Thahbib Rahman

Research Analyst

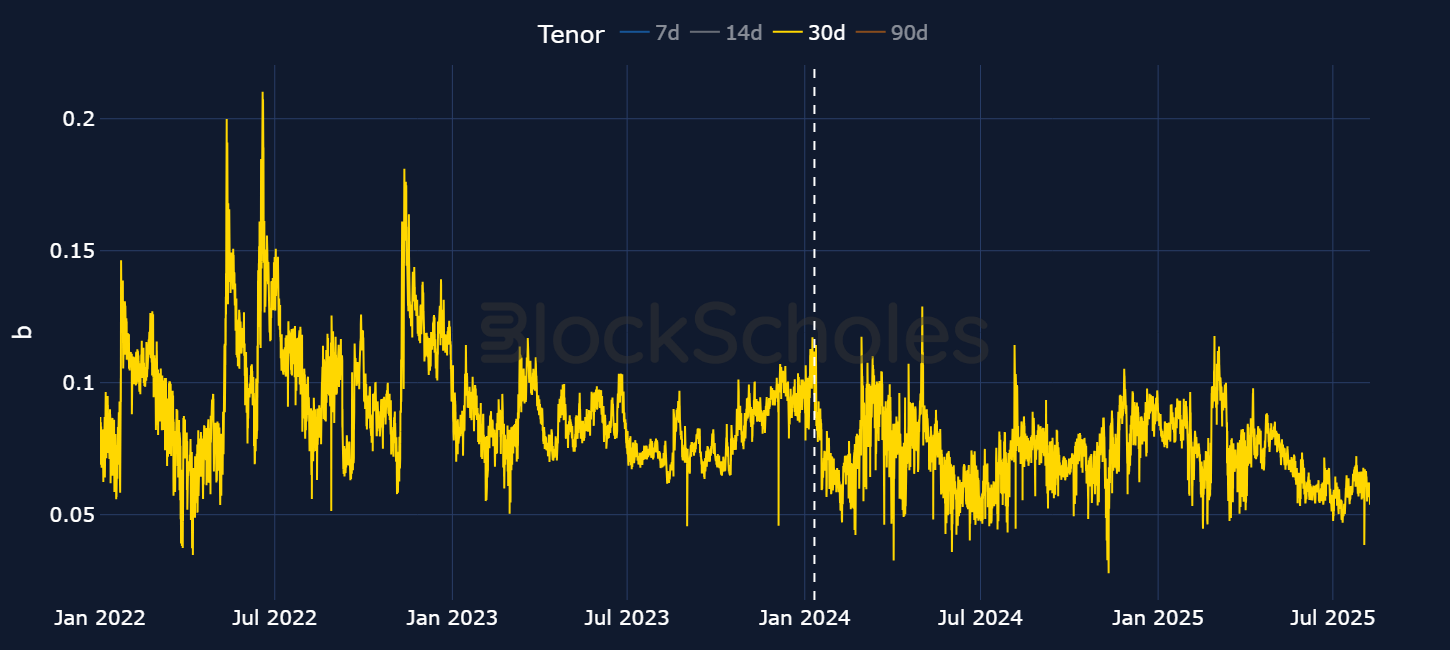

BTC’s volatility smile has flattened to cycle lows: Since 2022, BTC’s volatility smile steepness has become shallower, dropping close to its lowest levels in July 2025 — a sign that options markets appear to be assigning a lower probability of extreme BTC moves in either direction relative to moves close to the current spot price.

Despite Bitcoin touching multiple new ATHs, July was dominated by outperformances from Ether and other altcoins. The bullish price action across the board first began when the US House Committee on Financial Services announced that the week beginning Jul 14, 2025 would be declared “Crypto Week.” The end of that week marked a watershed moment for the digital assets industry: the US House of Representatives voted to pass the GENIUS Act after the bill had cleared the US Senate a month earlier. President Trump then signed the bill into law, stating “The GENIUS Act. They named it after me and I want to thank you. This is a hell of an Act.” Lawmakers in the US House also passed the CLARITY Act and the Anti-CBDC Surveillance State Act.

While BTC initially led the charge, signs of profit-taking and potential capital rotation meant that by the end of “Crypto Week,” it was altcoins that stole the show: in particular, Ethereum’s native token, Ether (ETH), rallied from $2,400 to just under $4,000 over the month (by more than 58%), and has since surpassed that $4,000 mark to trade closer to its 2021 ATH of $4,800. A regulatory environment that has been (and is likely to continue to be) beneficial to the wider altcoin market as a whole appears to have rekindled a risk-on appetite for non-BTC tokens. Indeed, BTC’s proportion of the total crypto market cap fell below the key level of 60% in July.

In this month’s volatility report, we’ll analyze the continued growth in the ratio of ETH at-the-money and BTC at-the-money volatility levels, as well as a notable divergence between BTC and ETH’s spot prices in 2025. We’ll then turn our attention to changes in the relative demand for out-the-money options at strikes further away from the current spot price.

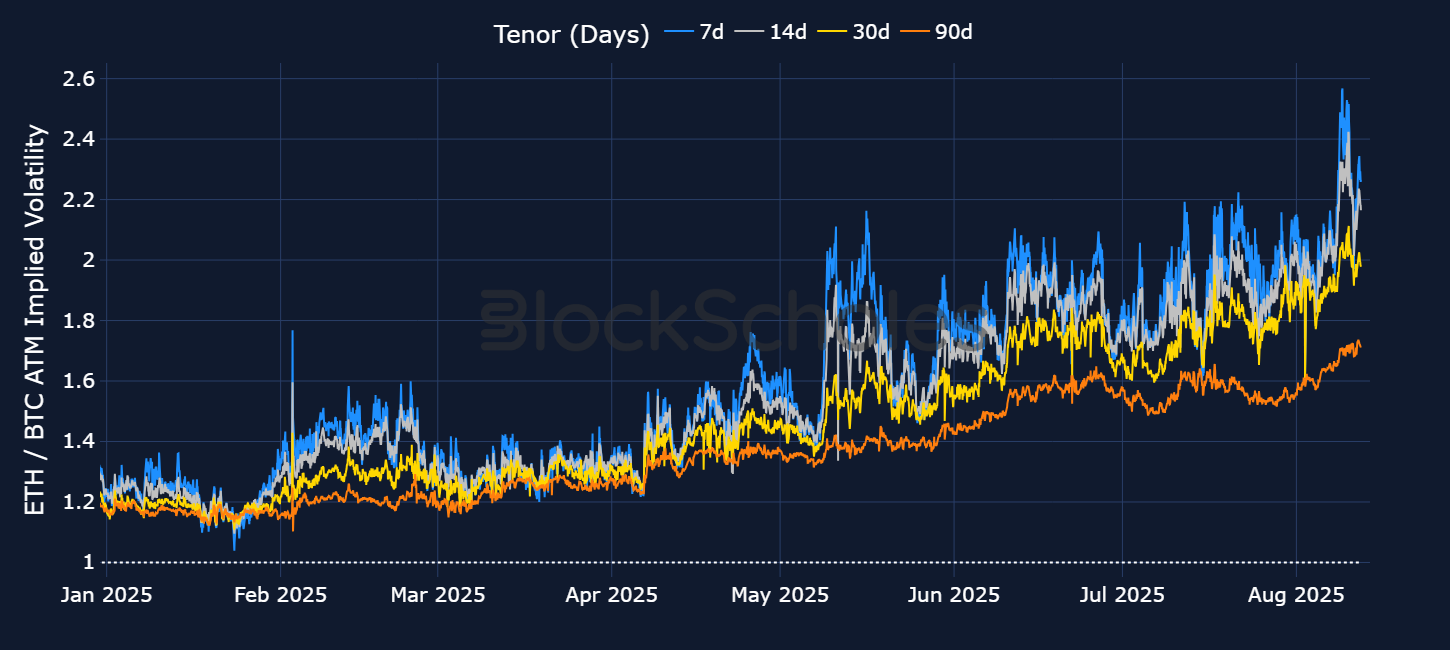

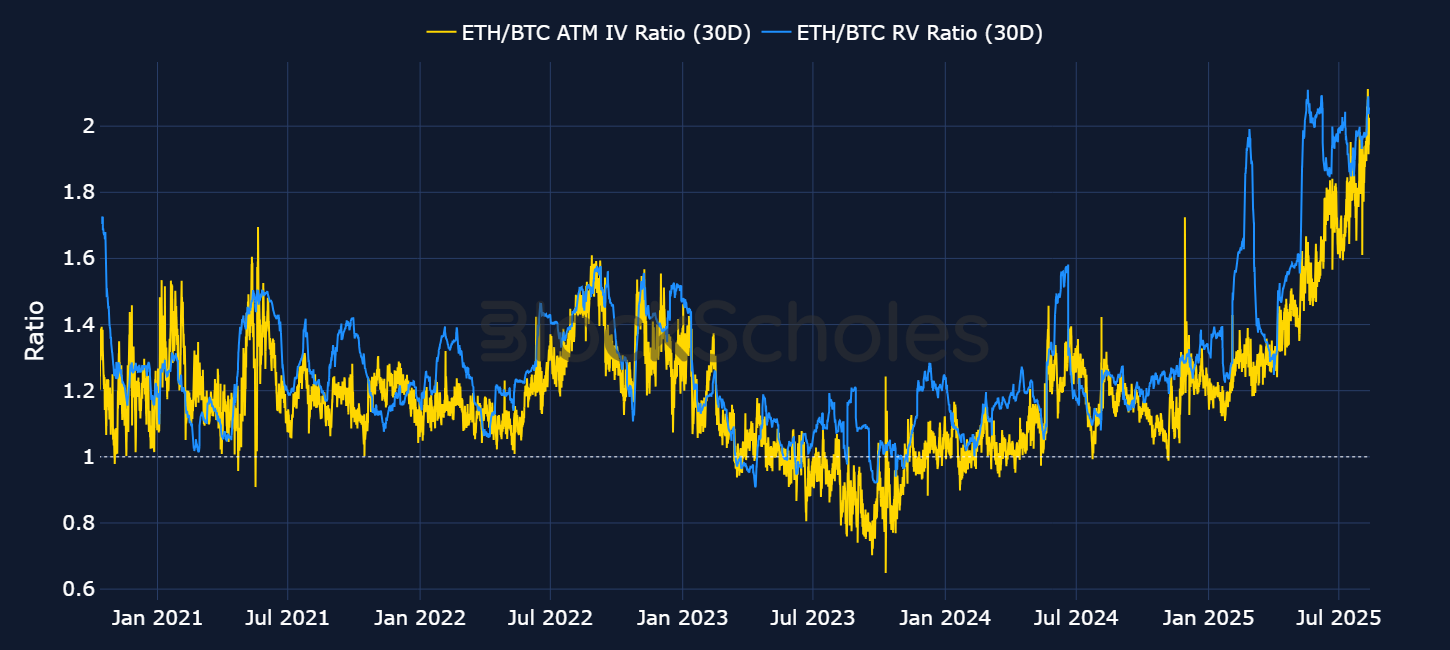

Through the month of July, ETH outperformed the rest of the crypto market with a vengeance, increasing by 58% (compared to a 14% rally in BTC). ETH began the month trading at $2,400, and by the tail end of July it was trading upward of $3,890. Coinciding with that spot price outperformance, the ratio of ETH at-the-money implied volatility (a measure of the demand for options) relative to BTC at-the-money implied volatility rallied further, a move higher that has continued well into August.

We first commented on this ATM IV ratio in our May volatility report, in which we highlighted that the ratio for 7-day BTC and ETH options started at 1.5 in May and rose to 2.16. This meant that by the middle of May, ETH 7-day options were trading with an implied volatility that was 2.16 times higher than equivalent-tenor BTC options.

In July, we saw a further steepening of that ratio across all tenors. For 7-day options, the ETH-to-BTC ATM IV ratio steepened from 1.63 to 2.2, meaning that 7-day ETH options carried a 2.2x implied volatility premium to their BTC counterparts — indicating that ETH options have been carrying a significant premium relative to their BTC counterparts as a result of increased expectations of ETH volatility (relative to BTC’s) by the market.

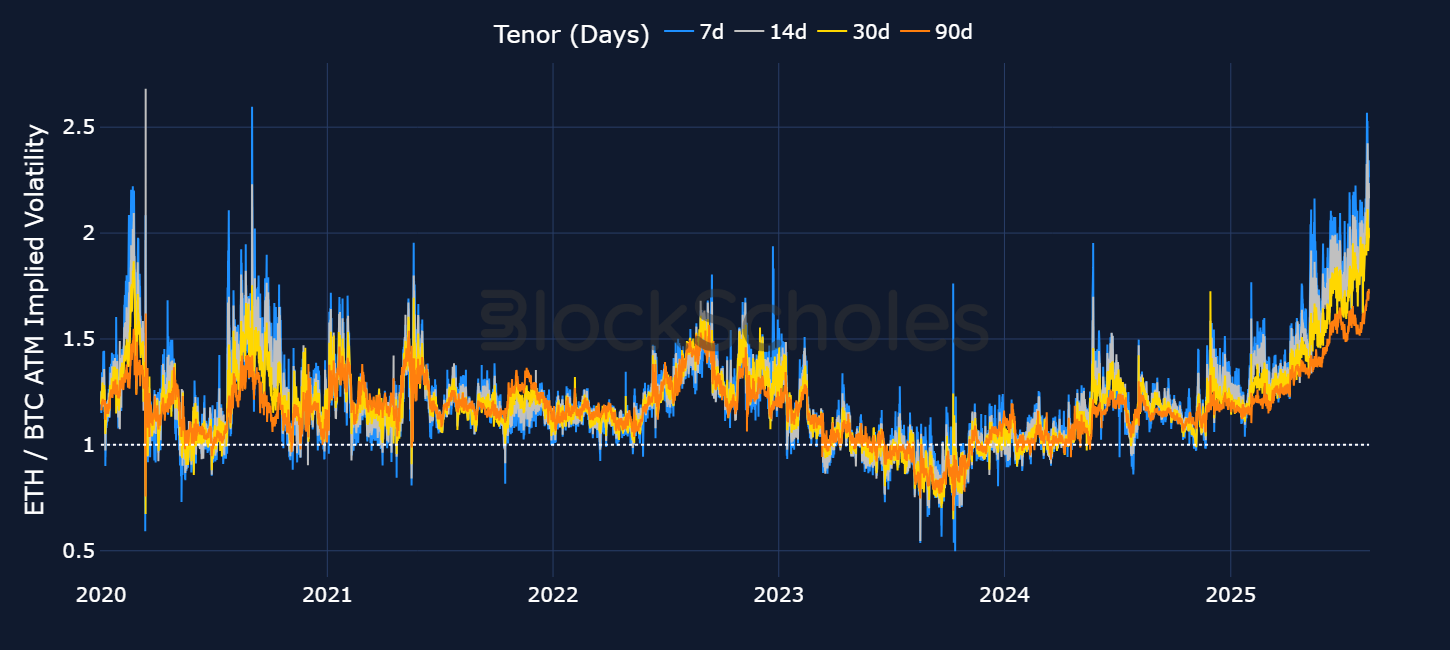

For most of these two major cryptos’ shared history, traders have priced in a higher premium for ETH options relative to BTC options. We can see that in the above chart, as the ratio has fallen below 1 only a handful of times, none of which have lasted very long.

This isn’t surprising. While ETH and BTC have a strong relationship, and have historically traded with high correlation, ETH has typically done so with a higher realized volatility than BTC. Moreover, this isn’t unique to the BTC-ETH relationship. In general, any BTC-altcoin pair has historically seen the altcoin trade in a more volatile manner than BTC, so it makes sense that forward-looking measures of volatility would exhibit the same relationship. We can confirm this by looking at ETH’s “beta” to BTC returns — a measure of the ratio of the size of ETH’s log-returns to BTC’s on a rolling 90-day basis.

What we find is that ETH has historically traded with an amplification of BTC’s returns, whether up or down. For example, when the beta is 1.6 (as was the case in July), it indicates that, on average, a 1% return in BTC (positive or negative) corresponds to a return of 1.6% in ETH in the same direction. This rolling measure of beta has steepened significantly in two separate regimes since 2023: the first began in January 2024, and the second (even steeper) increase in beta began in January 2025 — a pattern which is evident in the at-the-money volatility ratio, too.

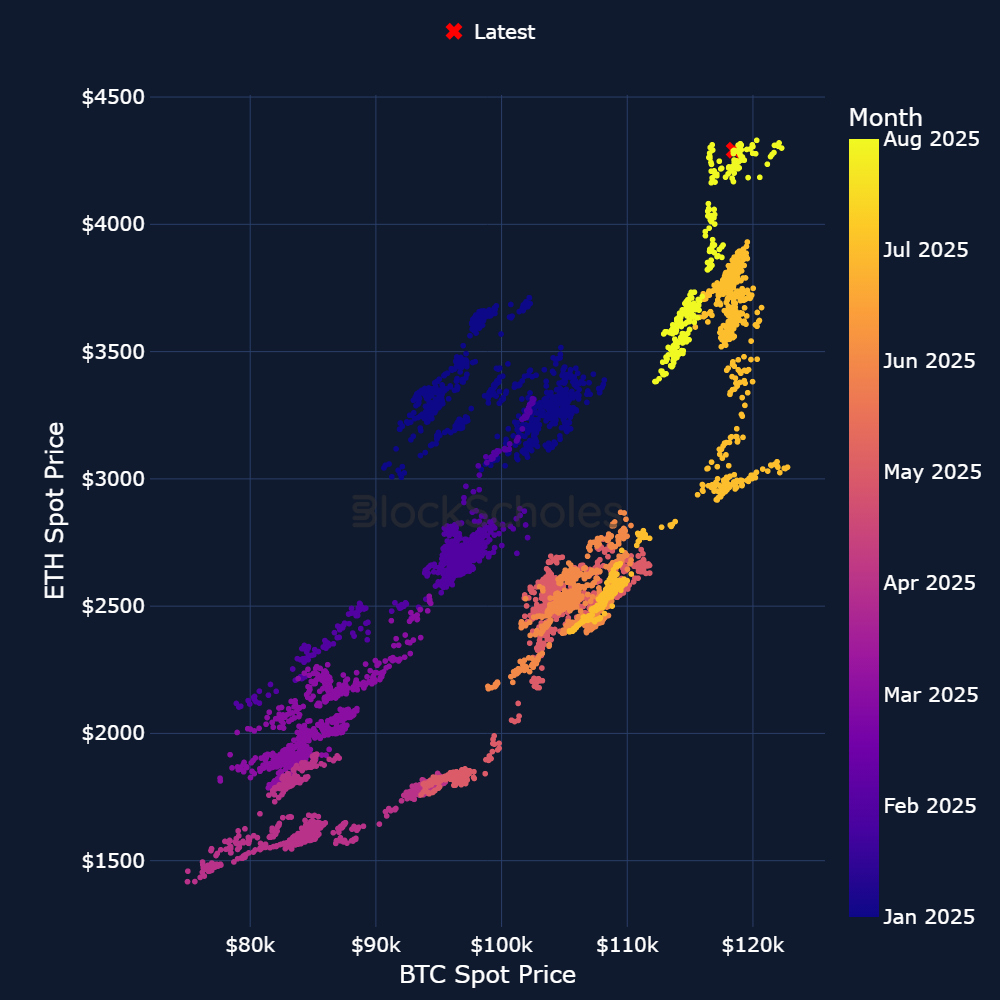

While ETH and BTC have historically been correlated with one another, in 2025 we’ve observed two intriguing patterns exhibited by the spot price of both assets. First, the spot prices of both BTC and ETH have displayed “stepwise”-like movements — whereby prices hold steady for a period of time, only to move sharply up or down in an aggressive manner before consolidating and holding steady once more. In the chart below, this is shown by plotting BTC’s spot price on the left-hand axis alongside ETH’s spot price on the right.

Secondly, BTC and ETH appear to be correlated with each other via two unique regimes. In the fallout from President Trump’s “Liberation Day” tariffs, BTC fell to a low of $75K, having started the year closer to $93K. Equivalently, ETH crashed to a low of $1,417 while starting the year above $3,300. BTC recovered quickly from its local bottom — by mid-May, it was once more trading back above $90K — while ETH failed to take the leg higher. In fact, ETH required two major moves, the first in May and an even bigger move in mid-July, to finally regain the level it dropped from at the start of the year. Both of those moves were sharp upward spikes in the stepwise manner we’ve explained above, with a near-flat consolidation period in between.

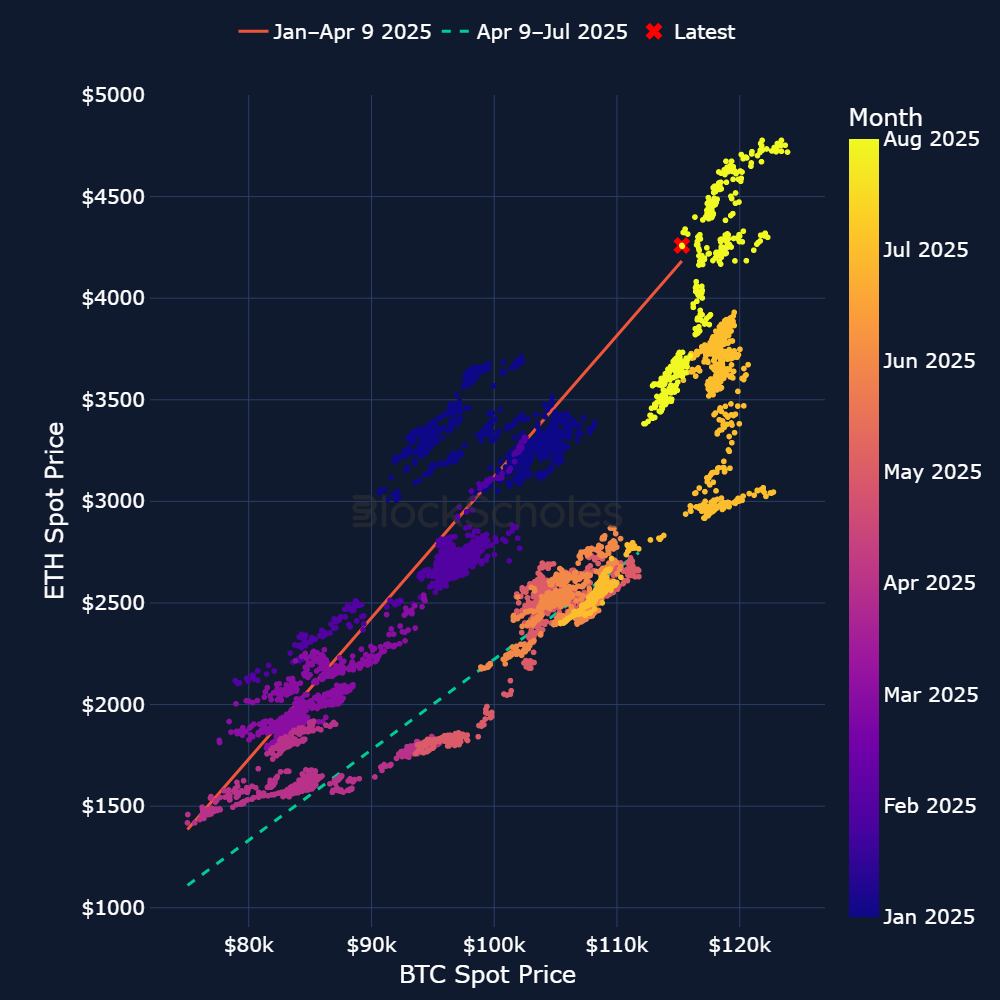

This observation admits three different periods in 2025. In the first and the third intervals, corresponding to Jan 1–Apr 9, 2025 and Jul 1–Aug 13, 2025 (respectively), BTC and ETH price levels held the same linear relationship to each other. This means that ETH’s price was (on average) the same multiple above BTC’s throughout the movements in this period.

However, in between those periods (from the start of April to the end of June), ETH and BTC moved with a slightly different relationship. This can be clearly seen in the chart below, which overlays the linear regression line for each period on top of each scatterplot. Take a BTC price of $100K, for example — the initial January-April relationship implies an ETH price of $3,100. However, in the second regime, that same BTC price of $100K implied a far lower ETH price of $2,200 in April. Graphically, the y-intercept of the regression line was far lower — and thus, for any given price of BTC, the linear fit implies a far smaller price for ETH. That then changes once more in July as the two assets return closer to their beginning-of-the-year relationship.

Tellingly, despite the divergence in the spot price of the two assets, one thing that remains constant throughout both regimes is that the ratio of at-the-money ETH implied volatility continues to steepen against BTC’s at-the-money implied volatility. Why is this the case?

The chart below is a time series of how the at-the-money implied volatilities of a 30-day BTC option and a 30-day ETH option have changed through the month of July. This clarifies why the ratio steepens throughout the month: BTC volatility fell while ETH volatility remained high.

Looking at the chart below, at-the-money IV for BTC 30-day options trades sideways throughout the entire month before it drops briefly from Jul 28, 2025. On the other hand, traders in ETH options show a much stronger willingness to push up the prices of ETH options and, therefore, their implied volatility. The 30-day IV rises from 58% to 71% in the first half of the month before hovering in the 60% region for the rest of it.

Even as BTC rises to a new ATH of $123K, bolstered by President Trump’s signing of the GENIUS Act and positive developments in regulation for the wider crypto industry, 30-day at-the-money implied volatility for BTC options barely moves.

There’s another factor that makes the divergence in ETH and BTC implied volatility even more revealing. In our May volatility report, we first highlighted the dislocation in implied volatility levels that matched a similar dislocation in the ratio of the two assets’ realized volatility levels — ETH’s and BTC’s 7-day realized volatility ratio reached an ATH of 2.9 on May 15, 2025, just one day before the peak in the equivalent implied volatility ratio.

However, this time, the realized volatility ratio declined from 2.05 to 1.85 in the first half of July, largely because of a falling realized volatility for ETH down toward BTC’s levels. Over that same time period, the at-the-money implied volatility ratio steepened from 1.6 to 1.95, due to both an increase in ETH IV and a flat market-implied volatility for BTC options at 35%.

We expect a convergence in the two ratios because — in general — if traders recognize over some period of time that ETH’s realized volatility is significantly higher than BTC’s, an expectation for that trend to continue would translate into an equivalent increase in the at-the-money volatility ratio. Similarly, if the delivered ratio declines, traders anticipating a continuation of that decline would price it into options markets.

However, the most recent convergence has done nothing to slow the trend: measured by both backward-looking realized volatility and forward-looking implied volatility, BTC’s volatility levels are reaching extreme lows, relative to both its own history and its historical relationship with ETH.

In July 2025, the ETH/BTC implied volatility ratio for 30-day options crossed 1.8 for the first time in five years. The last time it had reached a level this high was in February 2020. Then, in August 2025, the ratio rose to a new record high.

Back in February 2020, BTC at-the-money volatility was trading sideways at 55% (around 20 percentage points higher than current IV levels). At that time, ETH at-the-money volatility jumped from 69% to just under 100%, driving the increase in the ratio. This big move in ETH implied volatility in 2020 coincided with a spot price rally that saw ETH more than double from January 2020 (just before the Covid crash in March 2020). Over the same period, BTC had increased by a smaller 40%, while options markets were pricing in a far lower level of volatility for BTC relative to ETH.

In July 2025, however, the steepening was for a different reason: while ETH at-the-money volatility increased (though to a lesser extent than the increase back in 2020), BTC volatility fell, particularly at the end of July.

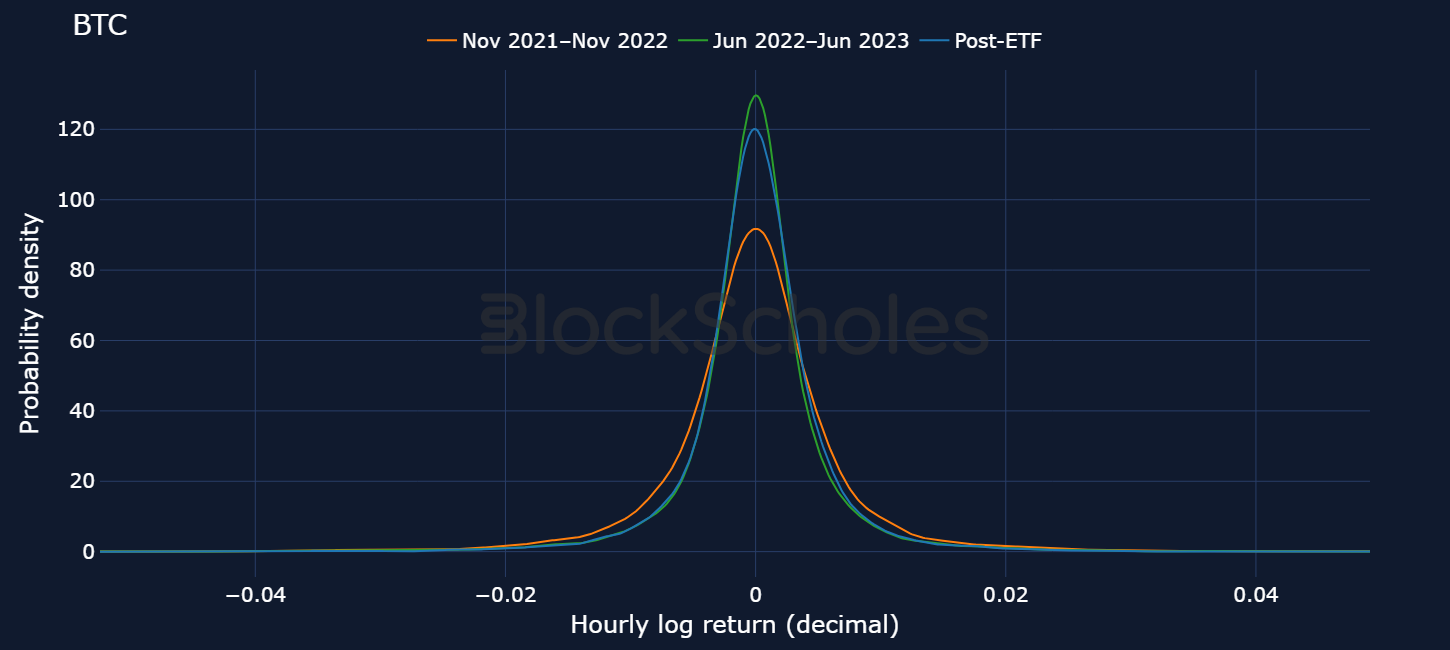

In our June volatility report, we put forward the case that while market maturity has been one cause for BTC’s volatility levels declining over time, Bitcoin Spot ETFs may have contributed to suppressing BTC volatility since their launch in 2024.

Below, we plot the distribution of hourly log returns for BTC across three distinct periods: the BTC bear market between November 2021 and 2022, the sideways price action following on from that bear market into 2023 and then the post-BTC Spot ETF period, i.e., January 2024 to the present. Following the spot ETF launch, the distribution of returns has become narrower with a higher peak. This is a clear indication that, post-ETF, the probability of smaller positive (or negative) returns is more likely, while the tails of the distribution have become thinner — meaning that outsized returns in either direction have become less common.

So, if small returns make up a far larger proportion of the distribution of returns and the likelihood of large positive or negative returns has become rarer, have forward-looking BTC options markets become attentive to this phenomenon? In other words, are options markets slowly assigning a smaller likelihood to outsized moves in spot?

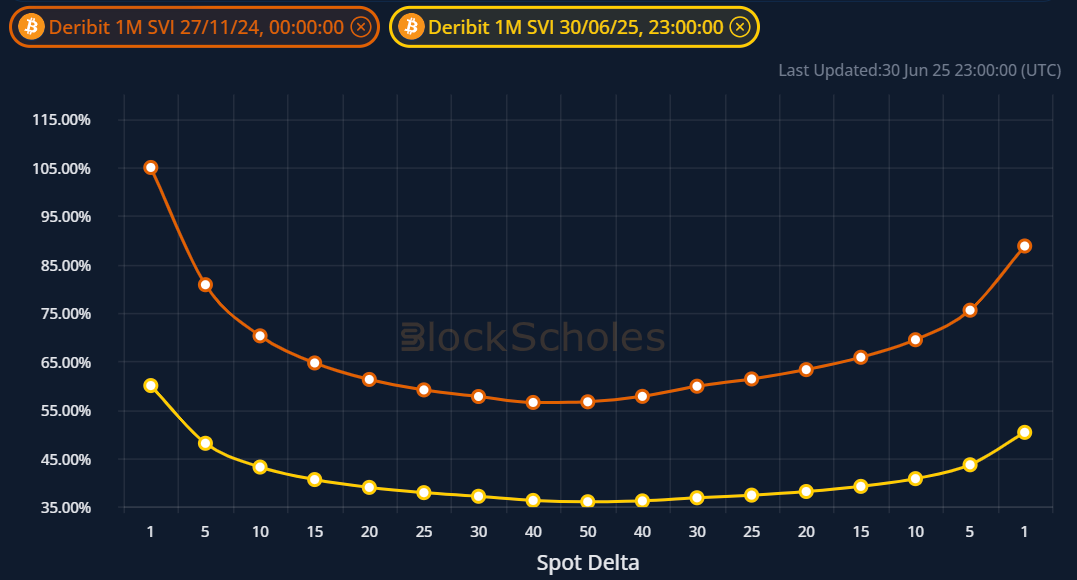

The steepness in the wings of the volatility smile is a helpful clue to answering this question. Steepness can be thought of as a way to show how high the wings of the volatility smile are, relative to the at-the-money level of volatility. A steep volatility smile means that markets are implying a large premium on out-of-the-money options, as traders believe large spikes in the underlying spot price are likely to occur.

Figure 14 showcases two different snapshots of BTC’s volatility smile for 30-day options. The orange line is timestamped Nov 27, 2024, when BTC and the wider altcoin market had exploded following President Trump’s election victory and BTC’s spot price had come within inches of $100K. However, as traders continued to take profits close to those levels, BTC fell back sharply from $99K to $91K. Meanwhile, 10-delta BTC options were trading with an IV premium of 13.6% relative to the at-the-money level. We can compare this to the far shallower smile, timestamped Jul 1, 2025, when BTC was trading range-bound between $106K and $109K, and out-of-the-money optionality wasn’t trading with a significant implied volatility premium to at-the-money options.

We can also measure the steepness of the smile over time using a tuning parameter in the volatility smile (“b”, left-hand axis). For BTC, we notice the trend of a shallower volatility smile since 2022. However, we also see that during the 2023 bear market, there was a long period of time during which the steepness of the volatility smile neither increased nor decreased. In January 2024, however, the smile shallowed significantly and has since continued to fall, dropping to 0.05 in July 2025.

This suggests that, over time, options markets appear to be assigning a lower probability to extreme BTC moves in either direction, relative to moves close to the current spot price — hence, a flatter volatility smile. OTM puts and calls are trading with an IV closer to the ATM level, meaning that traders are demanding a smaller premium for big moves, higher or lower, relative to the premium for smaller, more typical returns.

July 2025 saw a continuation of a narrative we first covered back in May 2025 — one in which BTC continues to print new ATHs, and yet does so with historically low levels of realized and implied volatility. In comparison, ETH continues to trade with higher volatility, and Ether options traders are still showing an appetite for pushing up ETH options prices during big market moves. This dynamic drove the ETH/BTC IV ratio for 30-day options to its highest level since 2020. However, unusually, this occurred despite the two assets’ realized volatility ratios softening throughout the same period, though only temporarily.

At the same time, BTC’s volatility smile has continued to flatten, consistent with the trend we highlighted following the launch of BTC Spot ETFs in early 2024. Out-of-the-money options, once priced with a significant premium, are now trading with IVs far closer to at-the-money levels, suggesting that traders are demanding a smaller premium for big moves (higher or lower), relative to the premium for smaller, more typical returns. This contrast is even more apparent when compared to ETH, whose implied volatility levels are far higher, as the IV ratio between the two majors continues to steepen across tenors.

.jpg)

.jpg)