside spot moves, though a far smaller premium than the -30% skew towards puts that we saw earlier in the month.

In our ‘It's Different This Time?’ outlook report for 2026, we highlighted that real world assets (RWAs) “will be a key driver of value in 2026, continuing the progress made by regulated Trad-Fi institutions with stablecoin adoption in 2025”.

One of the latest signs of the TradFi convergence with DeFi (decentralized finance) was an announcement last week that BlackRock, the world’s largest asset manager, would be listing its USD Institutional Digital Liquidity Fund (BUIDL) on UniswapX.

The announcement also stated that the asset manager would be purchasing an undisclosed amount of Uniswap’s native UNI token (“BlackRock has also made a strategic investment within the Uniswap ecosystem.”)

BlackRock’s BUIDL fund is the firm’s first tokenized money market fund. Launched in March 2024 in collaboration with tokenization firm Securitize, it now holds just under $2B in assets under management. The fund is represented on-chain by the yield-bearing stablecoin, BUIDL, a stablecoin pegged to a value of $1. The fund generates yield for holders of the token by investing into short-term cash and cash equivalent assets, such as US Treasury bill. The daily accrued dividends are delivered as new tokens each month to BUIDL holders. Only pre-approved investors can own and transfer the token and the fund has an initial minimum investment of $5M. Prior to the collaboration with Uniswap, BUIDL was not listed on any exchange.

The integration with Uniswap however will now mean shares of BUIDL can be traded on-chain against the USDC stablecoin, providing a new source of liquidity for tokenholders and bridging the gap between TradFi and DeFi. According to Uniswap’s founder, Hayden Adams, “Enabling BUIDL on UniswapX with BlackRock and Securitize supercharges our mission by creating efficient markets, better liquidity, and faster settlement”.

The initial market impact was clear — a more than 20% jump in UNI’s spot price from $3.2 to $4, allowing it to buck the wider bearish trend across the rest of the crypto market. However, the strategic announcement was not enough to sustain momentum in UNI’s spot price and it now trades only slightly above pre-announcement levels. Perpetual swap funding rates did not meaningfully back the rally either — with eight-hourly rates actually turning negative during the short-lived spot rally.

Part of that might be due to the unique nature of the listing itself. According to the announcement, only “pre-qualified and whitelisted” existing holders of the BUIDL token can trade on UniswapX (the protocol’s RFQ-based AMM). Participants can “identify the most competitive quote from an ecosystem of whitelisted market participants known as subscribers (including Flowdesk, Tokka Labs, and Wintermute)”. That means BUIDL is not yet available for open, permissionless trading, in the same manner as most other tokens on Uniswap. It also means that liquidity provision is restricted to authorized market makers — unlike traditional cryptocurrency pairs on Uniswap which utilize community-provided liquidity pools.

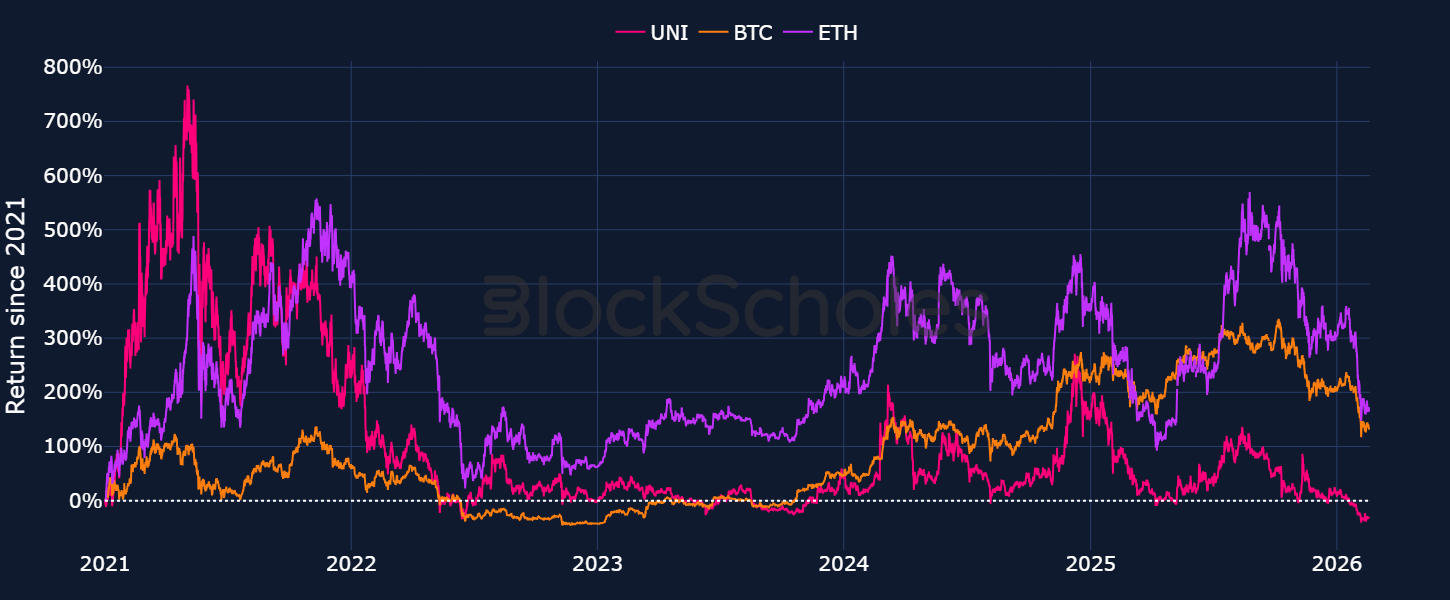

Zooming out, we can see that the UNI token has been on a steady decline ever since its May 2021 bull-market high of $44. In fact, while BTC and ETH have provided returns of 140% and 170% respectively since the start of 2021, UNI is down close to 30%. In last week’s edition we discussed the ‘Fat Protocol Thesis’, a thesis developed on the idea that base layer tokens would outperform application layer tokens.

Bitcoin’s hash rate (a measure of mining power in the BTC network) has historically moved in line with price cycles. Mining economics create a dynamic feedback loop: the cost to mine one bitcoin—driven by electricity prices, hardware efficiency, and network difficulty—is often described as a soft floor for price because sustained trading below production cost pressures higher-cost miners to shut off. Similarly, higher BTC spot prices mean miners are rewarded with higher dollar-denominated revenue, increasing the hashrate contributed to the network.

Late January 2026 saw a pronounced decline in Bitcoin’s hash rate, culminating in a flash hash crash on January 24. While the move occured close to the Feb 5 sell-off in BTC price, the drop in hash rate (typically a lagging indicator) occurred first, indicating that the disruption was not purely a function of mining economics.

Bitcoin mining remains geographically concentrated, with a small number of countries accounting for most of the global hash rate. The late-January flash crash coincided with a series of severe winter storms in Texas, highlighted in white below, during which Texas-based miners, voluntarily went offline to minimize grid stress during peak demand, with these shutdowns compensated through Electric Reliability Council of Texas (ERCOT) demand-response agreements. The United States contributes roughly 37.5% of global hash rate, indicating that if the storm was to blame, then close to 50% of the US hashrate was taken offline during this period. This has since recovered, but another multi-hazard storm is forecast for Feb 17–19, 2026.

A key focus is building a legal framework for perpetual derivatives, a major global crypto product still largely shut out of U.S. markets.

The listing adds to the growing range of crypto ETFs moving beyond BTC and ETH. It also comes as Grayscale’s Sui Staking ETF (GSUI) begins trading on NYSE Arca.

The iShares Staked Ethereum Trust, expected to trade as ETHB, was seeded with $100,000 and plans to stake the majority of its ether, typically 70% to 95%, with an estimated average staking yield of around 3% based on early 2026 benchmarks, not guaranteed.

The feature lets users speculate on which topics, memes and narratives will gain traction online, effectively enabling SocialFi traders to take long or short exposure to social-media virality.

The firm says demand is rising as gold hovers near record highs, with tokenised rails enabling 24/7 liquidity, faster settlement, real-time hedging and more flexible collateral use.

The Nasdaq-listed company partnered with Anchorage Digital and Solana lending protocol Kamino to enable loans backed by SOL that remain staked and held in segregated custody accounts at Anchorage, allowing holders to unlock liquidity without unstaking or selling and while still earning staking rewards.

Their request follows a separate House inquiry led by Rep. Ro Khanna, intensifying congressional scrutiny of the venture and its foreign ties.

The INJ Community BuyBack is gaining traction, combining accelerated token burns with a revenue-share mechanism for eligible participants.

Users commit INJ onchain, receive a pro-rata share of ecosystem revenue, and the committed tokens are permanently burned.

More than 6.9M INJ has been burned to date, with the initiative designed to further increase burn.

The pilot is designed to assess how tokenised sovereign debt could improve market infrastructure, including faster settlement and more efficient post-trade processes, while remaining separate from the government’s core debt management programme.

The Treasury is also engaging additional suppliers to support delivery of the required functionality, including on-chain settlement.

The product builds on Coinbase’s x402 protocol for automated crypto payments and complements its earlier AgentKit by offering a plug-and-play way to “give any agent a wallet.”

Aster Chain is intended to strengthen its on-chain infrastructure, offering dedicated support for its products, builder tools, and integrated fiat on- and off-ramps, following a testnet phase that drew more than 50,000 participants.

ESP is the native token of Espresso Network, launched as part of the project’s transition toward a permissionless proof-of-stake blockchain designed specifically to serve Ethereum rollups.

Espresso is positioned as infrastructure for the rollup ecosystem: rather than competing as an execution layer, it focuses on improving how Ethereum layer-2 networks coordinate, share security, and interoperate. Its core function is to provide fast, decentralised confirmations and transaction ordering that multiple rollups can rely on, helping reduce dependence on centralised sequencers and enabling smoother cross-rollup composability.

A central part of Espresso’s value proposition is faster finality for rollups: through its PoS validator set and HotShot BFT consensus, it can provide rollups with confirmations within seconds, rather than waiting for Ethereum’s 12+ minute finality.

At launch, Espresso Network set the total supply at 3.59B ESP and allocated 10% of this supply to a fully unlocked community airdrop. The airdrop was intended to reward early ecosystem participants and users of Espresso-integrated rollups, broaden token ownership, and decentralise governance from the outset.

It targeted over 1M eligible addresses and applied anti-Sybil checks to limit farming and wallet-splitting. These checks are designed to identify and filter clusters of wallets controlled by the same entity to prevent a single participant from claiming multiple allocations through duplicate or coordinated accounts. Beyond the community airdrop, the remaining supply was allocated to contributors and investors with multi-year vesting schedules, as well as to future airdrops, grants, ecosystem incentives, and foundation operations.

The Espresso Foundation also introduced a “Holder Score” framework. This model evaluates user engagement across more than 30 qualifying activities and prioritises sustained participation - particularly longer-term holding and staking - over short-term speculative behaviour. The objective is to mitigate typical launch volatility and encourage a more stable, conviction-driven ownership base that supports network security and ecosystem growth over time.

Espresso reported that it was finalising rollup blocks in roughly six seconds on average, compared with Ethereum’s 12-minute-plus finality window, and argued this gap had become a structural bottleneck as applications and liquidity spread across multiple rollups rather than remaining concentrated on a single chain.

Bybit converted the ESPUSDT Pre-Market Perpetual Contract into a standard perpetual contract on 12 Feb 2026, after which users could trade ESPUSDT with up to 50x leverage.

Open interest and trading volume data are sourced “as is” from the Bybit exchange platform API exclusively, and as such do not represent a comprehensive picture of the sum of trading activity across all derivatives markets or exchanges. The data visualized in this report consists of hourly and daily snapshots, recorded over the previous 30 days. Daily (hourly) snapshots of trade volume record the total sum of the notional value of trades recorded in the 24H (1 hour) period, beginning with the snapshot timestamp.

If not explicitly labeled as derived from another exchange, the input instrument prices to all derivatives analytics metrics in this report are sourced from the appropriate endpoints of Bybit’s public exchange platform API. In the event that data is labeled or referred to as representing the market on another exchange source, that data is sourced from the appropriate endpoint of each respective exchange’s public API.

Macroeconomic charts and data are sourced “as is” from the Bloomberg Terminal. Exchange data is sourced “as is” from publicly available exchange APIs. Block Scholes makes no claims about the veracity of public third-party data.

After acquisition of underlying-denominated raw data for open interest and trading volume on the Bybit exchange platform from Bybit’s API endpoint, equivalent dollar-denominated figures are calculated using the concurrent value of Block Scholes’s Spot Index for the relevant underlying asset.

Block Scholes’s Spot Index represents the aggregate Spot mid-price for a given currency across the top five CEXs by volume (with USD-quoted markets). It considers the proportion of total volume in the instrument on the exchange, as well as the deviation of a data point from those on other exchanges.

Futures prices are used for Block Scholes’s futures-implied yields calculation services in order to derive the constant-tenor annualized yields displayed in the Futures section of this report.

Options prices are used for Block Scholes’s implied volatility calculation services in order to calibrate volatility surfaces, from which all derivatives volatility analytics displayed in the BTC Options and ETH Options sections of this report are calculated. Volatility smiles are constructed by calibrating to mid-market prices observed in Bybit options markets. As part of the calibration process, prices go through rigorous filtration and cleaning steps, which ensures that the resulting volatility surface is arbitrage-free and has exceptional fit to the market observables.

.jpg)

.jpg)