Thahbib Rahman

Research Analyst

This report evaluates Bitget Wallet's DEX aggregator and Enterprise API against three other leading aggregators (KyberSwap, 0x, and Jupiter) using thousands of live quote comparisons pulled simultaneously across trade sizes from under $1,000 to $100,000, on BTC, ETH, SOL, and stablecoin pairs. We assess execution quality across three dimensions: price competitiveness (which aggregator returns the best swap price), slippage control (how much that price degrades with trade size), and fill reliability (how often an executable quote is returned).

.jpg)

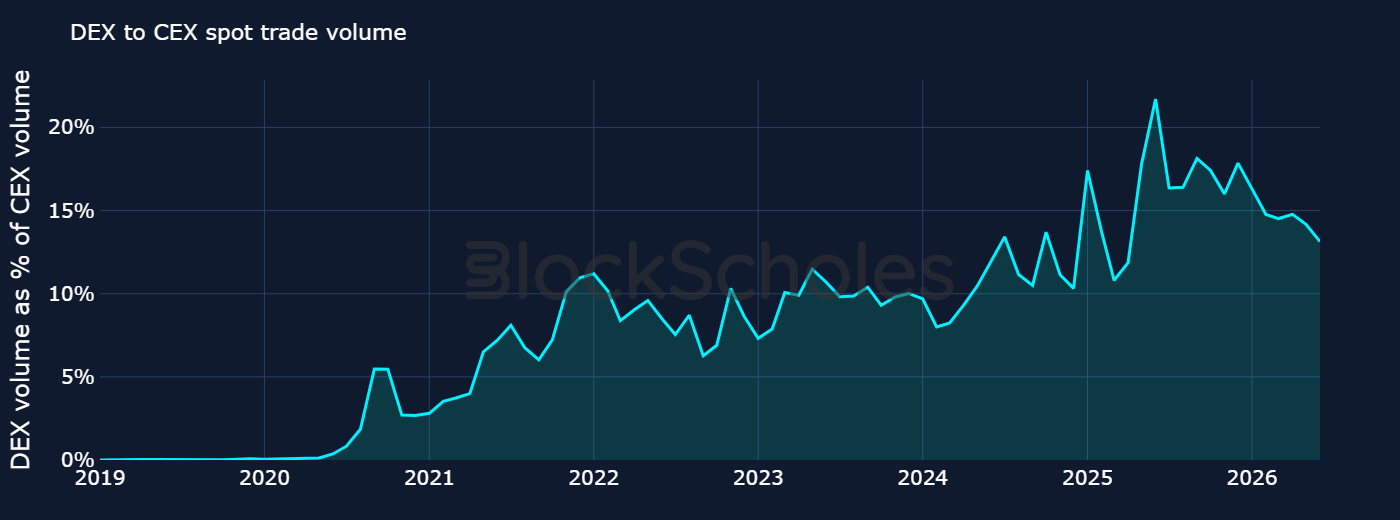

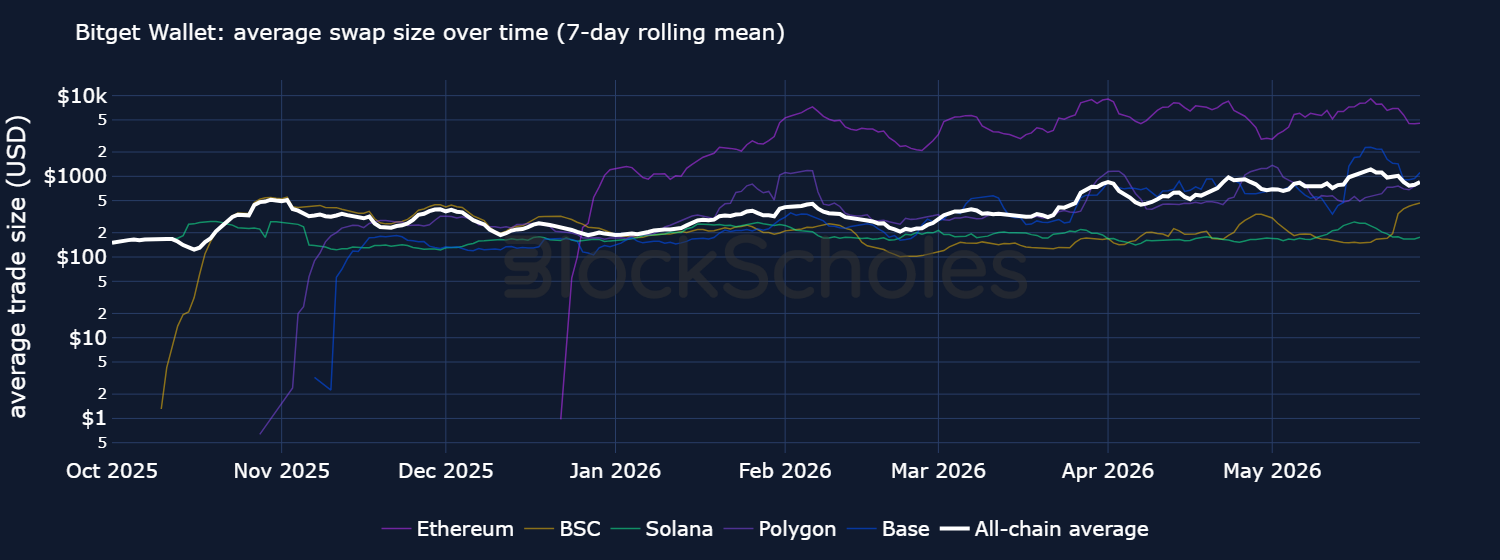

Decentralised exchanges have steadily taken spot volume share from centralised venues — the ratio of volumes on DEXs vs CEXs has risen from only 0.09% in 2020 to a peak of 22% in June 2025. That liquidity has, however, fragmented across various blockchains and hundreds of trading venues. At the same time, trade sizes are growing: average swap sizes on Bitget Wallet rose roughly five-fold in the first five months of 2026, peaking above $1,200, against the backdrop of a stablecoin market that has grown from under $1B in 2018 to over $300B today.

In this environment, aggregating liquidity is no longer the differentiator — it has become a baseline capability. The question that now determines execution cost is how well a routing engine navigates that fragmented liquidity, particularly as trades grow in size.

This report evaluates Bitget Wallet's DEX aggregator and Enterprise API against three other leading aggregators (KyberSwap, 0x, and Jupiter) using thousands of live quote comparisons pulled simultaneously across trade sizes from under $1,000 to $100,000, on BTC, ETH, SOL, and stablecoin pairs. We assess execution quality across three dimensions: price competitiveness (which aggregator returns the best swap price), slippage control (how much that price degrades with trade size), and fill reliability (how often an executable quote is returned).

Our key findings are:

The implication is that, as on-chain trade sizes continue to grow and decentralised applications continue to get built on-chain, the choice of routing engine provides a measurable and recurring cost advantage. Among the four platforms benchmarked, Bitget Wallet showcases meaningful performance differences, particularly for larger trade sizes on major token pairs.

Bitget Wallet, a part of the broader Bitget ecosystem, is a non-custodial crypto wallet that provides users with a suite of crypto services, including: seamless token swaps, trading, a decentralised app (dApp) browser, payment and portfolio management tools built for digital assets.

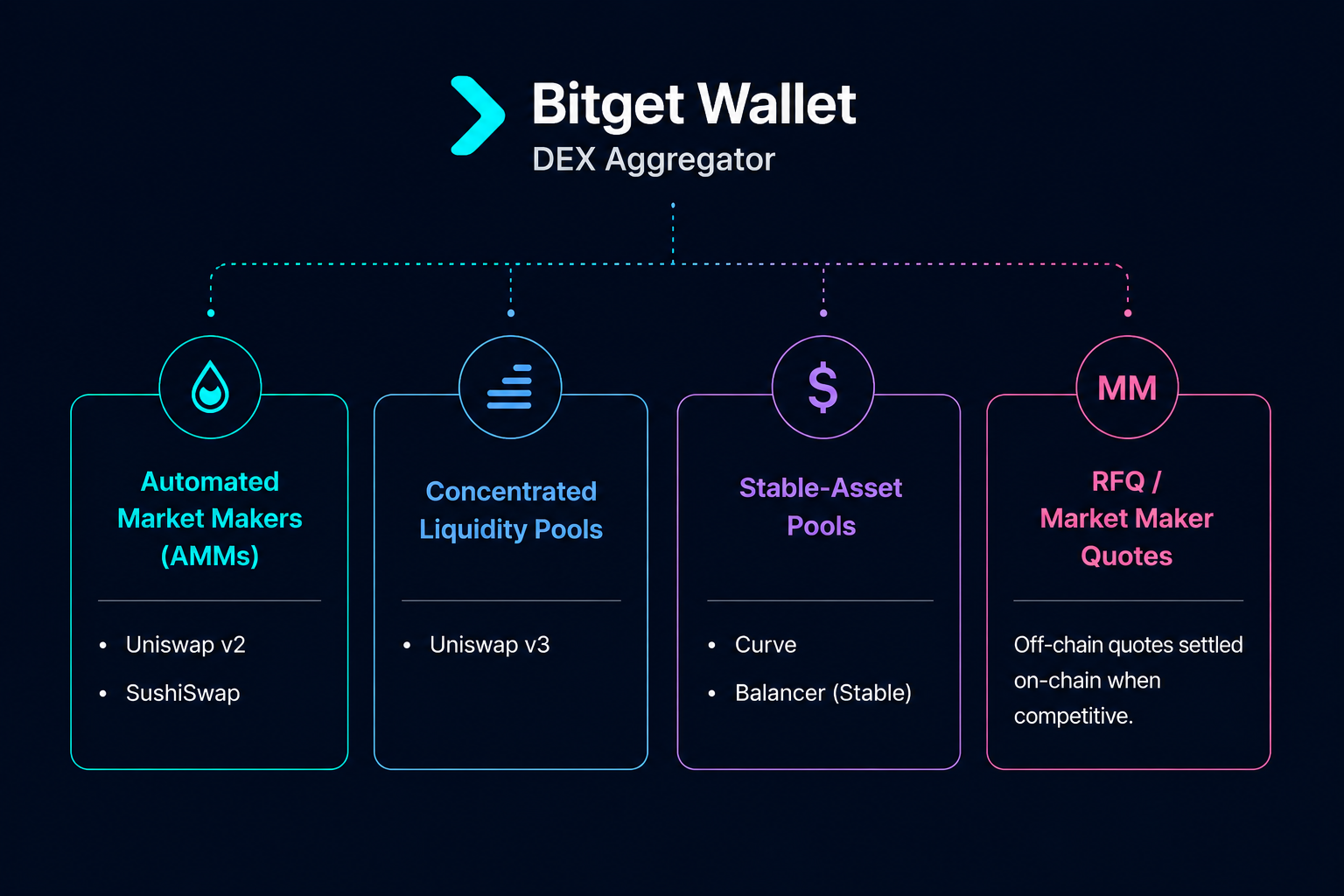

At the heart of Bitget Wallet is its proprietary multi-chain DEX aggregator, designed to deliver users with swap quotes and execution prices optimised for reliability, gas cost and speed. Bitget’s aggregation engine does this by aggregating liquidity from over 100 different DEX (decentralised exchange) venues, across 10 different blockchains. It then routes token swap orders across different liquidity providers, including AMMs (automated market makers), ProAMMs (prop AMMs) and RFQ (Request for Quote) venues, aiming to ensure price consistency and high execution success rates.

Users can make swaps via the front-facing wallet application, or via Bitget Wallet’s Enterprise Trading API. The latter is a B2B version of the same execution engine, exposed as an API. This is designed to be an infrastructure layer that supports institutional-grade, on-chain trading services. It allows third-party aggregators, trading frontends, wallets and applications to execute swaps on-chain, and conduct cross-chain asset transfers through a single API integration that uses Bitget Wallet’s DEX routing infrastructure.

This optimised framework has helped support token swaps into a single unified platform, designed to circumvent the complexities of navigating a multitude of external platforms when making token swaps and trading between assets on-chain. It also serves as part of Bitget Wallet’s broader evolution from a consumer wallet into a wider on-chain finance infrastructure provider.

However, DEX aggregation is now becoming a baseline capability for most venues that allow users to trade digital assets. As the size of the stablecoin and real-world asset market grows, more applications get built on-chain, and more users (both retail and institutional) enter the DeFi (decentralised finance) space, liquidity may become more fragmented across base layers and DeFi applications.

Therefore the next phase of crypto trading infrastructure is transitioning from simple quote aggregation towards consistent, institutional-grade execution quality. In this report, we aim to provide an overview of the current DEX aggregation landscape and evaluate Bitget Wallets’ Enterprise API and DEX aggregator through a variety of different metrics.

Over the past few years, the ratio of trading volumes on DEXs vs CEXs (centralised exchanges) has steadily risen. In 2020, that ratio was only 0.09%. By June 2025, it peaked close to 22% and has since hovered around 14%. Decentralised exchanges are increasingly taking away volume share from centralised exchanges.

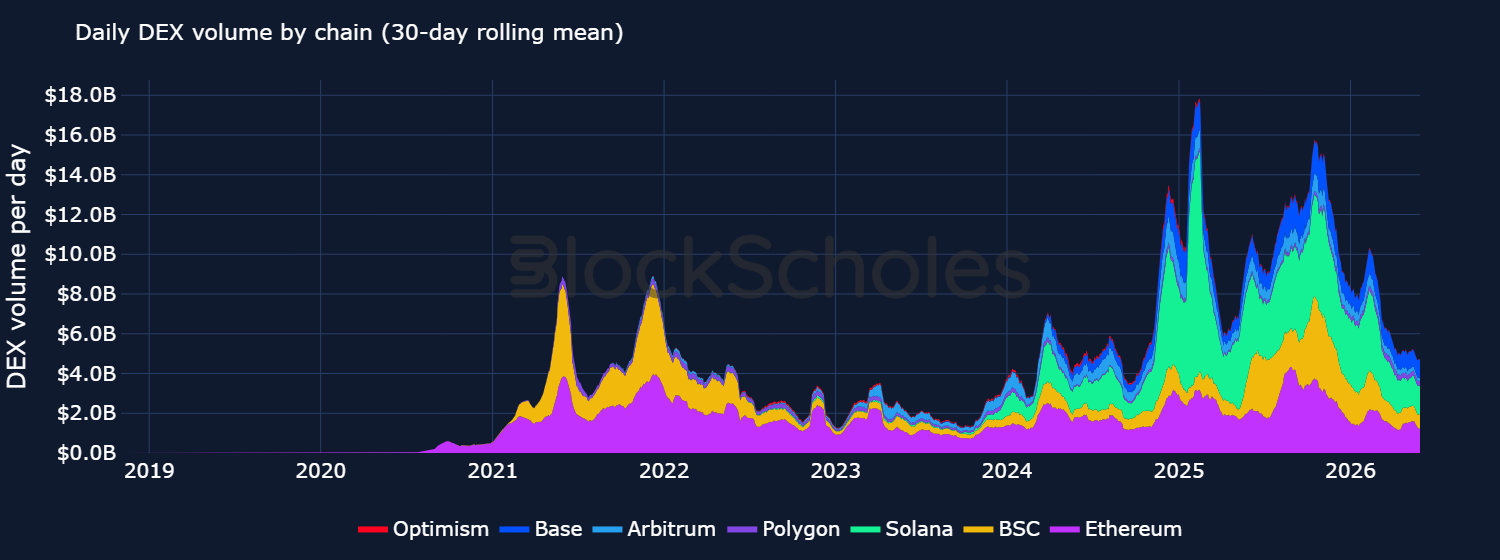

However, not only is volume and liquidity now more natively split across DEXs and CEXs, it is also fragmented across many different blockchain networks, as market participants turn towards a wider variety of chains to meet their use cases.

In 2019 and 2020, almost all DEX volumes transacted on Ethereum. Today, daily DEX volume is distributed across Ethereum, BNB Chain, Solana and a number of Ethereum-based layer-2 networks. This means that the same asset can trade in a multitude of pools across a multitude of chains. For DEX aggregators, this poses an execution problem. The router needs to be aware of where the best price is at the moment of quoting, across all of these venues, and route the order to that venue with gas, slippage, and settlement risk priced in.

The average size of on-chain transactions is growing over time, too. At the start of the year, the average swap size on Bitget Wallet was around $180. In the space of five months, it has increased five-fold, even peaking above $1,200 in mid-May. The trade volume spread across disparate blockchain ecosystems is increasingly of institutional size.

Increased on-chain activity and an aggressive push from institutions to enter the digital assets space also means the demand for institutional-ready settlement rails has increased exponentially – and stablecoins have widely been adopted as that settlement rail. Between 2018 to 2026, the supply of USD-pegged stablecoins grew from under $1B to over $300B. This is a market that Treasury Secretary, Scott Bessent, claimed could exceed $2T by 2028.

With users most commonly trading either a stablecoin pair such as USDC / USDT or a crypto token against a stablecoin, execution infrastructure that can support large stablecoin orders and swaps will continue to grow — especially as the market demand for stablecoins grows too.

The dynamic and structural change in the landscape of crypto trading towards DEXs has increased the demand for efficient DEX aggregators that can handle a growing number of on-chain token swaps in a competitive, low slippage manner. Additionally, it has resulted in an increased demand for efficient routing paths which best optimise capital efficiency, execution quality and fill reliability — particularly as trade size increases over time.

Execution quality can be measured in multiple dimensions: competitive execution prices, transaction reliability, depth of liquidity, slippage, and fees all impact the trade that a user ultimately transacts.

We first evaluate:

As key measures of the quality of execution on a DEX aggregator.

This is the most direct measure of execution quality – how competitive an aggregator’s headline swap price is. A consistent basis-point advantage can compound for institutions trading in size and volume. Scaled across many trades, we can understand if an aggregator has a structural pricing advantage over the routing engine of another.

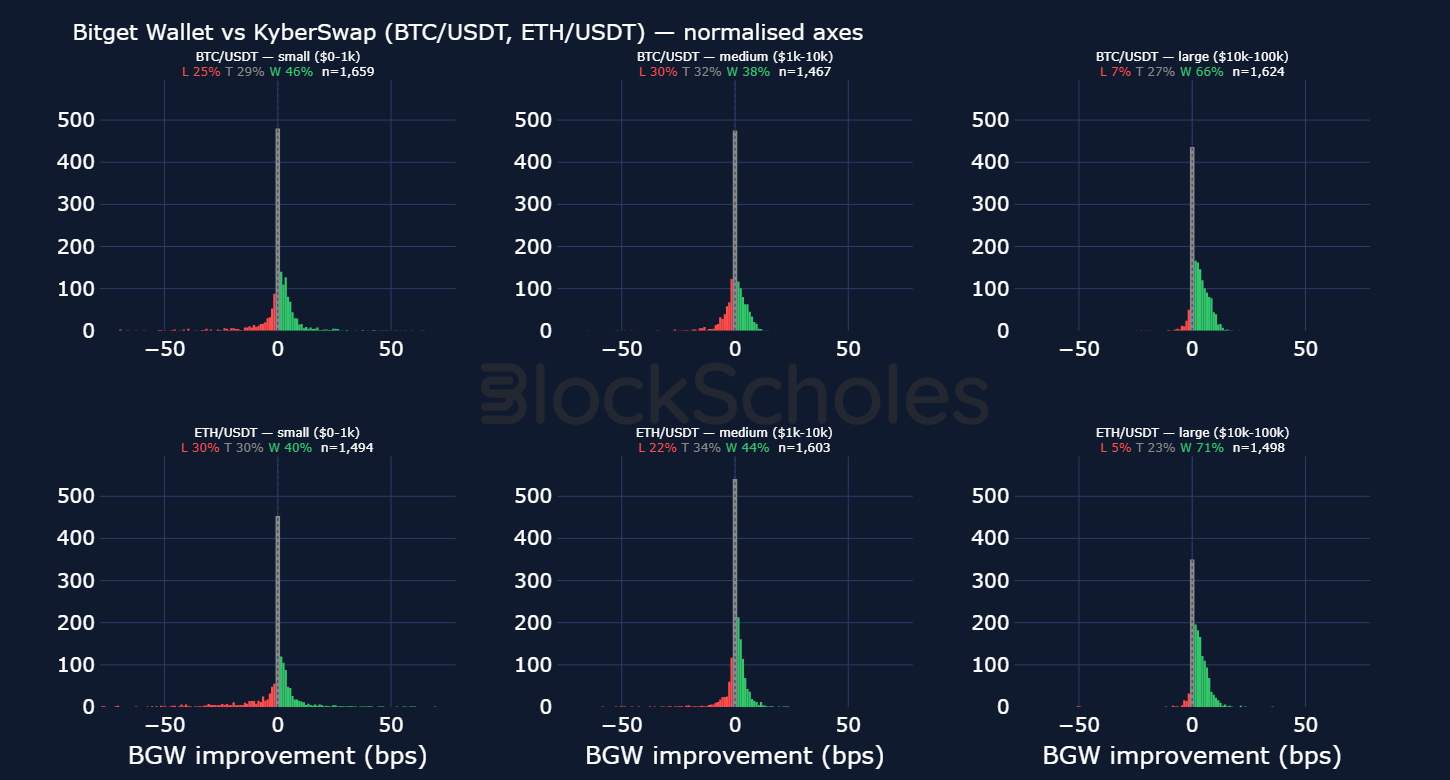

In the charts below we compare swap quotes at different trade sizes across different aggregators. For example, we compare the quote Bitget’s DEX aggregator provided a trader looking to swap X USDT tokens for ETH, relative to the quote that user would have received from other DEX aggregators, such as 0x and Kyberswap.

Each chart is a histogram where the horizontal axis measures how much more (or less) of the destination token Bitget Wallet's aggregator returned compared to the competitor, expressed in basis points. The vertical axis is the number of quote comparisons in each bin size.

A positive value (green bar) therefore indicates Bitget Wallet's aggregator provided a better quote (a lower price per token) than the compared aggregator, while a negative value (red bar) represents the opposite. Grey bars indicate when both aggregators quoted an amount within 1bps from one another — treated as ties.

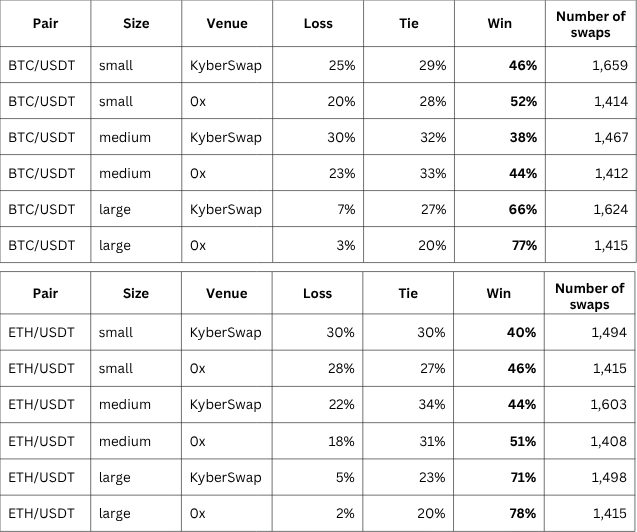

Initially, we compare the BTC/ USDT and ETH/ USDT token pair on Kyberswap and 0x and the SOL/USDT pair on Jupiter.

Bitget Wallet's aggregator shows a pricing edge over KyberSwap that is clearest at large trade sizes across the BTC/ USDT and ETH/ USDT spot pairs. For BTC/USDT, Bitget Wallet wins 66% of large ($10k-100k) quote comparisons, losing only 7% of the time. It provides a median advantage of +2.6 bps per quote for large quotes.

A 2.6 bp median advantage on a $50,000 trade is a $13 increase in output per trade. Taken alongside a 66% win-rate at large size means, across our sample data, nearly seven in ten institutional-sized BTC/USDT swaps would be priced more competitively by Bitget Wallet.

The pattern on ETH/USDT is even sharper for large trade sizes: Bitget Wallet wins 72% of large comparisons, losing only 5% of the time and has a median advantage of +2.7 bps.

The same comparison against 0x, another DEX aggregator, yields a similar result. Bitget Wallet delivers a stronger quote to traders for BTC/USDT swaps 77% of the time, while losing only 3% of the time. The median advantage is +3.2 bps for trades between $10k and $100k.

Similar to the comparison against KyberSwap, the win-rate percentage is 1pp higher for the ETH/USDT pair at 78% and the median advantage is +3.3 bps for larger sizes.

Across our sample data, this suggests Bitget Wallet’s aggregator outperforms at large trade sizes against other Ethereum-based aggregators for the most liquid crypto token pairs.

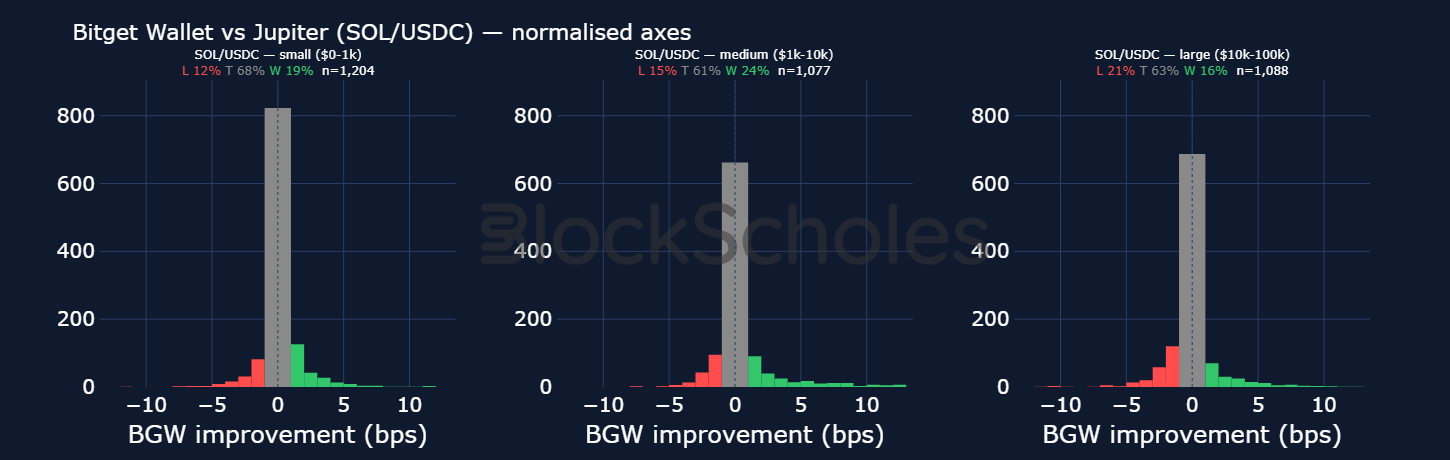

Bitget Wallet's pricing is comparable with Jupiter on SOL/USDC trades. Jupiter is the incumbent aggregator on the Solana network utilising liquidity across all major Solana-based DEX’s, including Raydium, Orca and Meteora. For example, over the past 30 days, Jupiter’s aggregator conducted just under double the volume of the second largest aggregator on the network.

Despite that dominance, on SOL/USDC — the deepest SOL-stable pair on Solana — Bitget Wallet's quotes sit within a basis point of Jupiter's the majority of the time. Ties account for 68% of small-size comparisons and 63% of large. Where the comparison does break a tie, Bitget Wallet wins more often than it loses at small and medium sizes (19% vs 12%, and 24% vs 15% respectively) and is close to even at large size (16% vs 21%).

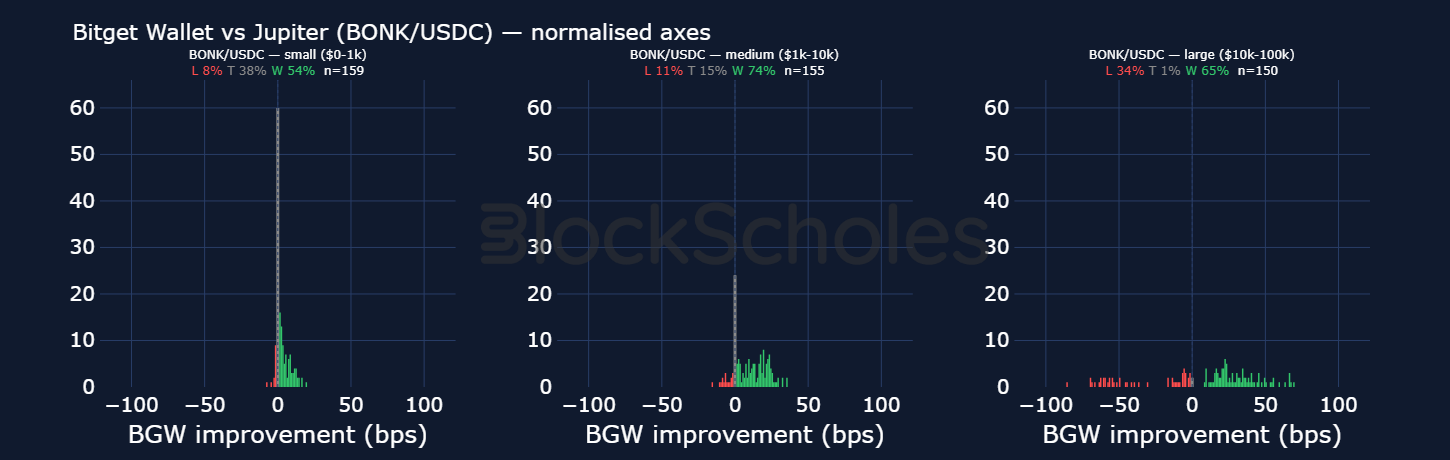

The Solana network is also home to more speculative, smaller-cap tokens which allows us to compare how aggregators perform on quotes that rely on thinner, more fragmented liquidity.

Looking at the BONK/ USDC pair, Bitget Wallet shows a clear pricing edge at every trade size, sharpest in the small and medium buckets. For small trades, Bitget Wallet wins 54% of the time and loses only 8%, well above the 38% tie rate. The advantage widens for trades between $1k-10k: Bitget Wallet wins 74% of comparisons against Jupiter while losing 11%, with a median quote advantage of +12 bps per trade.

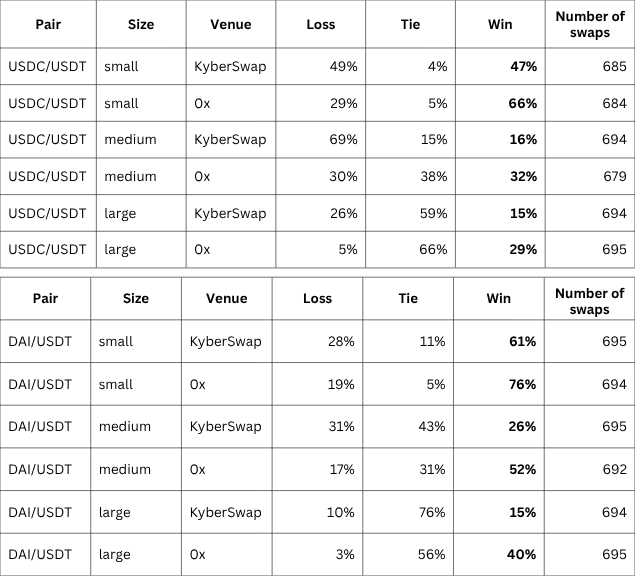

The analysis above provides some insight into price competitiveness across the three token pairs most synonymous with crypto — BTC, ETH and SOL, as well as a less liquid, smaller-cap token. We can extend this to compare competitiveness within stablecoin-to-stablecoin pairs.

According to data from Bitget Wallet, between April and May 2026, USDC/USDT was the second-most-traded pair by trade count (5.1% of all swaps), and DAI/USDT was sixth (2.7%). The same methodology is retained, but instead we define a tie in price competitiveness when two aggregators quote prices within a tighter range of 0.1bps, not 1bps. This is to account for a tighter spread in the liquidity pools for stablecoins compared to other crypto assets.

Across the three EVM-based aggregators, there is no clear price competitive edge for stablecoin pairs.

Slippage is defined as how far the average execution price of a market order drifts from the mid-price as the order size grows.

We use the same swap quotes collected in the price-competitiveness section above — every quote across the three trade-size buckets (small: $0–$1k, medium: $1k–$10k, large: $10k–$100k) — plus a dedicated reference bucket of trades at exactly $1,000.

For each aggregator on each pair, we use the price it quoted on a $1,000 trade as our estimate of the "mid"-price at that time. We focus on the ETH/USDT and ETH/USDC pairs for the EVM-based aggregators and the SOL/USDT and SOL/USDC pairs for the Jupiter comparison. Jupiter is a Solana-native aggregator and doesn't natively quote ETH/USDT — wrapped ETH on Solana is quotable but introduces a bridged ETH-to-ETH basis, so it's excluded.

Note: Automated market maker models don't have a mid-price in the same way as central-limit order books (CLOBs). The mid-price is the exact rate at which a swap would occur for a trade of infinitesimal size, absent any trading fees or slippage. A $1,000 trade is small enough that it doesn't meaningfully move the underlying liquidity pools, so the price it receives acts as a close estimate for the rate a trader would have got on a 'zero'-size trade.

Every medium and large bucketed quote from the same aggregator on the same pair is then compared to the aggregator's quote on a $1,000 trade (our reference for the mid-price) at that time, This allows us to see how the trader's price degraded as the aggregator was asked to swap a larger amount.

As an illustration: if a $50,000 ETH swap returns the user 23.81 ETH (an implied $2,099 per ETH) and a $1,000 swap was returned at $2,100 per ETH, the larger trade gave up roughly 5 bps, around $25 of value, to absorb the $50k size through that aggregator's route.

The chart above shows the slippage degradation for each aggregator on each pair: the change in median slippage moving from a $1,000 reference trade to a $10k–$100k trade.

On ETH/USDT, Bitget Wallet's slippage degrades by just +2.9 bps moving from the $1,000 reference to a $10k+ trade, against +7.5 bps for KyberSwap and +5.5 bps for 0x. On a $50,000 swap, that's roughly $15 of execution cost through Bitget Wallet versus $37 through KyberSwap and $27 through 0x.

On ETH/USDC the same pattern holds: Bitget Wallet degrades by only +2.3 bps versus +8.6 bps for KyberSwap and +6.7 bps for 0x — on the same $50,000 swap, around $12 of cost through BGW, $43 through KyberSwap, and $34 through 0x. Across our sample, Bitget Wallet handles size on Ethereum-based majors roughly 2–4x more tightly than its peers.

On SOL/USDT and SOL/USDC, Bitget Wallet and Jupiter both deliver very tight slippage control. Both degrade by under 1 bp moving from a $1,000 reference to a large trade — on a $50,000 swap, that's under $5 of execution cost through either aggregator. Bitget Wallet has a slight edge on SOL/USDT (+0.5 bps versus Jupiter's +0.7 bps), while Jupiter has a slight edge on SOL/USDC (+0.5 bps versus BGW's +0.9 bps).

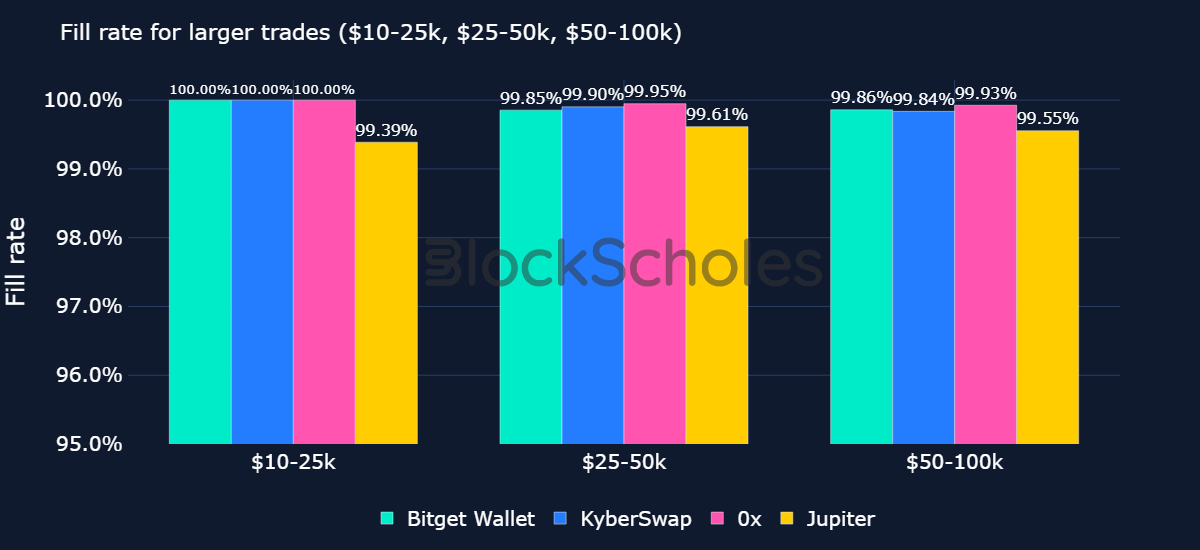

For institutional traders, execution quality is not just about maximising the amount of the destination token received or minimising slippage. Those metrics are clear measures of how competitive an aggregator's quoted route is, but they only matter if the quoted swap route can actually be executed. Fill reliability therefore sits alongside price competitiveness as a core execution metric and it measures something simple: given a request for a quote from a trader, how likely is it that the order gets filled by the aggregator? Can the aggregator not only find the best route for delivering the route such that the trade is executed?

This is more insightful when focusing on larger trades, where slippage is a bigger concern (and therefore the need to split a transaction across different routes is more necessary) and more fragile to execution risk.

The chart below focuses on swap quotes at three bands ($10k–25k, $25k–50k, $50k–100k) for the same BTC, ETH, SOL and stablecoin pairs. Across the board, fill reliability on liquid majors and stablecoins does not materially change: all four aggregators are capable of returning an executable quote on virtually every large-sized request with very high reliability rates. Jupiter does however stand out: despite having an above 99% fill rate, it is noticeably lower compared to the other three aggregators.

A quantitative comparison between different aggregation engines can help traders identify which aggregator is best suited to which swap. However, it is equally helpful to understand the architectural design choices that power these aggregators. We find that underneath the hood, most aggregators offer similar solutions to ensure execution quality. For example, all four aggregators analysed in this report utilise liquidity from a variety of different sources, integrate gas costs directly into provided quotes, and for larger orders, avoid using one liquidity source to minimise slippage.

Broadly speaking therefore, the competitive edge of an aggregator comes down to two things: the breadth of liquidity sources it can aggregate from, and a smart order routing algorithm that searches through that liquidity to split a trader’s swap.

All of the aggregators discussed so far in this report utilise various sources of liquidity:

Once an aggregator has integrated with these various liquidity protocols and providers, its routing algorithm faces a number of unique problems.

One such problem is how to maximise gas efficiency. Gas costs can be thought of as the on-chain settlement cost a user pays beyond just the top of the quoted output. A simple router may provide a quote which appears very competitive to the trader, but once gas fees are accounted for, the user nets less than the quote implies, resulting in a less-than-optimal quote, once all fees are accounted for. A gas-aware routing engine closes that gap.

Bitget uses a “Progressive Gas Algorithm” to solve this problem. Suppose its routing engine identifies that the best execution price for a trader’s swap would require utilising liquidity from more than one AMM pool, or via an intermediate token. More complex multi-hop / pool routes can squeeze out a marginally better price, but cost meaningfully more gas to settle.

Rather than choosing the pools that simply give the user the largest amount of the destination token and then considering the gas cost of that route afterwards, the algorithm does two things: it factors gas costs into the route initially, and for swaps that involve more than one route or pool, it progressively factors in the gas cost of each route. This means the algorithm actively considers whether an extra unit of the destination token is worth the additional gas cost from choosing that route.

Kyberswap implemented a similar mechanism under a different name: “Dynamic Trade Routing”. According to its documentation, its aggregator can be configured to minimize the number of transfers and that its competitive edge comes from its ability to calculate the most efficient trade route taking into account swap rates, slippage, and gas fees.

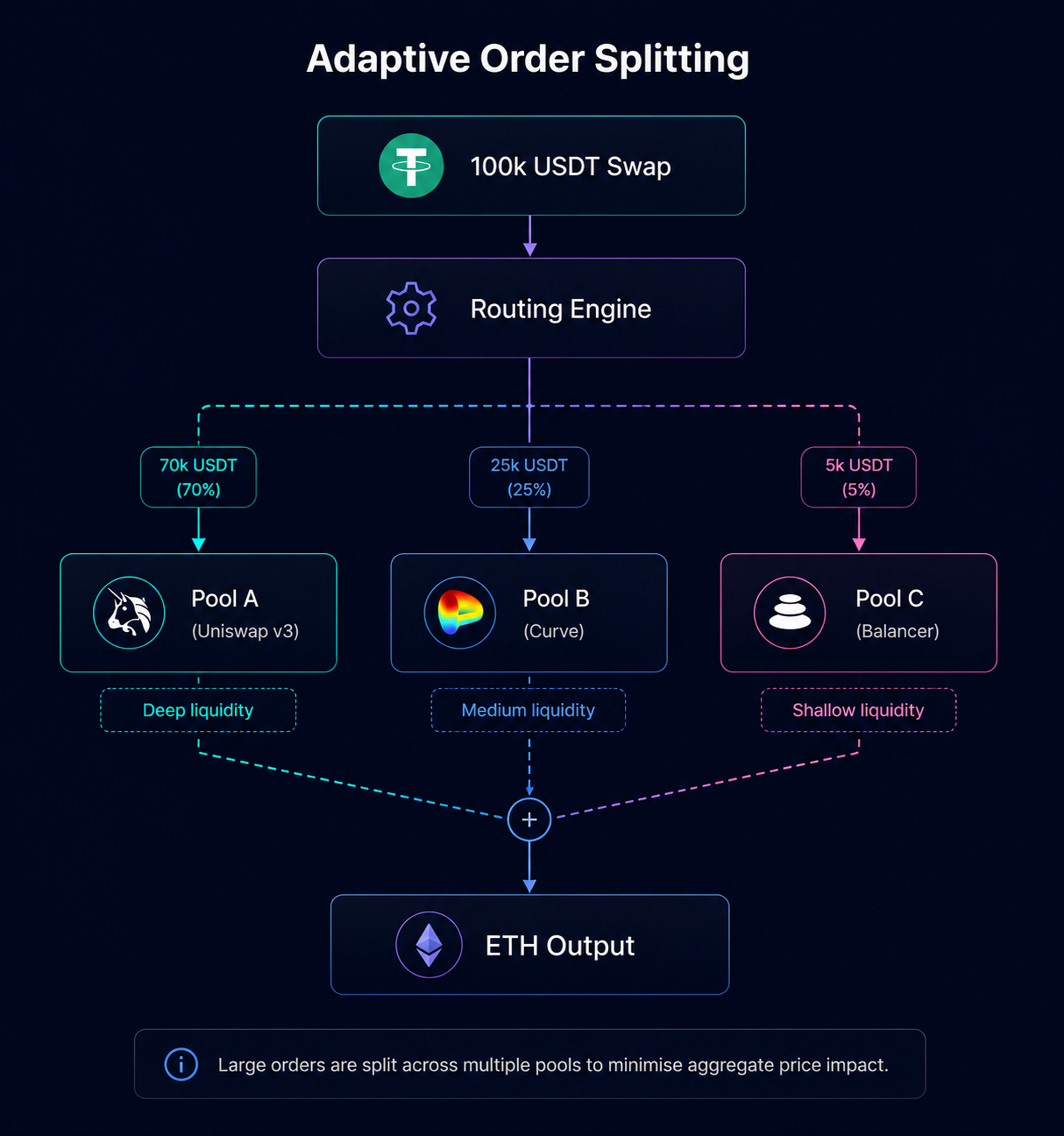

A second problem aggregators need to deal with is when a single pool cannot absorb a large swap without significant slippage. Price impact on a single AMM is convex in trade size, therefore splitting a large $100k order across several pools often leads to a better execution price than routing the order through one pool.

Bitget’s aggregator uses an “Adaptive Order-Splitting Algorithm” that is designed to dynamically split large swap orders across pools depending on their depth, instead of just relying on a fixed percentage split (e.g., for a $100k order, use liquidity from 4 different pools at 25% each). For example a $100K USDT swap for ETH might be routed 70% through Uniswap’s v3 ETH pool, 25% through Curve’s ETH pool and 5% through Balancer’s ETH pool.

This is something other aggregators do also — Jupiter’s routing engine, Metis, for example incrementally builds a route that splits and merges liquidity from different pools through the quote finding process, aiming to ensure optimal prices for more complex trades. KyberSwap's “Dynamic Trade Routing” also splits and merges orders across AMM and orderbook-DEX liquidity on the same principle.

The architectural DNA across most aggregators underneath the hood is quite similar, with different names explaining each design choice:

One area where Bitget Wallet does differentiate itself is in its real-time risk-filtering layer, called Sentinel. This is designed to exclude pools that display abnormal behaviour at routing time. This feature is designed to maximise execution feasibility and minimise the number of quotes that either revert or execute materially below the quoted swap rate.

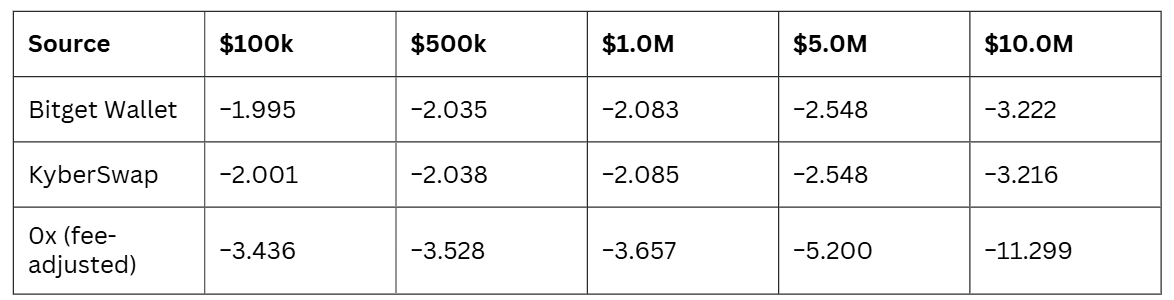

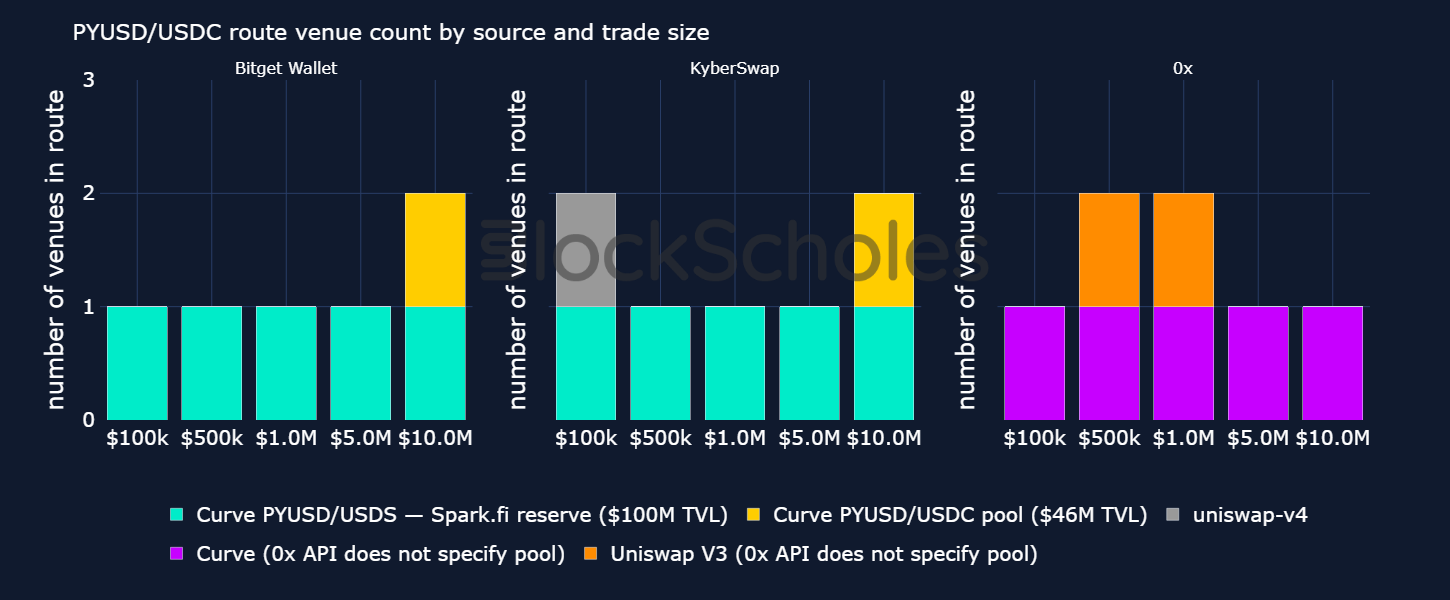

To see how some of these architectural design choices show up in real-time, across different sized swap quotes, we requested quotes on the stablecoin pair PYUSD/USDC (PYUSD being PayPal's USD-pegged stablecoin) at five different sizes ($100k, $500k, $1M, $5M, $10M) across Bitget Wallet, KyberSwap and 0x.

Up to $5M, Bitget Wallet and KyberSwap return functionally identical quotes. Both send 100% of the order through Spark.fi's PYUSD/USDS pool — the deepest single venue on the chain — and the output amounts match to four decimal places.

To utilise the deeper liquidity of this pool, the user’s USDC is actually first converted to USDS through two zero-slippage facilities: Maker's Lite-PSM (which converts USDC ↔ DAI at exactly 1:1) and Sky's peg-swap contract (DAI ↔ USDS at exactly 1:1, since USDS is Sky's rebrand of DAI). The resulting USDS is then swapped into PYUSD through the Spark.fi Curve pool.

While a relatively large pool, at a trade size of $10M, the Spark.fi pool would still result in marginal price moving against the user. Both Bitget Wallet and KyberSwap respond by splitting the order across PYUSD/USDS and PYUSD/USDC pools, while 0x does not. The result is around 8 bps of slippage protection (or $8,000) via Bitget Wallet and Kyberswap relative to the single-pool route offered by 0x. This case study showcases the value of the adaptive order splitting algorithm used by aggregators such as Bitget Wallet and searching across the full set of available liquidity pools rather than purely routing an order through the largest pool.

Bitget Wallet's DEX aggregator and Enterprise API are built to deliver consistent execution quality across fragmented on-chain liquidity. The aggregator’s routing engine is designed to provide swap quotes that are gas-efficient, split across pools to minimise slippage, and utilise liquidity across different on-chain and off-chain providers. Across the many metrics analysed in this report, a number of findings stand out.

Bitget Wallet's edge over competitors is at large trade sizes on Ethereum-based majors. For BTC/USDT and ETH/USDT, Bitget Wallet wins 66–78% of large-bucket quote comparisons against KyberSwap and 0x. Slippage is also considerably lower across larger trade sizes ($10k-100k) relative to other EVM-based aggregators, degrading by under 1 bp on ETH pairs for example.

That edge becomes less apparent on SOL-stablecoin pairs against Jupiter — the incumbent DEX aggregator on the Solana network. Aggregators also converge on stablecoin-to-stablecoin swaps, where no aggregator shows a clear, structural edge.

Aggregators differentiate themselves on the implementation of those choices (with similar design choices underneath the hood). For example, all four aggregators analysed across this piece use algorithms and routing logic to split swap quotes across different liquidity pools. Whether that occurs in practice across larger trade sizes is however what sets them apart. In our case study of large-sized PYUSD/ USDC swaps, Bitget Wallet and KyberSwap both split orders across two Curve pools, preserving roughly 8 bps of value relative to a single-venue alternative — around $8,000 on a $10M notional for example.

These findings are important given the underlying structural change in the decentralised exchange space. For example, average swap sizes on Bitget Wallet rose roughly five-fold in the first five months of 2026, peaking above $1,200 – showing the importance of execution quality as average trade size continues to grow.

Bitget Wallet's Enterprise API positions itself in the next layer of DEX aggregation, where the focus is on execution infrastructure. The results in this report suggest its routing engine is competitive in some of the key dimensions that institutional and larger-sized traders will be looking out for. Additionally, the Enterprise API and aggregator engine will continue to add value for DeFi participants, particularly as the liquidity landscape further fragments across blockchains and decentralised exchanges.

.jpg)

.jpg)