Andrew Melville

Head of Research

An aggressive rally in BTC’s spot price over the past week has seen the largest cryptocurrency by market capitalization surge to multiple new all-time highs, eventually touching a top of $123K. With that move higher, all measures of directional sentiment in derivatives markets supported the rally, as funding rates for BTC have been persistently positive and options skew is tilted toward calls. SOL has once more underperformed relative to a basket of Layer 1 (L1) blockchains this week, despite several bullish tailwind drivers in the form of positive inflows in the REX-Osprey SOL ETF and a number of corporations adopting or expanding a SOL-focused treasury strategy, including DeFi Development Corp. and Mercurity Fintech Holding Inc.

An aggressive rally in BTC’s spot price over the past week has seen the largest cryptocurrency by market capitalization surge to multiple new all-time highs, eventually touching a top of $123K. With that move higher, all measures of directional sentiment in derivatives markets supported the rally, as funding rates for BTC have been persistently positive and options skew is tilted toward calls. SOL has once more underperformed relative to a basket of Layer 1 (L1) blockchains this week, despite several bullish tailwind drivers in the form of positive inflows in the REX-Osprey SOL ETF and a number of corporations adopting or expanding a SOL-focused treasury strategy, including DeFi Development Corp. and Mercurity Fintech Holding Inc.

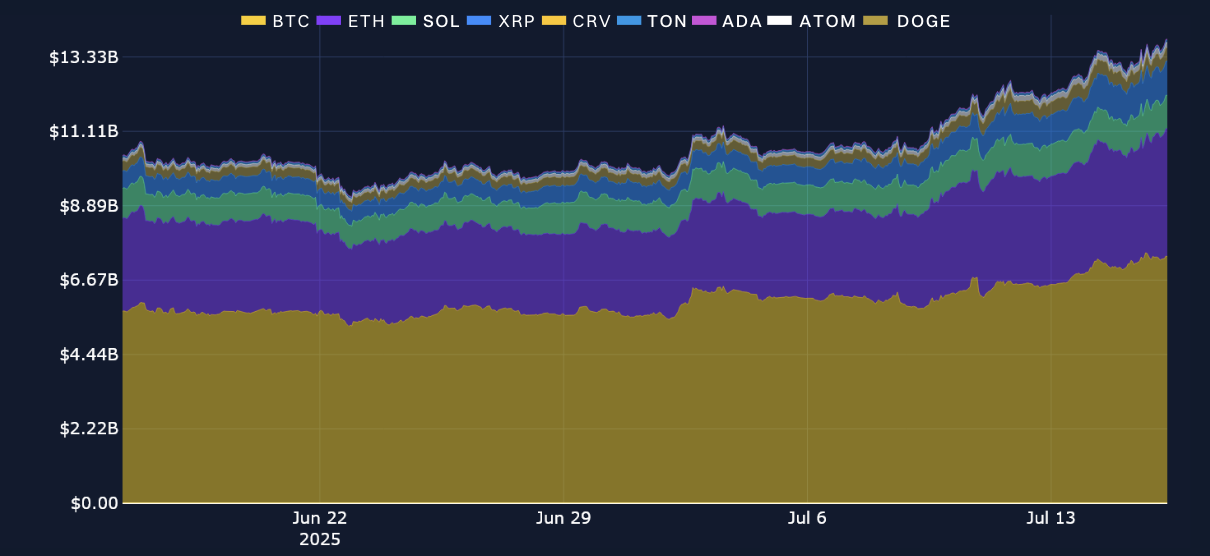

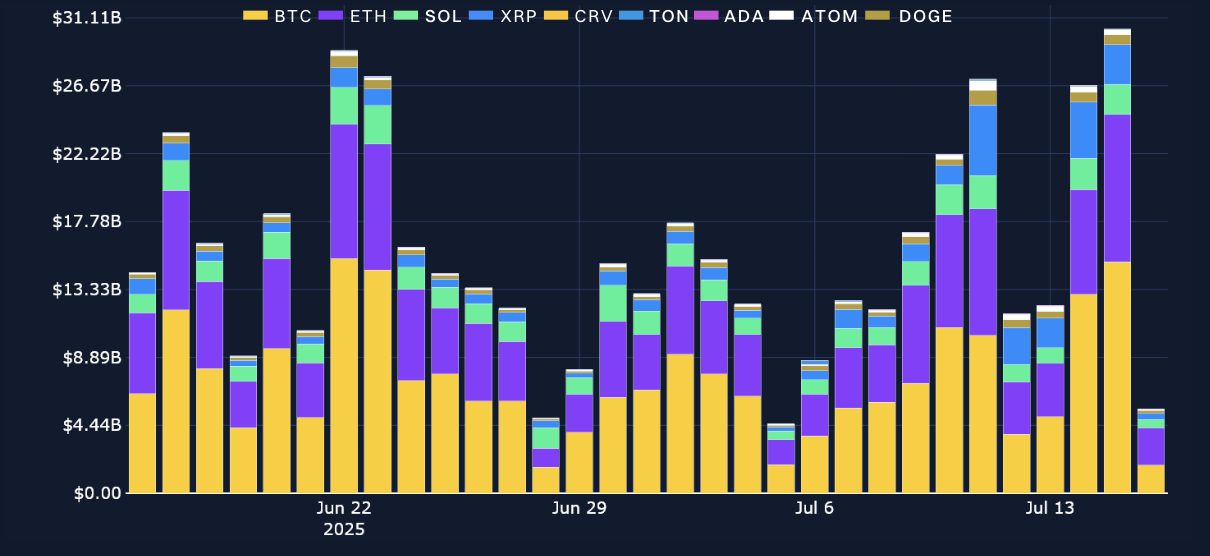

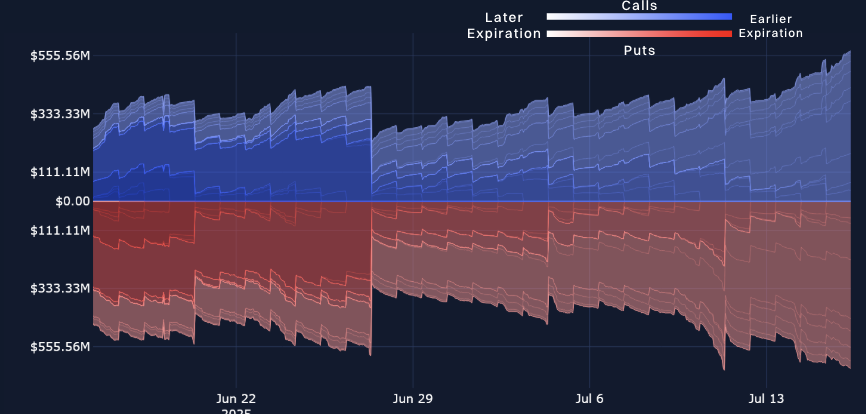

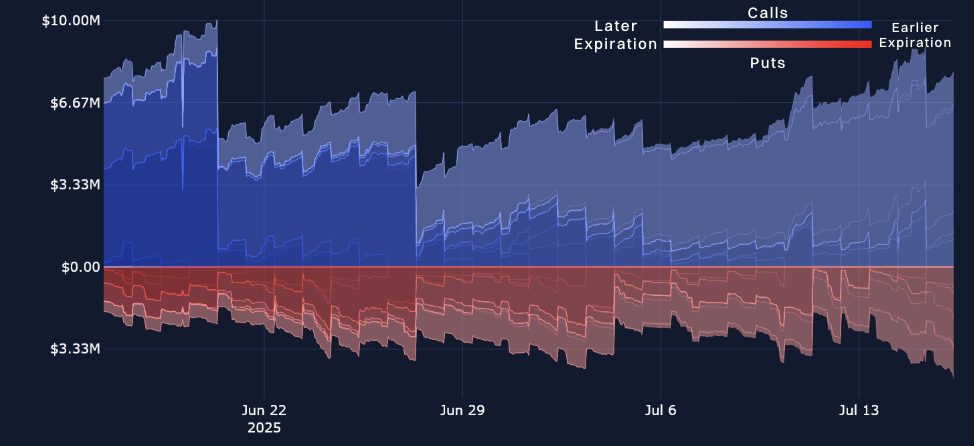

Perpetuals: Open interest has soared past $13B, a new high for the month of July, as BTC rose to $123K and ETH regained $3K for the first time since early February 2025.

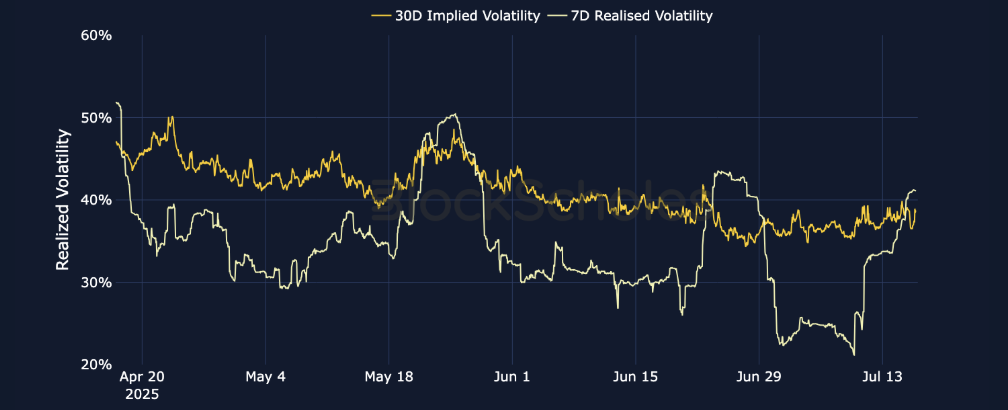

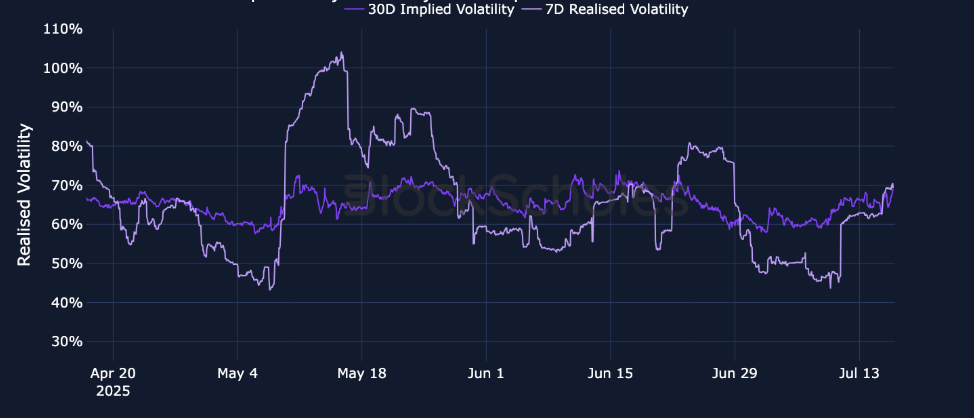

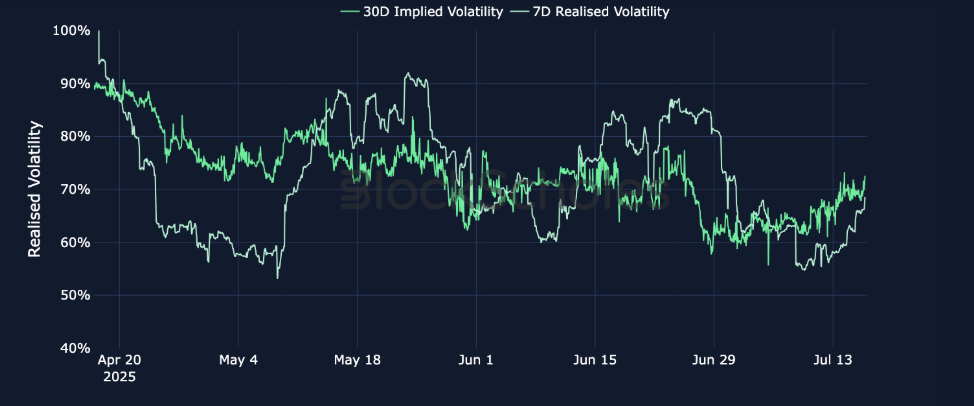

Options: The implied volatility of short-tenor BTC options broke out of last week’s 25–35% range, reaching a high of 41% before falling down again, as traders took profits at historic highs, pulling BTC back to $118K.

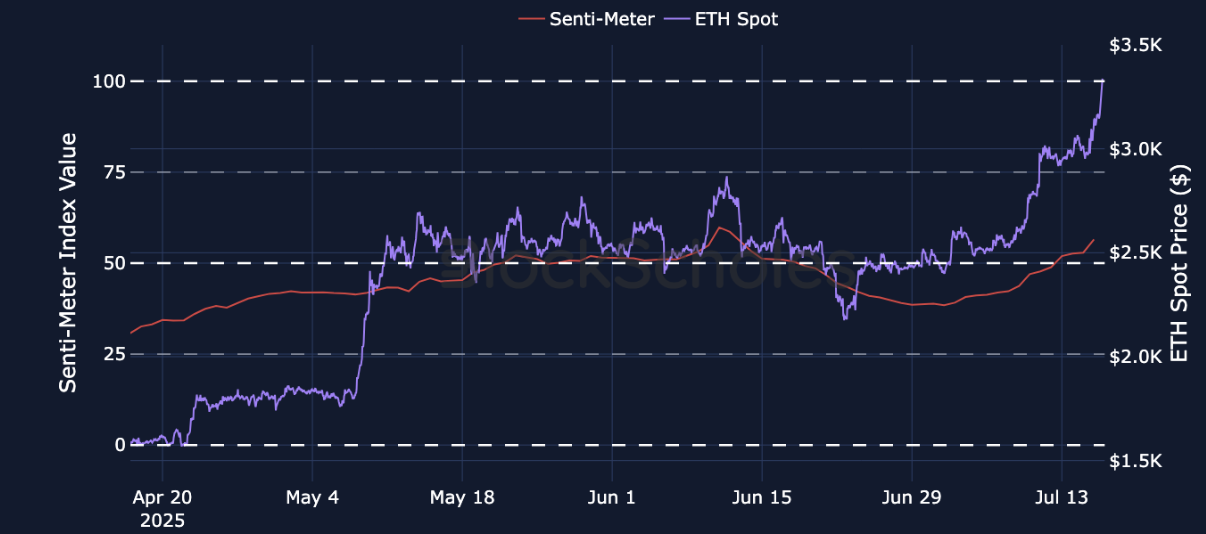

Block Scholes’s Senti-Meter Index aggregates the funding rate, future-implied yield and volatility smile skew into a single expression of sentiment in derivatives markets. See more in the methodology article here.

After ranging sideways at $108K between Jun 24–Jul 8, 2025, the past week saw BTC break out of its range aggressively. With that breakout, the spot price of the largest cryptocurrency by market cap rose to touch multiple new all-time highs:

As such, open interest has far exceeded the highs we saw in June, and currently amounts to over $13B. That increase in open interest from last week hasn’t just been concentrated in BTC, either: ETH, SOL, XRP and other major altcoins have seen their open interest increase. Trading volumes on the day BTC touched $123K exceeded $27B — volumes we last saw on Jun 22, 2025, when US President Trump confirmed that the US military had struck three key Iranian nuclear facilities.

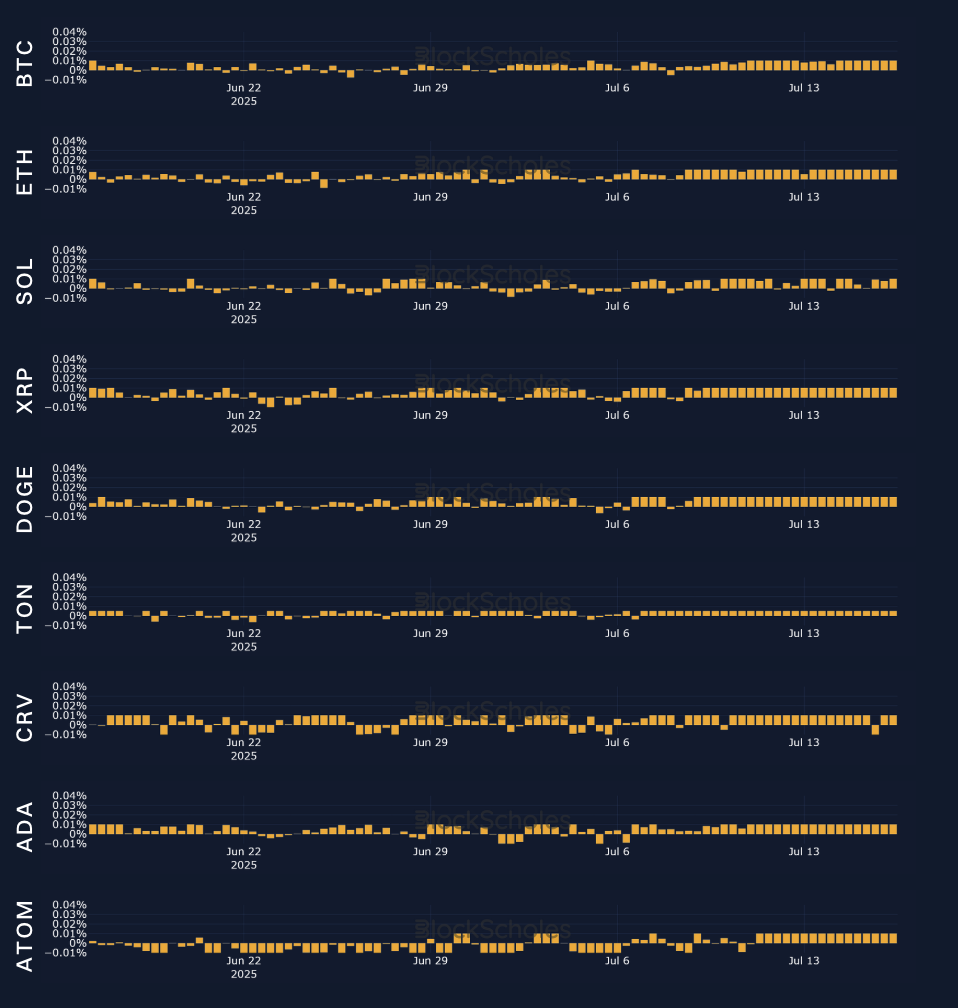

In last week’s commentary, we noted that after several weeks of mixed funding rates, the first week of July saw traders portraying a stronger conviction for higher spot prices, leading to more consistently positive funding rates. This week, if you weren’t aware that BTC had made multiple new all-time highs, funding rates for perpetual swap contracts may have given a sign that a big market move had taken place.

Across the board we’ve seen even stronger positive funding rates. For BTC, ETH, XRP, TON, DOGE, ADA and ATOM, the past seven days have witnessed the longest consecutive period over the past two months during which traders have shown a willingness to pay for leveraged upside exposure. That makes sense, given that BTC and a slew of the largest altcoins have all rallied between 9% and 30% over the past week, including SOL, which has increased 9%. However, unlike some of the other L1 tokens, SOL’s funding rates haven’t shown the same exuberant, consistently high positive values, with two negative eight-hourly rates even being registered since July 7, 2025. That may be a reflection of the fact that despite a 9% return over the past week, SOL has been outperformed by most L1s: over the same period, ETH is up 21%, XRP is up 26% and ADA is up 27%.

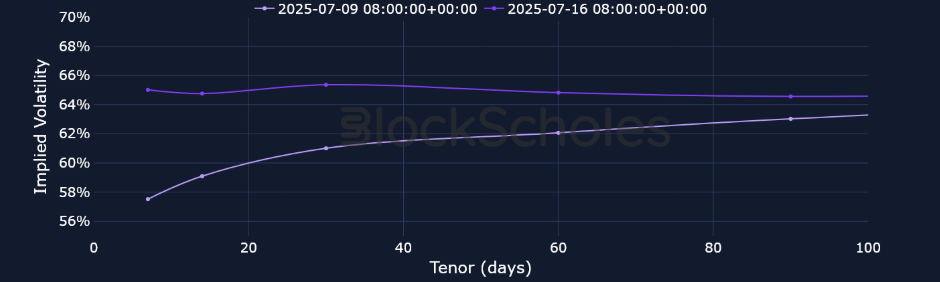

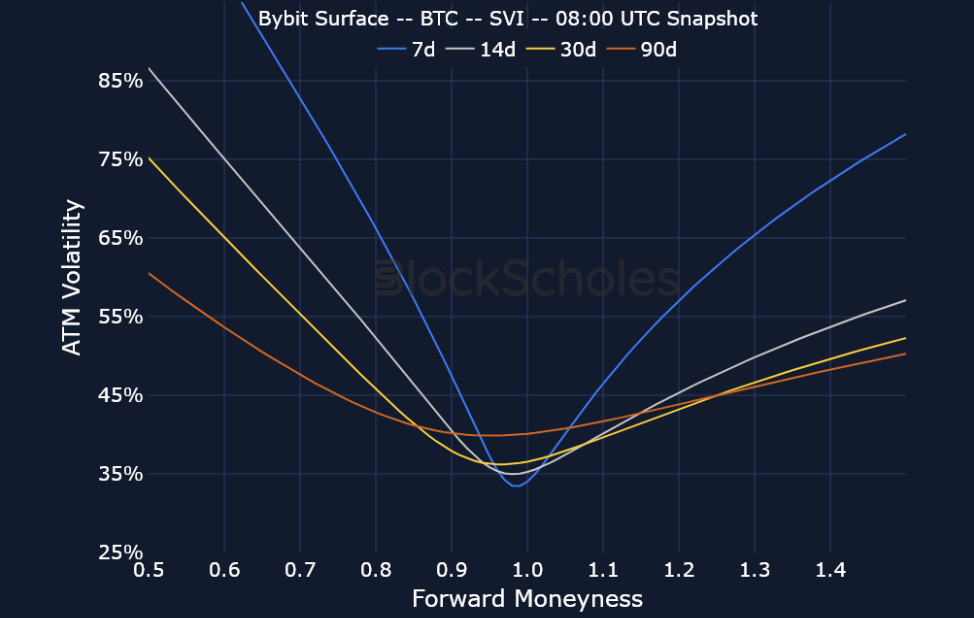

During the first week of July, the at-the-money (ATM) implied volatility premium on 7-day BTC options struggled to break free from the range of between 25% and 35%. This wasn’t due to a lack of macro or crypto related events, either. In fact, a US JOLTS report, a later nonfarm payroll report and also a trade deal made between the US and Vietnam still failed to spur a larger increase in the implied volatility of short-tenor BTC options.

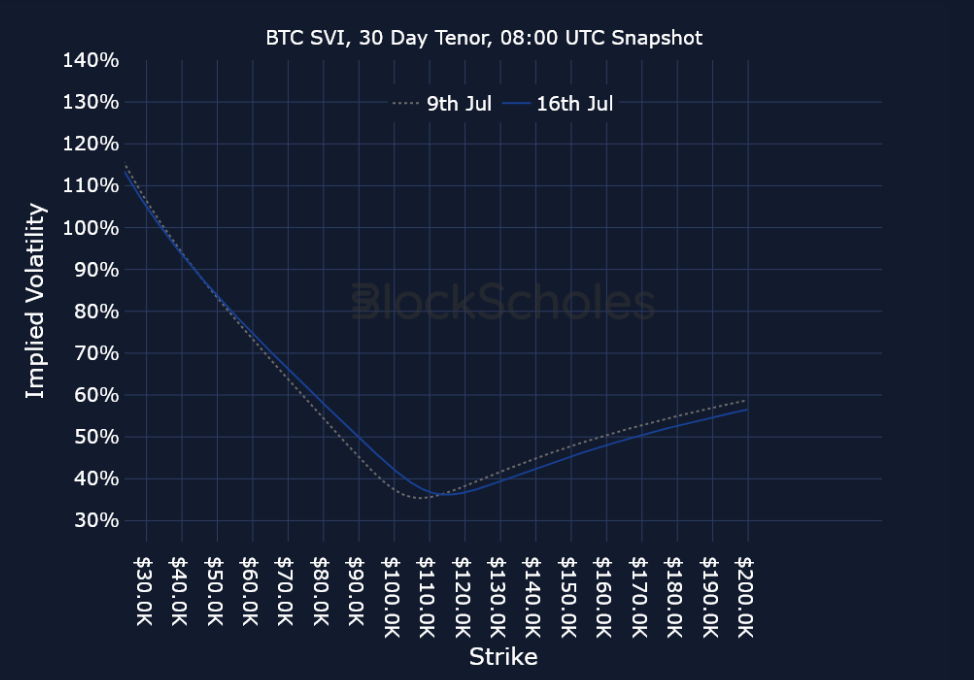

However, the past week’s aggressive spot rally from $108K to $123K was able to at least partly buck the trend. On Jul 13, 2025, as BTC was trading around $118K, the implied volatility on a 7-day BTC option shot up from 32% to 41%. As BTC’s price passed $120K, volatility remained in the upper 30% region. The move was ultimately short-lived, however, as traders sought to take profits at historically high levels and BTC’s spot price pulled back to $116K, falling 5% on Jul 15, 2025. With that move down, implied volatility levels once again fell toward the low 30s (now currently at 33%). Thus, we’re once more in an environment in which BTC’s spot price is historically high while the implied volatility of its options is close to historically low levels.

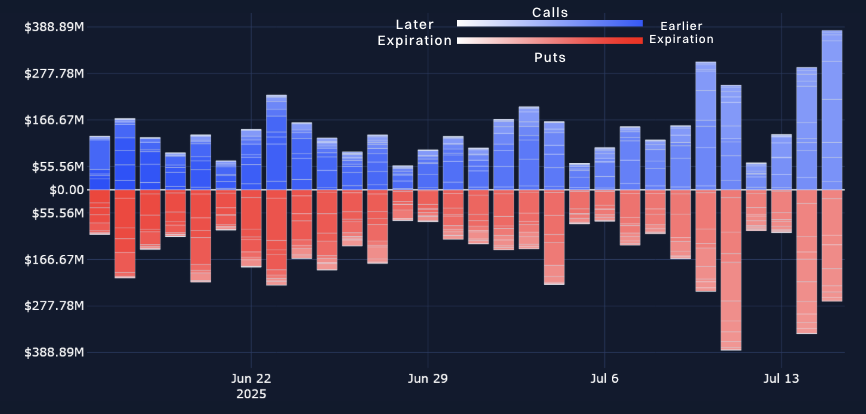

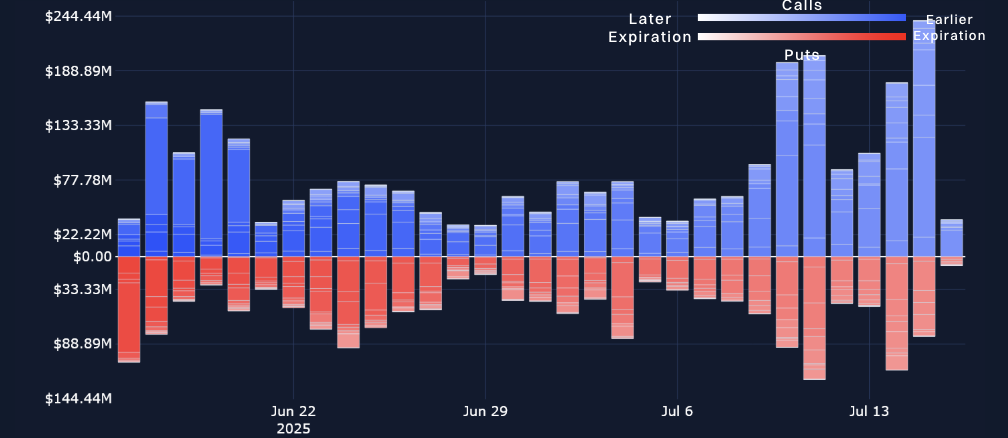

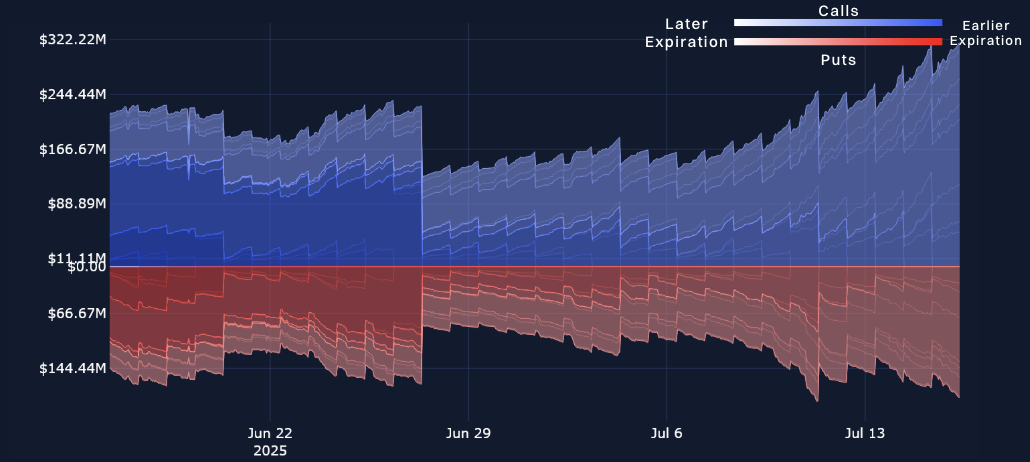

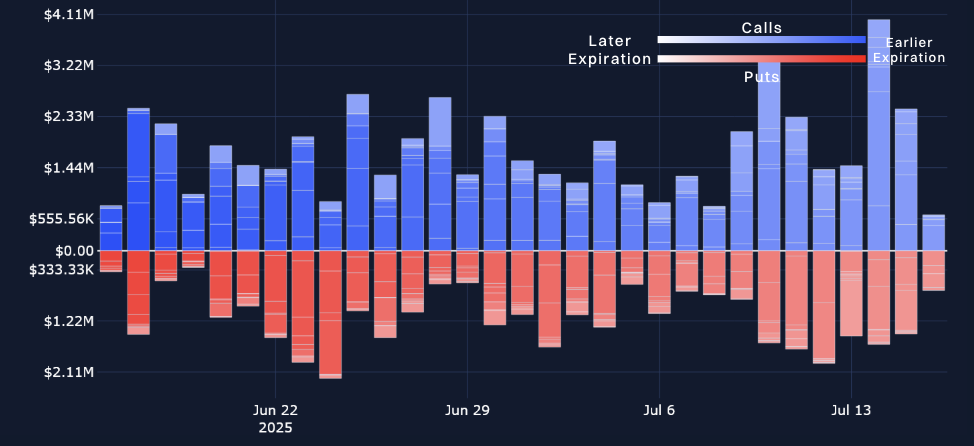

Nonetheless, after weeks of options volume and open interest being dominated in puts, this week a more-than-$200M increase in open interest for calls has now nearly balanced the open interest between calls and puts — and yesterday (Jul 15, 2025), options volumes in calls exceeded that of puts by $100M.

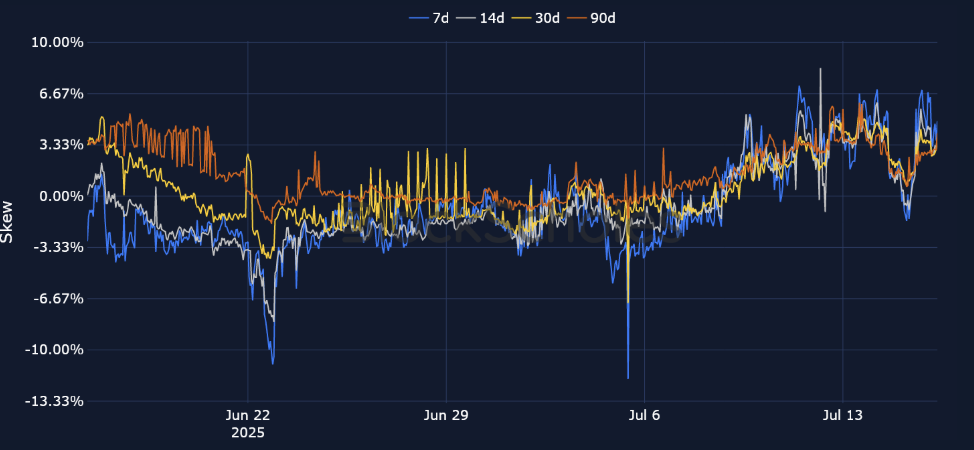

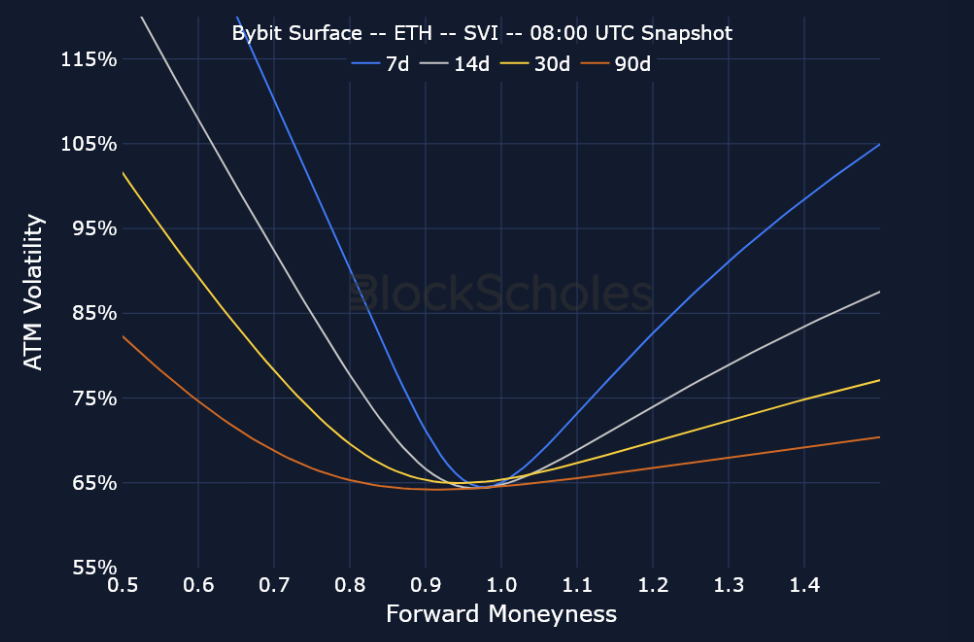

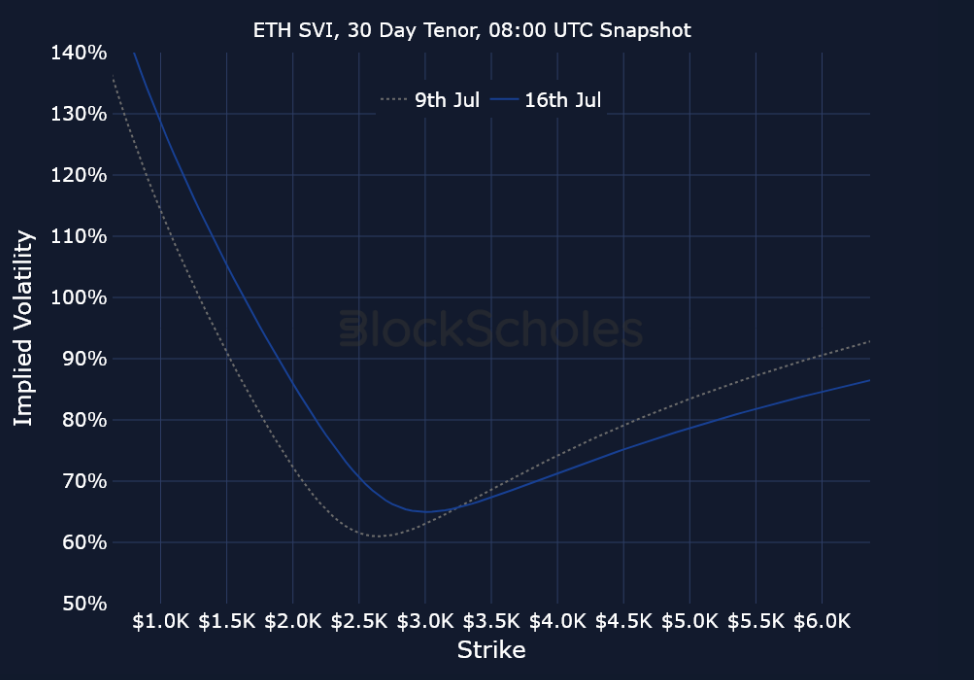

For the first time since early February 2025, ETH has regained an important psychological price point of $3,000. Today, it’s up more than 5%, and over the past seven days more than 20%, with its spot price currently trading at $3,150. Additionally, over the past week, implied volatility for short-tenor ETH options has surged higher. From Jul 8–16, 2025, the implied volatility premium on a 7-day ETH option has increased from 54% to 71%. Various directional measures of sentiment in derivatives markets all support a further rally in ETH, with skew tilted nearly 5% toward OTM calls for shorter maturity options, funding rates consistently positive and a positive yield on ETH futures contracts above spot price.

Options volumes exploded higher over the past week, and open interest is now once more dominated more than 2x by call options (relative to the open interest for puts).

As we highlighted in last week’s commentary, the Solana ecosystem continues to be bolstered by positive developments, yet it’s still underperforming a basket of other large L1 blockchains. Over the past week SOL has returned 9%. However, alternative L1 blockchains such as SUI are up 37%, and ETH has returned more than 20%.

On July 10, 2025, DeFi Development Corp. (DFDV) purchased 153,225 Solana tokens, bringing its total SOL holdings to 846,630 SOL. The company also announced plans to hold 1 SOL for every share of DFDV by the end of 2028. Separately, on Jul 14, 2025, Mercurity Fintech Holding Inc., a blockchain fintech company, announced plans to launch a $500M “DeFi Basket” Treasury with an initial focus on acquiring Solana tokens. Finally, as of its launch on Jul 2, 2025, the REX-Osprey SOL Staking ETF has seen only one day of outflows.

Despite a smaller increase in price relative to some of SOL’s competitors, however, call options volumes continue to dominate put volumes in SOL options, and open interest remains above $6M for calls.

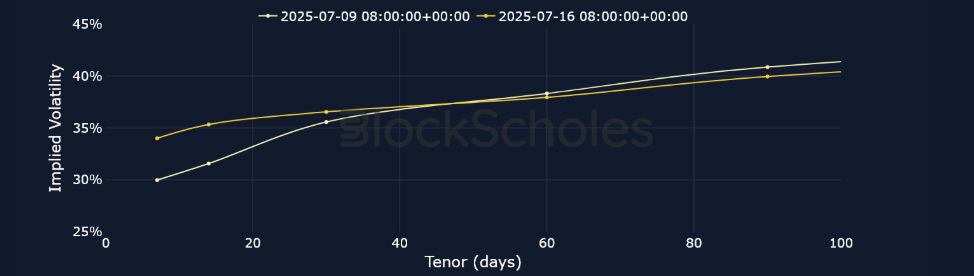

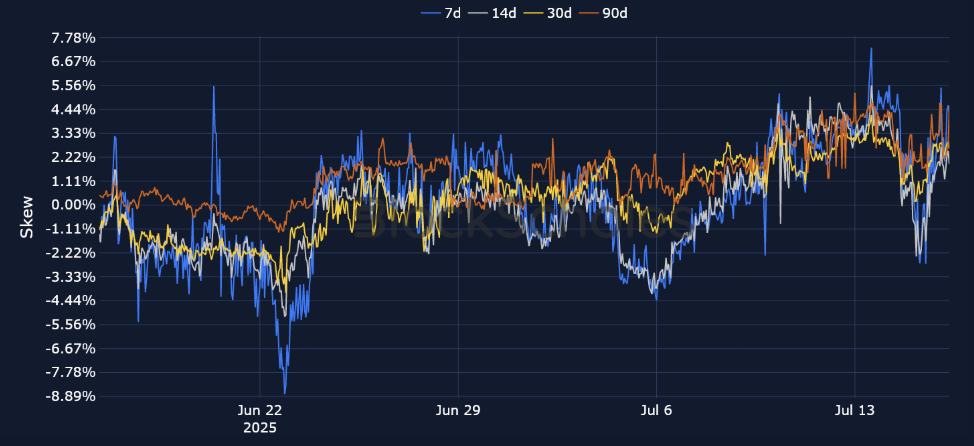

In line with BTC’s spot price, short-tenor BTC volatility smiles have gone through a whirlwind of sentiment changes. As BTC’s spot price first broke $120,000, OTM calls options traded with a 7.3% volatility premium relative to similar maturity OTM put options. And as its spot price fell from those highs, testing $116K, short-tenor smiles changed winds to favor OTM puts, with the put-call skew falling as low as −2.7%. However, just as quickly as it fell, it’s recovered, with traders now favoring OTM calls by 4.2%. That also currently matches the sentiment shown in BTC perpetual futures markets. However, unlike skew, funding rates have consistently shown a bullish picture over the past week.

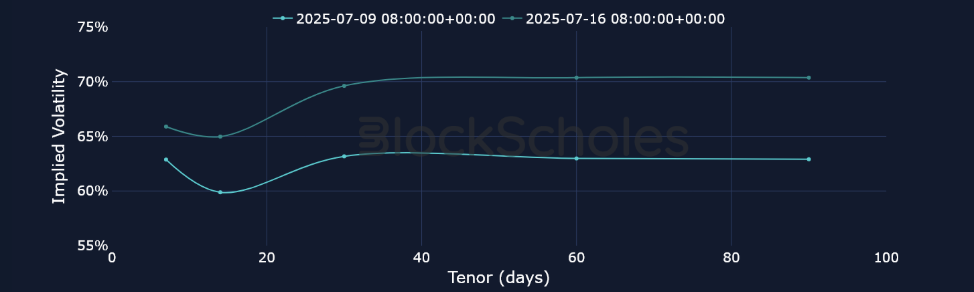

As ETH’s spot price has outperformed, its volatility smiles are slightly more skewed toward call options relative to BTC options. For example, the put-call skew for a 7-day ETH option is currently 4.9%. For longer tenors, however, such as 90 days, BTC call options carry a more positive skew.

Open interest and trading volume data are sourced “as is” from the Bybit exchange platform API exclusively, and as such do not represent a comprehensive picture of the sum of trading activity across all derivatives markets or exchanges. The data visualized in this report consists of hourly and daily snapshots, recorded over the previous 30 days. Daily (hourly) snapshots of trade volume record the total sum of the notional value of trades recorded in the 24H (1 hour) period, beginning with the snapshot timestamp.

If not explicitly labeled as derived from another exchange, the input instrument prices to all derivatives analytics metrics in this report are sourced from the appropriate endpoints of Bybit’s public exchange platform API. In the event that data is labeled or referred to as representing the market on another exchange source, that data is sourced from the appropriate endpoint of each respective exchange’s public API.

Macroeconomic charts and data are sourced “as is” from the Bloomberg Terminal. Exchange data is sourced “as is” from publicly available exchange APIs. Block Scholes makes no claims about the veracity of public third-party data.

After acquisition of underlying-denominated raw data for open interest and trading volume on the Bybit exchange platform from Bybit’s API endpoint, equivalent dollar-denominated figures are calculated using the concurrent value of Block Scholes’s Spot Index for the relevant underlying asset.

Block Scholes’s Spot Index represents the aggregate Spot mid-price for a given currency across the top five CEXs by volume (with USD-quoted markets). It considers the proportion of total volume in the instrument on the exchange, as well as the deviation of a data point from those on other exchanges.

Futures prices are used for Block Scholes’s futures-implied yields calculation services in order to derive the constant-tenor annualized yields displayed in the Futures section of this report.

Options prices are used for Block Scholes’s implied volatility calculation services in order to calibrate volatility surfaces, from which all derivatives volatility analytics displayed in the BTC Options and ETH Options sections of this report are calculated. Volatility smiles are constructed by calibrating to mid-market prices observed in Bybit options markets. As part of the calibration process, prices go through rigorous filtration and cleaning steps, which ensures that the resulting volatility surface is arbitrage-free and has exceptional fit to the market observables.

.jpg)

.jpg)