Thahbib Rahman

Research Analyst

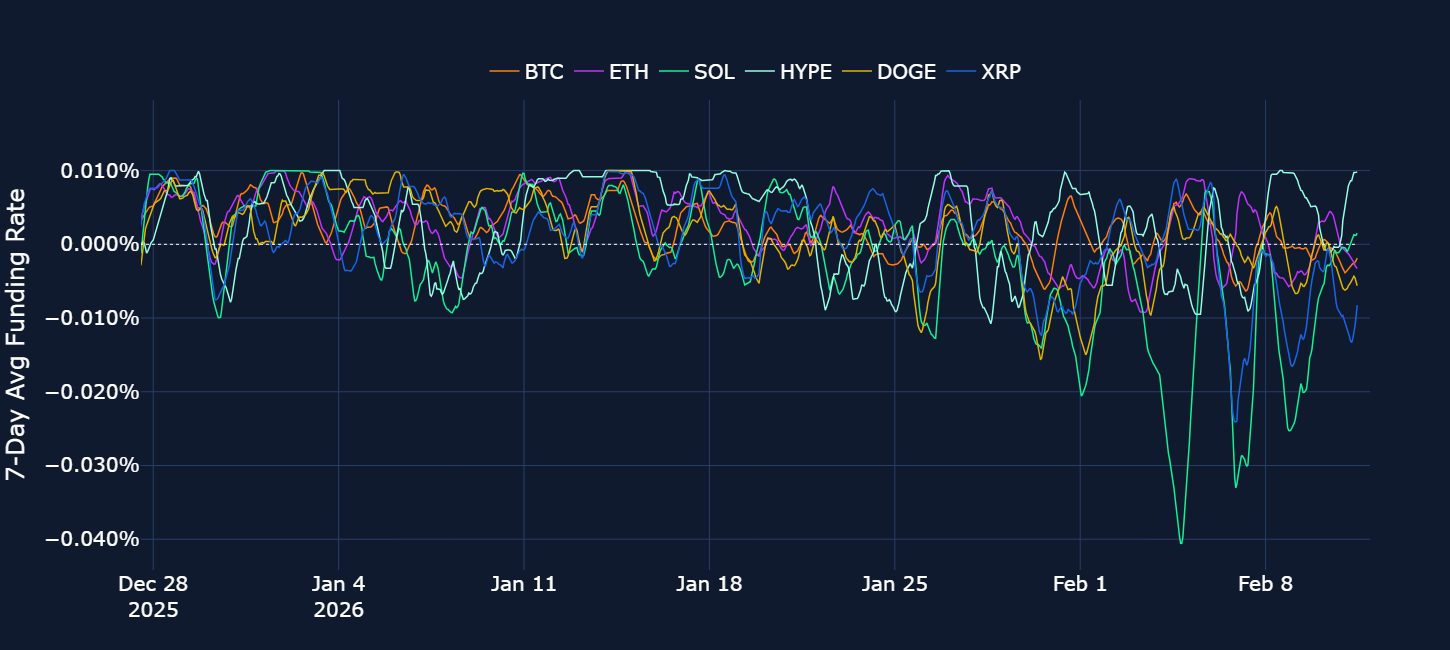

After last Thursday’s flash crash pushed BTC briefly to $60K, sentiment in derivatives markets has soured further. Short-dated BTC and ETH implied volatility surged to levels last seen during the collapse of the FTX exchange in November 2022, as the demand for downside protection against further drops in spot price rose to multi-year highs. The 50+% drawdown in BTC from its October 2025 all-time high dragged the rest of the crypto market down with it – with ETH falling below $2,000 and SOL returning to 2023-levels. Funding rates across the majority of large-cap altcoins turned negative, with the 7-day average funding rate for SOL falling to its lowest since the October 10, 2025 liquidation.

After last Thursday’s flash crash pushed BTC briefly to $60K, sentiment in derivatives markets has soured further.

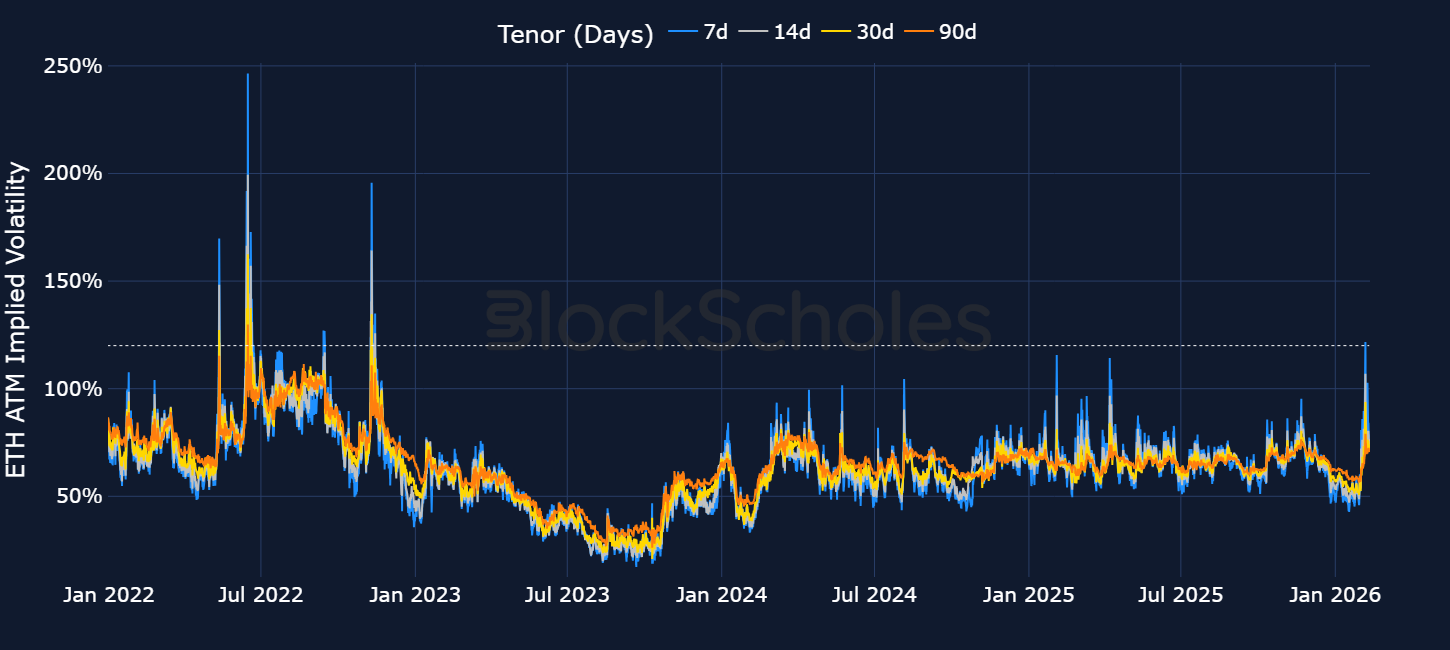

Short-dated BTC and ETH implied volatility surged to levels last seen during the collapse of the FTX exchange in November 2022, as the demand for downside protection against further drops in spot price rose to multi-year highs.

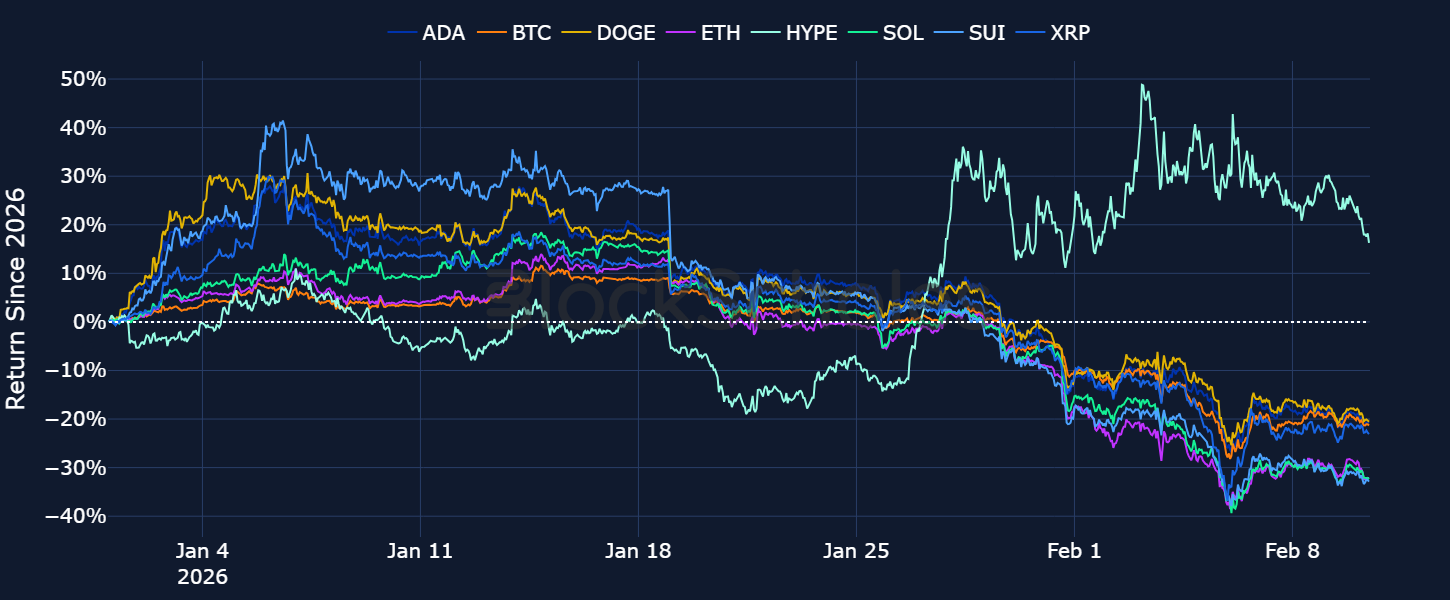

The 50+% drawdown in BTC from its October 2025 all-time high dragged the rest of the crypto market down with it – with ETH falling below $2,000 and SOL returning to 2023-levels. Funding rates across the majority of large-cap altcoins turned negative, with the 7-day average funding rate for SOL falling to its lowest since the October 10, 2025 liquidation.

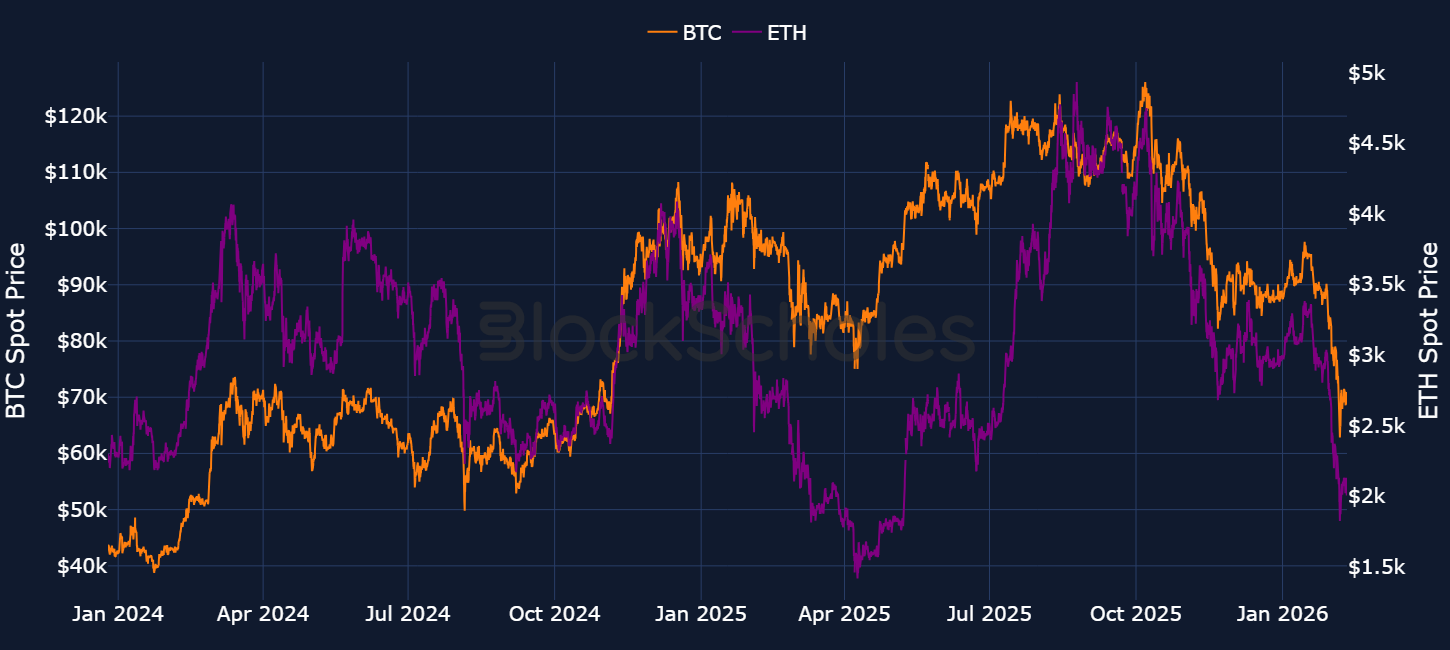

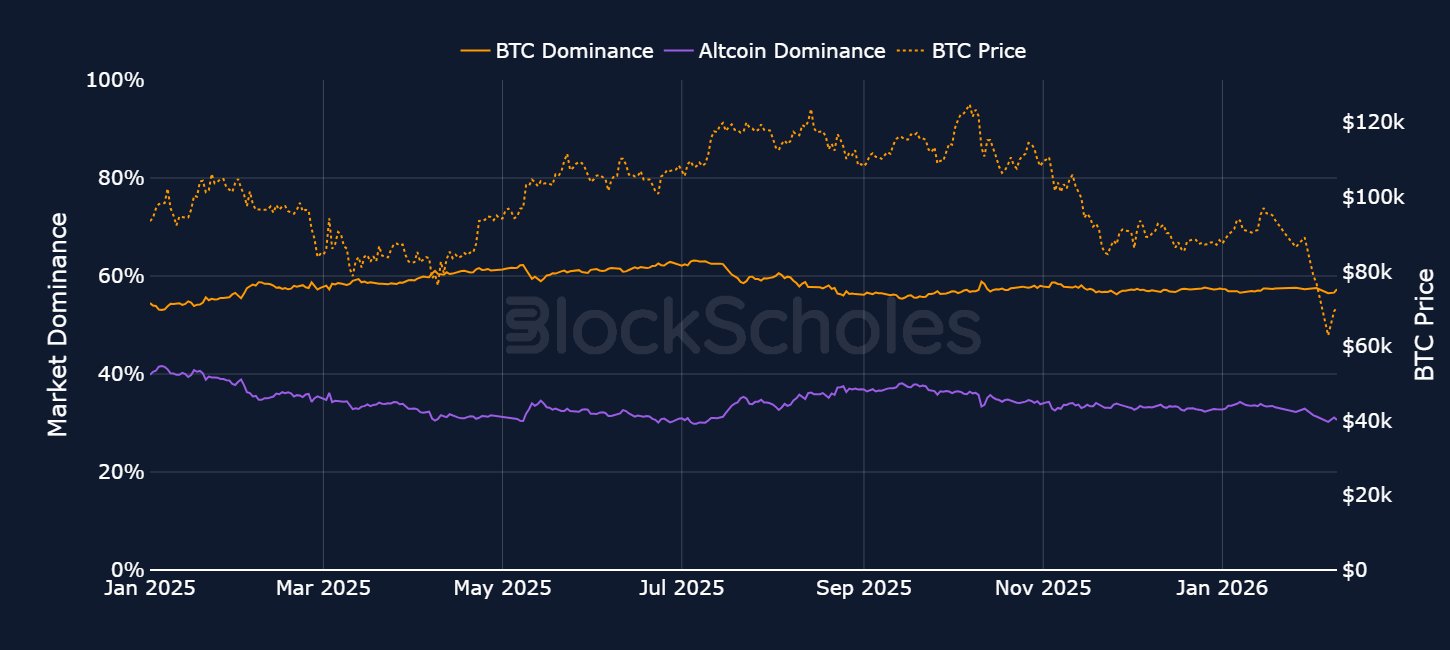

Notably, BTC dominance has held steady despite the drawdown, with capital flowing out of the broader crypto market proportionally rather than rotating into Bitcoin as a relative safe haven. Altcoin dominance, meanwhile, has continued its decline from ~36% in October to ~30% - with large-caps like ETH, XRP, and BNB all down over 60% from their highs and SOL down more than 70%.

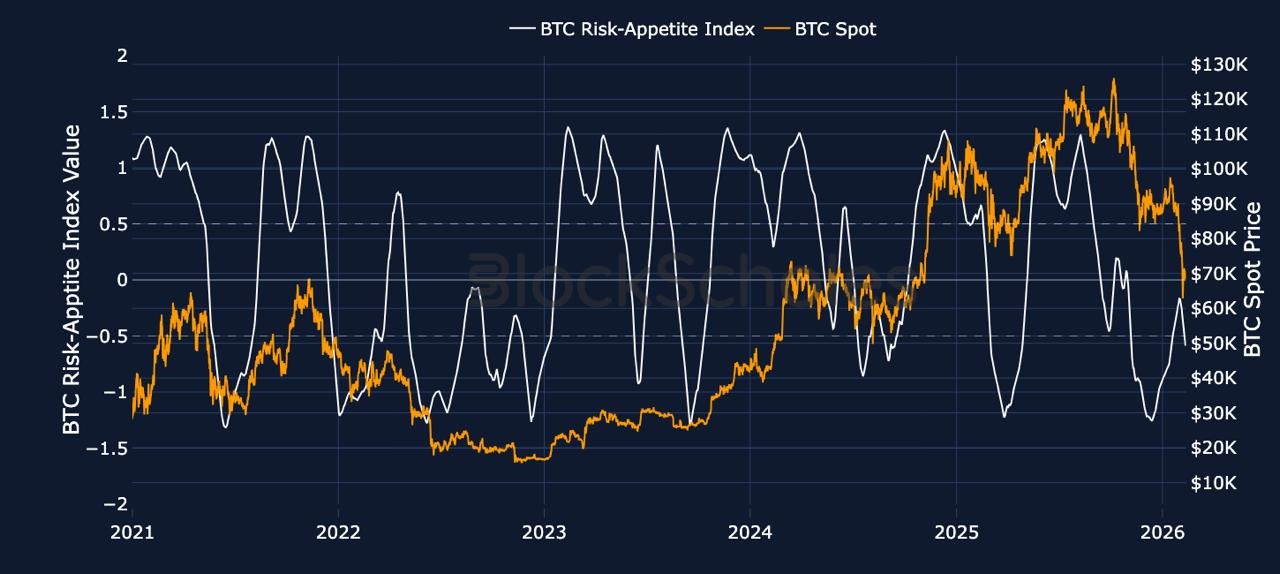

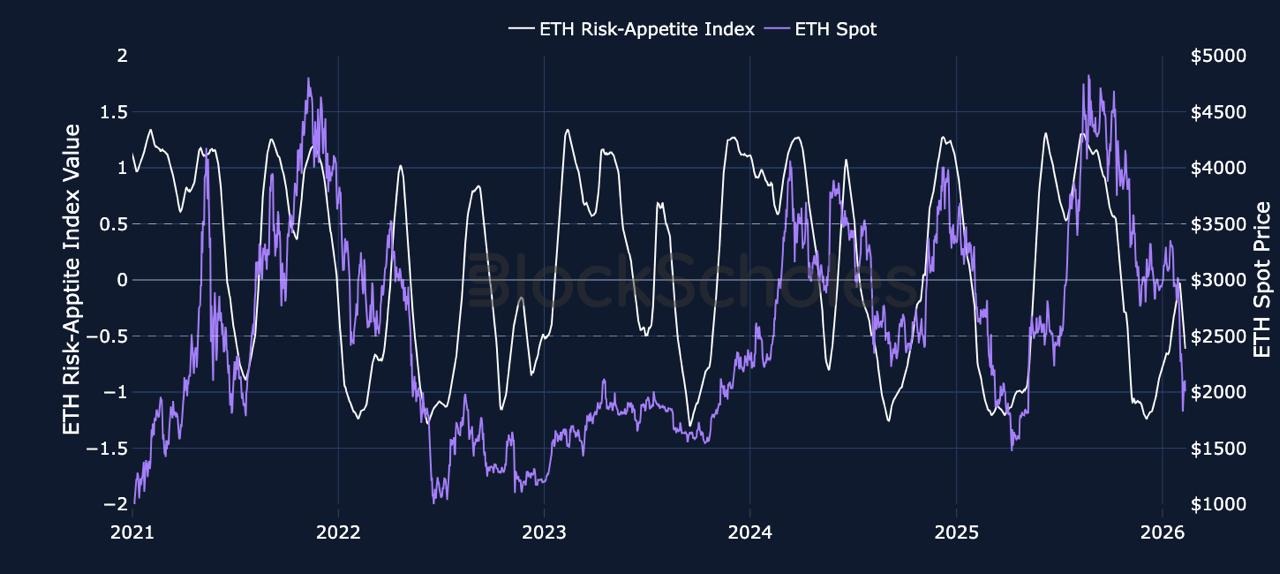

Block Scholes’ Risk Appetite Index measures the level of euphoria (above 1) or panic (below -1) in the spot market. Momentum in this index shows a strong relationship to spot returns.

The past week has seen major whipsaws in spot prices that have taken their toll on derivatives markets. On Thursday Feb 5, 2026, Bitcoin saw its largest single-day drawdown since the collapse of the FTX exchange in November 2022, briefly touching = $60K and erasing all of its post-Trump 2.0 gains. On Friday, it then recovered almost all the previous day’s losses just as fast and rallied back above $70K – a level it has since consolidated around for most of this week.

In last week’s edition of our report, we mentioned that while sentiment in derivatives markets had clearly weakened, options traders had yet to price in the same levels of panic or volatility that had coincided with previous major downturns in spot prices.

As BTC fell briefly wicked down to the $60K handle, however, that changed.

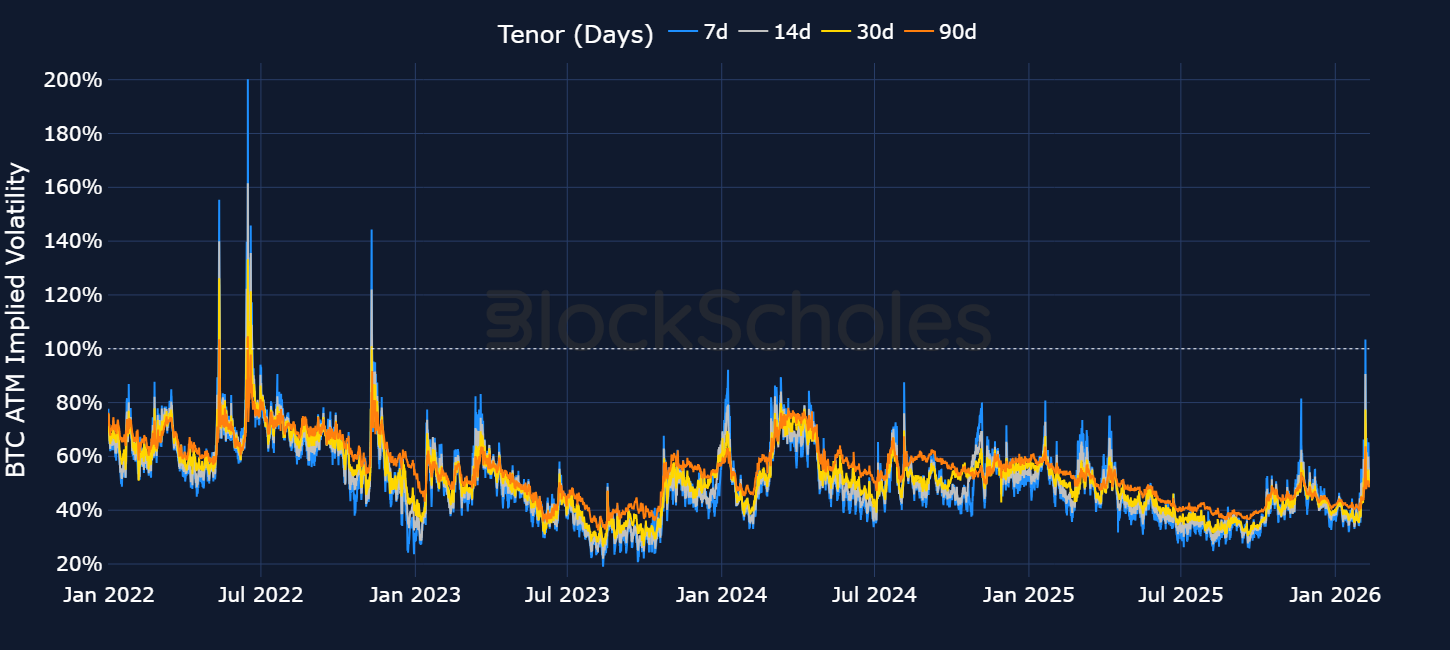

At-the-money implied volatility, a measure of forward looking volatility expectations, rose to its most elevated levels since the November 2022 crypto crash for BTC, with 7-day volatility exceeding 100% – a clear sign of the heightened demand from options traders for downside protection.

We saw similar moves in ETH options markets too, with short-dated volatility reaching their most extreme since the 2022 bear market crash. Therefore, despite not quite reaching the same levels of demand as back in 2022, a dip to $60K and sub-$1800 for BTC and ETH respectively was enough to significantly increase the price of optionality with traders willing to pay extreme premiums for put options.

Beyond the majors BTC and ETH, sell-side pressure in altcoins has also pushed large blue-chip alts below multi-year support levels. SOL for example is down 38% over the past month, trading at its lowest levels since late December 2023, with digital asset treasury companies that hold the token collectively sitting on more than $1.5B worth of unrealized losses. Additionally, DOGE has pared back all of its gains since President Trump’s election victory and the Department of Government Efficiency provided tailwinds for the token, and is now trading at its August 2024 price. As we mentioned last week, the sole outperformer among major altcoin tokens is Hyperliquid’s HYPE token, which despite suffering losses last week, is still up 16% year-to-date.

As BTC’s spot price dropped to $60K, funding rates across major altcoins turned negative – a sign that short traders were so bearish they were willing to pay a recurring premium to maintain their short positions. That conviction in lower prices was most clear in SOL for example, where the 7-day average funding rate fell to -0.04%, its lowest since the October 10, 2025 liquidation.

Interestingly, despite the major drawdown in BTC’s own price, its funding rates did not turn meaningfully negative during the crash, which could suggest the selloff was concentrated in spot markets, and less driven by leverage or a large number of short traders piling into perpetual futures contracts.

The 'Fat Protocol' thesis originated in 2016, referring to the idea that crypto protocols and base layer networks such as Ethereum and Solana would be valued higher than the application layer built on top of them — i.e., the decentralized applications built on those networks.

The thesis brought forward the notion that the crypto sector consisted of “fat” protocols and “thin” applications. That compared to the internet stack which was composed of “thin” protocols and “fat” applications, with value concentrated in the latter (leading to high valuations of large US tech companies such as the Magnificent-7).

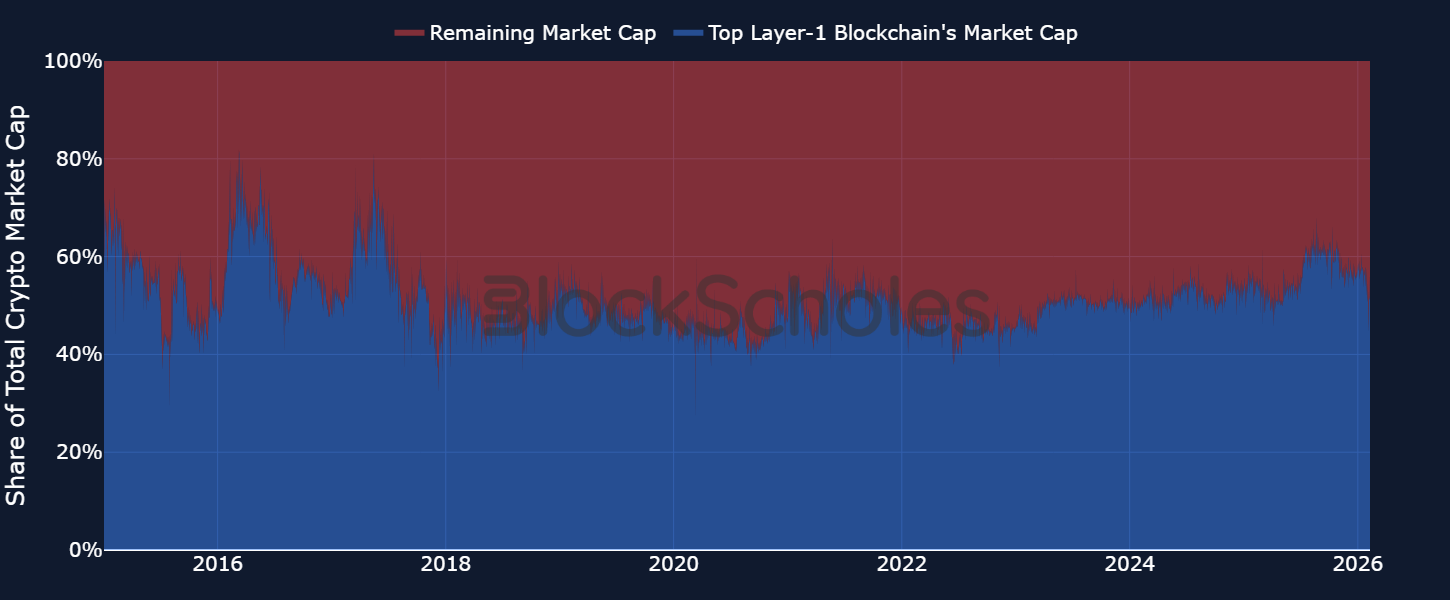

Decomposing the crypto market structure today, we see that the ‘Fat Protocol’ thesis still holds.

Among the top 20 crypto assets by market capitalization, nine are layer-1 blockchains (excluding BTC). Those nine L1 networks have consistently accounted for 50-60% of the total crypto market-cap when removing BTC.

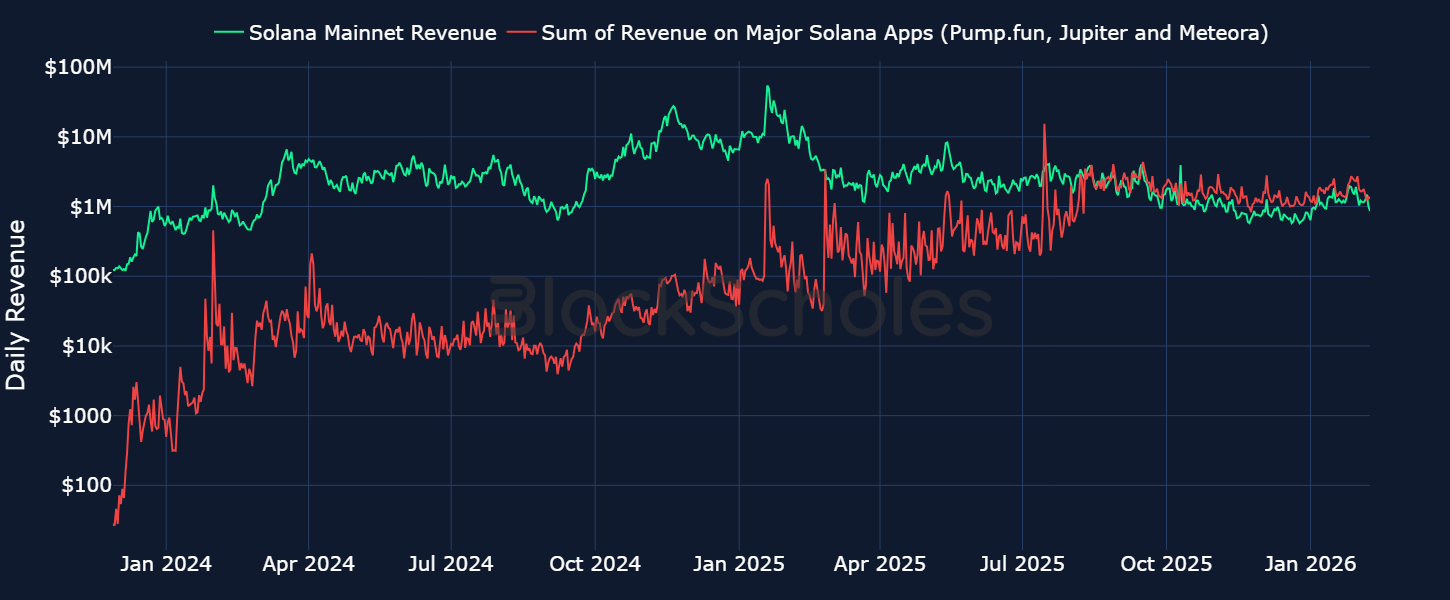

However, when it comes to revenue generation (defined as the portion of fees that accrue to the tokenholder, including the portion of network transaction fees that are passed to holders via token burns - supply reduction which benefits holders passively - and fees paid to validators and stakers), those same base layer protocols have underperformed relative to the applications built on top of them. Major decentralized applications on the Solana network (such as Pump.fun, Meteora and Jupiter) now collectively generate more revenue than the Solana network as a whole.

We see a similar trend between the Ethereum network and some of its major applications. The Ethereum network still generates more revenues than lending protocol Aave, but since Aave’s launch, revenues have grown from $12K to over $250K, while revenues on Ethereum have drifted lower from a peak of $46M down to $400K. Therefore, despite the application layer making up a fraction of total crypto market capitalization, it is trending towards matching (and potentially exceeding) base layer protocols in terms of revenue generation.

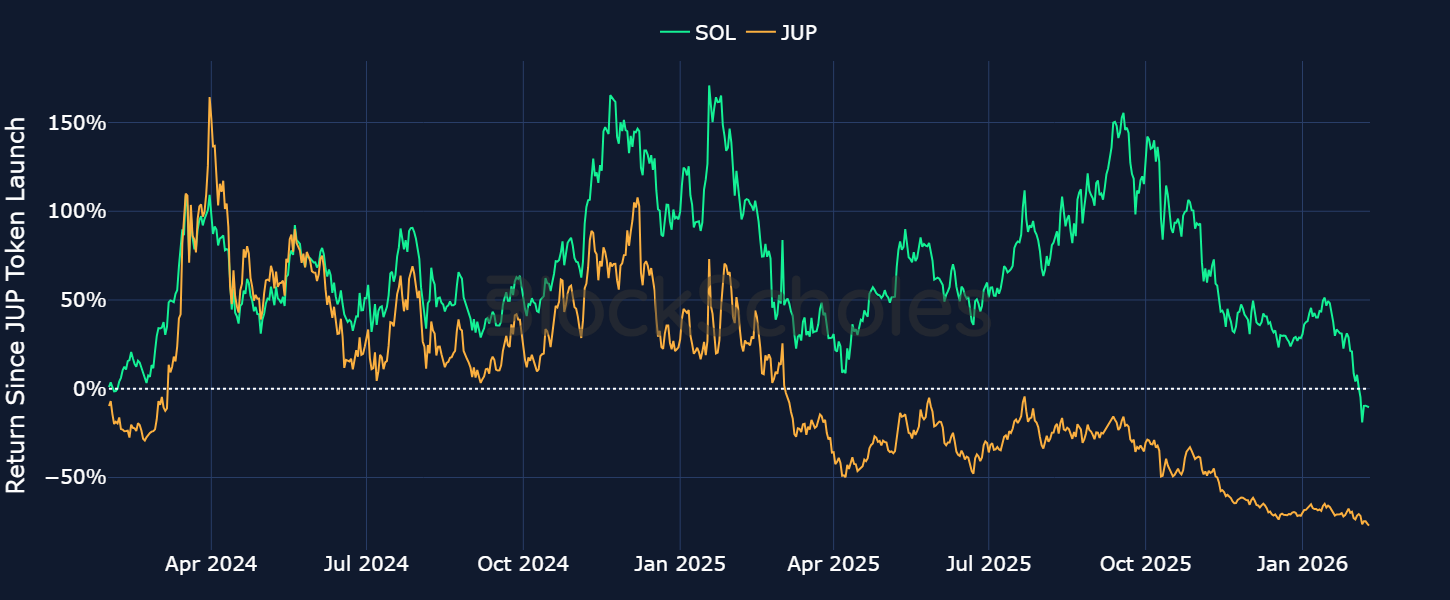

Despite this trend towards revenue outperformance, crypto traders have historically been far better off holding the native token of the network, and not the native token of the application itself; that is, app performance is yet to translate into token outperformance.

For example, when we compare the performance of ETH and the AAVE token since its launch in October 2020 we notice that a holder of AAVE since launch would have doubled their money, while that same holder would have seen a more than 400% gain holding ETH.

The same can be said when comparing the Solana network’s SOL token relative to the tokens of some of the largest applications built on Solana. Take the example of DEX aggregator Jupiter’s JUP token – after a brief period of outperformance during launch, it is down 77%, while holding SOL would have returned a smaller -10%.

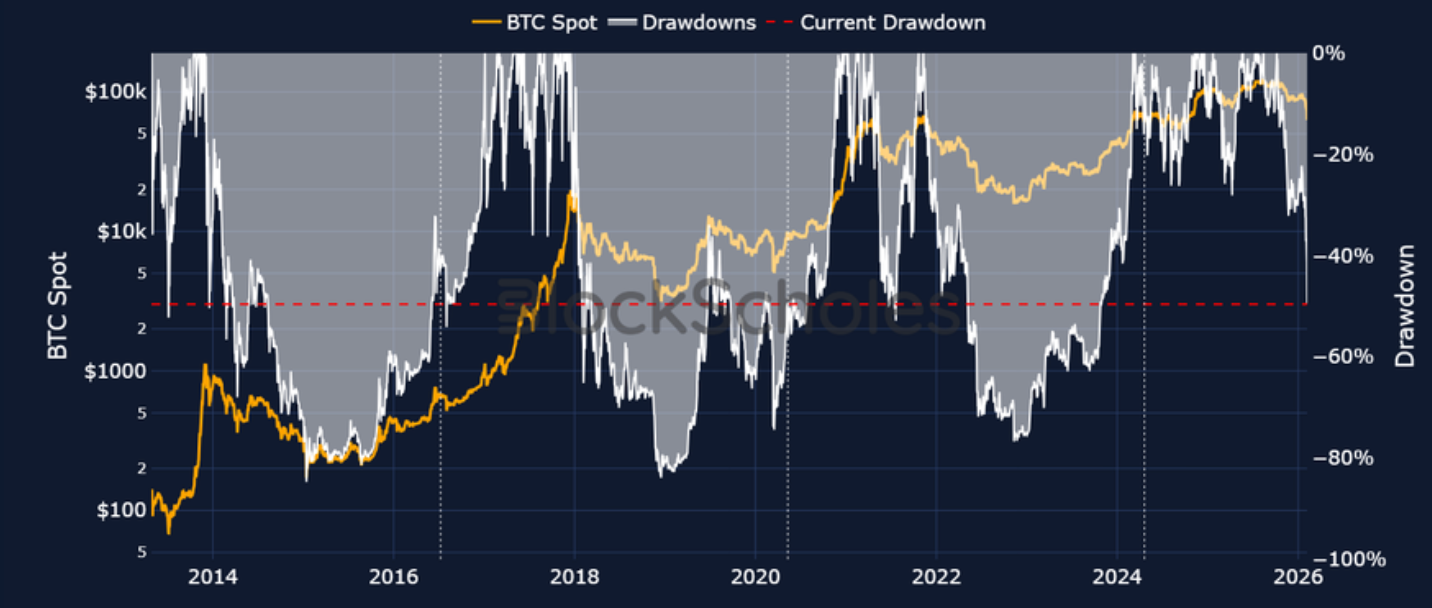

Despite Bitcoin spot drawdowns continuing to decline this week—now sitting at around 50%—we have yet to see levels fall to previous bear market lows. Instead, there are still signs of cautious optimism in the market, particularly as institutional players in crypto continue to operate as usual, releasing updates on business developments while digital asset treasury strategies remain intact, with some even announcing additional token purchases.

However, BTC dominance has not fallen alongside spot price. Instead, capital appears to have flowed out of the broader crypto market proportionally, meaning combined altcoin and stablecoin holdings have declined in line with BTC outflows. This proportional move highlights a wider risk-off sentiment across crypto, rather than signalling a Bitcoin-specific move.

This marks a key difference from previous trends where BTC dominance moves alongside BTC spot.

In comparison, altcoin dominance has been steadily declining since October crypto highs, falling from around 36% to a sharp drop toward 30% alongside the broader crypto market’s downturn. This highlights the lack of meaningful capital rotation from BTC into altcoins. Bitcoin is typically viewed as the “safe-haven” asset within crypto, and when it declines, altcoins tend to fall alongside it, often providing a more leveraged move to the downside. This has been evident in recent performance, with large-cap altcoins such as Ethereum, XRP, and BNB all down over 60% from their all-time highs, while Solana is down more than 70%, and smaller-cap altcoins and memecoins have fared even worse.

Although BTC and the broader crypto market cap have fallen in dollar terms, stablecoins — primarily dollar-pegged assets such as USDT and USDC — are designed to hold a constant $1 value. Consequently, as other crypto assets decline in price, stablecoins account for a larger proportion of the total market capitalization.

Regardless, we have seen a longer-term increase in stablecoin relative market share, even through periods when BTC and altcoins were in bull markets and appreciating relative to the dollar’s fixed value. This reflects the evolving role of stablecoins, driven by increased regulation and years of maintaining their peg. Where stablecoins were once mainly a bridge to bring cash on-chain and transact into tokens—acting as a middleman and extra step—they are now increasingly treated as an on-chain dollar and a store of value, removing the need to move capital off-chain.

It’s intended to simplify payments integration for developers by standardising the checkout flow and handling on-chain settlement via TON.

The initial rollout is limited to Mini Apps, with planned additions such as subscriptions and gasless transactions over time.

At the token generation event, 25% of the 1B supply will be distributed – including a 240M token airdrop to Backpack Points users and 1M tokens earmarked for Mad Lads NFT holders.

The remaining supply is split into two equal 37.5% tranches labelled pre- and post-IPO, with the pre-IPO allocation set to unlock progressively as the exchange hits “growth triggers” such as regulatory approvals, new region launches, and product rollouts.

Each transaction is signed directly on a Ledger device, combining decentralised exchange access with hardware-level security.

The integration supports major networks including Ethereum and leading L2s, with OKX DEX aggregating liquidity across hundreds of venues to deliver competitive pricing.

The testnet gives developers an EVM environment with test assets and tooling to prototype regulated, onchain trading and DeFi integrations, while Robinhood frames the chain as a bridge between traditional market access and Ethereum liquidity.

Jeff Weinstein, Stripe’s product lead, said on X on Tuesday that the rollout is expected to expand over time to additional protocols, currencies and blockchains.

The system is built on Stripe’s PaymentIntents API, enabling businesses to programmatically charge AI agents for API usage, Model Context Protocol calls and HTTP requests.

In parallel, CoinGecko activated x402 for parts of its API on Tuesday, allowing agents to pay $0.01 in USDC per request for data across multiple networks, turning market data access into a simple pay-per-use utility.

Access at launch will be limited to whitelisted institutional participants, with Securitize managing eligibility and onboarding market makers to support liquidity.

The deal follows Pump.fun’s earlier move into trading tools, including its October 2025 acquisition of Padre, which it later rebranded as "Terminal", with the team saying the addition of Vyper will improve EVM trading support, including on Base.

The development builds on Startale Group and SBI Holdings’ August 2025 partnership announcement to jointly launch an onchain trading platform focused on tokenized equities and real-world assets.

The company is working with the Rysk protocol to launch an onchain options vault on Hyperliquid, with plans to eventually open the structure to other institutional HYPE holders

Aztec is a privacy-focused Ethereum Layer 2 that uses zero-knowledge proofs (zkSNARKs) to verify transactions and smart-contract execution without revealing sensitive details. AZTEC is the network’s native token, intended to support core protocol functions and align incentives for participants, including governance as the network evolves.

A key part of Aztec’s design is its “ZK² Rollup” approach: each private transaction is proven with its own zkSNARK, then many of those proofs are aggregated into a single proof that gets posted to Ethereum. This compression reduces the amount of data that needs to go on-chain and helps lower costs, while maintaining strong privacy guarantees.

Bybit announced the listing of AZTEC on its Spot trading platform today.

Open interest and trading volume data are sourced “as is” from the Bybit exchange platform API exclusively, and as such do not represent a comprehensive picture of the sum of trading activity across all derivatives markets or exchanges. The data visualized in this report consists of hourly and daily snapshots, recorded over the previous 30 days. Daily (hourly) snapshots of trade volume record the total sum of the notional value of trades recorded in the 24H (1 hour) period, beginning with the snapshot timestamp.

If not explicitly labeled as derived from another exchange, the input instrument prices to all derivatives analytics metrics in this report are sourced from the appropriate endpoints of Bybit’s public exchange platform API. In the event that data is labeled or referred to as representing the market on another exchange source, that data is sourced from the appropriate endpoint of each respective exchange’s public API.

Macroeconomic charts and data are sourced “as is” from the Bloomberg Terminal. Exchange data is sourced “as is” from publicly available exchange APIs. Block Scholes makes no claims about the veracity of public third-party data.

After acquisition of underlying-denominated raw data for open interest and trading volume on the Bybit exchange platform from Bybit’s API endpoint, equivalent dollar-denominated figures are calculated using the concurrent value of Block Scholes’s Spot Index for the relevant underlying asset.

Block Scholes’s Spot Index represents the aggregate Spot mid-price for a given currency across the top five CEXs by volume (with USD-quoted markets). It considers the proportion of total volume in the instrument on the exchange, as well as the deviation of a data point from those on other exchanges.

Futures prices are used for Block Scholes’s futures-implied yields calculation services in order to derive the constant-tenor annualized yields displayed in the Futures section of this report.

Options prices are used for Block Scholes’s implied volatility calculation services in order to calibrate volatility surfaces, from which all derivatives volatility analytics displayed in the BTC Options and ETH Options sections of this report are calculated. Volatility smiles are constructed by calibrating to mid-market prices observed in Bybit options markets. As part of the calibration process, prices go through rigorous filtration and cleaning steps, which ensures that the resulting volatility surface is arbitrage-free and has exceptional fit to the market observables.

.jpg)

.jpg)