Thahbib Rahman

Research Analyst

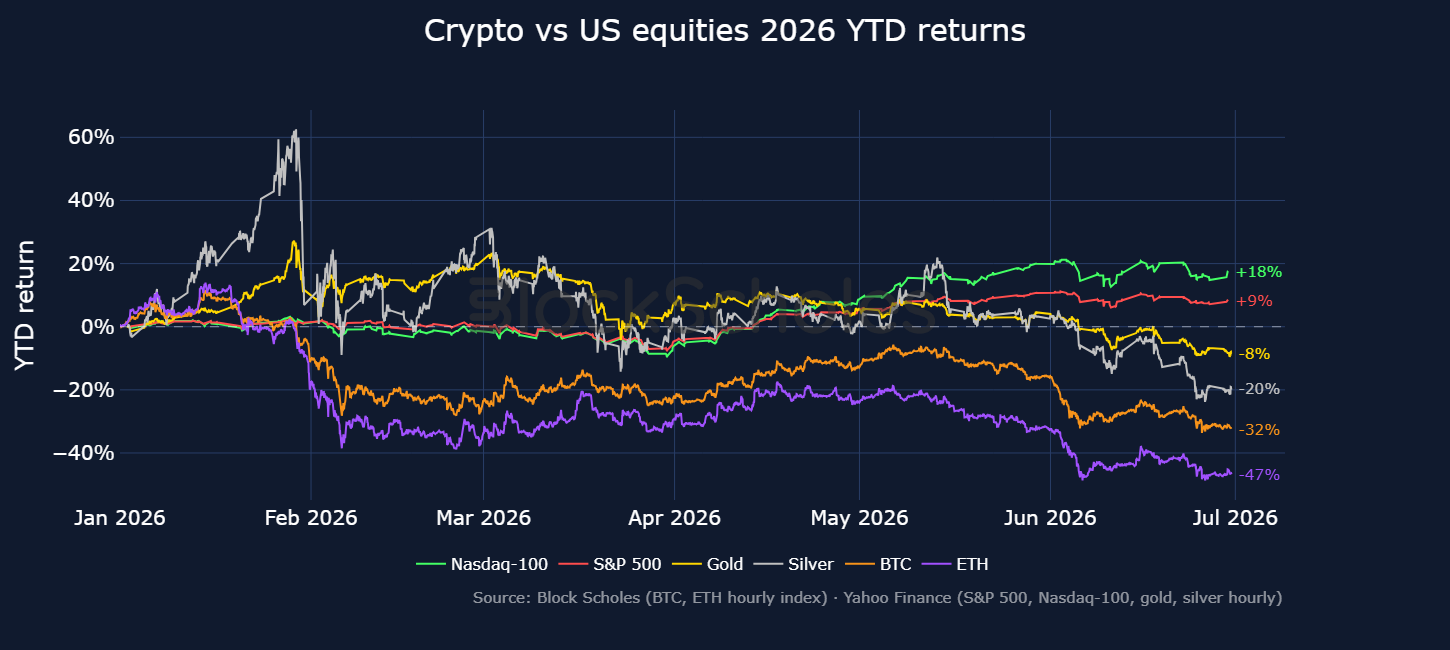

The first half of 2026 was characterized by cross-asset volatility from cryptocurrencies to US equities and precious metals. Of the three asset classes however, crypto prices have fared the worst, with BTC down 50% from its October 2025 all-time high and ETH down more than 66% from its respective August 2025 high. Each successive leg lower in crypto-asset prices through the year was driven by a different factor — some were idiosyncratic to digital assets, and others a consequence of a deteriorating macro backdrop.

The first half of 2026 was characterized by cross-asset volatility from cryptocurrencies to US equities and precious metals. Of the three asset classes however, crypto prices have fared the worst, with BTC down 50% from its October 2025 all-time high and ETH down more than 66% from its respective August 2025 high.

Each successive leg lower in crypto-asset prices through the year was driven by a different factor — some were idiosyncratic to digital assets, and others a consequence of a deteriorating macro backdrop.

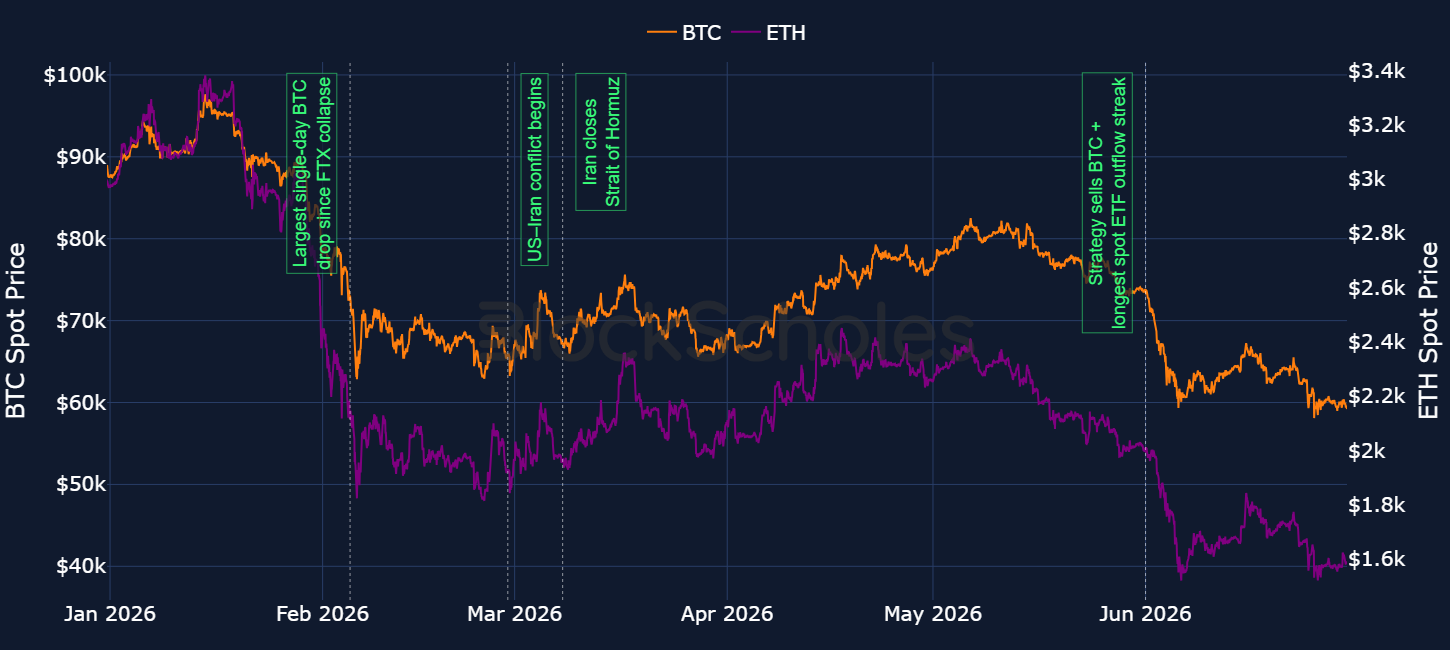

On Feb 5, 2026, a selloff in crypto that had begun earlier that month intensified, with BTC falling 18% intraday to $60,000. That marked the largest single-day drop in spot price since the collapse of the now-defunct FTX exchange in November 2022. The wider altcoin market plunged just as hard: ETH fell below $1,800 while SOL fell through support at $80.

That cascade of selling was not crypto-specific: on Wall Street, fears of mega-cap tech stocks being overvalued and a potential bubble around artificial intelligence saw a de-risking out of US equities also. Since that initial scare at the start of the year, sentiment has shifted — US equities have marched past the 7,000 mark, driven in part by investor confidence in the durability of the AI rally.

By the end of February, President Trump announced that the US had launched preliminary airstrikes against Iran. That ushered in the phase of geopolitical volatility that has since clouded financial markets to the present day. Despite risk-on assets being able to shrug off the tensions over time, the closure of the Strait of Hormuz — the key waterway for 1/5th of the world’s oil supply — has continued to weigh on sentiment due to its implications on US inflation and Fed monetary policy.

BTC then slowly staged a recovery back above $80K before being dragged down by another bout of de-risking in June. That coincided with the longest spot Bitcoin ETF outflow streak since their January 2024 launch and a symbolic 32 BTC sale from the largest Bitcoin digital asset treasury firm, Strategy. BTC has since traded rangebound around $60K.

Crypto’s underperformance relative to a basket of macro assets is best seen below. Despite the macro headwinds from the US-Iran conflict, risk-on equities have powered through the year. Additionally, while precious metals have struggled to catch a bid since their blow-off top earlier in the year, BTC and ETH stand out as the clearest underperformers.

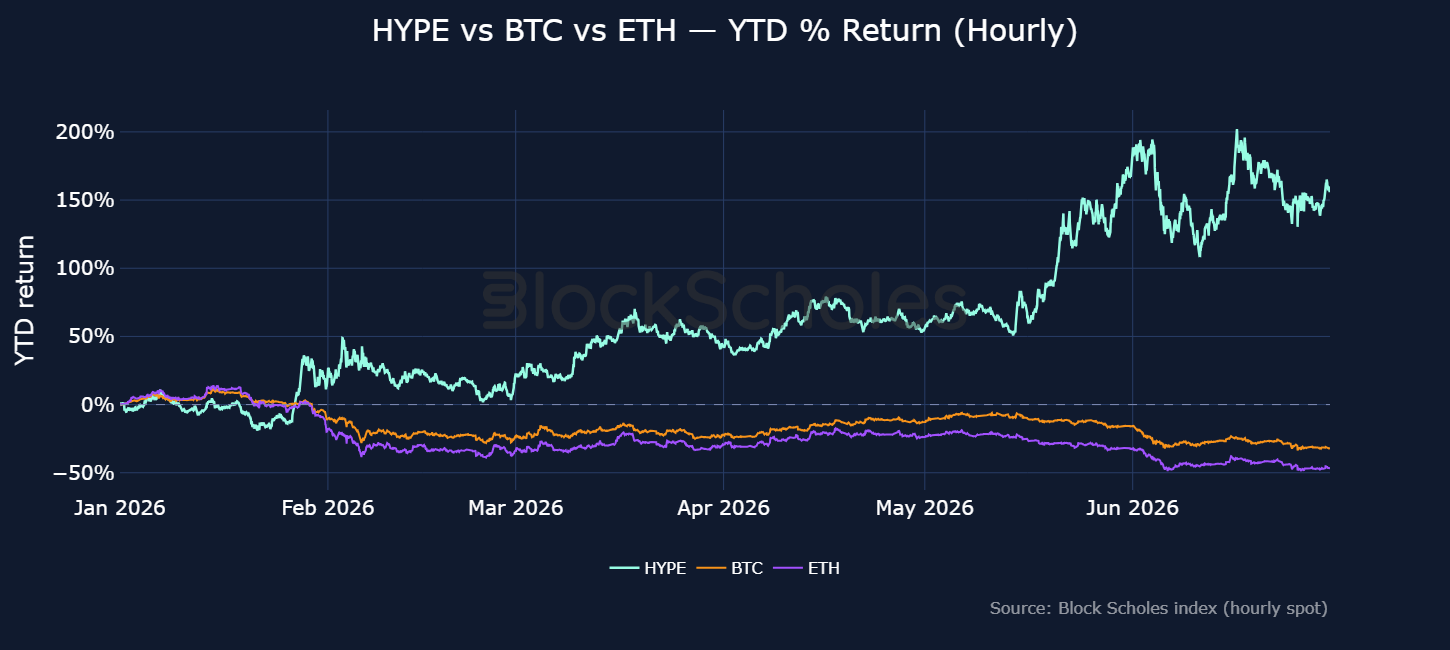

While the rout in digital assets has, for the most part, been broad-based, specific segments of the market have outperformed.

In our outlook report for 2026, we argued:

“We will see a further flight to fundamental value: altcoins with their own regulatory wrapper and those with innovative ecosystems that stand to gain the most from continued regulatory friendliness are likely to see inflows, creating a further bifurcated market.”

One asset in particular which fits that description is Hyperliquid’s native HYPE token — which is up 150% year-to-date. HYPE has been supported by a number of factors:

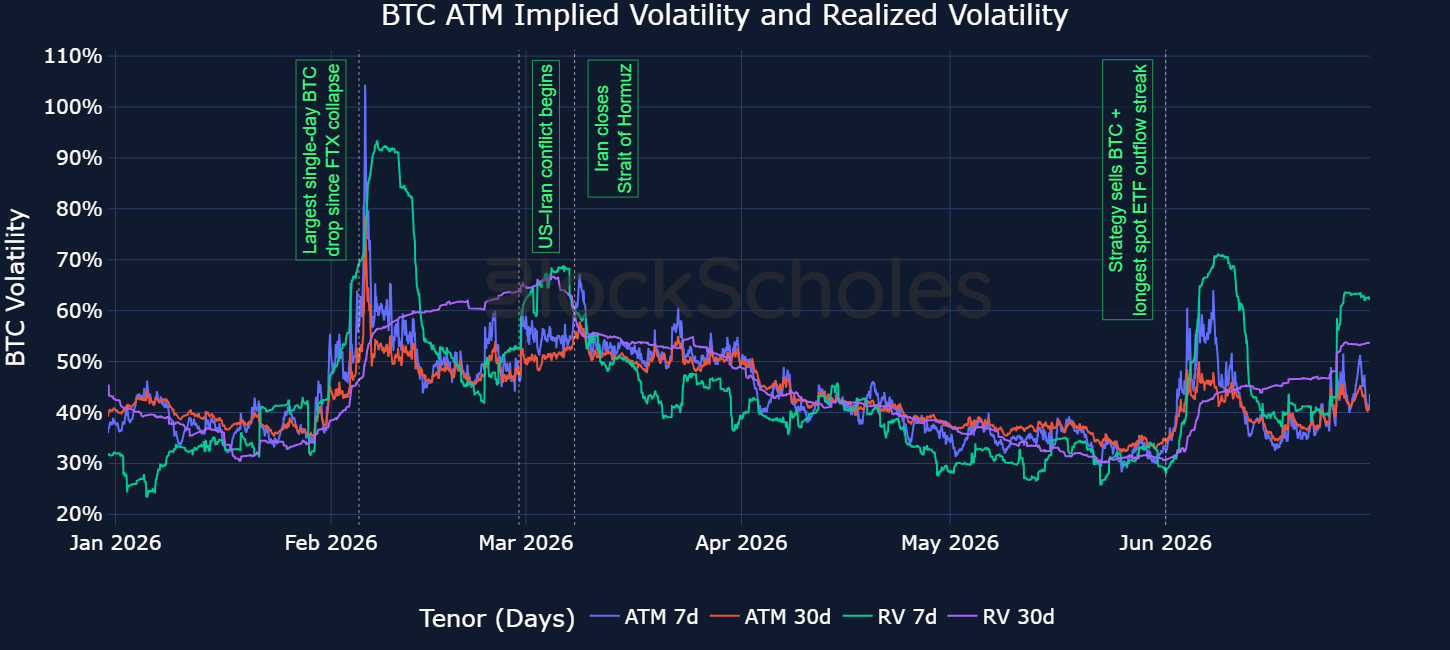

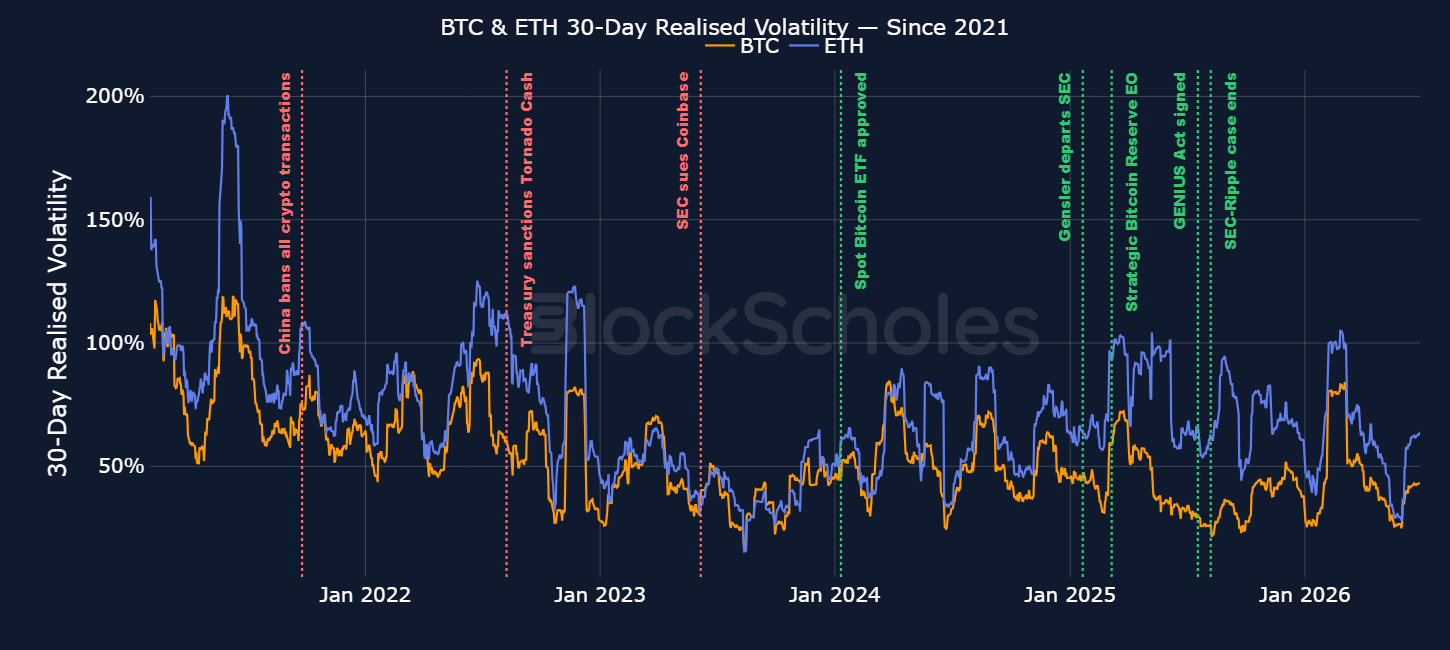

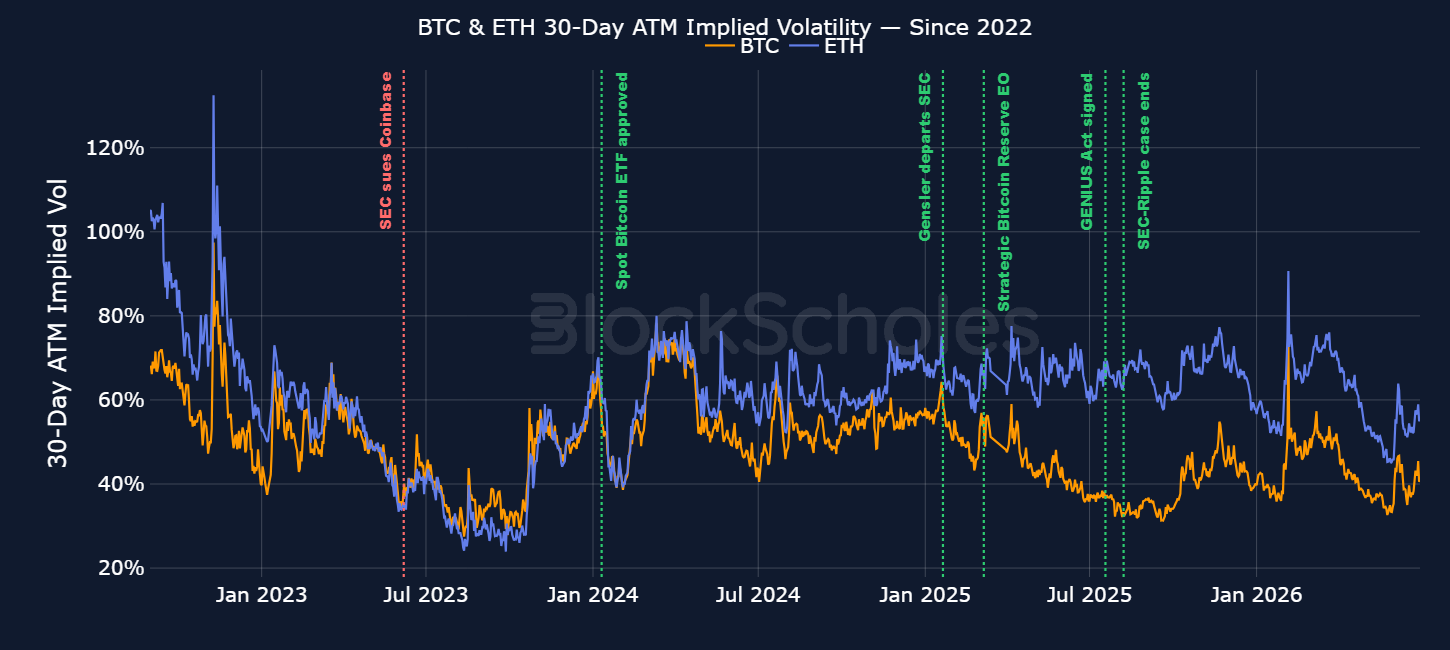

The aggressive spot price selloffs have had a notable impact on options markets. BTC’s at-the-money implied volatility, a forward-looking measure of the expected volatility of an asset over a specific period of time, jumped towards 103% in early February — matching levels seen during November 2022.

That jump in forward-looking volatility expectations was at least partly driven by realized volatility — the volatility delivered by spot prices jumping to levels last seen in March 2025 during the US tariff saga.

Subsequent events in the year, such as the US-Iran conflict and Strategy’s Bitcoin sale did not see volatility spike as high, though nonetheless punctuated periods of sideways volatility, when markets expected quieter times ahead (such as the May year-to-date low in ATM IV).

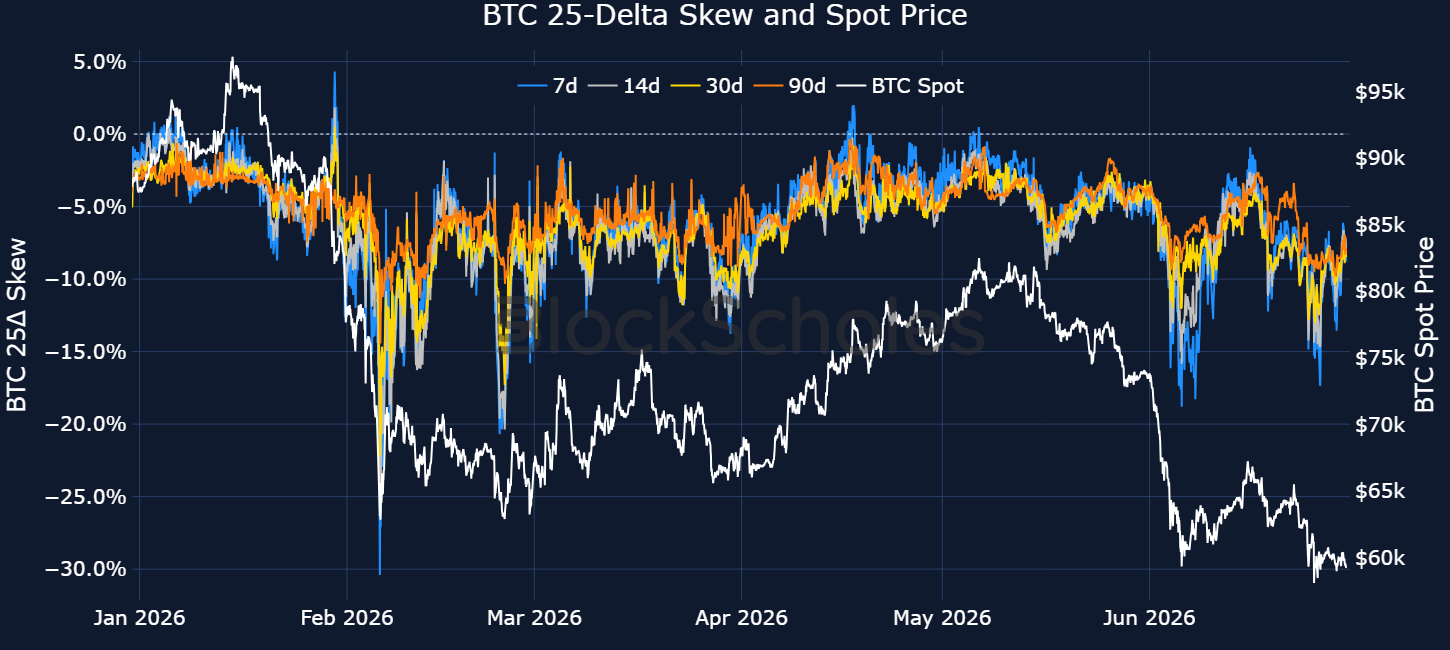

For most of the year, in options markets, downside protection has been priced at a significant implied volatility premium to OTM calls — brief periods of spot recovery have been unable to drive a meaningful skew back towards call options.

A distinct hawkish tilt in the Fed’s June meeting under the helm of new Chair Kevin Warsh may be one driving force for markets to maintain that put-premium.

According to the summary of economic projections in that meeting, nine policymakers see the chance of at least one interest rate hike before year-end. That marks a significant turnaround from the March FOMC meeting where the median forecast was for one rate cut in 2026 with no policymakers pencilling in expectations of a rate hike.

Chair Warsh also used the press conference to emphasise a few other key points:

Based on these factors, we expect Fed monetary policy to have a significant impact on price action for the second half of the year.

The lack of forward guidance could see more volatility on FOMC meet days while any follow-through on the implied hawkish tilt and reiterated dedication to the inflation mandate could potentially act as a headwind for risk-on assets, including crypto.

Additionally, Warsh has in the past critiqued the size of the Fed’s balance sheet and its implications on blurring the lines between fiscal and monetary policy. This is a view held by other key members of the Trump-appointed administration, such as Stephen Miran who was briefly a voting member of the FOMC.

Ahead of the US mid-term elections in November 2026, those views may become an important macro driver. Seasonal patterns suggest fiscal support has tended to increase around mid-term election cycles and has historically been supportive of risk-on assets. It remains to be seen however if a potential reduction in the Fed’s balance sheet as Warsh is advocating for will shift more focus to the fiscal policy of the US Treasury.

As in H1 2026, we expect developments in the US regulatory environment to continue to be an important driver for the second half of the year.

Regulatory developments have long played an important role in shaping sentiment across crypto markets, often becoming the dominant narrative as they unfold. In particular the widely anticipated US- based CLARITY Act will be watched closely for progression before 2027.

The Digital Asset Market Clarity Act of 2025 (H.R. 3633) (the CLARITY Act) marks the most comprehensive US crypto market-structure bill ever to clear a chamber of Congress. It passed the House by 294 votes to 134 on 17 July 2025, and has spent the last four months under consideration by the Senate.

The CLARITY Act does two things. First, it establishes a clear division between the CFTC and SEC, the two main US financial regulators, to determine which regulator is responsible for each type of cryptoasset. Second, it creates a federal rulebook for the exchanges and broker-dealers that trade it:

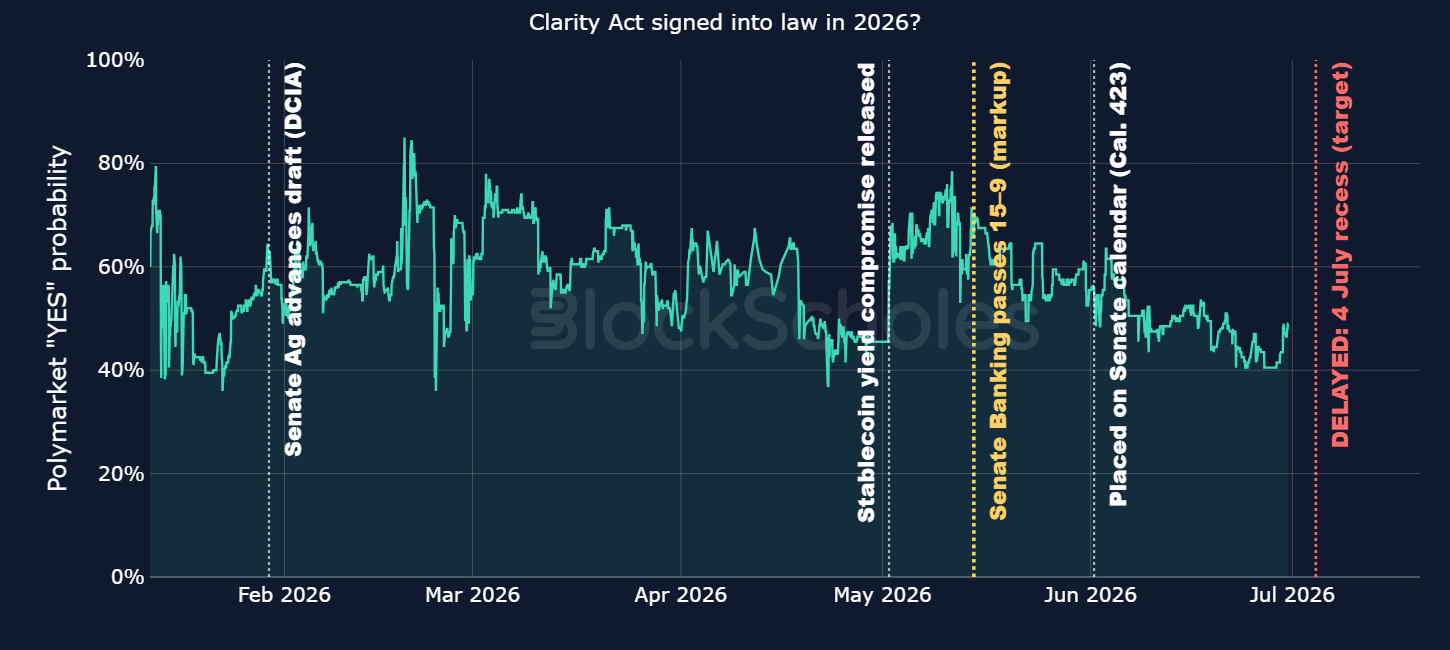

The White House and several senators had floated an optimistic 4 July 2026 as a target for signing the CLARITY Act into law, but this is clearly unattainable given the time and procedural steps left.

"We're targeting July 4th. I think that would be a tremendous birthday present for America, celebrating our 250th." — Patrick Witt, Executive Director, President's Council of Advisors for Digital Assets, Consensus Miami

Based on the timelines for previous bills becoming law, a September 2026 or later target now appears more realistic. However, the biggest risk in the realistic schedule is the August recess. If the bill is not on the President's desk by mid-September, midterm campaigning may take precedence and make a politically charged crypto vote harder to achieve the necessary support.

This is reflected in Polymarket odds pricing in the likelihood of "Clarity Act signed into law in 2026?", now at under 50%. This probability has been slowly dropping since recent highs in May 2026 and the markets digest the probability of the law progressing is less likely as the year progresses and other political campaigns take precedence.

Assuming the bill moves through each stage, unimpeded:

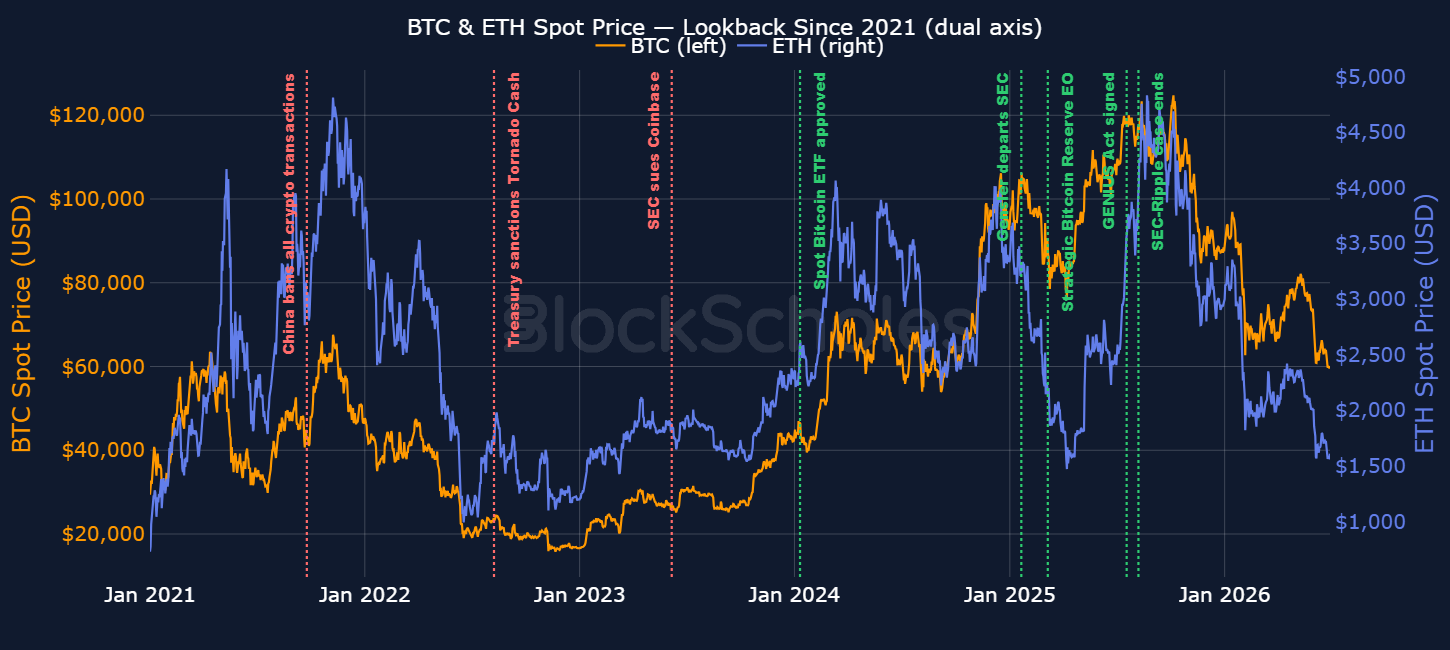

In the spot market, major policy milestones can have a visible impact on price action, particularly when they are perceived as supportive for the sector. Examples include the approval of spot ETFs and the run-up to Gary Gensler’s departure from the SEC, both of which formed part of a broader market expectation that the U.S. regulatory environment would become more lenient toward crypto, as seen in the chart below.

However, once these developments are confirmed, the data does not always move in the direction that might be expected. The chart below tracks a range of policy events, with restrictive developments, such as China’s ban on crypto transactions, shown in red, and more constructive developments, such as the GENIUS Act being signed, shown in green. Across these examples, the largest 30-day gain followed a restrictive event, with BTC rising 42.2% after China’s ban. By contrast, the three largest 30-day declines followed pro-crypto developments: the Strategic Bitcoin Reserve executive order at -7.2%, the end of the SEC-Ripple case at -6.2%, and Gensler’s departure at -5.3%.

For upcoming regulatory events, this raises the question of whether major regulatory milestones (such as the CLARITY ACT) will materially affect markets. In particular, the key question may not be whether the headline is pro-crypto or restrictive, but whether the outcome is already embedded in market expectations. If supportive policy progress is largely anticipated, confirmation alone may not be enough to generate a positive spot reaction.

With the polymarket-implied probability of the CLARITY ACT passing this year at under 50%, a faster progression could in fact provide an immediate supportive effect to crypto prices.

ETH shows a clearer relationship between positive policy developments and stronger price performance. Following the GENIUS Act, ETH outperformed BTC by 26.5 percentage points, with ETH rising 26.0% while BTC fell 0.5%. This may have reflected the market’s expectation that stablecoin legislation would benefit blockchains such as Ethereum, which host a large share of stablecoin activity across both the base layer and Layer 2 networks.

ETH also outperformed BTC by 15.4 percentage points after the SEC-Ripple dismissal, rising 9.2% compared with BTC’s 6.2% decline. This move can be linked to the broader implications for altcoins, which had faced pressure under the SEC’s approach to treating certain token sales as securities.

We expect this trend to continue in the second half of 2026, but with divergent reactions across the altcoin market. The strongest reactions are likely to come from networks where the regulatory development has a clear link to future demand, usage, or revenue. Chains that are able to attract stablecoin issuance, tokenisation activity, or institutional on-chain flows should therefore be better placed to benefit from further regulatory clarity.

Policy developments that provide clearer rules for stablecoins, token issuance, and on-chain financial activity are likely to have a larger impact on assets that are directly exposed to those use cases. ETH and other chains that can capture these flows are likely to remain more sensitive to supportive regulatory developments than BTC.

While spot price action gives a mixed picture, realised volatility shows a clearer post-event response. BTC 30-day realised volatility rose after five of the eight regulatory developments analysed, with the largest increases following the Strategic Bitcoin Reserve executive order, where volatility rose from 41% to 66%, and China’s crypto transaction ban, where it rose from 65% to 77%.

This is an important distinction for future regulatory events: the market reaction in realised volatility may depend less on whether a development is supportive or restrictive, and more on whether it is expected or surprising. If the outcome is widely anticipated and therefore already already priced into the markets, confirmation may reduce event premium rather than create a new directional move.

We expect this pattern to continue into the second half of 2026. Spot reactions in BTC are likely to remain muted unless the regulation is directly relevant, with much of the impact continuing to be priced in ahead of time, as seen in previous regulatory events. The strongest price reactions are more likely to come from tokens or blockchains that directly benefit from, or are negatively affected by, specific regulatory outcomes. The volatility reaction may be more visible than the spot move, although it will need to compete with a likely seasonal lull in volatility over the summer, as well as the impact of continued institutional volatility selling.

In contrast, BTC 30-day ATM implied volatility fell after five of the six events since September 2022. Unlike realised volatility, which reflects actual price movement after the event, implied volatility reflects the market’s pricing of expected future volatility through options. A decline after major regulatory developments therefore suggests that, once the event has passed or the outcome is known, traders have less need to pay for optionality to hedge against, or position for, that specific risk.

This reaction in implied volatility confirms that markets are more sensitive to surprise than to confirmation.

When we look towards the next set of regulatory catalysts, such as the CLARITY ACT which follows a defined route through the US legislative process, there are multiple milestones which must be met for the act to progress. This provides multiple and staggered opportunities for the market to reprice assets and react to the potential possibility of the act passing, with less emphasis placed on the final passing of the act.

As mentioned above, a key risk for the CLARITY Act is timing – if the bill is delayed further, midterm campaigning could take priority and make passage harder under a potentially different balance of Democrat and Republican senators. However, it would also add a new layer of uncertainty, as the midterms will decide all 435 House seats and around one-third of the Senate. This could change the lawmakers and committee chairs responsible for advancing crypto legislation through each stage.

A more crypto-friendly Congress could move market-structure and stablecoin legislation faster, while a skeptical Congress could slow the process, alter the bills, or add stricter consumer-protection and enforcement rules. The generic ballot points to a less Republican-leaning environment. The impact would not be limited to the CLARITY Act, but would also apply to future crypto legislation and the rulemaking process.

The midterms will be a key driver of the second half of 2026. Markets will price in the effect of likely election outcomes and possible changes in control of Congress. A supportive result could improve crypto sentiment, while a more skeptical outcome could raise enforcement concerns. However, as with other regulatory events, the largest market reaction is likely to come from an unexpected result or shift in the election race.

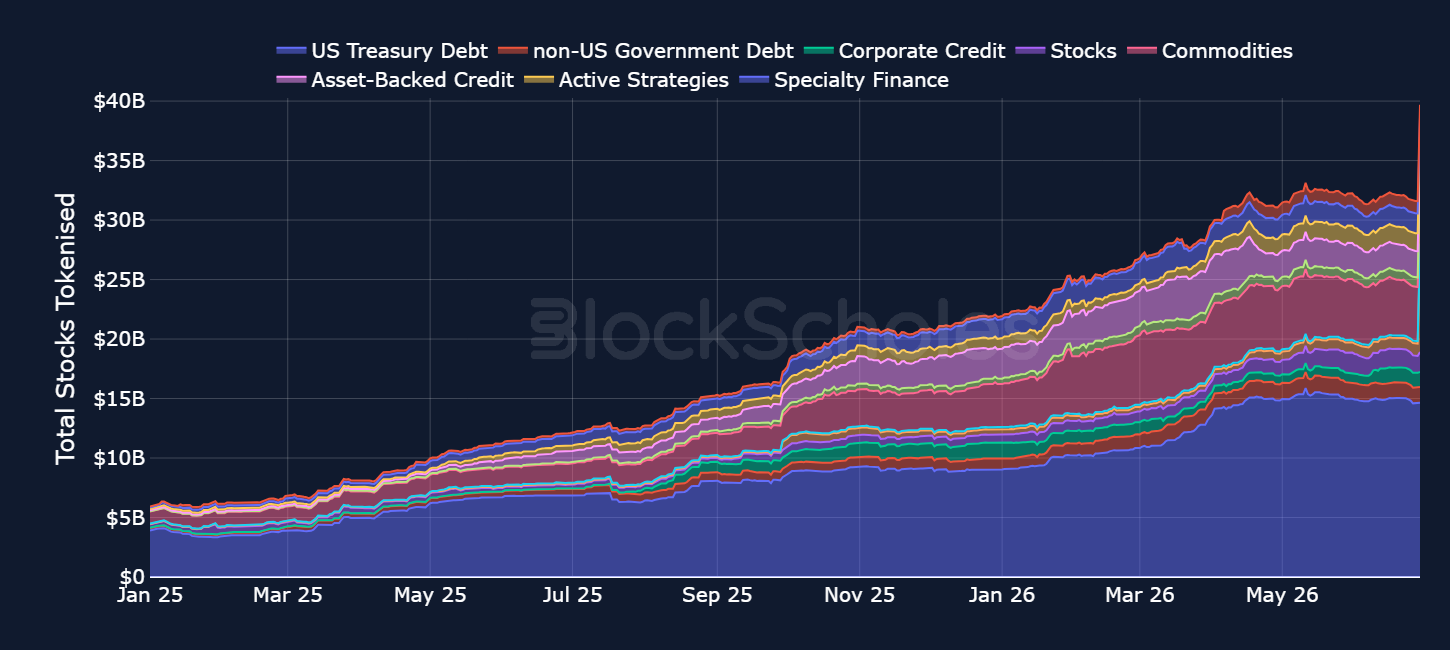

The first half of 2026 has also been defined by the mostly linear growth of real-world assets (RWAs) which we expect to continue throughout the second half of the year. Off-chain financial instruments such as Treasuries, funds, equities and private credit are increasingly represented on-chain.

RWA growth has accelerated sharply from January 2025 through to around April 2026, before beginning to flatten. However, this is not a reflection of a slowdown in the trend. Instead, we expect growth to continue, spurred by the steady flow of headlines around traditional financial institutions exploring on-chain and tokenised solutions. In 2026, this included a bank-led initiative to tokenise bank-issued USD deposit tokens, supported by firms including Bank of America, BNY, Citi, HSBC and J.P. Morgan. Separately, ICE announced plans to tokenise all NYSE U.S.-listed equities and ETFs.

With this, continued growth, and potentially even acceleration, in tokenisation appears inevitable as major TradFi institutions lead the way in bringing assets on chain and set a standard for other off-chain firms to follow.

For the crypto ecosystem, this means that RWAs are likely to compete more directly with altcoins for capital and attention. As tokenised Treasuries, funds, equities and credit products become easier to access on-chain, investors may have less need to seek exposure through higher-volatility tokens alone. This supports our broader view that the next phase of crypto market growth may be driven less by speculative altcoin rotation, and more by assets that connect on-chain infrastructure with real-world financial use cases.

It also creates more places for stablecoin balances to flow. Large on-chain stablecoin balances currently sit in cash-like form, but tokenised Treasuries and money market-style products offer a way for that capital to move into yield-bearing instruments. This is especially relevant given that Treasuries already make up a large share of RWA balances, despite stablecoin holders generally not receiving interest directly. Over time, this could make on-chain markets look more like a full financial system, where stablecoins act as the settlement layer and RWAs provide the investable assets around it.

The app is expected to use a points-based system rather than real-money wagering at launch, though Meta has not ruled out eventually adding real-money betting.

While the legislation is primarily focused on improving housing affordability and expanding supply, it also includes a provision preventing the Federal Reserve from issuing a CBDC or substantially similar digital asset until the end of 2030.

The CFTC said Kentucky's efforts to shut down federally regulated designated contract markets interfere with the federal framework for national swaps markets, arguing that the agency has exclusive jurisdiction over prediction markets.

The company reported $10.7B in crypto, cash, marketable securities and "moonshot" holdings, including $601M in cash and marketable securities, a $104M stake in Eightco Holdings, and its core ETH treasury.

The order sets a clear federal migration timeline for post-quantum cryptography, requiring high-value government assets to transition by the end of 2030 and high-impact systems by the end of 2031.

The contracts would allow customers to take yes-or-no positions on where the S&P 500 closes, paying a fixed cash settlement if the outcome is correct and nothing if it is not.

The fund, which serves roughly 1,200 small and medium-sized companies, is expected to invest through a passive fund holding multiple cryptocurrencies managed by a major hedge fund.

The partnership will begin with a proof-of-concept for stablecoin-powered overseas remittances on Solana, before expanding into tests with international partners and further checks around AML and KYC processes.

The team urged users to withdraw funds from all bridges deployed on Taiko and asked centralised exchanges to suspend deposits of its native token while the incident is investigated.

New minting and positions are now closed, while existing users have three months to return aUSDT and reclaim their XAUT collateral.

The product is designed to behave like high-yield digital credit, using variable dividends to anchor the price near $100.

The multi-chain DEX, backed by Polychain, Coinbase Ventures and Jump Crypto, cited prolonged unfavourable market conditions and insufficient revenue to keep operations running.

Users have until 16 July to withdraw funds before the platform shuts down.

Corning Incorporated is a publicly listed US materials-science and manufacturing company, traded on the New York Stock Exchange under ticker GLW. The company is best known for its long-standing expertise in specialty glass, ceramics, optical fibre and advanced materials, with technologies used across consumer electronics, telecommunications, data centres, life sciences, automotive and industrial applications.

Corning is a long-established industrial technology company with a history of innovation in glass and materials engineering. Its products are often "behind the scenes" but strategically important: the glass on smartphones and displays, the optical fibre used in broadband and data-centre networks, laboratory products used in life sciences, and ceramics used in emissions-control systems.

The company operates across several major end markets. In Optical Communications, Corning produces optical fibre, cables and connectivity solutions used in telecom networks and high-speed data infrastructure. In Display Technologies, it supplies precision glass used in televisions, monitors and other screens. In Specialty Materials, Corning is known for products such as advanced cover glass used in mobile devices and other durable glass applications. It also has businesses in Life Sciences and Environmental Technologies, giving the company a diversified industrial footprint rather than reliance on a single product category.

What makes Corning particularly interesting today is its exposure to the infrastructure side of the AI and data-centre buildout. As artificial-intelligence workloads expand, data centres require faster, denser and more efficient connectivity. Optical fibre and photonics are increasingly important because they can help move large volumes of data with lower latency and less heat than traditional copper-based systems. Corning's optical communications capabilities therefore position it as a potential beneficiary of rising investment in AI infrastructure, cloud computing and high-speed networking.

Corning has also been actively communicating a more ambitious growth plan to investors. Its "Springboard" strategy is designed to increase sales, improve margins and capture demand from secular growth markets. Management has also discussed longer-term annualised sales targets, including a path toward significantly higher revenue by the end of the decade, supported by growth in optical communications, AI-related infrastructure, display, specialty materials and other markets.

Bybit listed the GLWUSDT Perpetual Contract. Trading is now open with up to 20x leverage.

.jpg)

.jpg)