Thahbib Rahman

Research Analyst

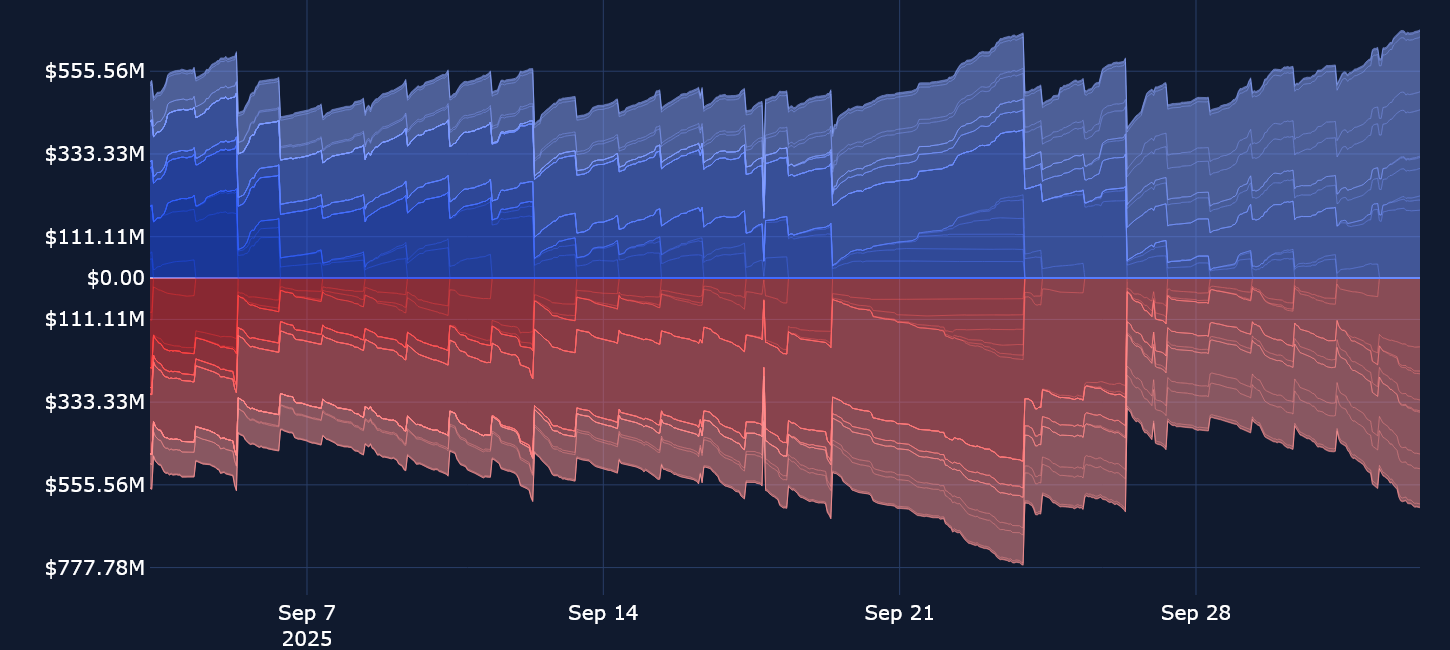

A recent major liquidation event beginning Sep 22, 2025 dropped the levels of open interest in Bybit perpetual swap contracts. That resulted in the notional value of outstanding contracts falling from the all-time highs reached in the run-up to the Federal Reserve’s September FOMC meeting. The decline coincided with a major slump in spot prices, in which BTC lost a key support level and dropped below $108K, while ETH plunged through the $4,000 level. Since those local lows, crypto asset spot prices have begun to recover, with BTC now trading back above $118K and ETH at $4,400. That’s also despite a US government shutdown, which has (as yet) had seemingly little impact on spot or derivatives markets.

A recent major liquidation event beginning Sep 22, 2025 dropped the levels of open interest in Bybit perpetual swap contracts. That resulted in the notional value of outstanding contracts falling from the all-time highs reached in the run-up to the Federal Reserve’s September FOMC meeting. The decline coincided with a major slump in spot prices, in which BTC lost a key support level and dropped below $108K, while ETH plunged through the $4,000 level. Since those local lows, crypto asset spot prices have begun to recover, with BTC now trading back above $118K and ETH at $4,400. That’s also despite a US government shutdown, which has (as yet) had seemingly little impact on spot or derivatives markets.

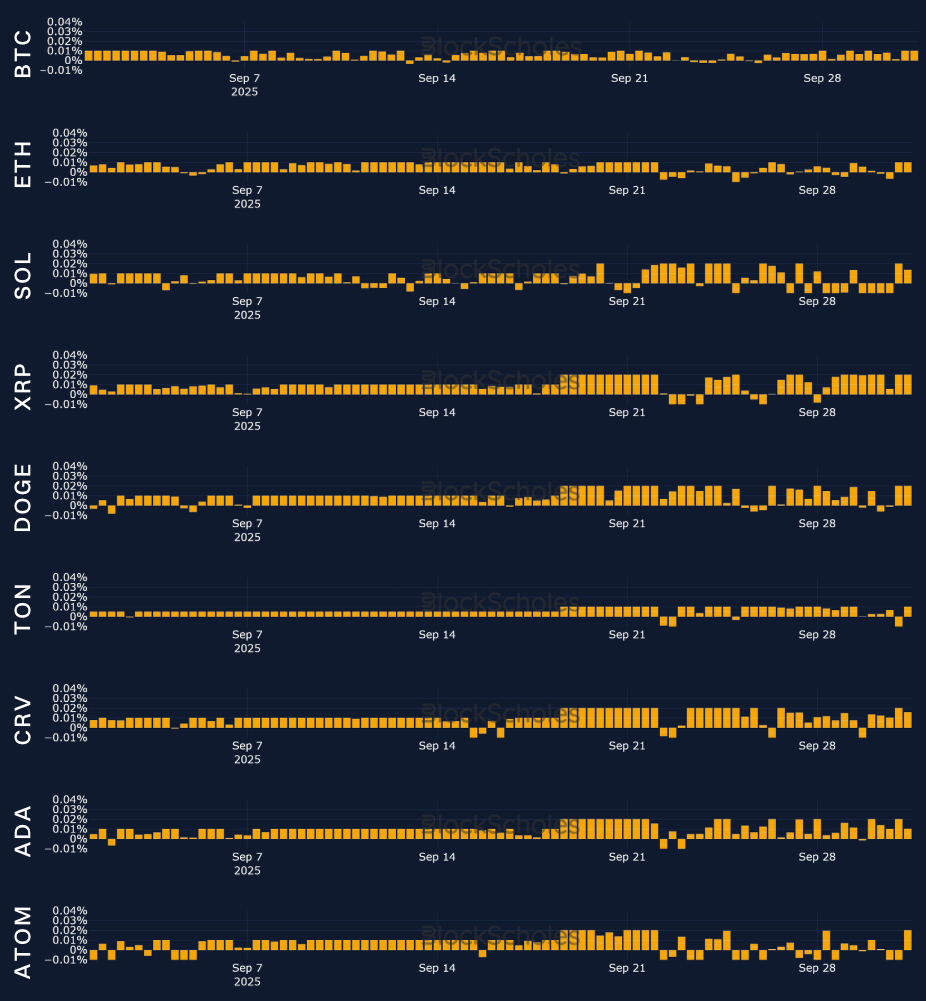

Perpetuals: Open interest in perpetuals has dropped from its all-time high levels, and funding rates for altcoins finally hit a wall. After resisting the bearish sentiment priced in by options markets, altcoin funding rates for ETH, SOL and XRP briefly dropped negative over the past week, though still remaining neutral-to-positive for BTC.

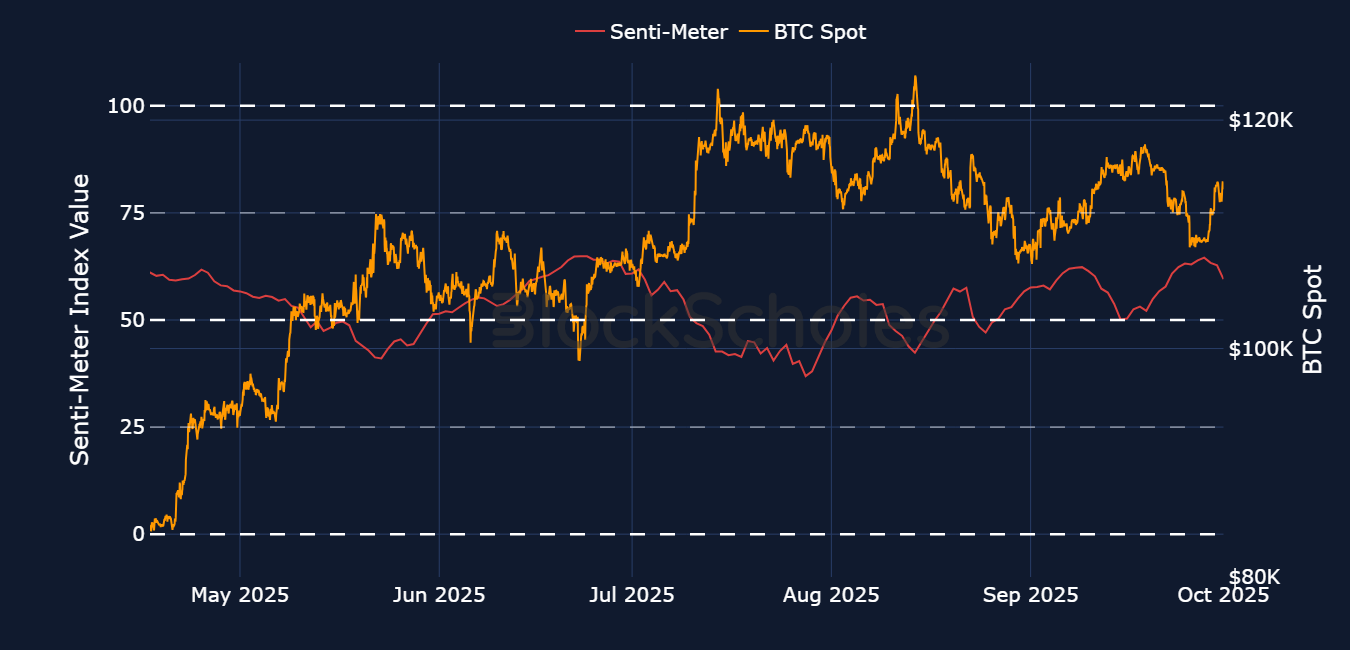

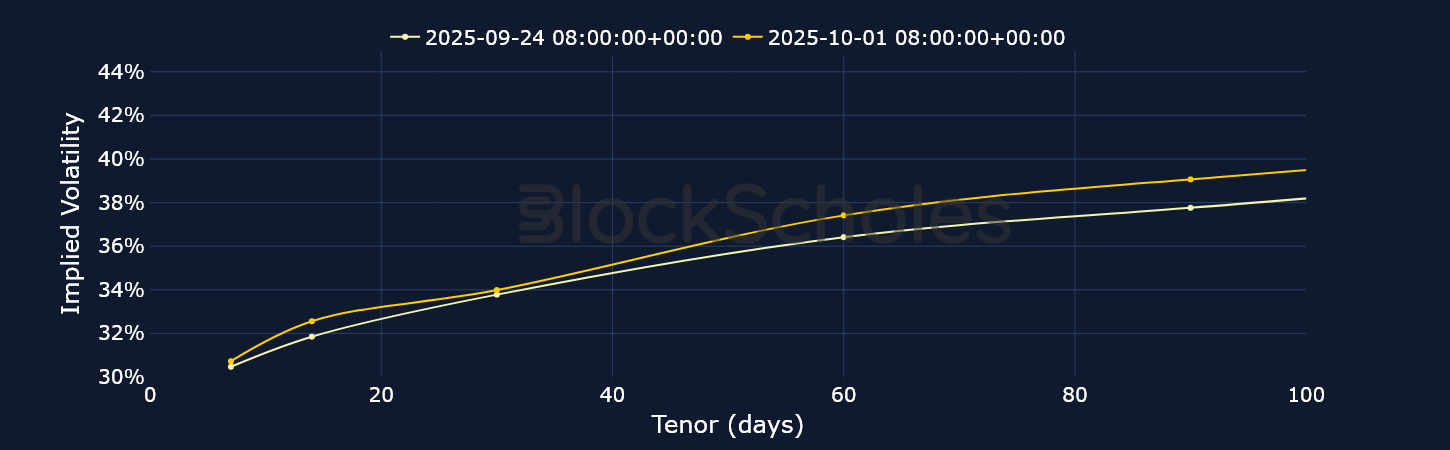

Options: Volatility smile skews remain bearish, despite an early October rally in spot prices.

Block Scholes’s Senti-Meter Index aggregates the funding rate, future-implied yield and volatility smile skew into a single expression of sentiment in derivatives markets. See more in the methodology article here.

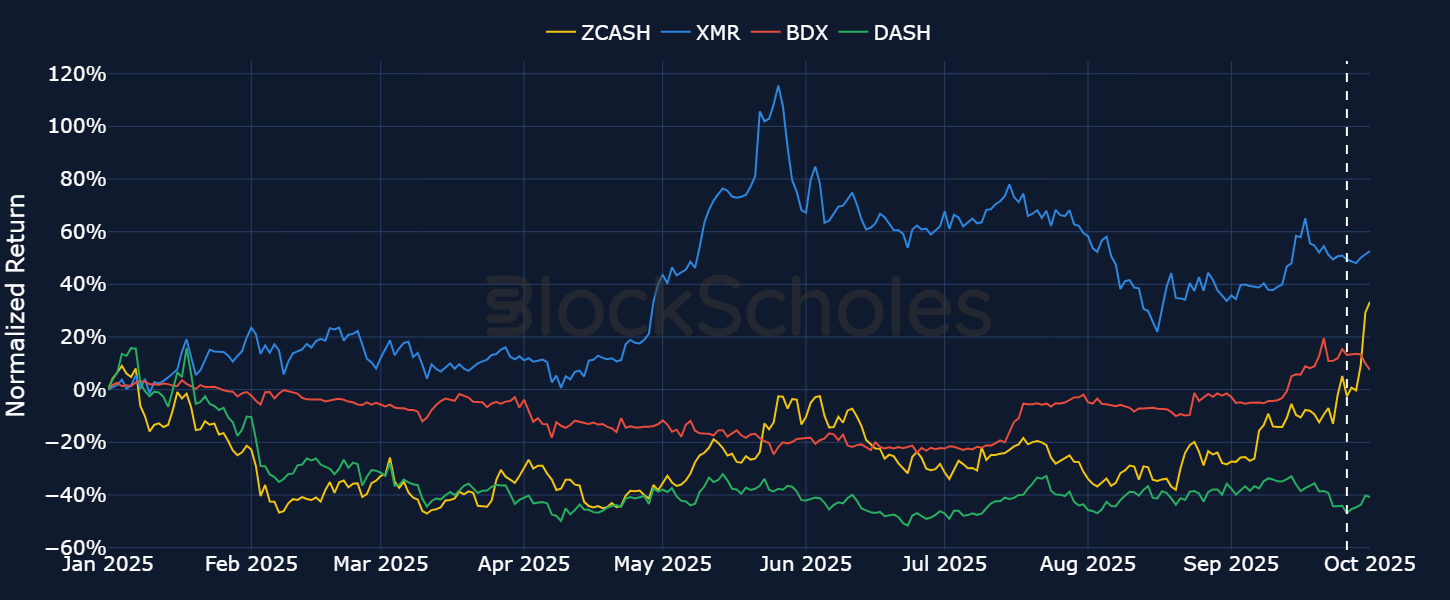

Zcash (ZEC) is a privacy token launched in 2016 that focuses on advanced zero-knowledge (ZK) proof technology. Since its launch, the token has aimed to offer a more advanced level of privacy when using it for transactions through “shielded addresses,” which are designed to encrypt transaction and address data stored on its blockchain. It has rallied in both of the previous bull runs/altcoin season cycles — first in 2017–18, when it surged to almost $900, and once more in 2021, when it rallied from $50 to upward of $300.

Over the past week, ZCash has enjoyed another major run, nearly doubling in price from $40 to above $95. There are a number of plausible explanations for ZEC’s rally:

Other privacy-related tokens have also rallied over the past two weeks, including Monero (XMR) and Beldex (BDX), though both of those tokens have underperformed relative to Zcash.

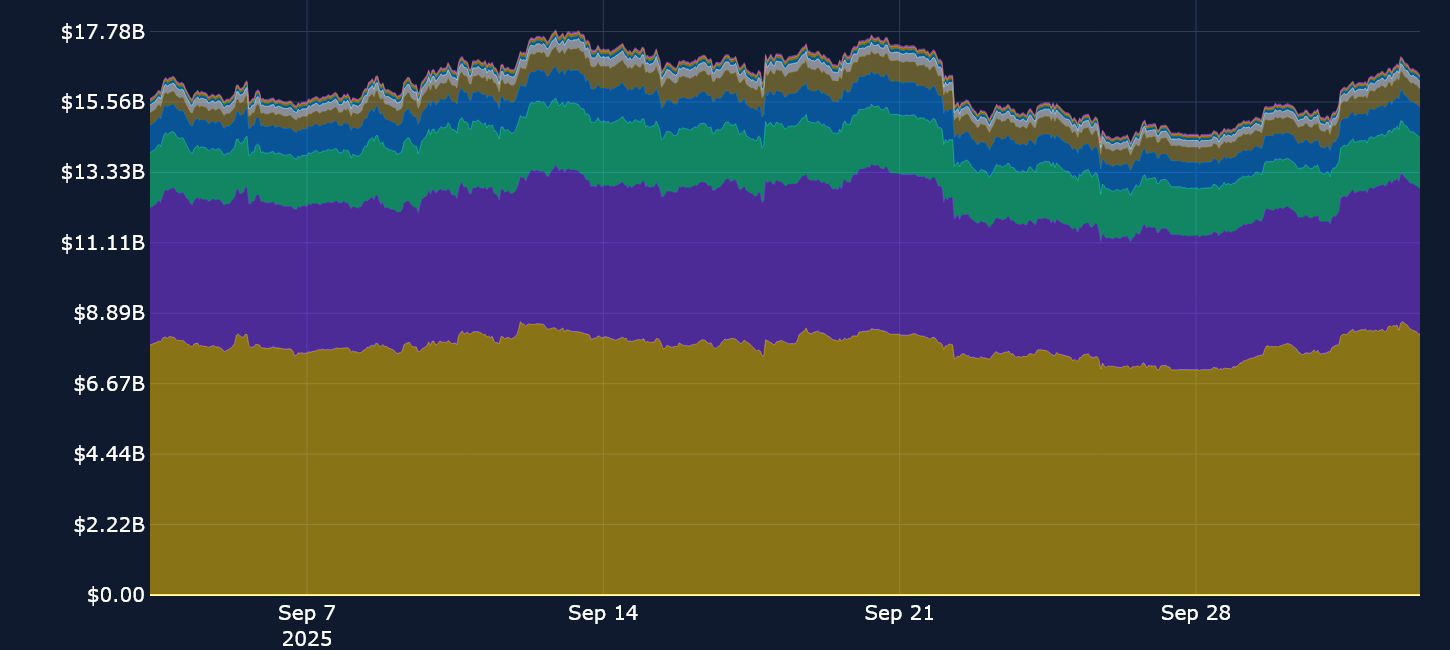

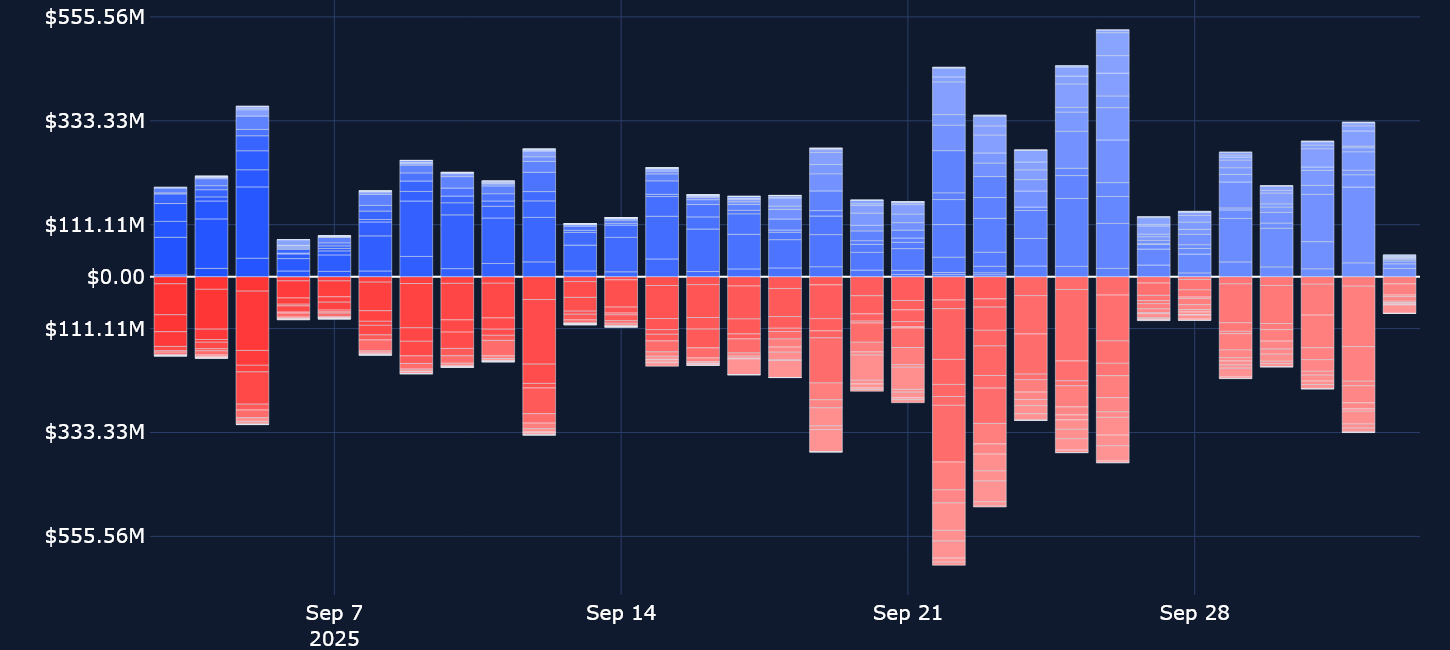

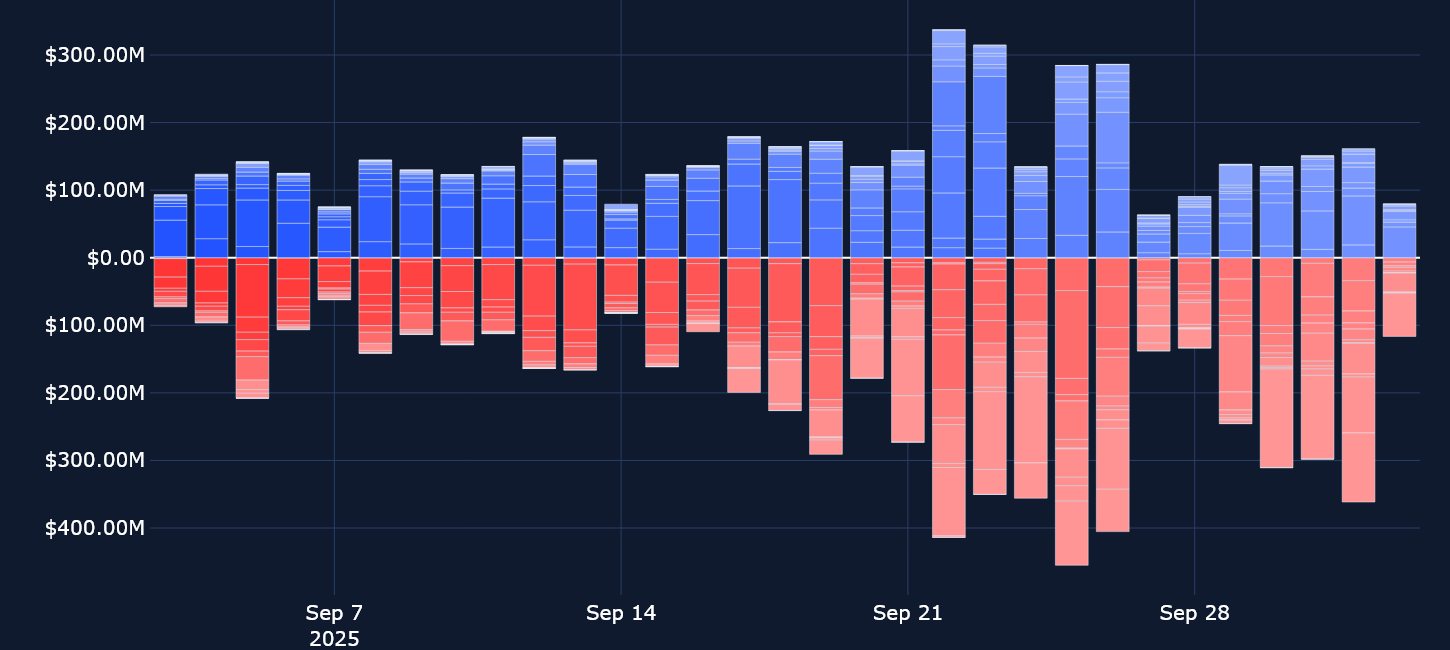

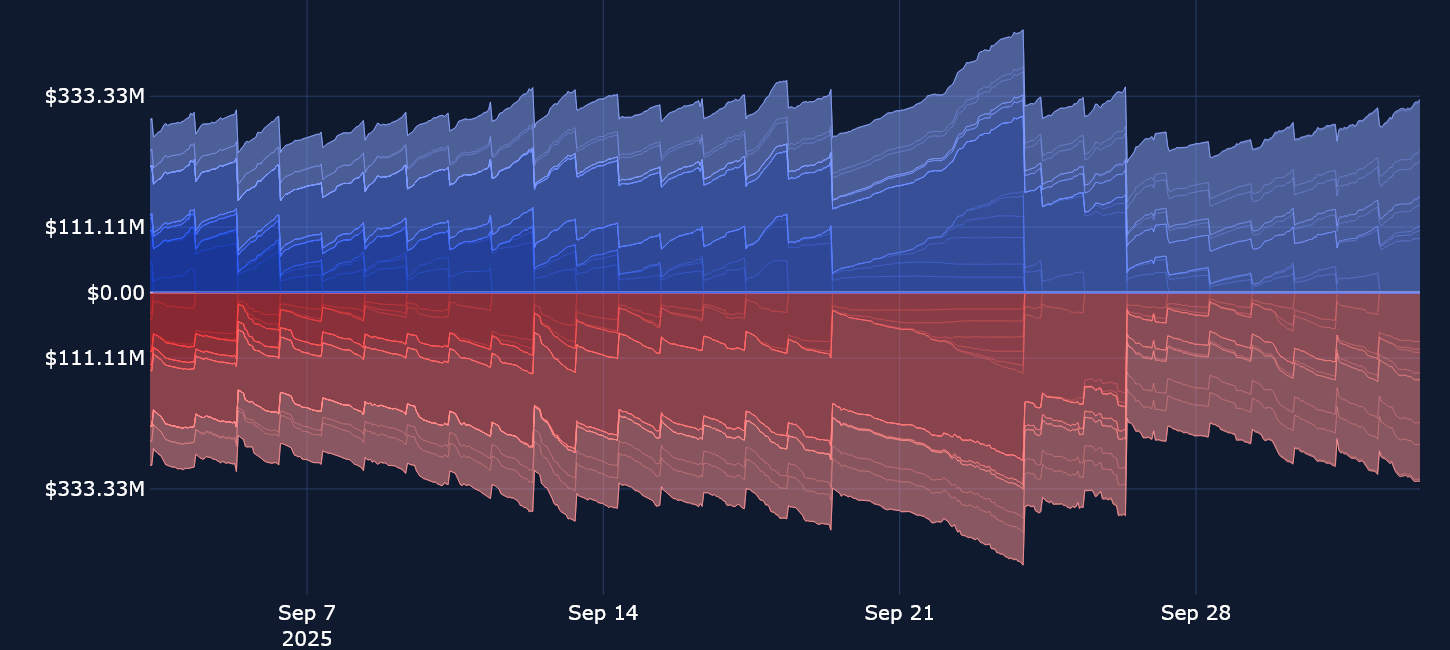

Open interest in leveraged perpetual swaps markets has dropped off from the all-time high levels that were reached in the run-up to the Federal Reserve’s September FOMC meeting. On Monday, Sep 22, 2025, the largest long liquidation event of the year took place, with more than $1.5B in long positions being liquidated across exchanges. This is certainly visible in the open interest chart (below). Between the late evening of Sep 21, 2025 and the early morning of Sep 22, 2025, open interest in ETH contracts plunged from $5B to $4.3B, as Ether’s spot price fell by more than 9% on the day.

Another small wipeout of positions occurred more recently on Sep 26, 2025 when both BTC and ETH fell below major support levels as BTC revisited $108K and ETH dropped to $3,800. ETH’s spot price has yet to recover to its pre-Sep 22, 2025 levels, while BTC has fully reversed its losses.

In the last edition of our Analytics Report, we mentioned that funding rates for the majority of crypto tokens had stubbornly refused to price in the same level of bearishness that options markets had been pricing in (and for the most part, still are) for BTC and ETH. The past week finally saw leveraged swap traders give in, and short positions have shown a willingness to pay a premium to longs in order to hold their short positions, in anticipation of a further drop lower in spot prices. That has meant funding rates for major altcoins — such as ETH, SOL and XRP — have at times over the past week and a half dropped below 0%.

Interestingly, BTC perp traders have still not been shaken out of their long position holdings, as funding rates have stayed positive for the entire month, barring a few exceptions when rates only marginally fell below neutral levels. This means that October has begun on the same footing as September, with leveraged swap traders reluctant to price in the same bearishness for BTC as for options markets.

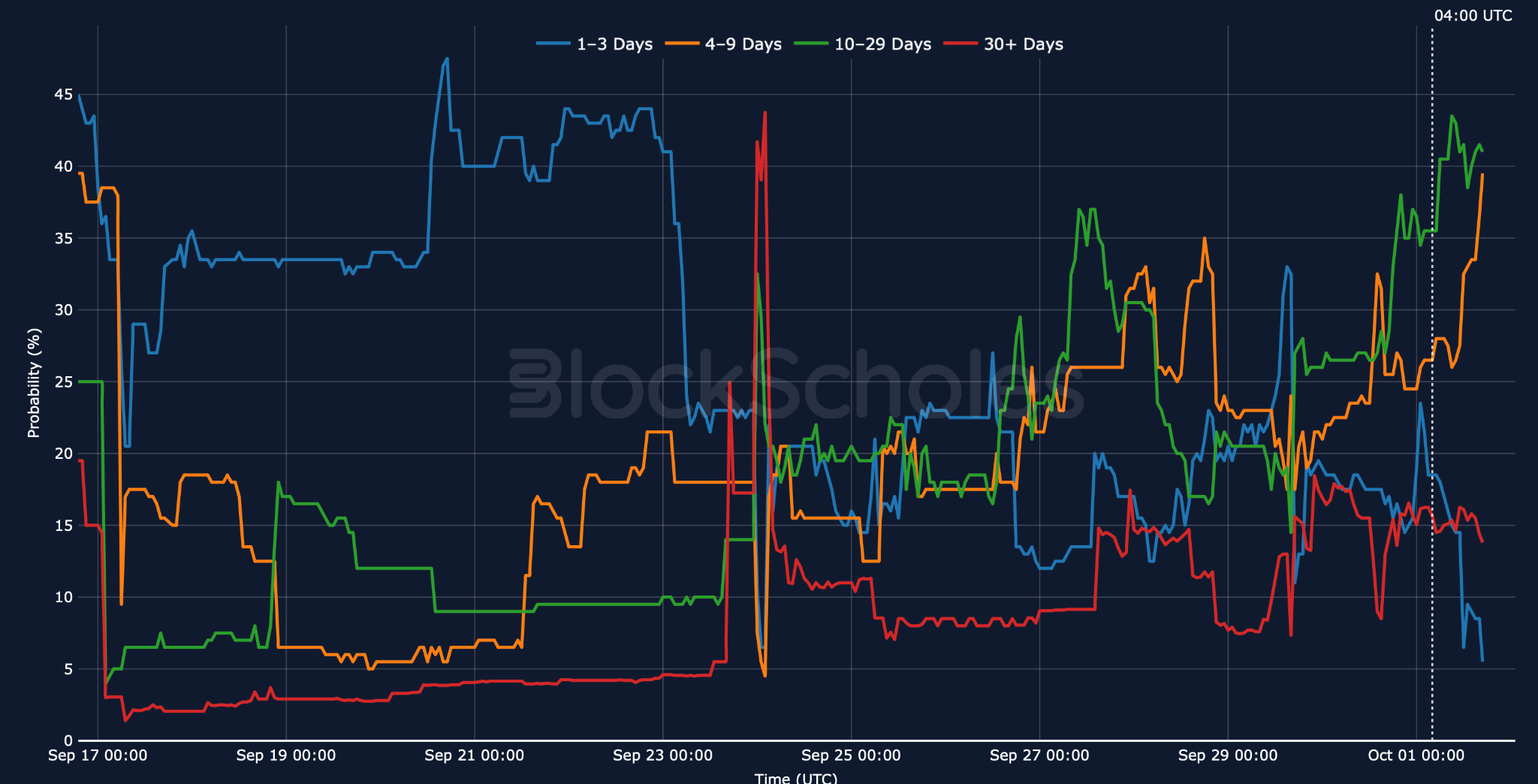

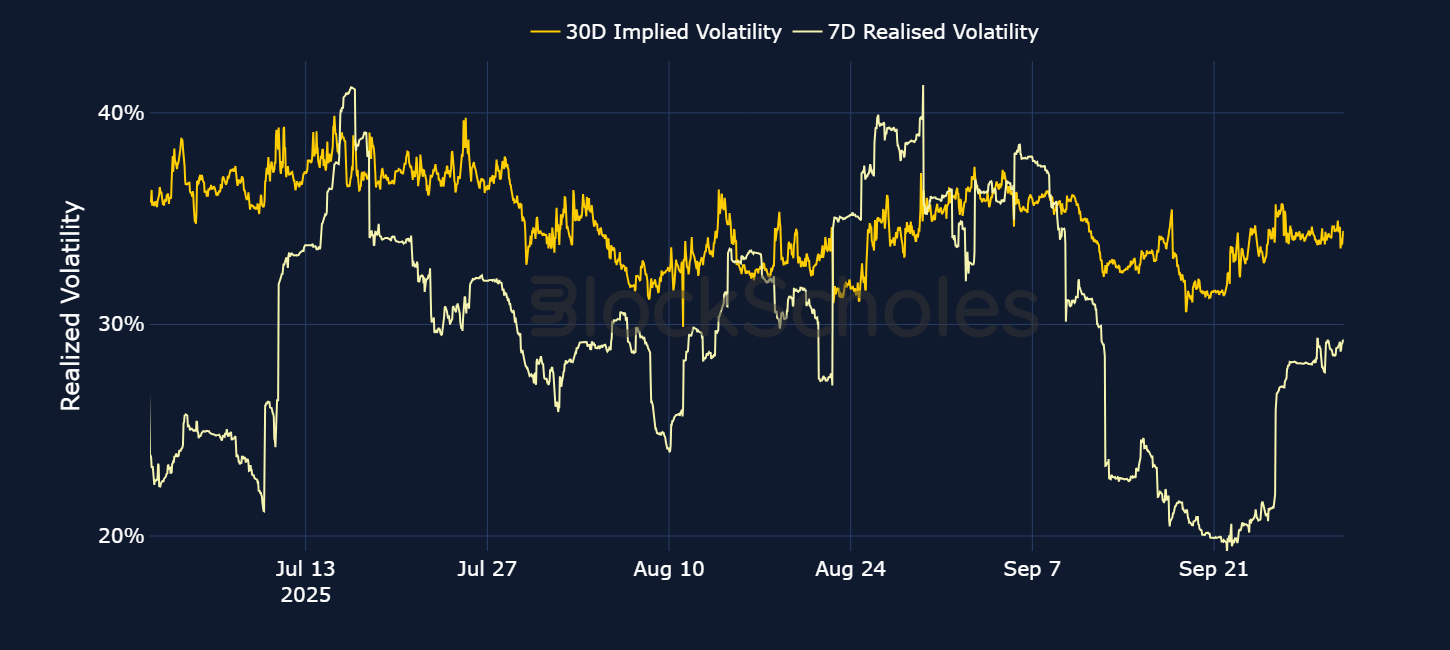

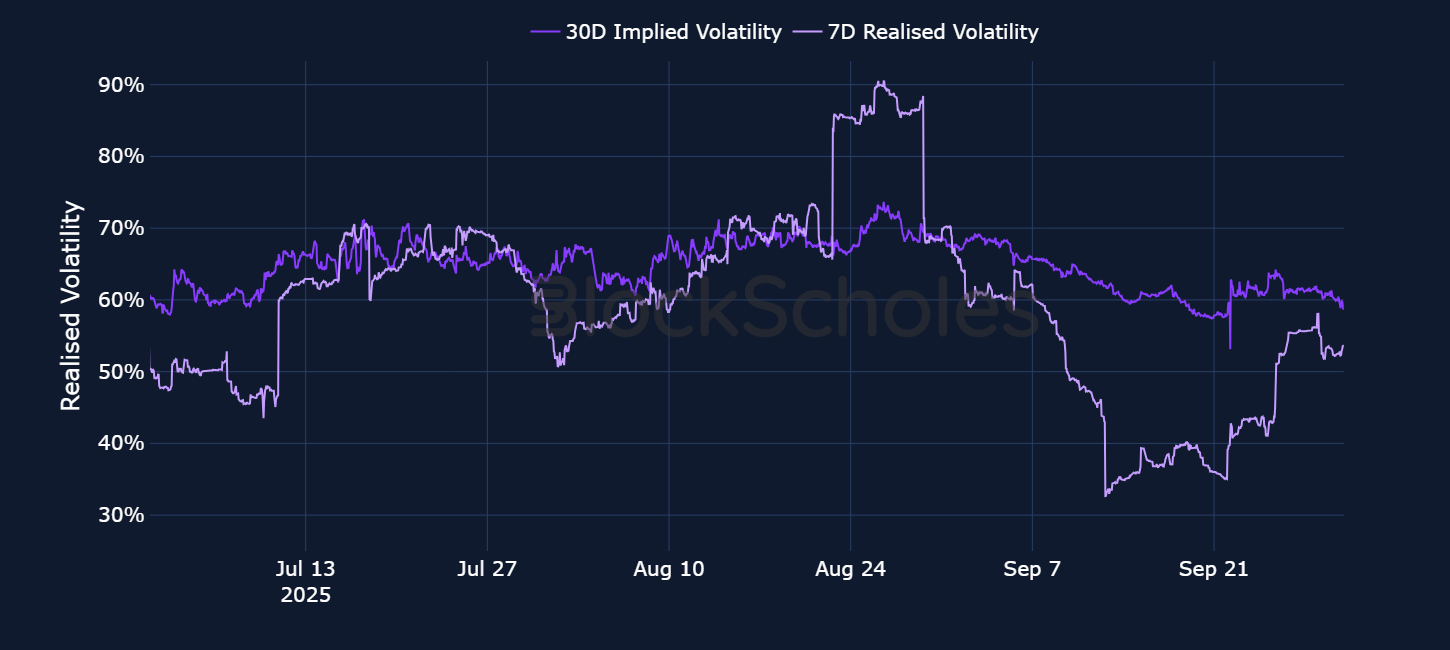

After a brief inversion in the term structure during the FOMC meeting on Sep 17, 2025, BTC’s implied volatility has once more trended back toward its historic lows. That move in ATM volatility appears to have been a byproduct of the complete collapse in realized volatility following the FOMC meeting. On Sep 21, 2025, 7-day realized volatility fell below 20% — a level last seen in mid-2023, barring several instances earlier in 2025.

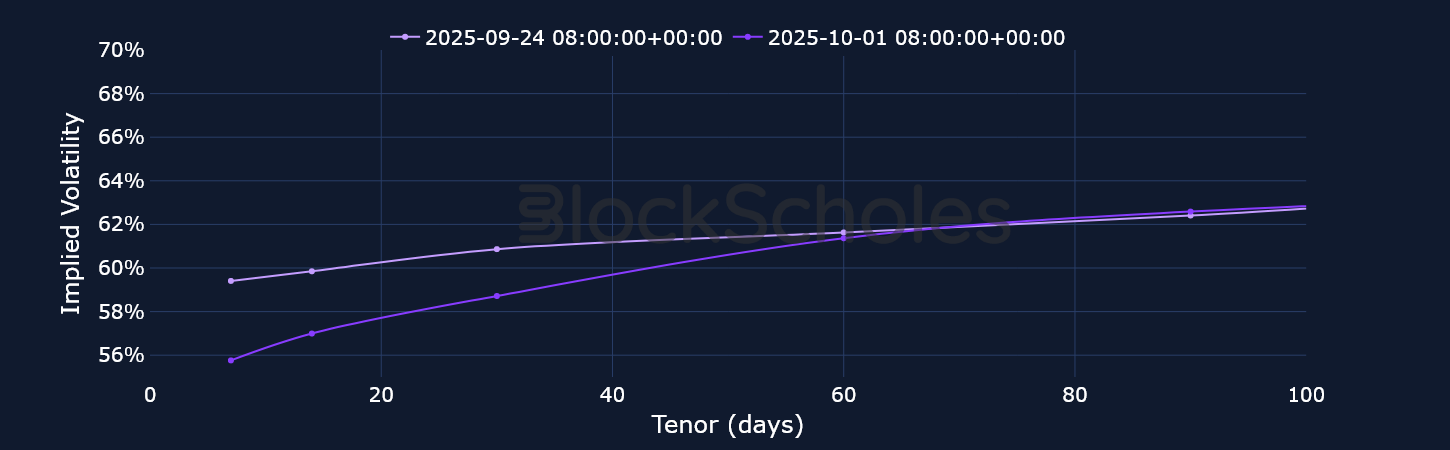

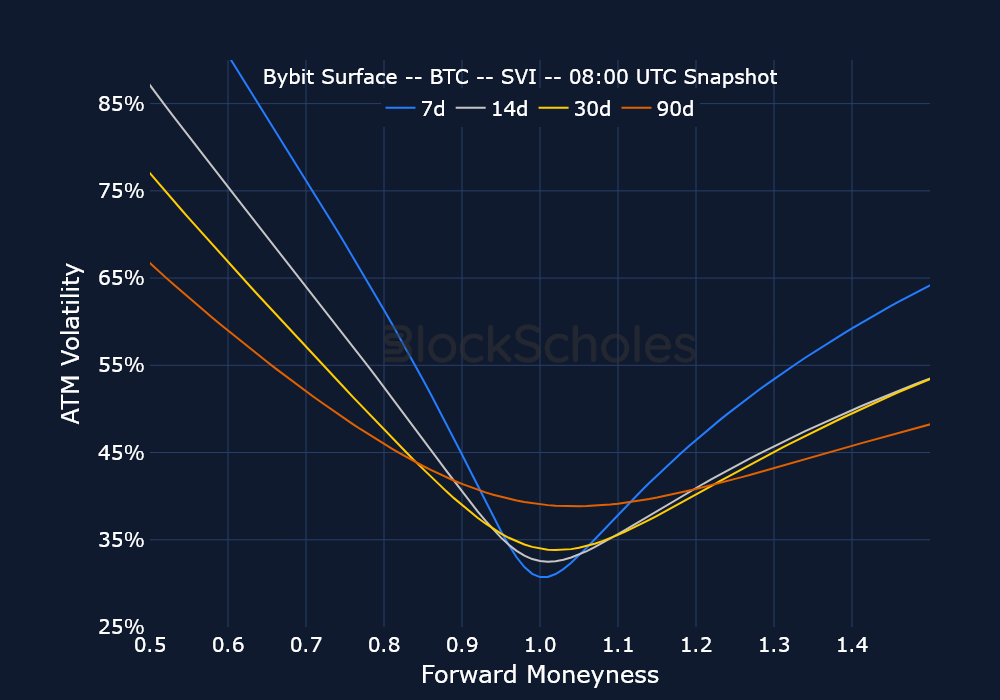

Despite some major twists and turns, September ultimately ended up being a modestly bullish month for BTC, as it closed the month trading at $114K (relative to a $107K open). Nevertheless, options markets have refused to price out their bearish expectations, as volatility smiles across the term structure remain put-skewed. Over the past few days, that skew has eroded, particularly for short-tenor options, though it still remains slightly negative.

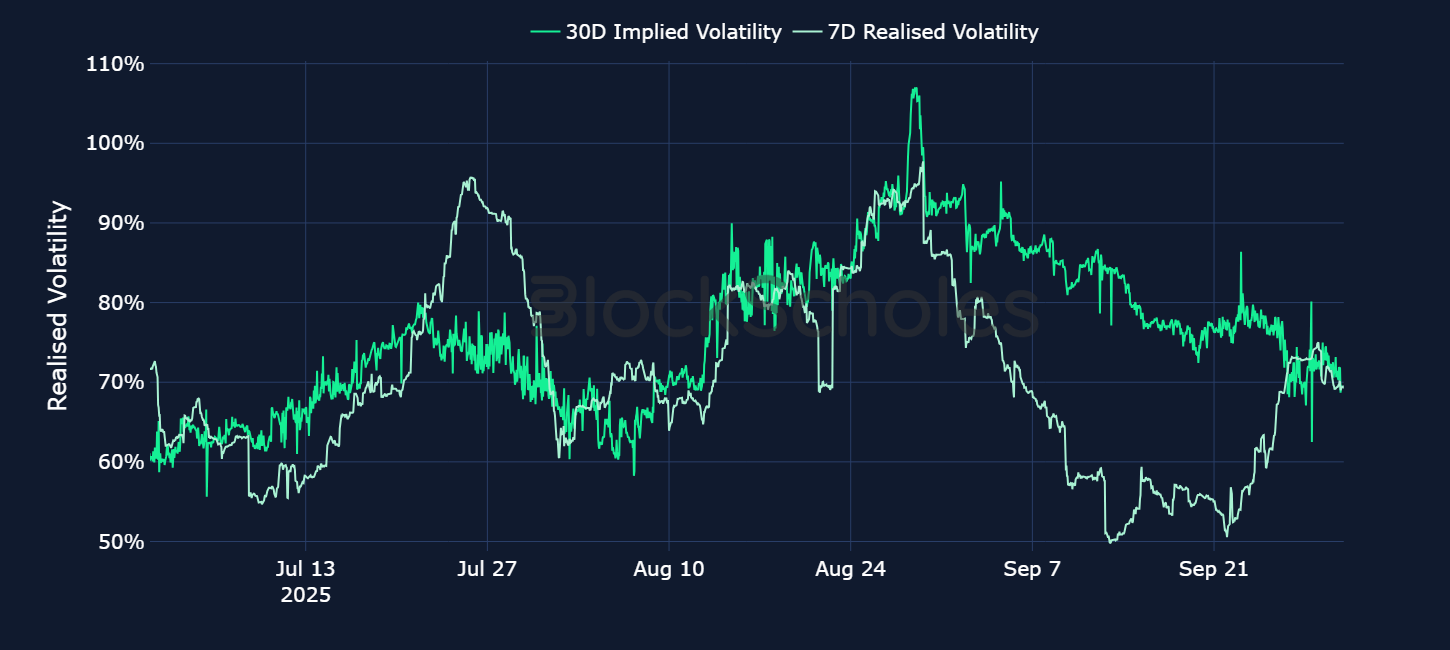

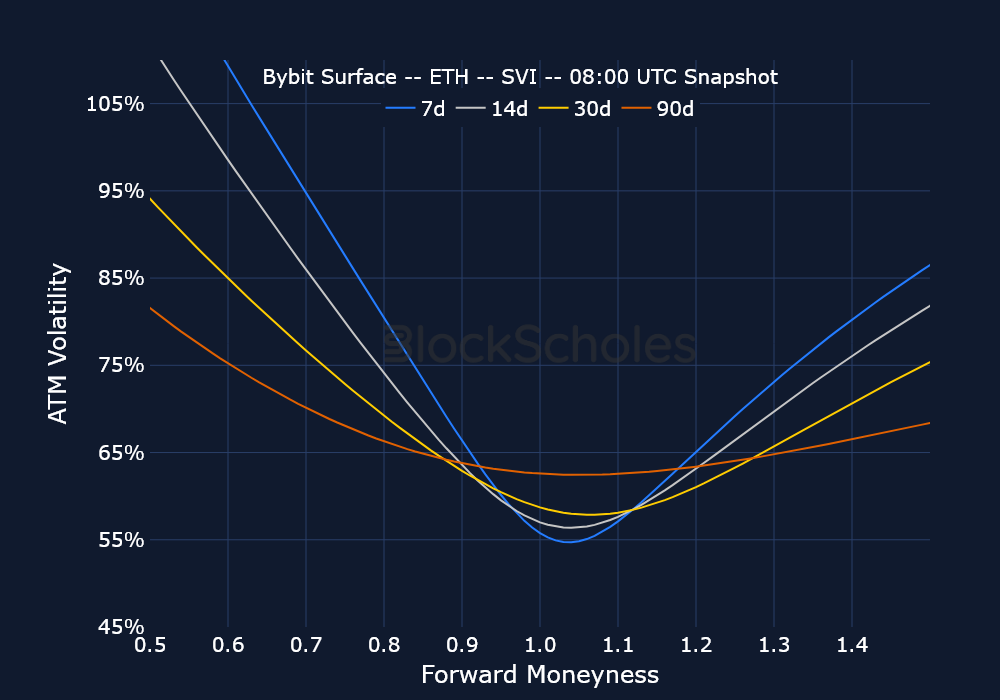

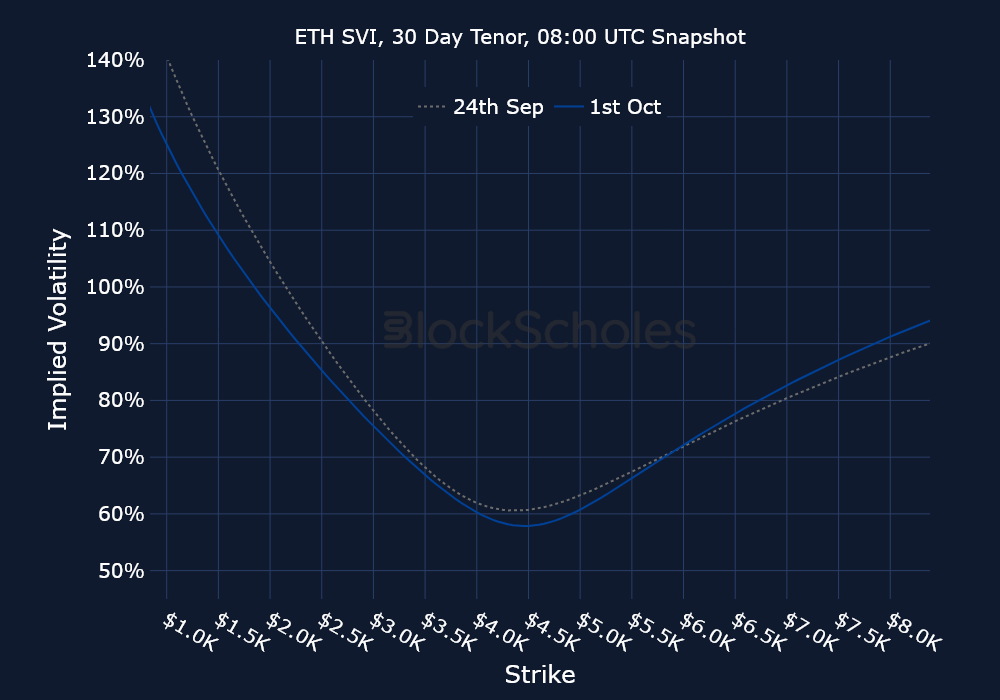

Options volumes for Ether continue to be dominated by puts, with volumes exceeding $400M during the spot price meltdown earlier in September when ETH fell below the major support level of $4,000. Spot Ethereum ETFs provided little respite for ETH traders toward the end of the month, as a five-day streak of consecutive outflows saw $795M worth of ETH being sold.

Similarly to BTC options, traders in ETH options continued to price in expectations of lower volatility as the month progressed, with ATM volatility levels declining 10 volatility points from the start of the month to its end. Additionally, as is the case with BTC volatility smiles, short-tenor ETH put-call skew has mostly remained tilted bearishly toward OTM puts.

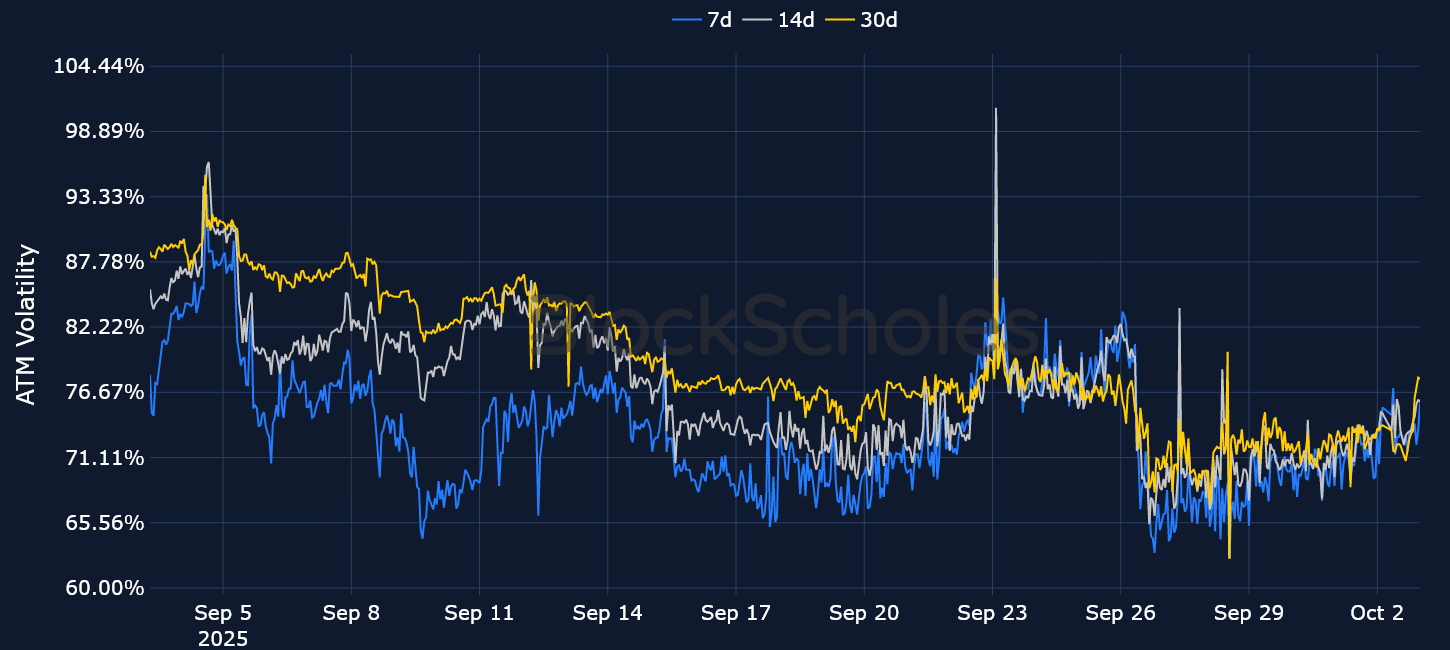

The large divergence between SOL’s realized volatility and implied volatility in the middle of September has now been resolved, with both measures registering at around 70%. Alongside BTC and the wider crypto market, SOL’s spot price rallied in the first half of the month, reaching a monthly high of $250. This was also bolstered by bullish announcements from digital asset treasury companies venturing into the token to form treasury reserves — something that was initially limited to just BTC and ETH. Most of those gains, however, have been lost through the second half of September, as SOL’s spot price fell to a low of $192.

Recently, both call option volumes and put option volumes have been quite small relative to the two major periods in the middle of the month. On Sep 18, 2025, put option volumes reached $100M, concentrated in longer-dated expirations and far exceeding the volume in calls.

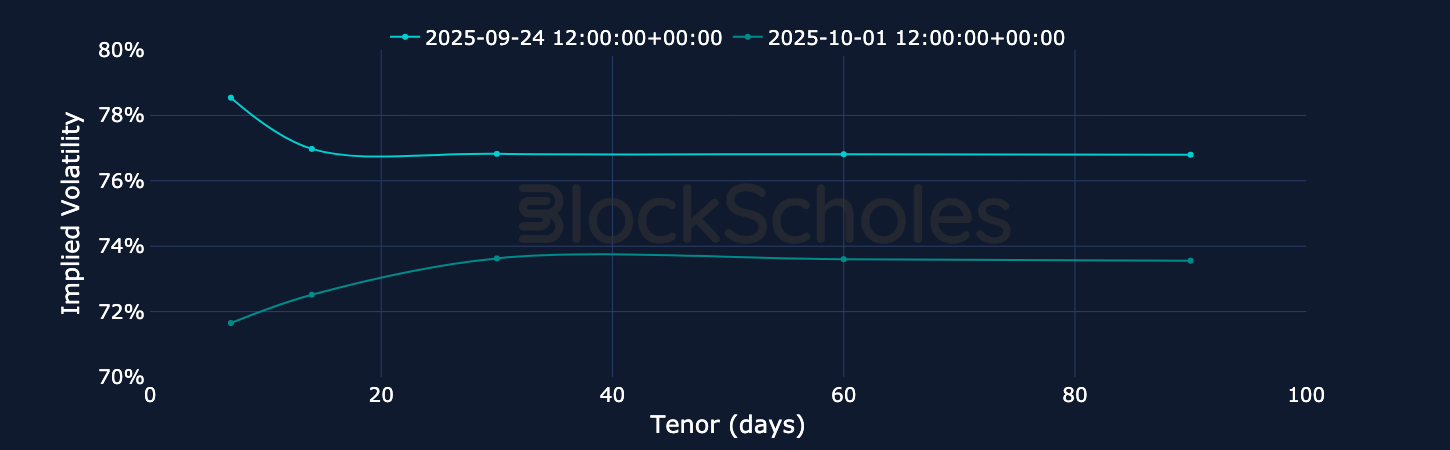

Throughout September, both BTC’s and ETH’s volatility smiles painted a similar story to the movements in spot markets until the middle of the month, as spot prices rallied progressively higher. Options traders began to price out their bearish sentiment, and volatility smiles eventually tilted toward calls. Then, as the FOMC September meeting passed and spot prices began to sell off in the second half of the month, volatility smiles began to skew further toward OTM puts.

Over the past week, BTC’s and Ether’s spot prices have enjoyed a modest recovery, with BTC now trading close to $118K and ETH trading at $4,400. This retracement has also been accompanied by an erosion in the put-call skew ratio, which is now trading close to neutral for short-tenor BTC options. For ETH, however, the US government shutdown appears to have had a more material impact. In the hours leading up to the event, ETH skew shifted heavily in favor of puts (recording a 12% skew toward OTM puts). In the immediate hours following the official shutdown announcement, most of that bearish skew was then priced out, and 7-day volatility smiles are trading just below neutral levels, similar to BTC.

Open interest and trading volume data are sourced “as is” from the Bybit exchange platform API exclusively, and as such do not represent a comprehensive picture of the sum of trading activity across all derivatives markets or exchanges. The data visualized in this report consists of hourly and daily snapshots, recorded over the previous 30 days. Daily (hourly) snapshots of trade volume record the total sum of the notional value of trades recorded in the 24H (1 hour) period, beginning with the snapshot timestamp.

If not explicitly labeled as derived from another exchange, the input instrument prices to all derivatives analytics metrics in this report are sourced from the appropriate endpoints of Bybit’s public exchange platform API. In the event that data is labeled or referred to as representing the market on another exchange source, that data is sourced from the appropriate endpoint of each respective exchange’s public API.

Macroeconomic charts and data are sourced “as is” from the Bloomberg Terminal. Exchange data is sourced “as is” from publicly available exchange APIs. Block Scholes makes no claims about the veracity of public third-party data.

After acquisition of underlying-denominated raw data for open interest and trading volume on the Bybit exchange platform from Bybit’s API endpoint, equivalent dollar-denominated figures are calculated using the concurrent value of Block Scholes’s Spot Index for the relevant underlying asset.

Block Scholes’s Spot Index represents the aggregate Spot mid-price for a given currency across the top five CEXs by volume (with USD-quoted markets). It considers the proportion of total volume in the instrument on the exchange, as well as the deviation of a data point from those on other exchanges.

Futures prices are used for Block Scholes’s futures-implied yields calculation services in order to derive the constant-tenor annualized yields displayed in the Futures section of this report.

Options prices are used for Block Scholes’s implied volatility calculation services in order to calibrate volatility surfaces, from which all derivatives volatility analytics displayed in the BTC Options and ETH Options sections of this report are calculated. Volatility smiles are constructed by calibrating to mid-market prices observed in Bybit options markets. As part of the calibration process, prices go through rigorous filtration and cleaning steps, which ensures that the resulting volatility surface is arbitrage-free and has exceptional fit to the market observables.

.jpg)

.jpg)