Thahbib Rahman

Research Analyst

In less than a week, President Trump and his administration went from issuing a 48-hour ultimatum to Iran to announcing a five-day pause on any energy infrastructure airstrikes to then reportedly sending a 15-point plan to Iran in a de-escalatory effort to end the war.

In less than a week, President Trump and his administration went from issuing a 48-hour ultimatum to Iran to announcing a five-day pause on any energy infrastructure airstrikes to then reportedly sending a 15-point plan to Iran in a de-escalatory effort to end the war.

Meanwhile, the crypto industry also jumped a major regulatory hurdle earlier this week after the SEC, along with the CFTC, issued a joint interpretation guideline clearly defining how federal securities laws apply to crypto assets and crypto transactions.

Despite the regulatory advance, spot and options markets have largely continued to trade at the whims of geopolitical headlines.

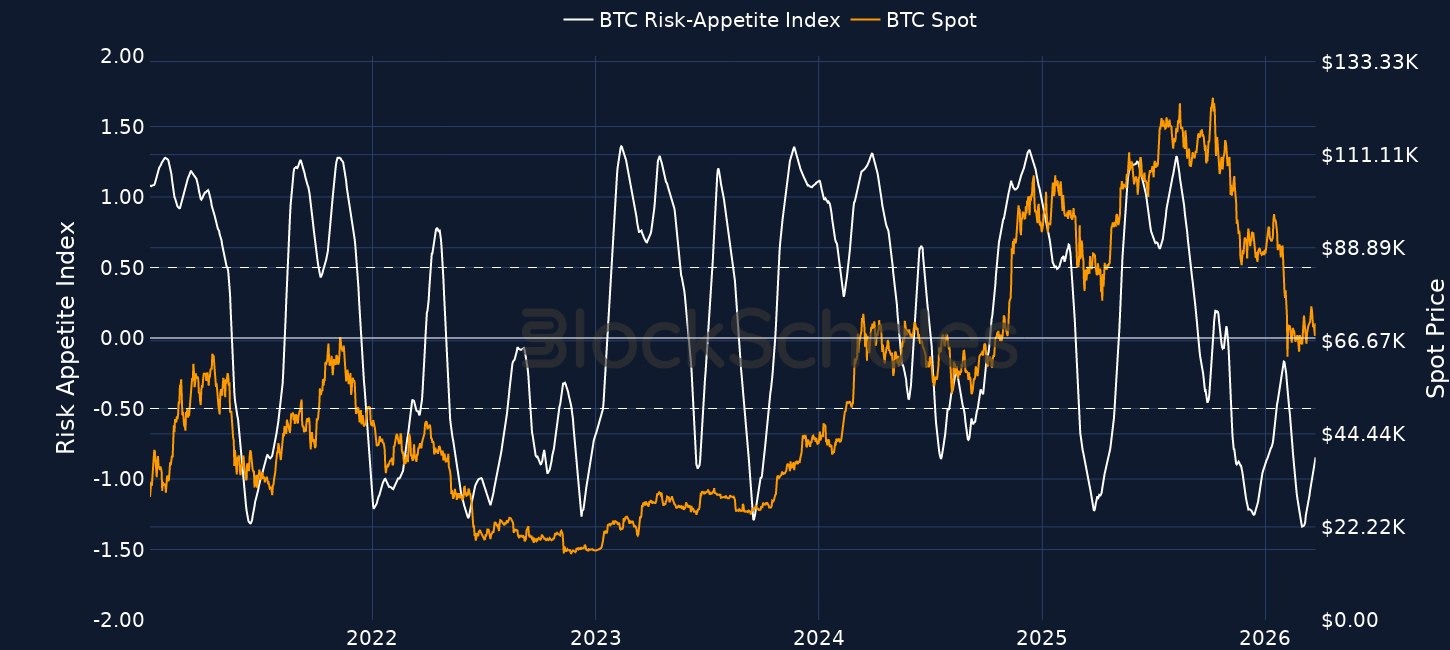

Spot price has recovered in a V-shaped manner amidst the headlines, while options markets are slowly pricing out some of their bearish positioning. If history is any guide, past escalations between the US and Iran have largely been faded by markets; with BTC’s median return 100 days after military conflicts against Iranian forces close to +26%.

Block Scholes’ Risk Appetite Index measures the level of euphoria (above 1) or panic (below -1) in the spot market. Momentum in this index shows a strong relationship to spot returns.

Despite the crypto industry receiving a major regulatory win as the SEC issued a comprehensive interpretation guideline for how to classify crypto assets, risk-on sentiment (and by extension crypto spot prices) have still largely traded on the ebbs and flows of the war in the Middle East.

Between March 20 - 23rd , President Trump’s public messaging pivoted between the US:

Monday’s de-escalatory pivot (in which Trump announced a five-day pause on any energy infrastructure strikes) was met with a sharp bout of volatility across financial markets. BTC immediately rallied more than 4% to trade above $70K, Brent crude oil prices plunged by nearly 15%, US treasury yields fell across the curve, and US equities ended the session higher.

Spot price has continued to hold up around $70K after it was reported that the US had sent a 15-point peace plan to Iran in a bid to bring the conflict to an end, which the latter swiftly rejected before issuing their own terms.

Iran War: Past precedence points to future gains?

As the war enters its fourth week, it’s perhaps timely to revisit historical precedence that may offer some longer-term optimism for crypto traders. The chart below compares BTC’s spot price 30 days before and 100 days after periods when the US undertook major hostile measures against Iran.

Key events, for example, include:

In all three cases, BTC spot price traded higher 100 days after the attacks began. Despite such episodes in recent years, of course, it must be stated that the current Middle East conflict is unprecedented in many ways.

What makes the current conflict unique is both its duration and the effective closure of the Strait of Hormuz – something never before implemented by Iran.

Nonetheless, across the three cases, BTC’s median return 100 days after the date that the escalations began was +26%. So far, since President Trump’s Feb 28, 2026 announcement that the US had struck Iran, BTC is up 8%% at the time of writing, below the +16% median this many days into past escalations.

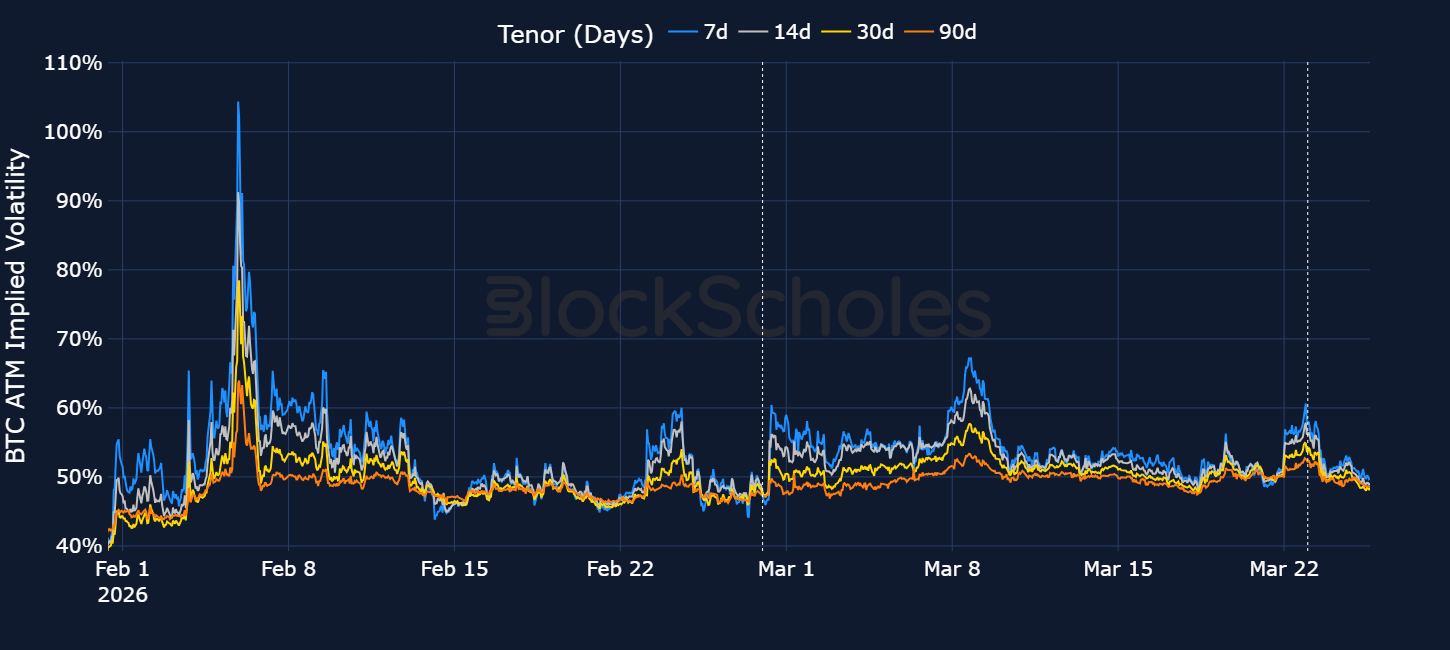

In BTC options markets, Trump’s apparent willingness to bring an end to the war has resulted in traders pricing out some of their expectations for volatility over the short-term. The 7-day at-the-money implied volatility level has fallen from 60% to 50% and trades far lower than the early-February highs of 104%.

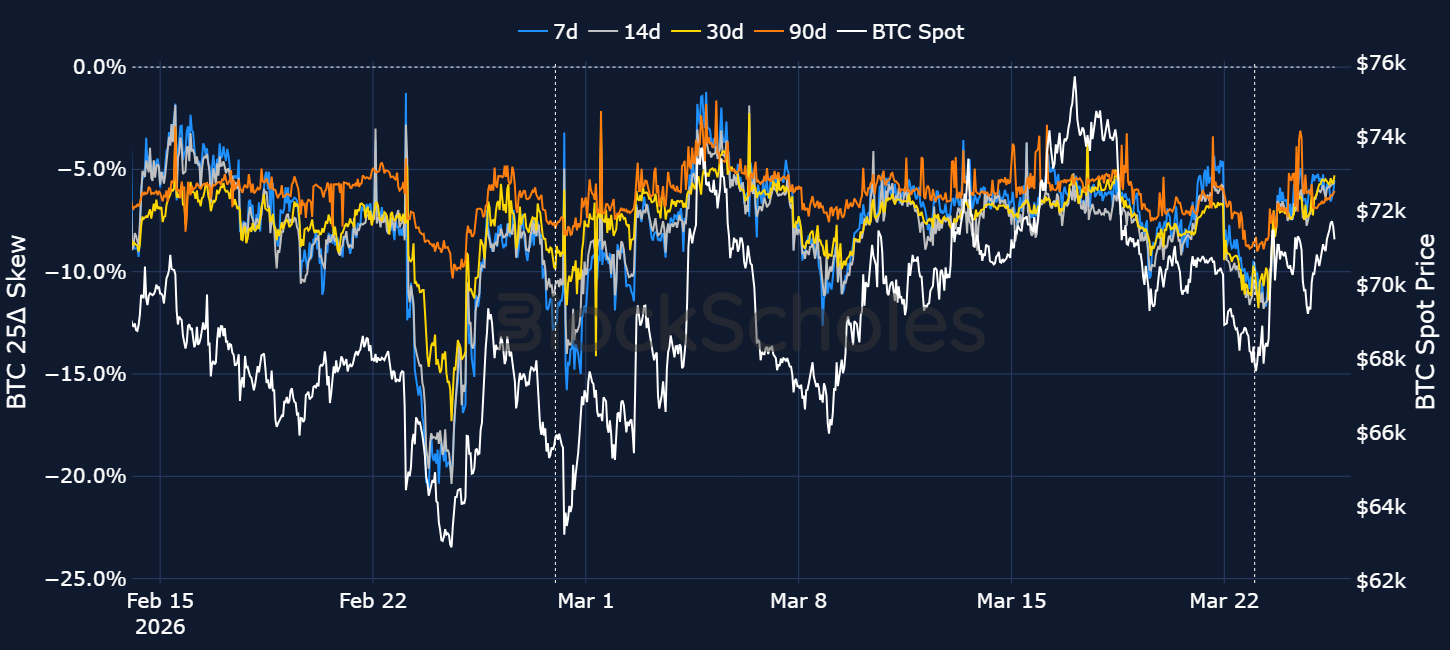

Additionally, as spot price hovers around $70K, much of the premium towards OTM put contracts across the volatility surface has eroded. 7-day put-call skew has risen from -11% to -4%. As we have come to expect for most of this year, however, the small upwards repricing in spot price has not been enough to shift traders bullish yet, as both BTC and ETH options markets continue to assign volatility premiums for downside protection.

The Commodity Futures Trading Commission (CFTC) and the Securities and Exchange Commission (SEC) have jointly issued an interpretation clarifying how federal securities laws apply to certain crypto assets.

While the Trump administration signalled a shift toward a more crypto-friendly regulatory stance, the landscape has remained clouded by uncertainty around how these rules are interpreted and enforced in practice.

Landmark cases such as XRP, where charges were initially brought and later partially dropped, have created sharp swings in token prices and reinforced perceptions of inconsistency.

This ambiguity has, in turn, contributed to continued hesitation among institutions who remain cautious about entering the space both as investors and as issuers of crypto-related products.

Regulators Align

This joint crypto interpretation release landed just a week after the SEC and CFTC formalised closer coordination through a Memorandum of Understanding, aimed at tightening oversight across both crypto and traditional financial markets.

As digital assets increasingly sit across securities and derivatives regimes, the agreement sets out a clearer framework for how the two regulators will work together. The aim is to align definitions, coordinate rulemaking, and reduce inconsistencies in how crypto is classified and supervised.

It also tackles one of the biggest friction points in crypto regulation: overlapping oversight.

Instead of both agencies supervising the same activity, the framework assigns responsibility based on the function and risk profile of each activity. At the same time, the SEC and CFTC will expand data-sharing and jointly monitor firms operating across both jurisdictions, with more coordinated surveillance and risk assessment to better capture cross-market exposures and systemic links within crypto markets.

The agreement still preserves each regulator’s statutory authority, but enables more practical coordination in supervision and enforcement.

Alongside this, “Project Crypto” has been introduced as a joint initiative to align federal oversight of digital assets and clarify how different asset types are treated. The CFTC’s guidance is also being developed in parallel with the SEC’s approach, reinforcing consistency across the regulators.

In particular, the SEC and CFTC have moved toward a more structured approach by classifying crypto assets into five categories based on their characteristics, uses, and functions:

The interpretation seeks to define which asset types fall under the SEC’s jurisdiction, meaning they will be classified as a security. Importantly, for these tokens not to be considered securities, they must not grant rights to profits or income.

“Digital commodities” are crypto assets that derive their value from the operation of a decentralised crypto system rather than from managerial efforts and are generally not securities, although classification depends on facts and circumstances. Digital commodities are integral to the functioning of a crypto system and may be required for participation in network activities such as validation and governance. Examples of digital commodities include Bitcoin (BTC), Ether (ETH), Solana (SOL), and Cardano (ADA). While not automatically under CFTC jurisdiction (despite their name) certain non-security crypto assets may meet the definition of a commodity under the Commodity Exchange Act.

“Digital collectibles” are crypto assets primarily valued for cultural, artistic, or social significance and are generally not securities, but may be securities in specific cases depending on how they are structured or marketed. Their value is driven by factors such as scarcity and popularity, with examples including artistic NFTs and meme coins such as Pepe (PEPE) and Dogwifhat (WIF).

“Digital tools” are crypto assets that perform practical functions such as membership access, credentials, or tickets and are generally not securities, provided they are used for utility rather than investment purposes. Digital tools are often non-transferable or “soul-bound” and derive value from their functional utility. Examples of digital tools include Ethereum Name Service (ENS) domain tokens and tokenised event tickets such as NFT-based conference passes.

"Stablecoins" such as USD Coin (USDC), issued by permitted issuers are excluded from the definition of a security by statute. Other stablecoins may or may not be securities depending on their specific characteristics and circumstances. Their nature of pegging an underlying crypto or non-crypto asset creates a close overlap to the definition of digital securities and may or may not be securities depending on their structure, issuer, and rights attached.

"Digital securities" such as tokenised shares and blockchain-based representations of traditional equities or bonds are securities and remain securities regardless of whether they are issued Crypto services provide an even murkier grey area, with each needing to be independently distinguished to determine whether they fall under the SEC’s jurisdiction. In practice, these categories are not treated as distinct legal classes; rather, they serve as analytical guidance as to whether a service constitutes an “investment contract” or not.

The SEC has also highlighted five services in particular:

"Protocol Mining" refers specifically to proof-of-work (PoW) networks, where participants validate transactions and secure the network by solving cryptographic puzzles e.g. Bitcoin (BTC) and Monero (XMR). In return, miners receive newly generated digital commodities as rewards under the rules of the network protocol. This activity is not considered a security because it is classified as administrative or ministerial in nature, with rewards functioning as compensation for computational services rather than profits derived from the managerial efforts of others. Proof-of-stake (PoS) systems are not included within Protocol Mining and are instead treated separately under "Protocol Staking".

"Protocol Staking" refers to participation in proof-of-stake networks, where users lock tokens to validate transactions and earn rewards. e.g. Ethereum (ETH) staking (post-merge) and Solana (SOL) staking. It is not considered a security as the activity is treated as administrative or ministerial, with rewards tied to protocol rules rather than discretionary managerial efforts.

"Staking Receipt Tokens" represent ownership of deposited digital assets and associated rewards. For example, liquid staking tokens such as Lido’s stETH represent a user’s staked ETH position plus accrued rewards. They are not securities when linked to non-security assets outside an investment contract, but they can be securities if they represent underlying assets that are themselves securities or part of an investment contract.

"Wrapping" involves depositing a crypto asset and receiving a redeemable token on a one-to-one basis e.g. Wrapped Bitcoin (WBTC). It is not considered a security when applied to non-security assets, as the process is administrative and does not involve discretionary management, although wrapped versions of securities remain securities.

"Airdrops" refer to the distribution of tokens for little or no consideration, often used to build user bases and decentralise networks. They are generally not investment contracts, although this may change if accompanied by promotional activity creating an expectation of profit from managerial efforts.

The company agreed to repurchase around $367.5M of its 2030 notes for $322.9M and $633.4M of its 2031 notes for $589.9M, effectively retiring debt at a discount.

The initiative will initially focus on crypto assets, blockchain, artificial intelligence, and prediction markets to support responsible innovation while maintaining U.S. competitiveness.

Led by Michael J. Passalacqua, the task force will also coordinate with agencies, including the U.S. Securities and Exchange Commission (SEC) and its Crypto Task Force, to align oversight alongside the Innovation Advisory Committee.

This builds on its previous programs announced in 2024 and 2025, where Robinhood have repurchased more than 25M shares at an average price of around $45, totalling over $1.1B.

According to Bloomberg, the New York-based firm is focusing the new capital on areas such as stablecoins, tokenisation and institutional onchain finance.

Outside the new fund, ParaFi has also raised a further $325M for its broader digital asset strategies since the start of 2025, bringing total assets under management to around $2B.

The proposed fund, which would trade on Nasdaq under the ticker GHYP if approved, would track HYPE using CoinDesk benchmark data and custody assets with Coinbase Custody.

With the SEC waiving the standard waiting period, the changes took effect immediately and also allowed these products to trade as FLEX options (Flexible Exchange Options).

Separately, Nasdaq ISE is still seeking approval to raise IBIT-specific position limits to 1M contracts.

Kalshi has introduced new screening tools to stop political candidates from trading on their own races and is extending similar protections to sports markets through integrity-monitoring lists designed to block athletes, coaches, referees and other insiders.

Polymarket, meanwhile, has strengthened its market oversight by updating its Terms of Use and the Polymarket US Rulebook, alongside launching dedicated Market Integrity pages that explain how enforcement works in practice.

The filing also adds new sales agents, keeps prior MSTR and STRC issuance programmes in place, and replaces the prior STRK programme with a new $2.1B STRK facility.

Designed for treasury and collateral management, the fund offers near-instant settlement, multi-currency subscriptions and redemptions, and 24/7 transferability, with Chainlink providing on-chain NAV reporting.

The first rollout is on the Canton Network, where Moody’s is also operating a node, embedding credit insight directly into blockchain-based financial workflows rather than leaving it as a separate off-chain input.

The development allows institutional clients to trade and hedge exposure outside traditional market hours using either fiat or stablecoins.

The company’s strategy focuses on holding and actively deploying XRP, and the combined entity is expected to launch with at least 473M XRP on its balance sheet.

If completed, the Nasdaq listing would position Evernorth as a dedicated vehicle for both price exposure and yield generation.

The Asunción-based deployment, part of its BUZZ AI Cloud platform, is already running large language model training workloads and will serve as a proof-of-concept for scaling AI infrastructure across the company’s hydro-powered footprint in the country.

CLUSDT is a crude oil-linked perpetual contract quoted against USDT, with its pricing anchored to CL, the index that tracks the front-month WTI crude oil futures contract (Bybit: USOUSD).

As the key benchmark for US oil price discovery, CL is the instrument through which the market most directly reprices changes in crude fundamentals. That importance extends well beyond the energy complex - movements in oil feed directly into fuel costs, inflation expectations, transport margins and broader cross-asset risk sentiment.

As a result, CL is closely watched across both traditional finance and crypto markets, especially in light of the ongoing Middle East conflict.

What is driving CL at present is a sharp repricing of a global oil shock. In its March 2026 Oil Market Report, the IEA said the war in the Middle East is creating the largest supply disruption in the history of the global oil market. It noted that crude and product flows through the Strait of Hormuz had fallen from around 20M barrels per day (mb/d) before the war to minimal levels, and that Gulf producers had cut total oil production by at least 10 mb/d as storage filled and alternative export capacity proved limited.

The crisis has intensified global energy pressures, with Chevron warning of a potential California fuel crisis, hundreds of fuel shortages reported in Australia, the Philippines declaring a national energy emergency, and Asian nations reportedly hoarding jet fuel.

Bybit has listed CLUSDT Perpetual Contract on 24 March 2026. Trading is now open with up to 50x leverage.

Open interest and trading volume data are sourced “as is” from the Bybit exchange platform API exclusively, and as such do not represent a comprehensive picture of the sum of trading activity across all derivatives markets or exchanges. The data visualized in this report consists of hourly and daily snapshots, recorded over the previous 30 days. Daily (hourly) snapshots of trade volume record the total sum of the notional value of trades recorded in the 24H (1 hour) period, beginning with the snapshot timestamp.

If not explicitly labeled as derived from another exchange, the input instrument prices to all derivatives analytics metrics in this report are sourced from the appropriate endpoints of Bybit’s public exchange platform API. In the event that data is labeled or referred to as representing the market on another exchange source, that data is sourced from the appropriate endpoint of each respective exchange’s public API.

Macroeconomic charts and data are sourced “as is” from the Bloomberg Terminal. Exchange data is sourced “as is” from publicly available exchange APIs. Block Scholes makes no claims about the veracity of public third-party data.

After acquisition of underlying-denominated raw data for open interest and trading volume on the Bybit exchange platform from Bybit’s API endpoint, equivalent dollar-denominated figures are calculated using the concurrent value of Block Scholes’s Spot Index for the relevant underlying asset.

Block Scholes’s Spot Index represents the aggregate Spot mid-price for a given currency across the top five CEXs by volume (with USD-quoted markets). It considers the proportion of total volume in the instrument on the exchange, as well as the deviation of a data point from those on other exchanges.

Futures prices are used for Block Scholes’s futures-implied yields calculation services in order to derive the constant-tenor annualized yields displayed in the Futures section of this report.

Options prices are used for Block Scholes’s implied volatility calculation services in order to calibrate volatility surfaces, from which all derivatives volatility analytics displayed in the BTC Options and ETH Options sections of this report are calculated. Volatility smiles are constructed by calibrating to mid-market prices observed in Bybit options markets. As part of the calibration process, prices go through rigorous filtration and cleaning steps, which ensures that the resulting volatility surface is arbitrage-free and has exceptional fit to the market observables.

.jpg)

.jpg)