Thahbib Rahman

Research Analyst

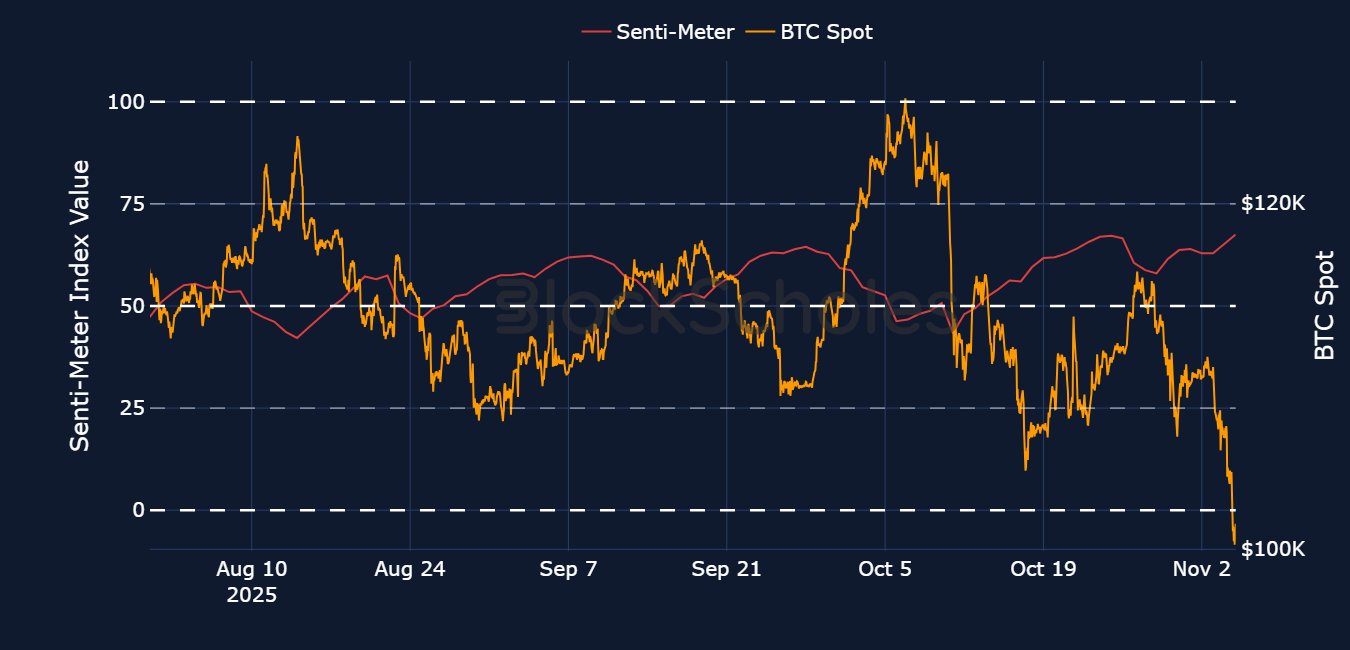

A revisit to $100K for BTC has further diminished sentiment in derivatives markets. Open interest in perpetual futures contracts remains low, with very few signs of traders showing any willingness to reenter positions that may have been closed out during the $19B liquidation unwind in October. However, the lack of a major drop in perp open interest suggests that the most recent spot market crash was driven by the selling of spot holdings, rather than a liquidation cascade, such as back in October. On the other hand, open interest in BTC and ETH options still remains resilient, suggesting an increased use of options contracts in order to gain spot exposure.

A revisit to $100K for BTC has further diminished sentiment in derivatives markets. Open interest in perpetual futures contracts remains low, with very few signs of traders showing any willingness to reenter positions that may have been closed out during the $19B liquidation unwind in October. However, the lack of a major drop in perp open interest suggests that the most recent spot market crash was driven by the selling of spot holdings, rather than a liquidation cascade, such as back in October. On the other hand, open interest in BTC and ETH options still remains resilient, suggesting an increased use of options contracts in order to gain spot exposure.

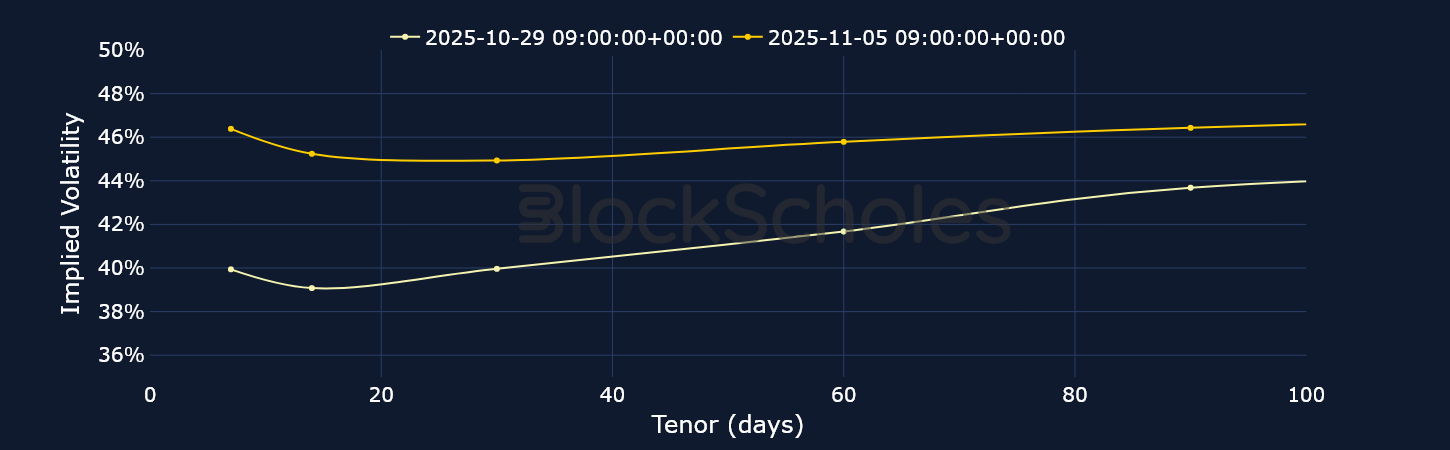

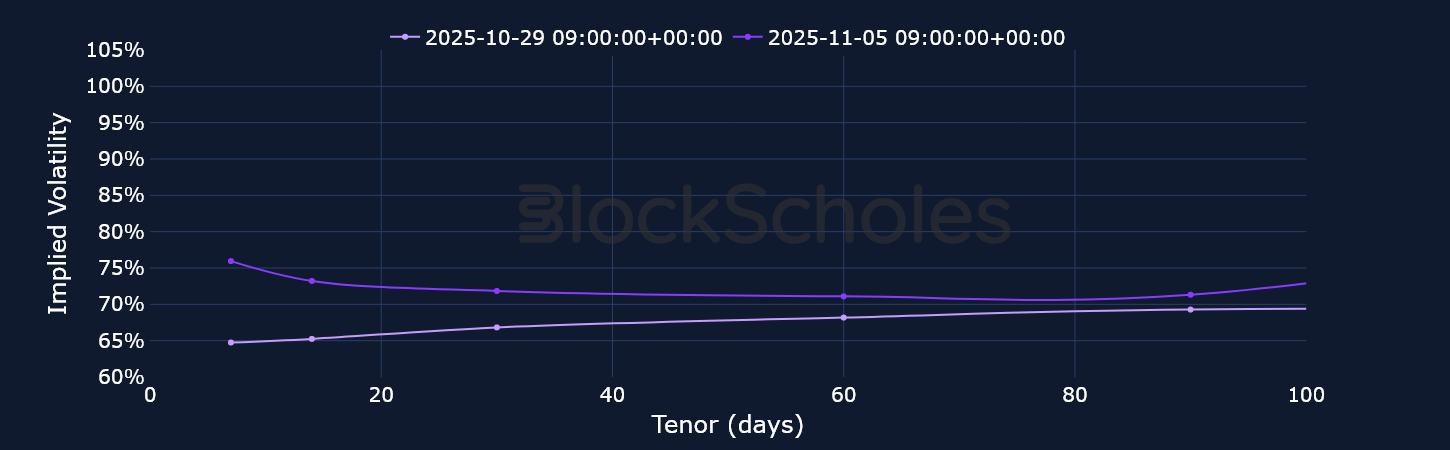

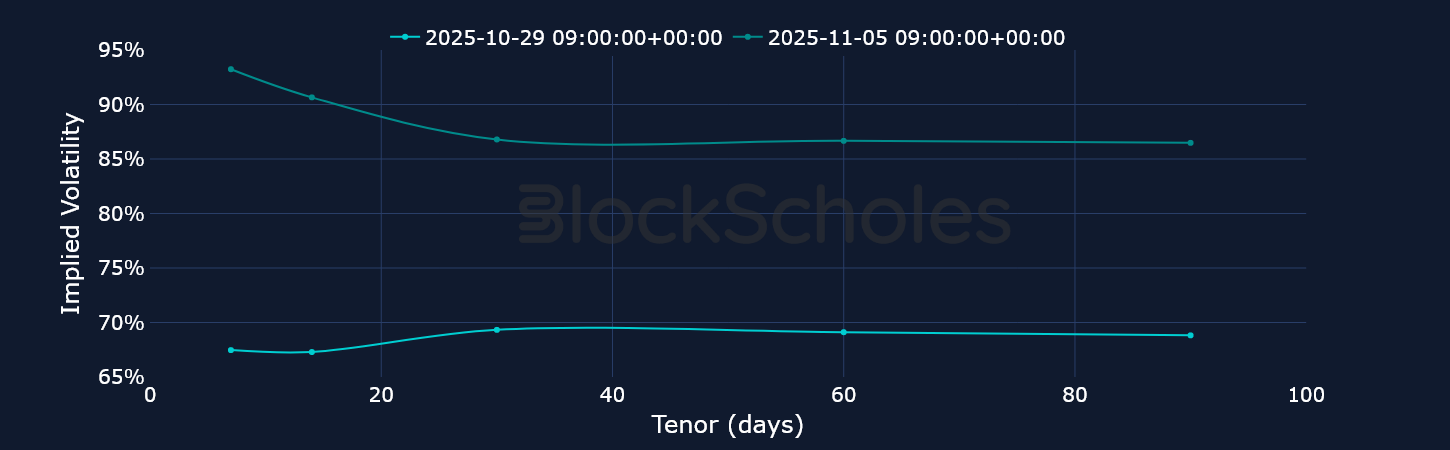

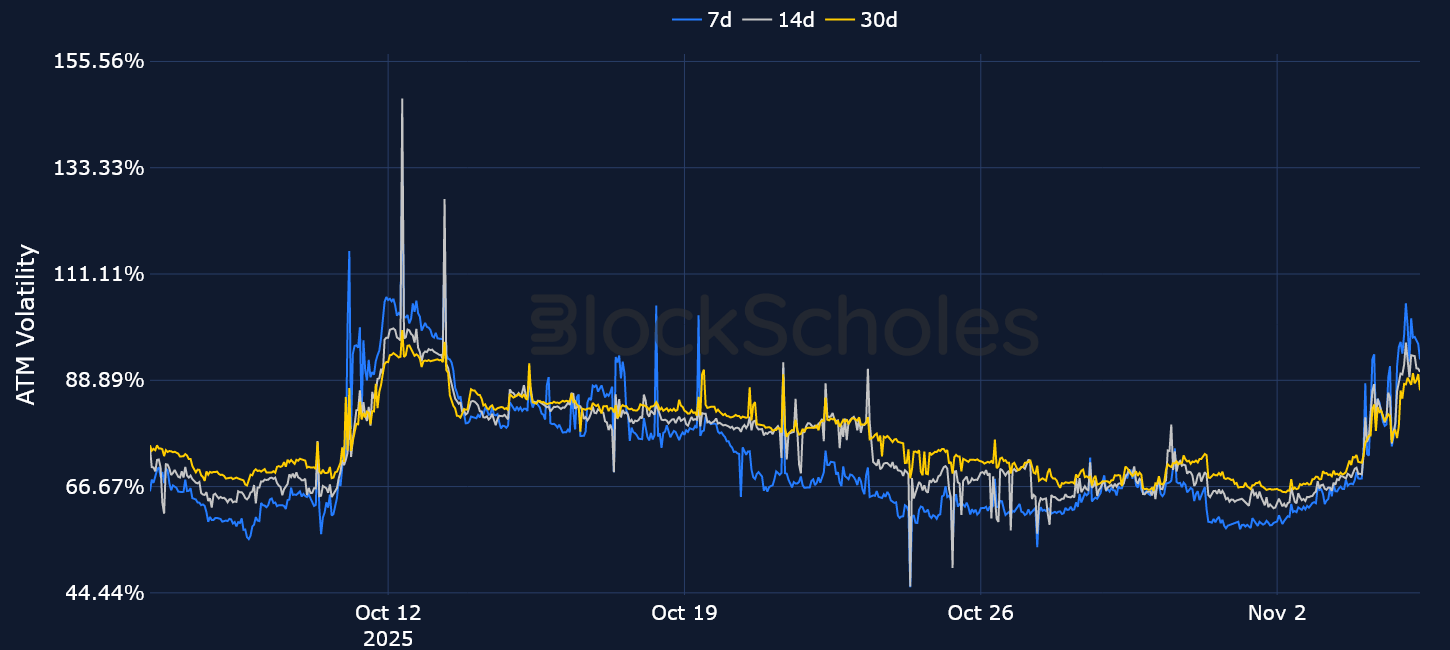

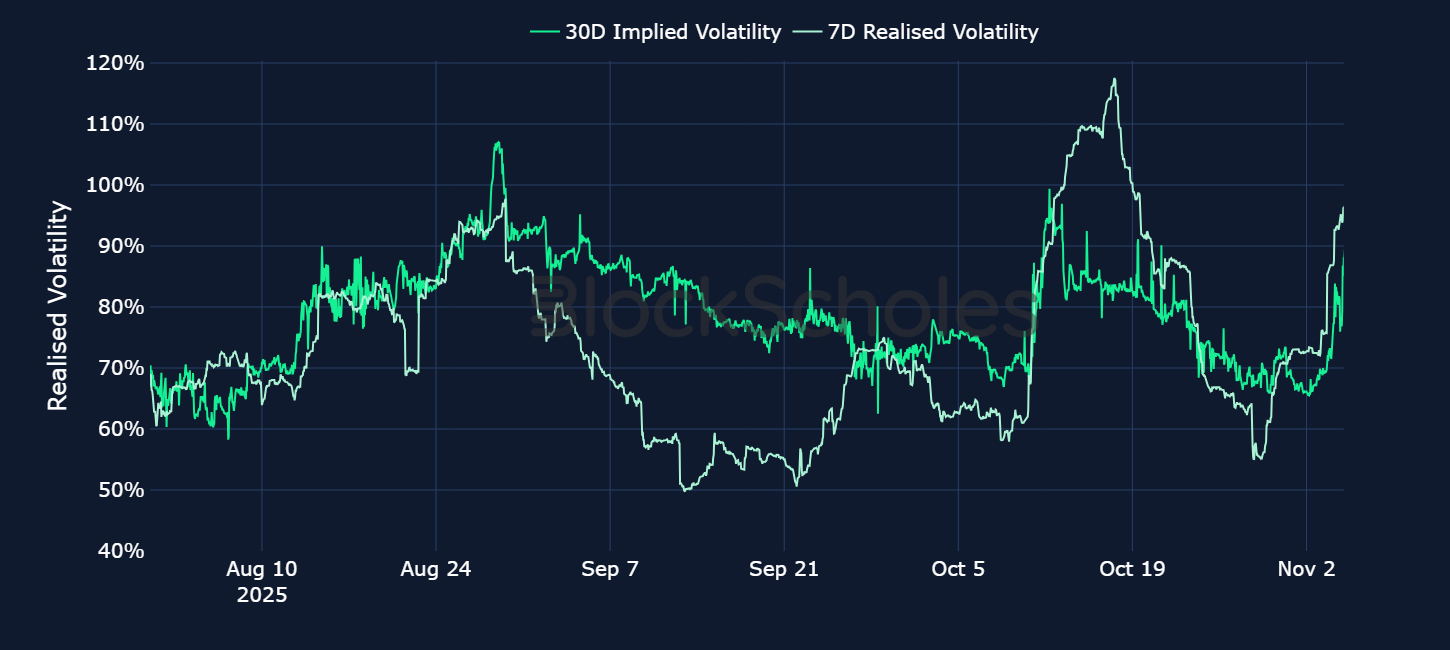

BTC fell to $99K earlier this week, while ETH fell by double digits, wiping out all of its gains for the year. As such, delivered volatility for both assets surged higher and, with it, brought about a blowout in the front end of the term structure of volatility. This means that both BTC and ETH volatility term structures are currently inverted, with short-tenor optionality trading at a premium.

Perpetuals: Open interest remains as flat as it has been over the past two weeks, and still far from a recovery to pre-October 10 levels. Meanwhile, funding rates across tokens are trading at mixed levels.

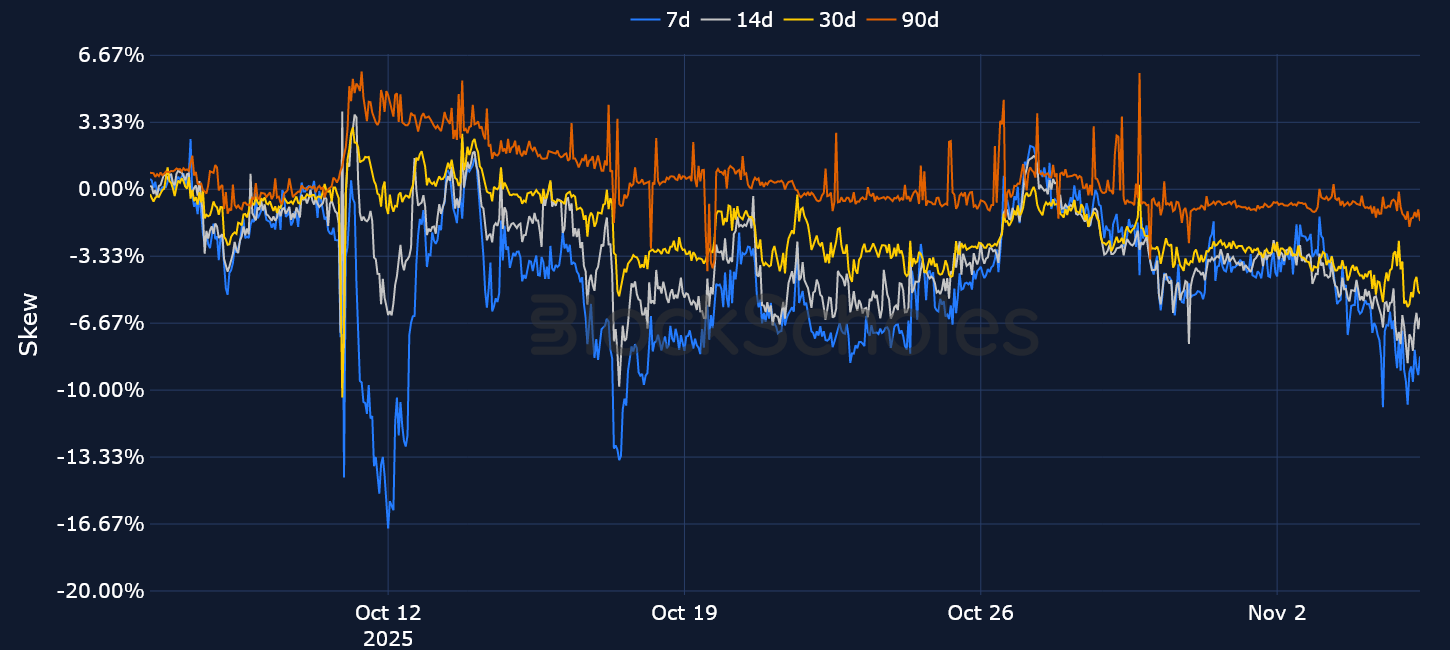

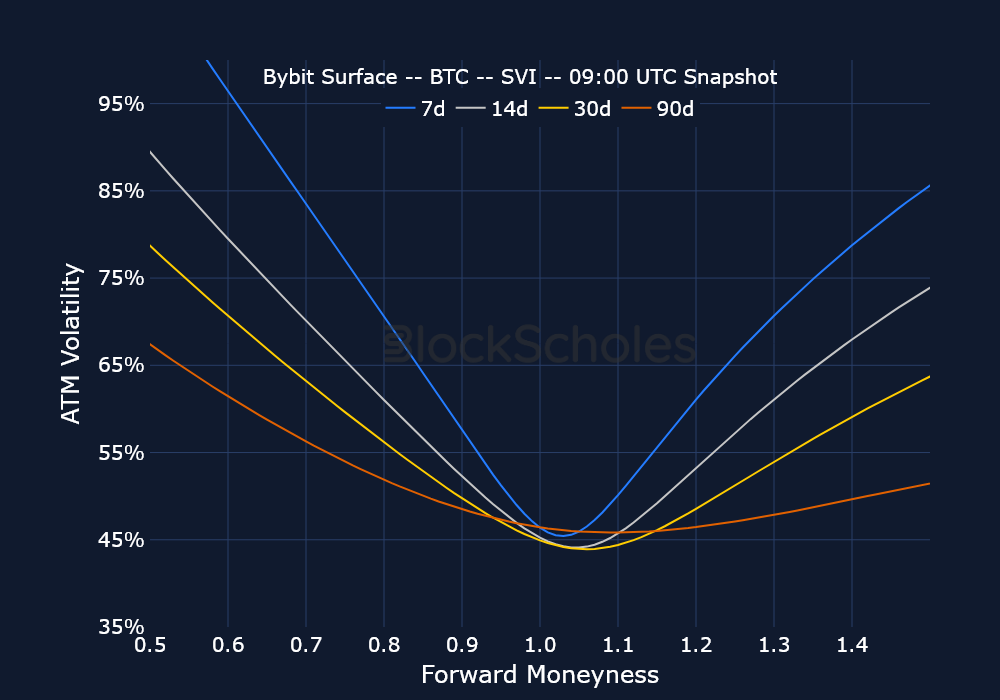

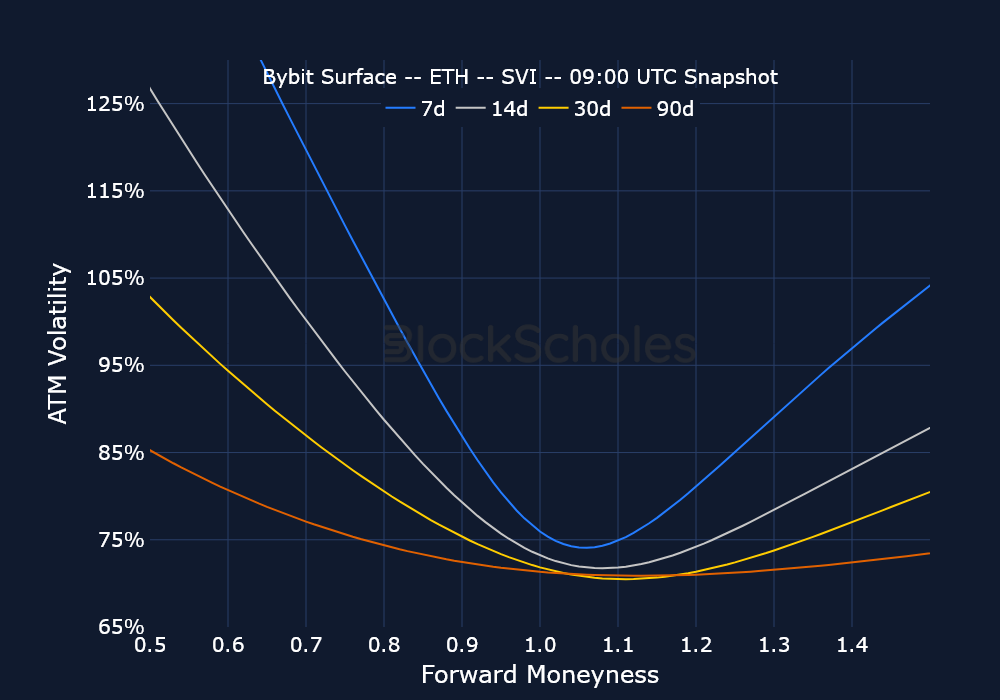

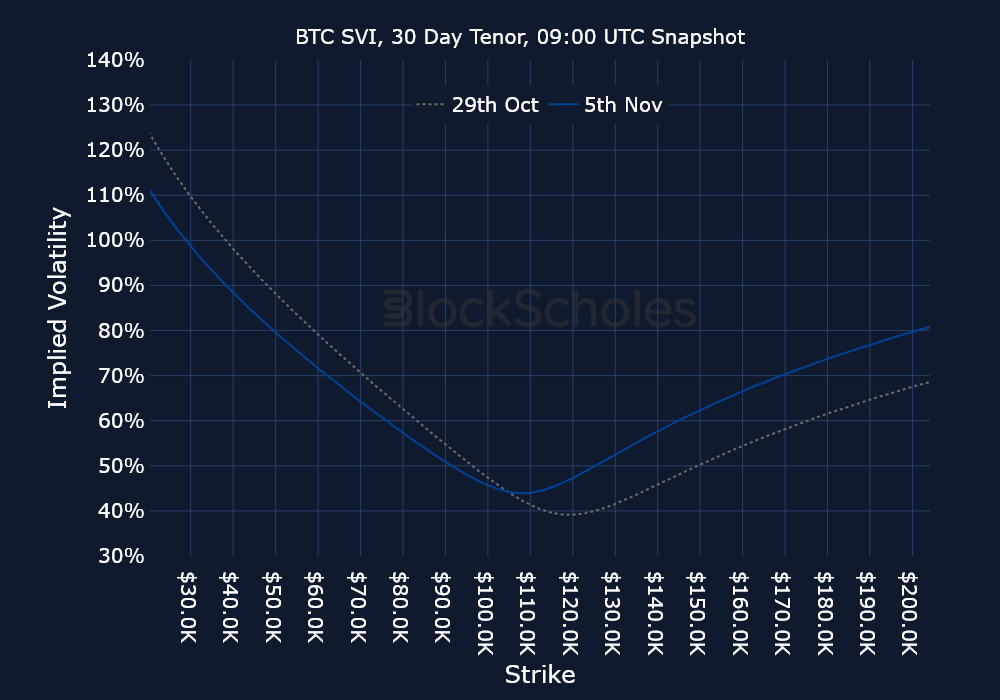

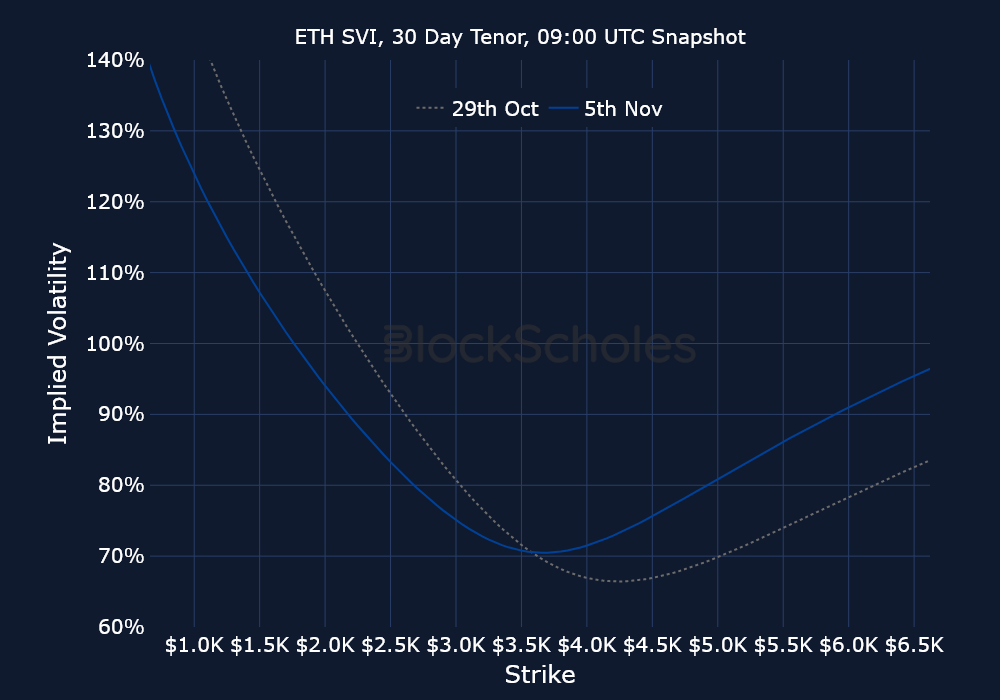

Options: BTC and ETH volatility smile skews tilted further toward OTM put options during the most recent spot price whipsaw, while ATM implied volatility across different tenors jumped higher. The inverted term structure of volatility suggests that traders are bracing for heightened volatility in the near term, even more than they anticipate over longer horizons.

Block Scholes’s Senti-Meter Index aggregates the funding rate, future-implied yield and volatility smile skew into a single expression of sentiment in derivatives markets. See more in the methodology article here.

In early October 2025, we highlighted the tremendous growth in ZCash (ZEC), a privacy token launched in 2016 that focuses on zero-knowledge (ZK) proof technology. In that report, we highlighted the growth in ZCash from $40 to upward of $95. That rally has shown no signs of slowing down, and since then, ZCash has more than quadrupled in price and is now trading above $400.

Along with ZEC, a slew of privacy-related tokens have begun to rally more recently, including FIRO and DASH. Firo (formerly known as Zcoin) is another privacy-focused token that deploys ZK proofs to ensure anonymous transactions. However, it takes it a step further by allowing users to actually burn tokens and redeem them for new tokens with no transaction history. That adds an additional element to the privacy meta, as the majority of tokens focus on obfuscating transactions, rather than destroying the tokens linked to the transaction. FIRO has shown incredible strength, too: while the broader altcoin market has dropped by double digits in the past week, FIRO is up 239% in the past three months and 30% over the past seven days.

One reason that’s been advocated for the recent rally in privacy-related tokens is the increasing institutionalization of crypto assets, including BTC and ETH, through the use of Spot ETFs or digital asset treasury (DAT) firms. Privacy tokens, therefore, provide a way for some of the original advocates of crypto and blockchain technology to maintain their agenda. This has also occurred alongside an explosion in Google searches for privacy-related crypto tokens.

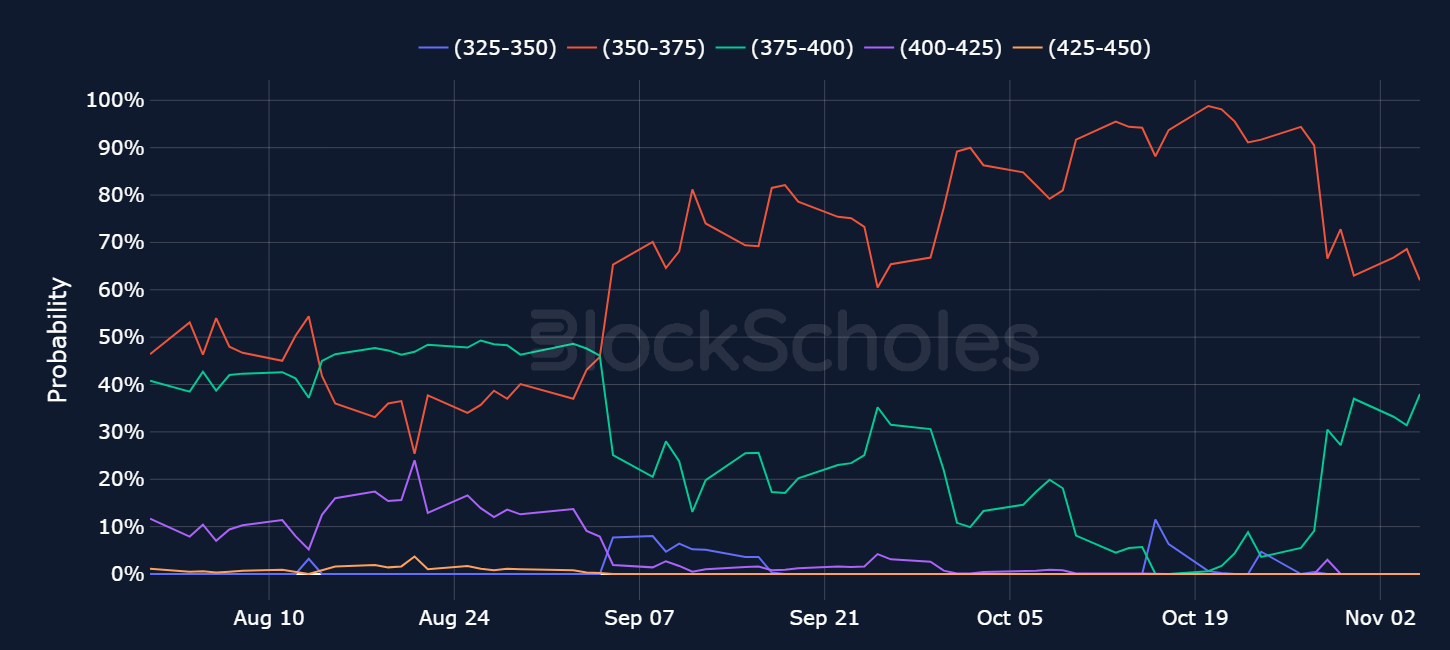

December Rate Cut Expectations — Through October the market had priced in a 25bps rate cut for the Dec 10, 2025 meeting at 98.8% probability, from the current rate of 375-400. Since, expectations of no cut have risen, now nearing 40% probability.

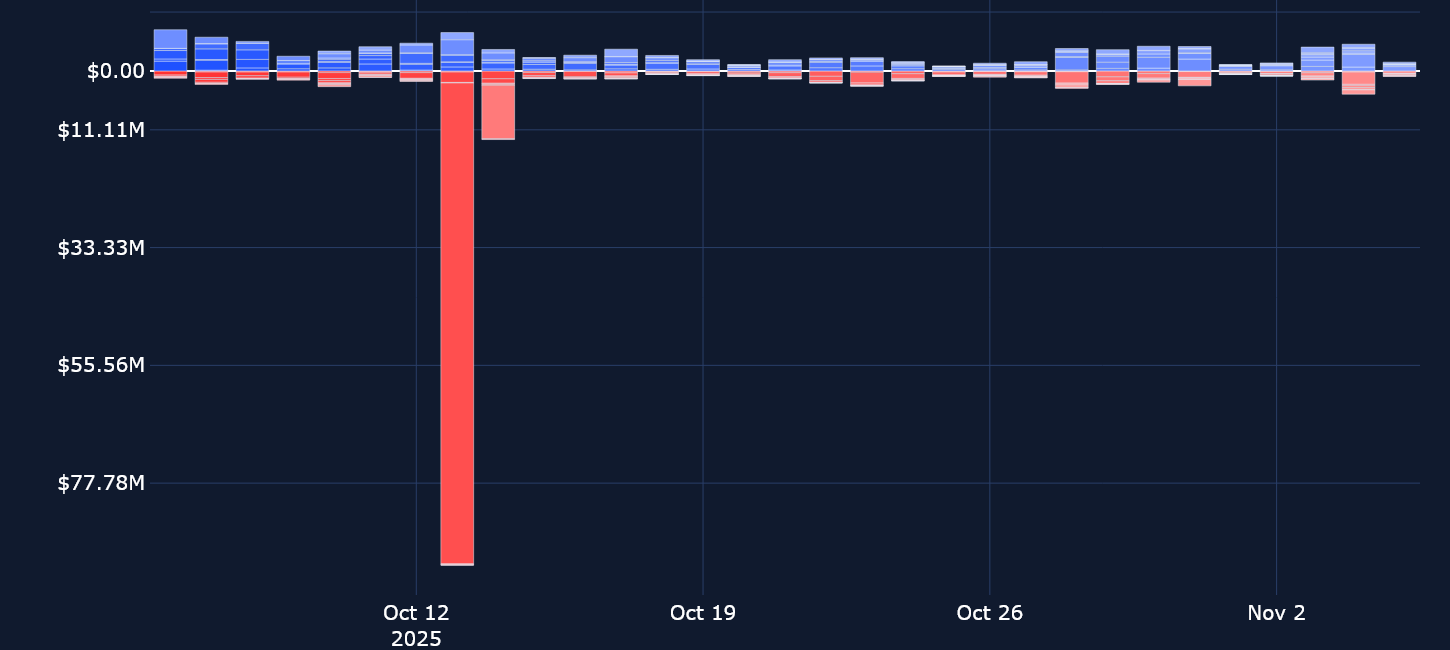

After a long period of sideways trading between $105K and $115K, BTC fell through the $105K level earlier this week. That then led to a swift retest of $99K, a level BTC hadn’t traded at since June 2025. As showcased in the chart below, however, this week’s market crash in crypto prices appears more to be a result of spot holders selling their positions, rather than a liquidation-driven cascade, as was the case on Oct 10, 2025, when more than $6B of long and short positions in Bybit perpetual contracts were wiped out. Instead, this week, we see a much smaller drop in the notional size of open interest of $500M.

As we commented last week, perpetual futures traders on Bybit are showing little appetite to reopen positions that were closed during the October market crash. Open interest in Bitcoin futures remains far below pre-crash levels, and even with funding costs remaining somewhat positive for some tokens, traders continue to show little willingness to reenter the market. The lack of retail participation in leverage trading — alongside the start of what could turn into a trend of DAT firms selling crypto holdings — is something to pay close attention to. In the past ten days alone, Sequans Communications sold 970 BTC from its digital asset treasury, while ETHZilla sold $40M worth of Ether — though that was to buy back its own shares, and not yet quite a panic-driven sale.

After funding rates for most tokens turned negative following the Oct 10, 2025 tariff announcements, this week we see more variation in funding rates across assets. BTC funding rates briefly turned negative on Nov 4, 2025, as the spot price fell to its lowest level since June 2025. However, funding rates quickly rebounded and now remain at modestly positive levels.

ETH funding rates have switched bearish for a more extended period, and are now only slightly above neutral levels. The drop to negative levels suggests traders were willing to pay a premium to hold their short leveraged positions in ETH, betting on further downside in an asset that has already fallen 30% in the past 30 days alone. ETH has now pared back all of its year-to-date gains, and is currently trading less than half a percentage point above the level with which it entered 2025.

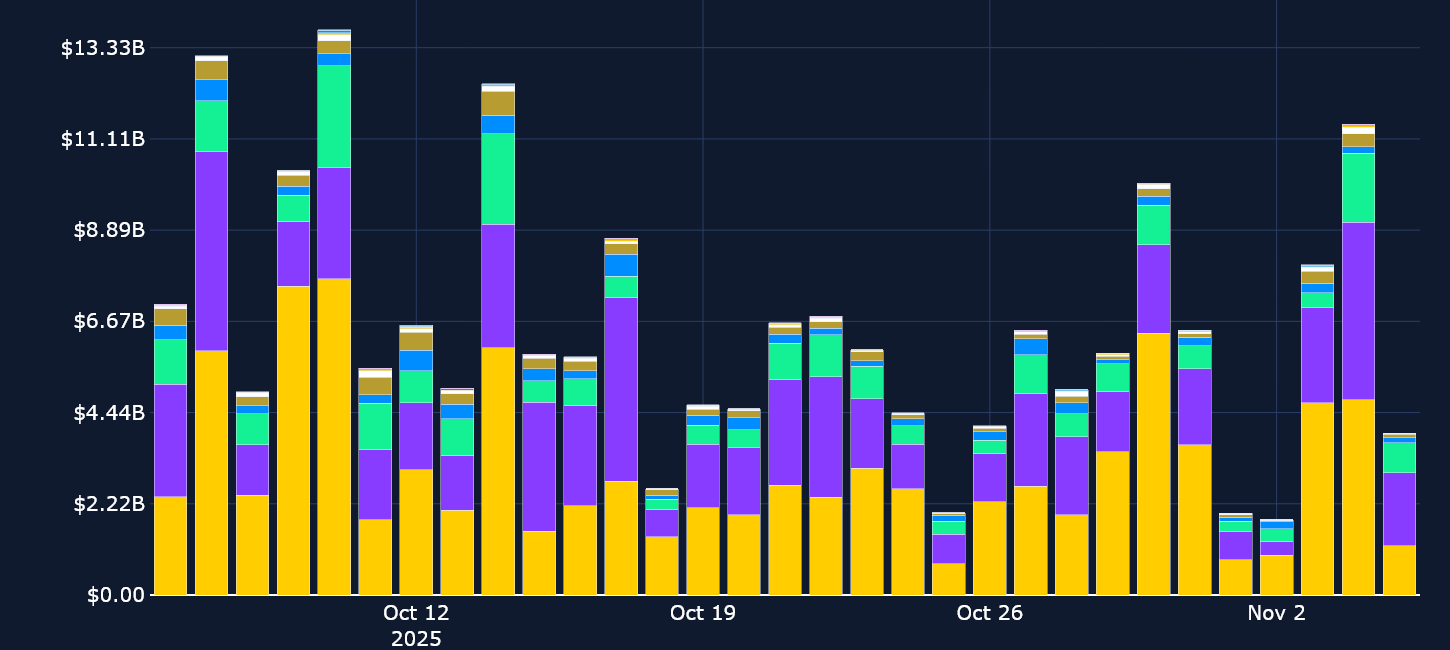

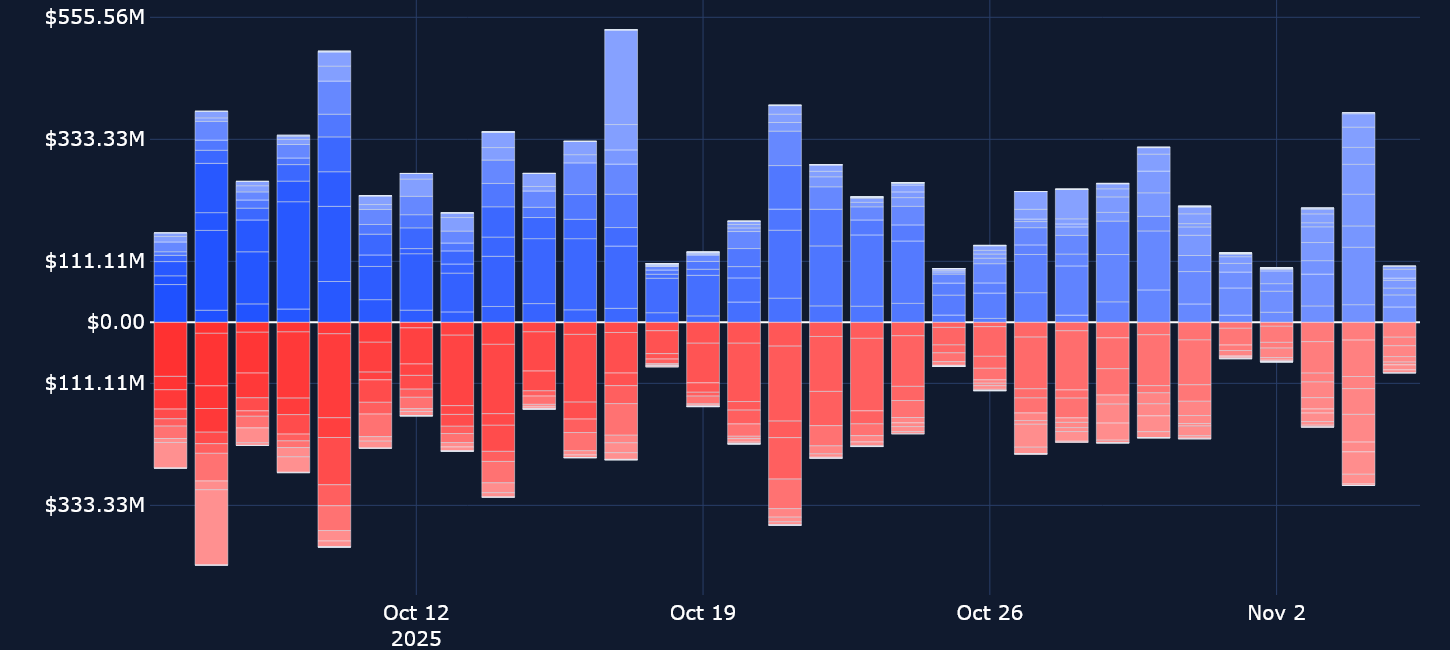

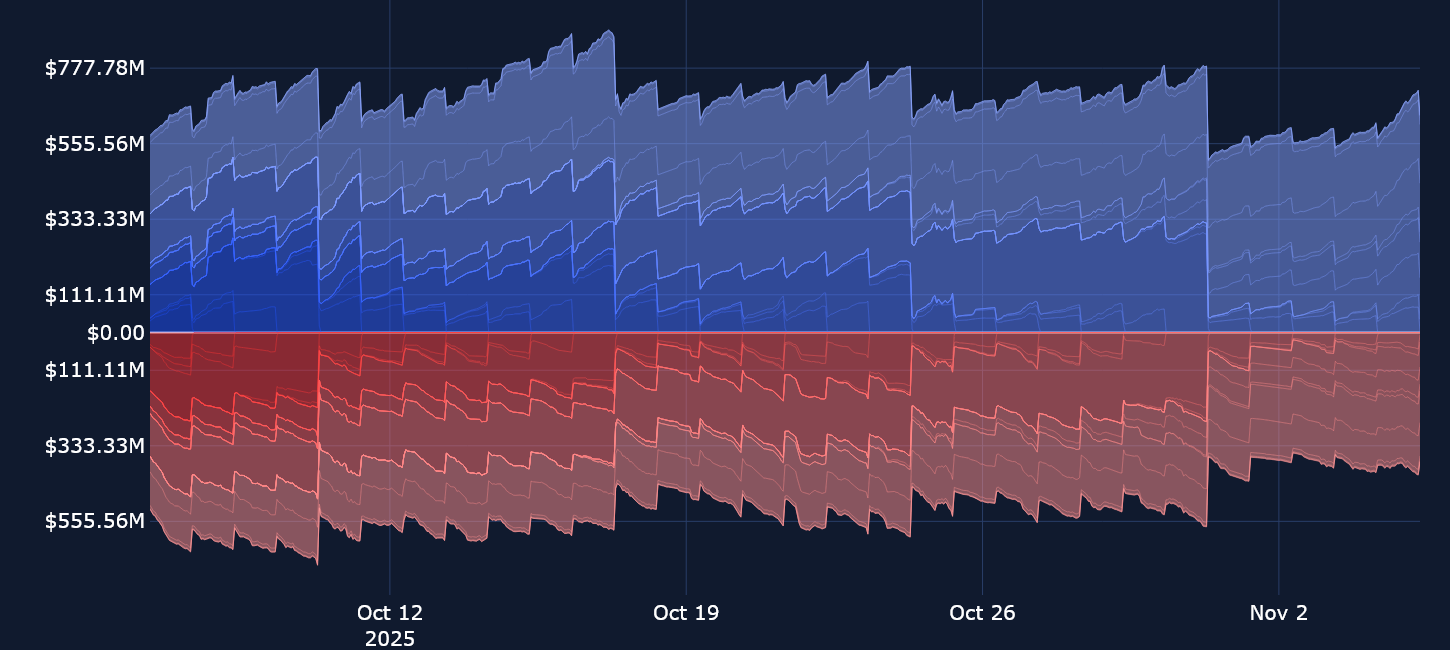

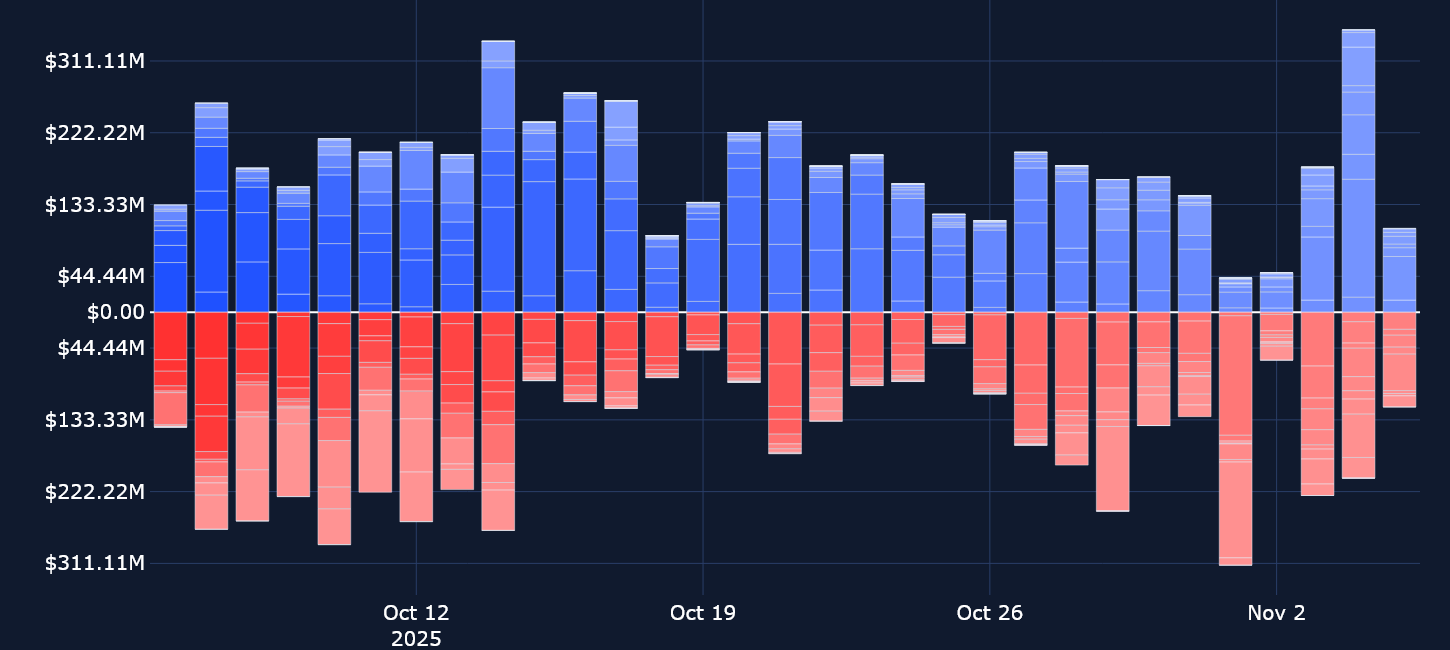

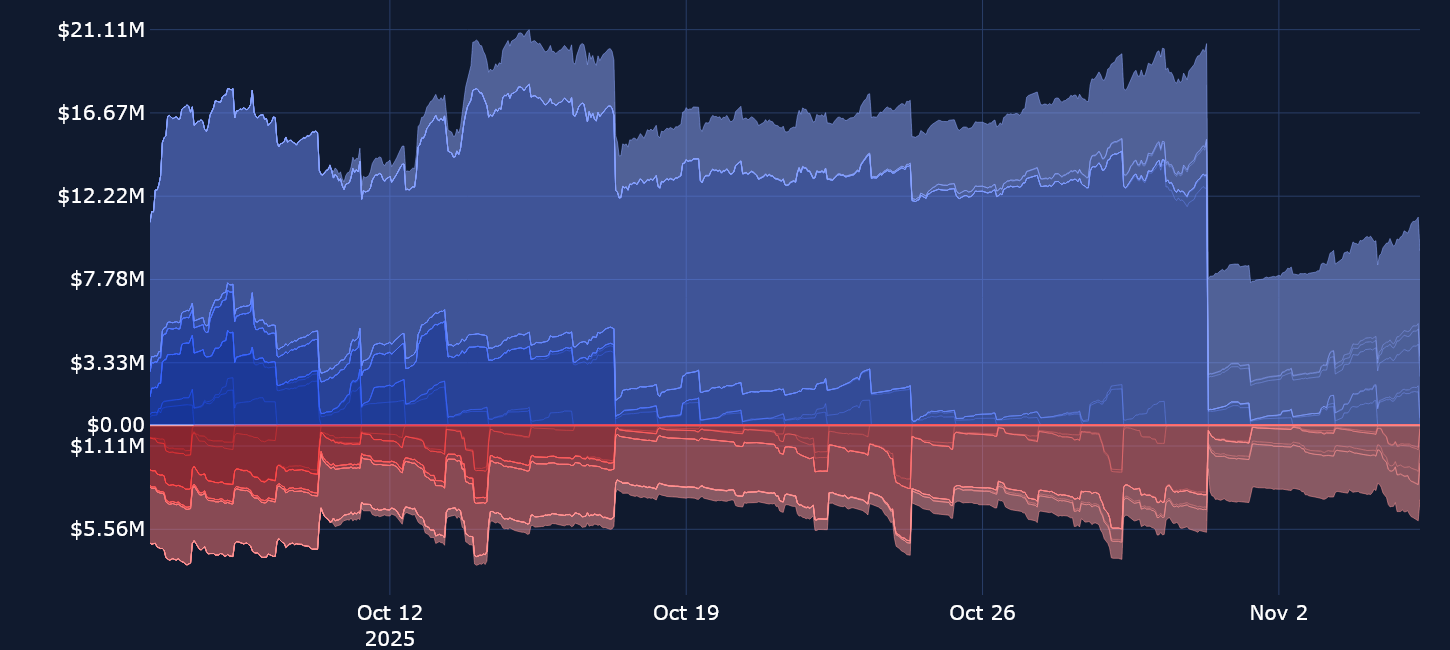

Open interest has rebuilt at a relatively fast pace since the end of the October expiration, meaning traders have wasted little time to recapture their exposure to BTC after their positions were cleared. Therefore, similar to last week’s report, we see continued signs of traders choosing options contracts over perpetual futures contracts to hedge against further downside moves, or to speculate on future price moves. On Nov 4, 2025, options volumes also reached their highest levels since Oct 21, 2025, as BTC plunged more than 6%, part of a wider risk-asset sell-off across US equities and other markets.

That sell-off resulted in another front-end blowout of the term structure, as short-tenor volatility jumped nearly 10 percentage points above 50%. This suggests that traders continue to expect extreme volatility in the short term, more so than levels expected over a longer horizon. Such fear of volatility coincides with a further weakening in bearish sentiment in volatility smiles, which have skewed even more toward out-of-the-money puts — telltale signs of a cautious and fearful market.

BYBIT BTC OPTIONS OPEN INTEREST

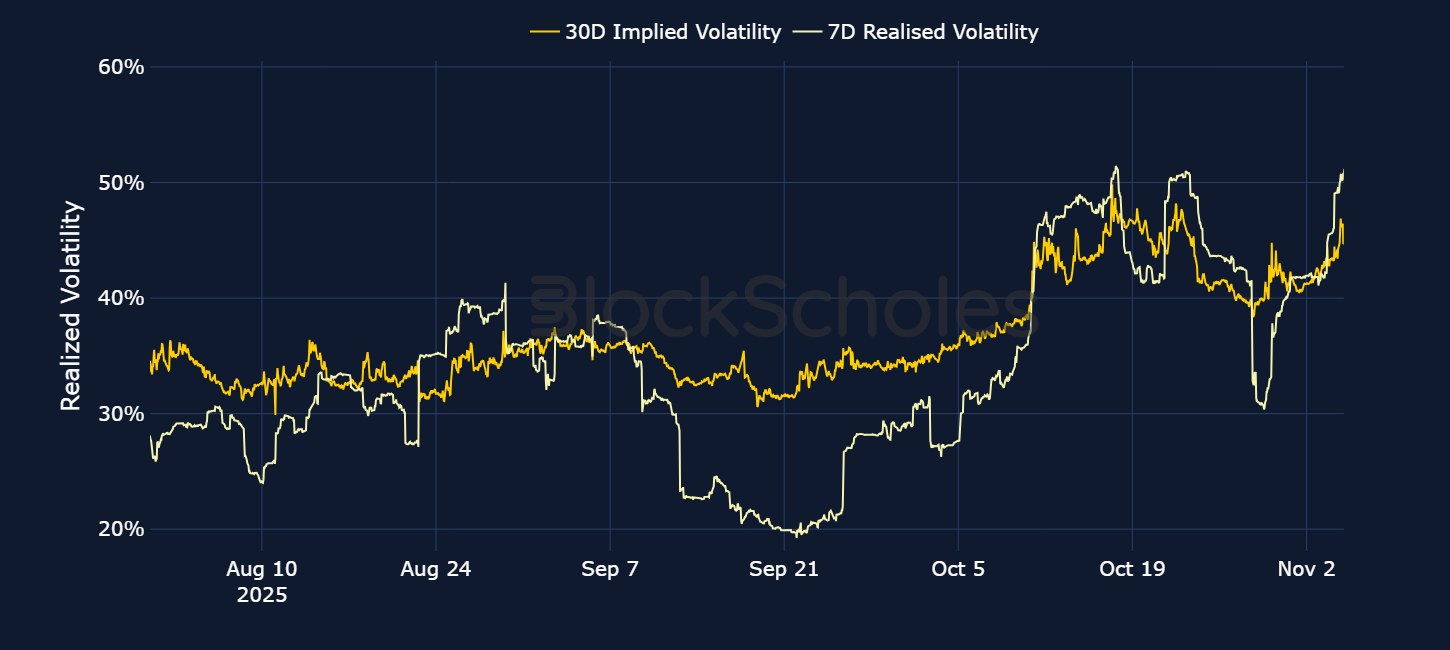

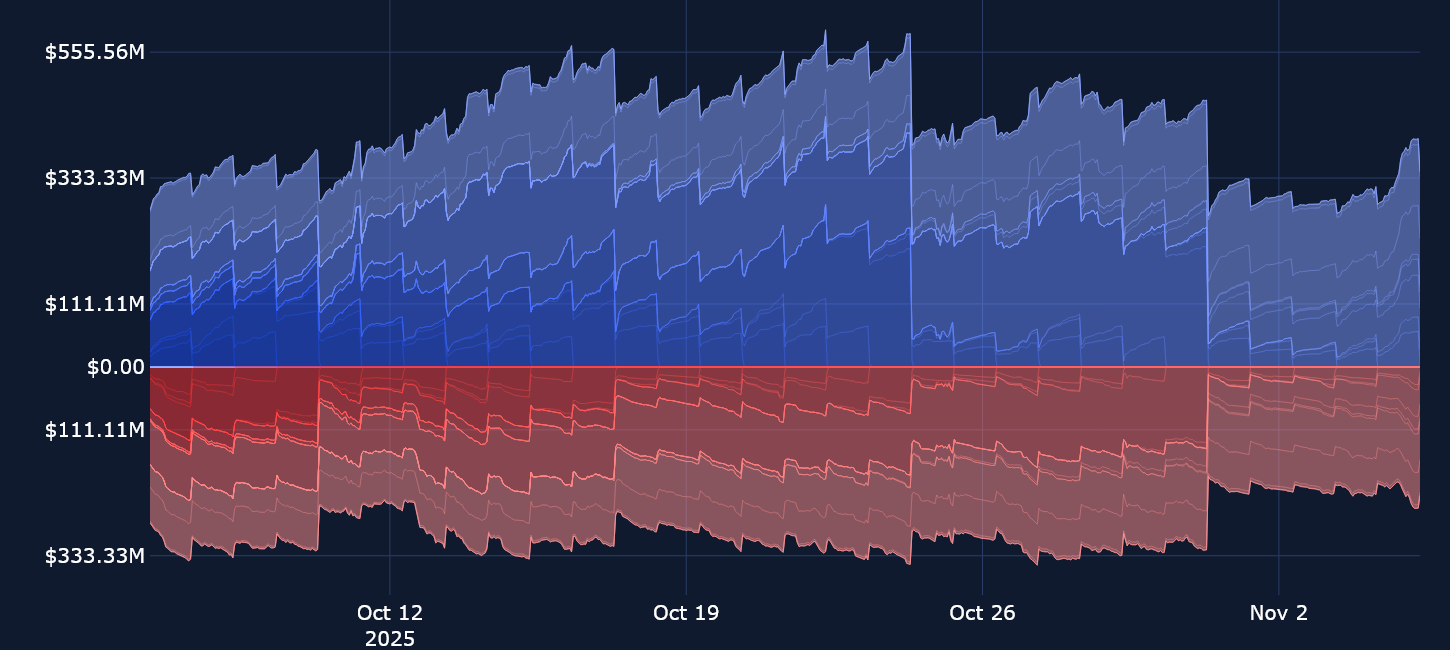

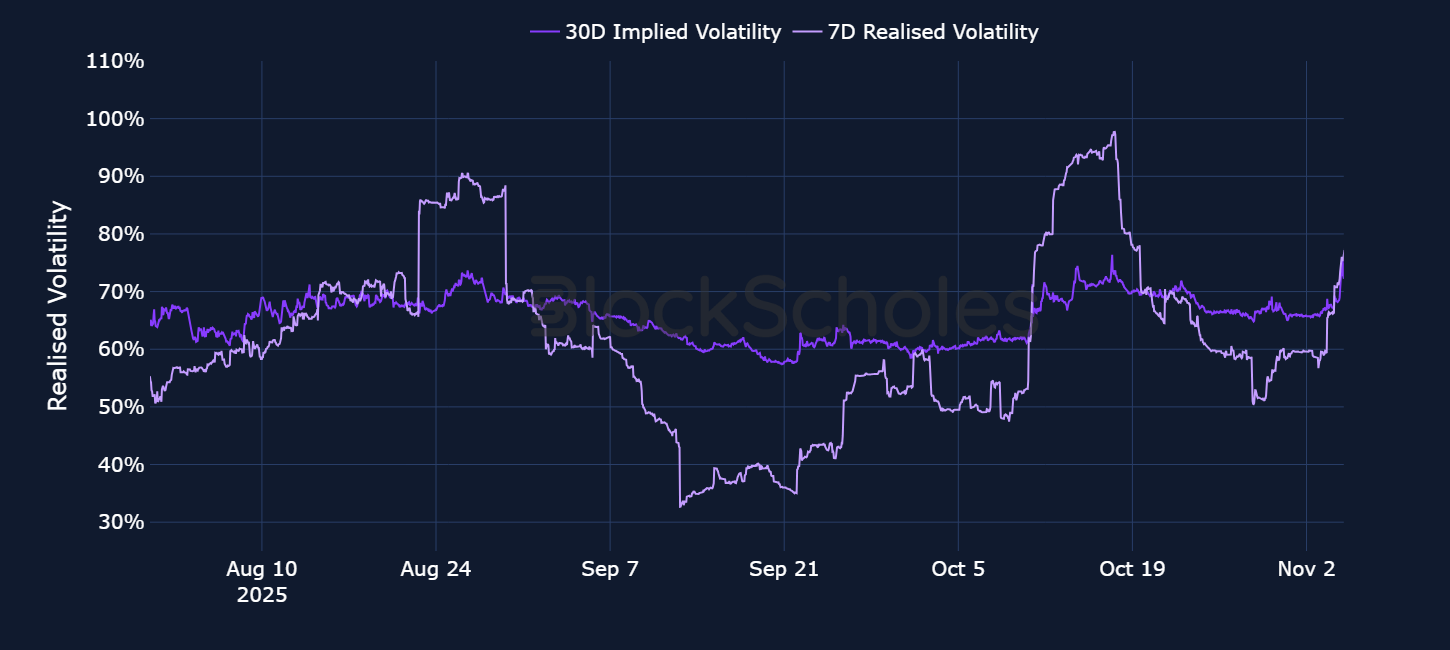

Open interest in ETH contracts has seen a slight pickup again following the October expiration, though it remains somewhat subdued. As we’ve come to expect, ATM volatility for ETH options reacted more sensitively to the spot price sell-off in crypto assets this week, relative to BTC options. Front-end volatility surged to 86%, firmly inverting ETH’s volatility term structure. The move in implied volatility — which is a measure of forward-looking volatility expectations — makes sense, given that delivered volatility over the past seven days shot up equally this week. While BTC’s realized volatility overtook the volatility implied by the price of 30-day BTC options for ETH, the two are now trading at the same level.

The recent crash in crypto prices has seen the total market cap of all crypto assets drop to $3.5T — with ETH taking a brunt of that hit. Its price dropped double digits on Nov 4, 2025, falling through a number of support zones and reaching as low as $3,050. The depth of the sell-off now means ETH has pared back all of its gains for the year, and is currently trading only 0.5% higher than its level on Jan 1, 2025.

While the gain in open interest following the end of October was a sign that traders were at least showing some signs of reentering options markets for ETH and BTC, the same cannot be said for SOL traders, as notional open interest is now below $12M for call options. SOL has dropped more than 15% in the past five days, and is firmly in the negative when it comes to year-to-date returns (−15.8%). Volumes for both call and put options also continue their signs of fatigue, having been flat for the past two weeks.

The breakout in implied volatility for SOL options is unsurprising, given that realized volatility surged this past week, jumping from 55% to 96% within the space of three days.

The past month in crypto has provided spot holders with little relief. After two agonizing weeks of sideways trading — following a huge liquidation event from which crypto spot, perp and options traders have clearly failed to recover — markets received a further kick lower earlier this week. For the first time since Jun 22, 2025, BTC retested $100K, actually falling below it to $99K. That marks a 20% drop from its all-time high. Unsurprisingly, options traders turned further bearish. This is apparent when looking at the evolution of the 25-delta put-call skew ratio, which measures the difference between the IV of a 25-delta call minus a 25-delta put. Values below zero are a clear indication of the preference to hedge against further downside price action, and not yet a sign of any optimistic hope of a bounce higher.

The same story is seen with ETH, the only difference being that ETH traders are pricing in an even more bearish outcome, as the premium for 7-day put options is trading at nearly a ten volatility point excess to similar dated calls.

Open interest and trading volume data are sourced “as is” from the Bybit exchange platform API exclusively, and as such do not represent a comprehensive picture of the sum of trading activity across all derivatives markets or exchanges. The data visualized in this report consists of hourly and daily snapshots, recorded over the previous 30 days. Daily (hourly) snapshots of trade volume record the total sum of the notional value of trades recorded in the 24H (1 hour) period, beginning with the snapshot timestamp.

If not explicitly labeled as derived from another exchange, the input instrument prices to all derivatives analytics metrics in this report are sourced from the appropriate endpoints of Bybit’s public exchange platform API. In the event that data is labeled or referred to as representing the market on another exchange source, that data is sourced from the appropriate endpoint of each respective exchange’s public API.

Macroeconomic charts and data are sourced “as is” from the Bloomberg Terminal. Exchange data is sourced “as is” from publicly available exchange APIs. Block Scholes makes no claims about the veracity of public third-party data.

After acquisition of underlying-denominated raw data for open interest and trading volume on the Bybit exchange platform from Bybit’s API endpoint, equivalent dollar-denominated figures are calculated using the concurrent value of Block Scholes’s Spot Index for the relevant underlying asset.

Block Scholes’s Spot Index represents the aggregate Spot mid-price for a given currency across the top five CEXs by volume (with USD-quoted markets). It considers the proportion of total volume in the instrument on the exchange, as well as the deviation of a data point from those on other exchanges.

Futures prices are used for Block Scholes’s futures-implied yields calculation services in order to derive the constant-tenor annualized yields displayed in the Futures section of this report.

Options prices are used for Block Scholes’s implied volatility calculation services in order to calibrate volatility surfaces, from which all derivatives volatility analytics displayed in the BTC Options and ETH Options sections of this report are calculated. Volatility smiles are constructed by calibrating to mid-market prices observed in Bybit options markets. As part of the calibration process, prices go through rigorous filtration and cleaning steps, which ensures that the resulting volatility surface is arbitrage-free and has exceptional fit to the market observables.

.jpg)

.jpg)