Thahbib Rahman

Research Analyst

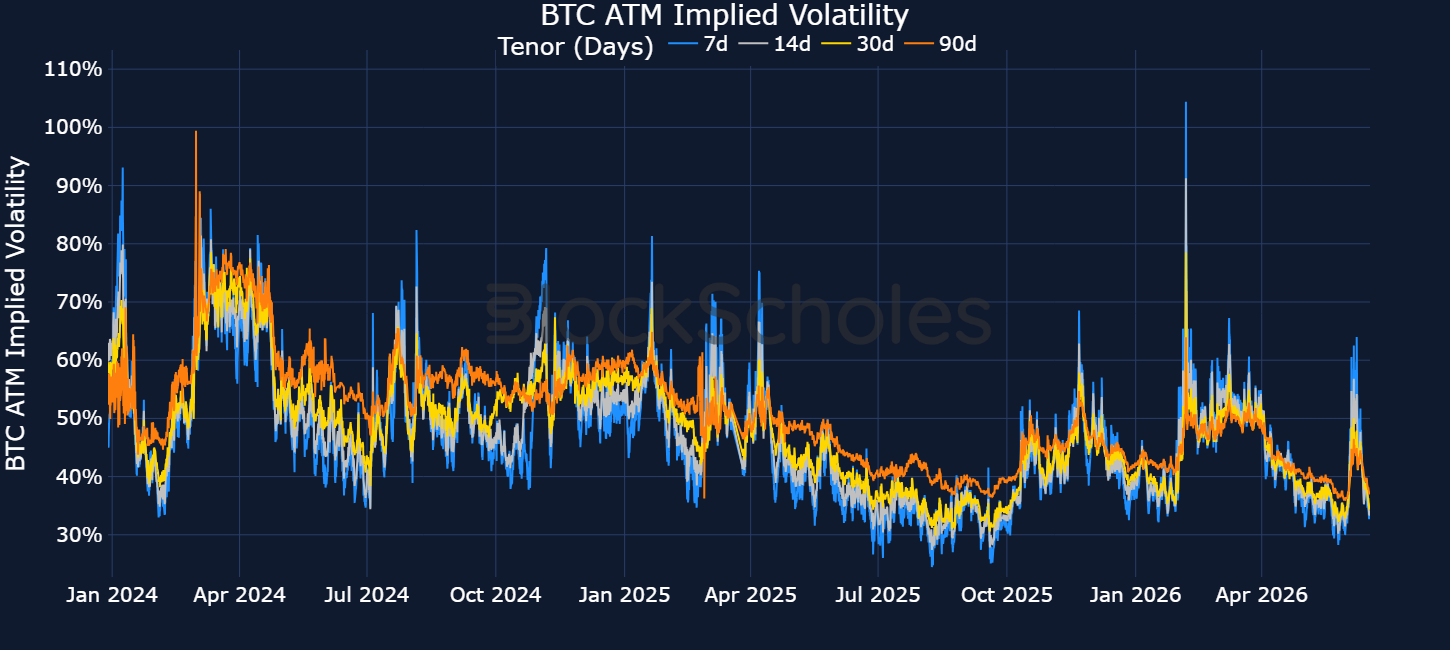

Realized volatility has fallen sharply following the announcement of an interim peace agreement between the US and Iran, reversing much of the volatility spike that accompanied BTC's brief drop below $60K earlier this month. As such, realized volatility is returning to the subdued levels that have characterized the May-to-August summer period since 2023. Options markets are increasingly pricing for those calmer conditions to persist. Short-dated BTC at-the-money implied volatility has fallen to 33%, only marginally below longer-dated tenors at 37%, leaving volatility expectations close to their year-to-date lows across the term structure.

Realized volatility has fallen sharply following the announcement of an interim peace agreement between the US and Iran, reversing much of the volatility spike that accompanied BTC's brief drop below $60K earlier this month.

As such, realized volatility is returning to the subdued levels that have characterized the May-to-August summer period since 2023.

Options markets are increasingly pricing for those calmer conditions to persist. Short-dated BTC at-the-money implied volatility has fallen to 33%, only marginally below longer-dated tenors at 37%, leaving volatility expectations close to their year-to-date lows across the term structure.

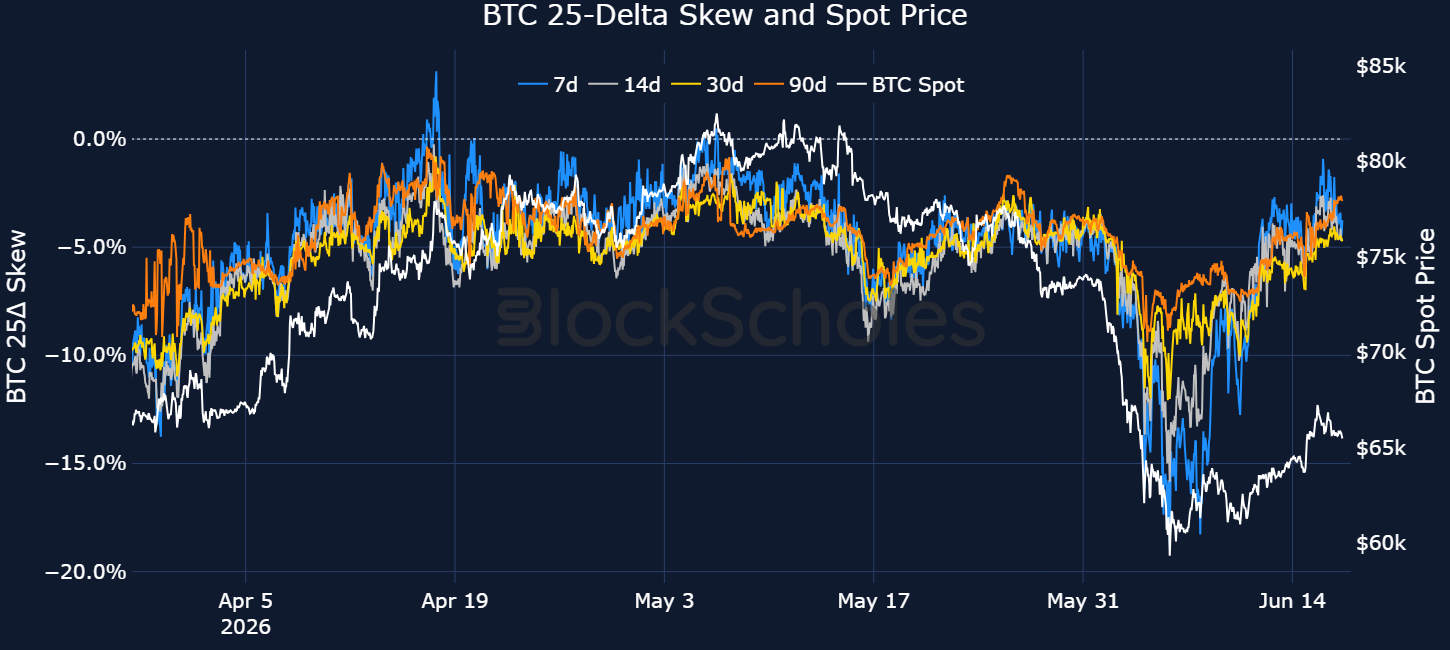

The improvement in macro sentiment has also driven a significant reduction in demand for downside protection.

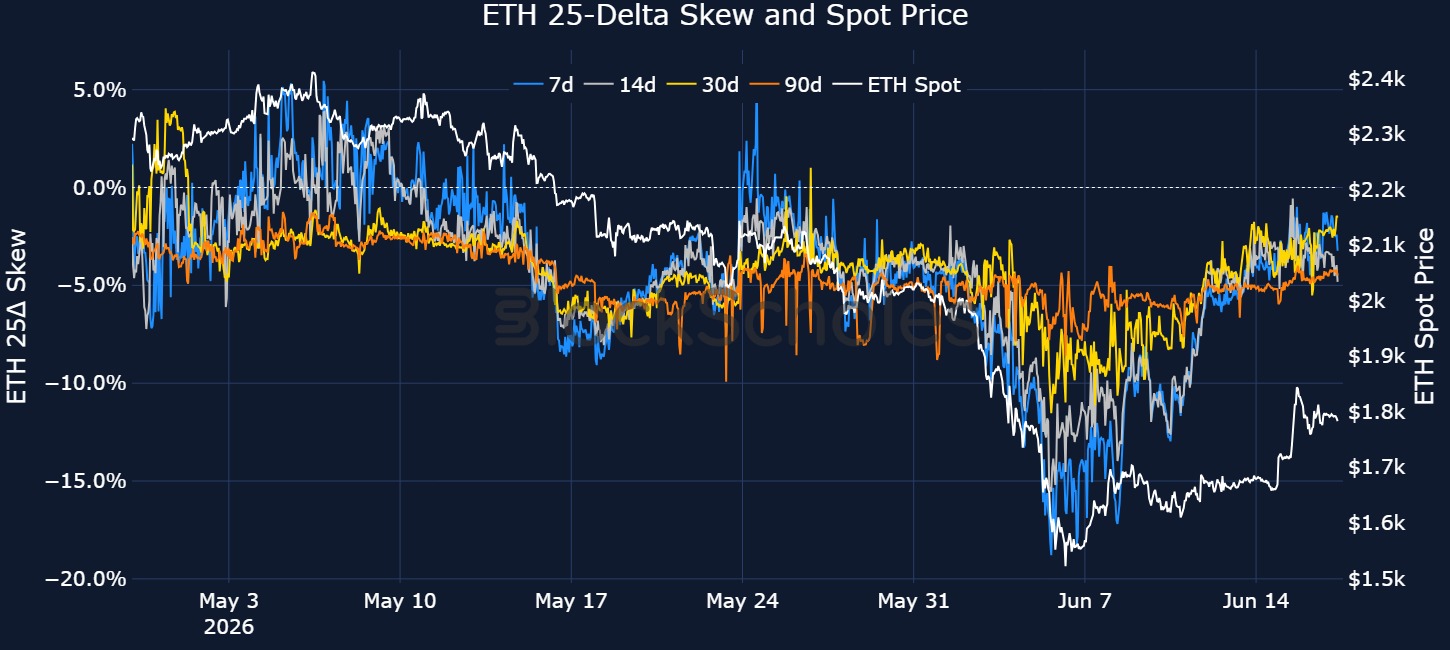

BTC's 7-day 25-delta put-call skew has recovered from -18% to -1.9% in just two weeks, while ETH's equivalent skew has rebounded from -19% to -1.0%, reflecting a substantial unwind in the bearish positioning that dominated options markets during the recent selloff.

While traders have become markedly less defensive, options markets have not yet turned outright bullish.

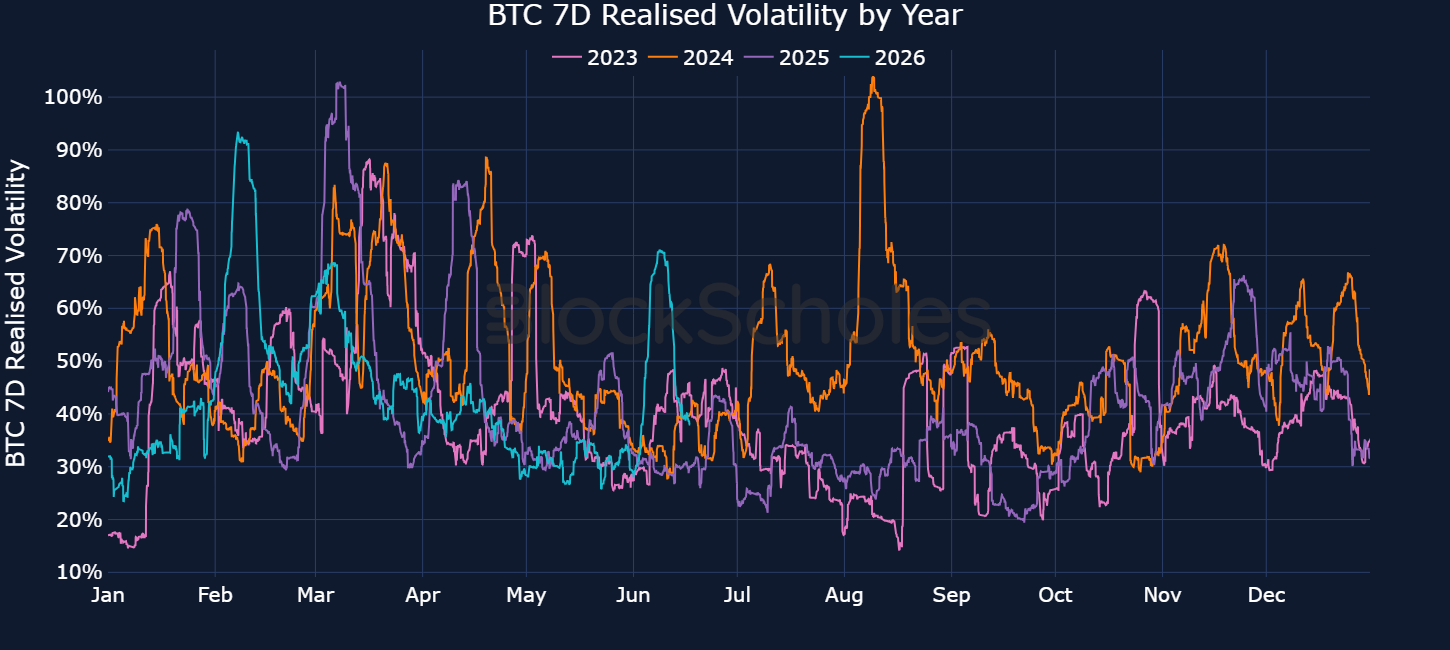

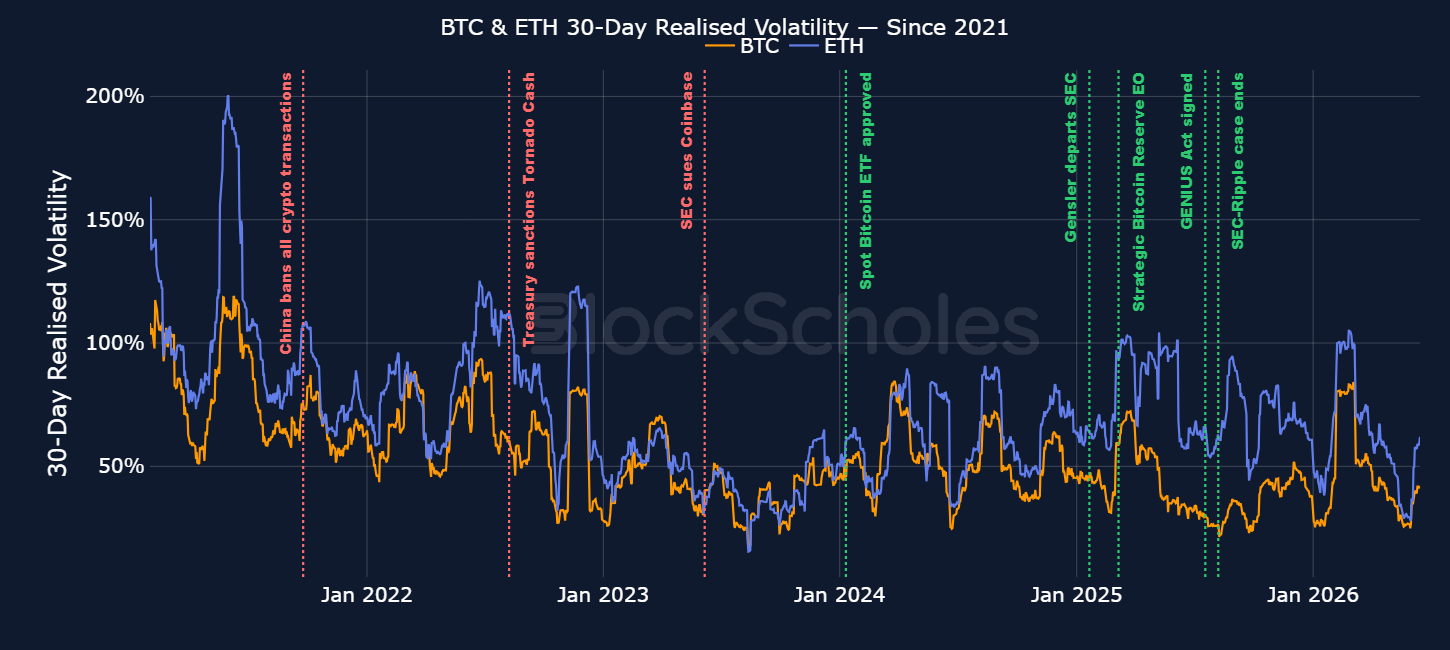

Since 2023, volatility in crypto has shown seasonal patterns.

In particular, realized volatility – a measure of the actual historical price fluctuations over a given period – has fallen to the lower end of its yearly range around the summer months of May to August.

The chart below plots the 7-day realized volatility on hourly returns and reveals that realized volatility often moves sideways between 30-40% through the summer, before a sharp upward bounce around September time.

In May 2026, 7-day realized volatility fell to 26%, within 2 percentage points of the year-to-date low realized in early January. After a brief move higher in volatility – when spot price fell below $60K – the announcement of an interim peace deal between the US and Iran has seen realized volatility drop by 30 percentage points from its high of 70% to 40%. It is now once more approaching the range we’ve seen it linger around in previous summers.

With volatility having eased significantly over the past week, options traders have revised down their expectations for future volatility. Recent diplomatic efforts to bring an end to the four-month-long conflict have encouraged traders to price for a continuation of the calmer market conditions observed in recent sessions, resulting in lower at-the-money implied volatility across maturities.

7-day BTC ATM IV (a forward-looking measure of the volatility with which traders expect BTC to trade over the next seven days) is currently at 33%, while the IV of longer-dated options is only marginally higher at 37%. That suggests that, for now, demand for options is close to its year-to-date low across all maturities.

Sentiment across risk-on assets this week has moved higher amidst the sharp drop in oil prices, which is rapidly approaching pre-conflict levels. BTC briefly rose to a two-week high, jumping above $67K and pushing options traders to further reduce their demand for downside protection.

The 7-day 25-delta put-call skew, a measure of the implied volatility difference between equally out-of-the-money put options and call options, rose to a one-month high of -1.9%. While the negative value still shows more demand for put options over calls, it marks a significant turnaround from the -18% skew only two weeks ago. The peace deal in the Middle East has not been enough to turn traders bullish just yet, but it has driven a significant reduction in the bearish sentiment that has characterized options markets for most of this year.

ETH volatility smiles show a similar recovery in sentiment. As spot price broke above $1,800 earlier this week, 7-day put-call skew nearly shifted bullish, trading at -1%. Since the June 6 local bottom, spot price is up more than 15%, while skew has recovered from -19% all the way to -1.0%.

Regulatory developments have long played an important role in shaping sentiment across crypto markets, often becoming the dominant narrative as they unfold.

In the spot market, major policy milestones can have a visible impact on price action, particularly when they are perceived as supportive for the sector.

Examples include the approval of spot ETFs and the run-up to Gary Gensler’s departure from the SEC, both of which formed part of a broader market expectation that the U.S. regulatory environment would become more lenient toward crypto.

However, once these developments are confirmed, the data does not always move in the direction that might be expected.

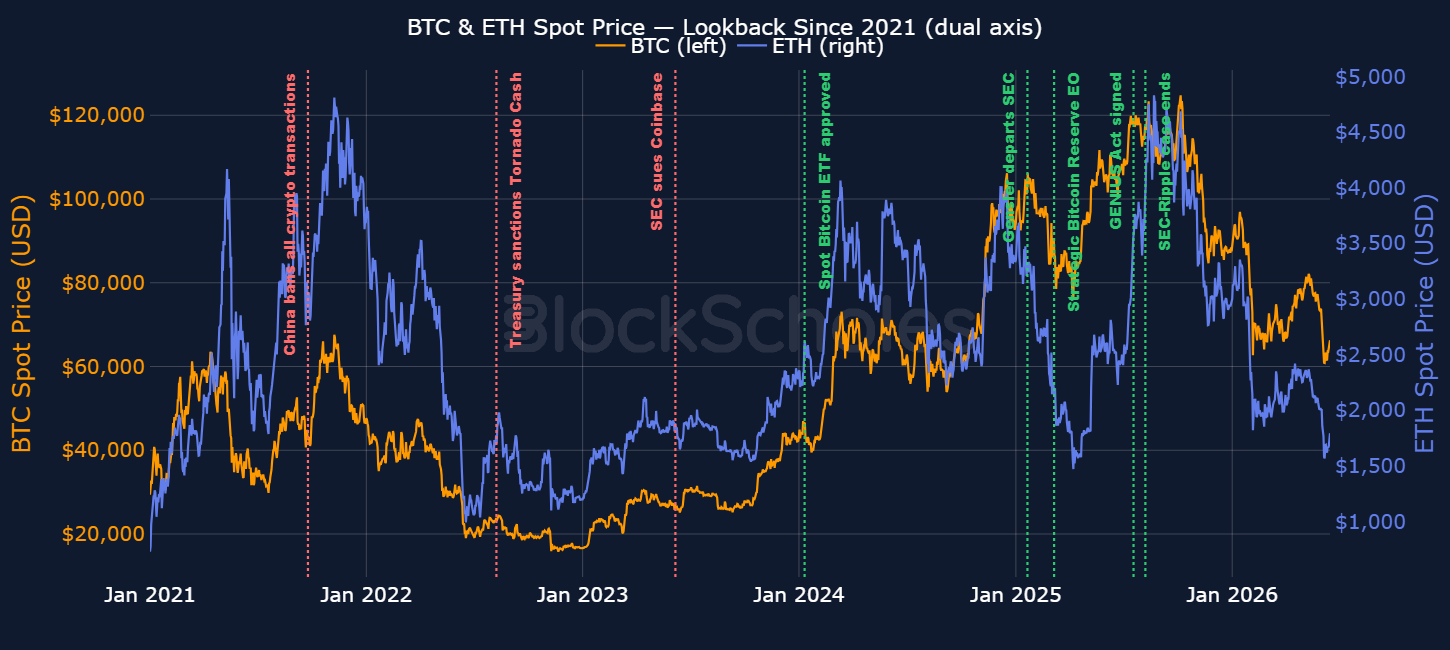

The chart below tracks a range of policy events, with restrictive developments, such as China’s ban on crypto transactions, shown in red, and more constructive developments, such as the GENIUS Act being signed, shown in green.

Across these examples, the largest 30-day gain followed a restrictive event, with BTC rising 42.2% after China’s ban.

By contrast, the three largest 30-day declines followed pro-crypto developments:

ETH, however, shows a clearer relationship between positive policy developments and stronger price performance.

Following the GENIUS Act, ETH outperformed BTC by 26.5 percentage points, with ETH rising 26.0% while BTC fell 0.5%. This may have reflected the market’s expectation that stablecoin legislation would benefit blockchains such as Ethereum, which host a large share of stablecoin activity across both the base layer and Layer 2 networks.

ETH also outperformed BTC by 15.4 percentage points after the SEC-Ripple dismissal, rising 9.2% compared with BTC’s 6.2% decline. This move can be linked to the broader implications for altcoins, which had faced pressure under the SEC’s approach to treating certain token sales as securities.

While spot price action gives a mixed picture, realised volatility shows a clearer post-event response.

BTC 30-day realised volatility rose after five of the 8 regulatory developments analysed, with the largest increases following the Strategic Bitcoin Reserve executive order, where volatility rose from 41% to 66%, and China’s crypto transaction ban, where it rose from 65% to 77%.

On 6 March 2025, President Trump signed an executive order establishing the Strategic Bitcoin Reserve and the United States Digital Asset Stockpile. The reserve was capitalised with bitcoin already held by the U.S. government, mainly from criminal and civil forfeiture, and directed that these holdings be treated as a long-term store of value rather than sold. While a U.S. bitcoin reserve had been rumoured, the structure and timing of the order were not fully expected, which likely contributed to the volatility increase.

By contrast, realised volatility fell after Gensler’s departure, from 46% to 43%, and after the GENIUS Act, from 32% to 26%. Both events had been widely anticipated in the run-up to confirmation, suggesting that expected developments may see event premium fade once delivered. Unexpected changes, whether positive or negative for crypto, are more likely to trigger larger price swings.

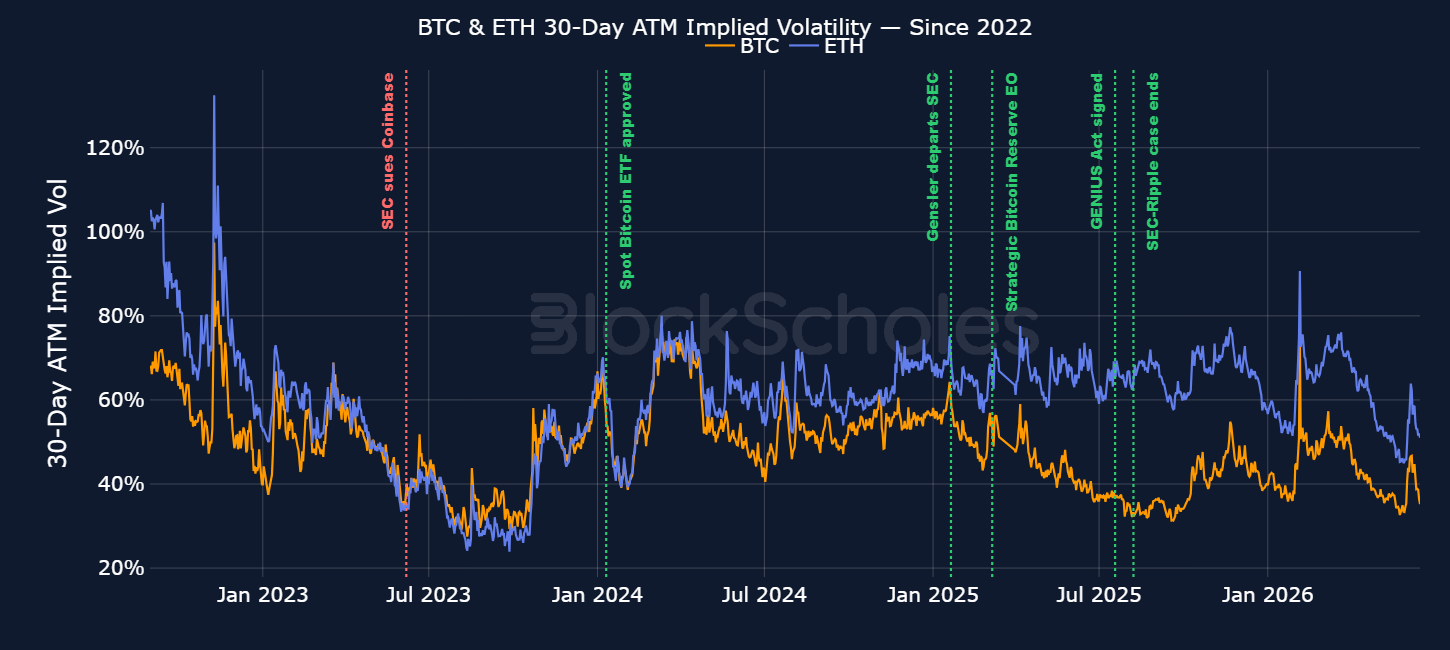

In contrast, BTC 30-day ATM implied volatility fell after five of the six events in the sample, with data beginning in September 2022. Unlike realised volatility, which reflects actual price movement after the event, implied volatility reflects the market’s pricing of expected future volatility through options. A decline after major regulatory developments therefore suggests that, once the event has passed or the outcome is known, traders have less need to pay for optionality to hedge against, or position for, that specific risk.

The only increase followed the Strategic Bitcoin Reserve executive order, when implied volatility rose from 49% to 51%. By contrast, the largest decline followed the spot Bitcoin ETF approval, with implied volatility falling from 57% to 45%, as a highly anticipated milestone was confirmed and event risk was priced out of the options market.

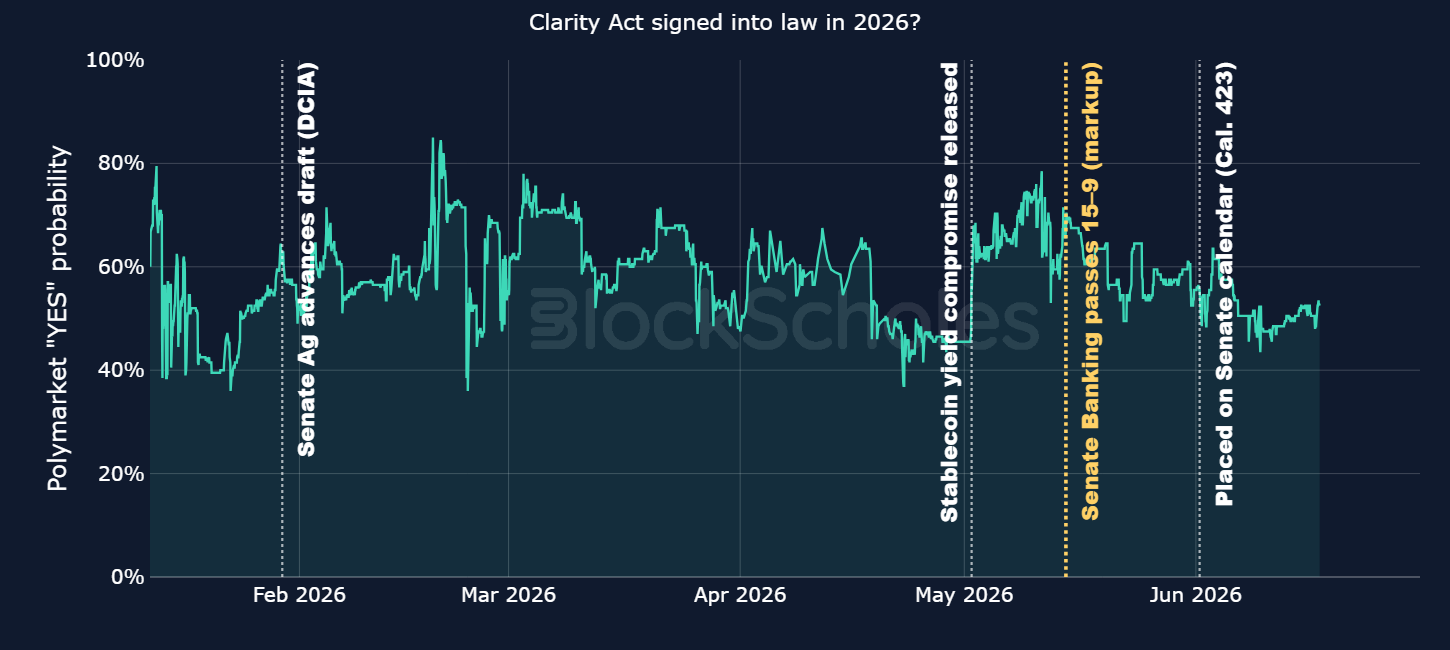

The Digital Asset Market Clarity Act of 2025 remains at the forefront of the U.S. crypto policy agenda. The bill is intended to establish clearer rules for digital asset markets and define the regulatory framework under which crypto activity can develop in the United States.

Senate Banking Committee Chairman Tim Scott described the bill as “the future of finance,” arguing that it lays “the rules of the road” and positions America as “the crypto capital of the world.” His comments reflect the broader political framing around the bill, which presents digital asset market structure as both a financial regulatory issue and a question of U.S. competitiveness.

The bill was introduced on 29 May 2025 and passed the U.S. House of Representatives on 17 July 2025 by a vote of 294–134. The Senate Banking Committee then advanced the bill on 14 May 2026 by a vote of 15–9, before it was placed on the U.S. Senate Legislative Calendar.

Placement on the Senate Legislative Calendar makes the bill eligible to be scheduled for full Senate consideration, but it does not set a floor-vote date – leaving an indefinite time window for progression of the bill. The remaining steps include a full Senate floor vote, reconciliation with the House-passed version, and a presidential signature.

The broader market remains split on the likelihood of this bill progressing in 2026 as shown in The Polymarket market “Clarity Act signed into law in 2026?” The chart below shows the market over its full lifetime, with the dotted vertical lines marking the key legislative milestones listed.

Prediction markets are coming under scrutiny with a dispute over whether these contracts should fall under state gaming laws or federal commodities oversight. Kalshi has been at the centre of this legal battle as individual states have moved to restrict what they view as unlawful gambling activity.

State oversight argues most strongly for sports-based prediction markets, where the underlying event is a sporting outcome, such as whether a team wins, a player scores, or a match finishes with a certain result. In these contracts, the economic exposure is very similar to a bet placed with a sportsbook. For example, buying a contract at $0.60 that pays $1 if a team wins means risking $0.60 to make $0.40, equivalent to taking odds that imply a 60% probability of that outcome. The key difference is in market structure: whereas a sportsbook typically sets the odds and manages its own book, a prediction market is exchange-based, with users trading contracts against each other. However, the end exposure remains a binary cash payoff on a sporting result.

In contrast, the Commodity Futures Trading Commission (CFTC) argues that Kalshi’s event contracts qualify as derivatives under the Commodity Exchange Act, and that federally regulated exchanges should fall under the agency’s exclusive jurisdiction.

Kalshi and the CFTC’s stance is clearest for prediction markets based on existing and tradeable financial assets such as BTC, oil, the S&P 500, gold, and Treasuries, where event contracts do resemble derivatives – in particular cash-or-nothing digital options. These prediction market contracts have option-like characteristics, including non-linear sensitivity to the underlying price, volatility, time to expiry, and the probability distribution around the strike.

Importantly, prediction markets based on financial assets can be used to express or hedge exposure to a specific market outcome. This is especially important in structured products, where different trades are combined to create a specific exposure profile.

Prediction markets fall in the gray area between “betting” and derivative, embodying characteristics of both

Macro and political-event prediction markets sit in a more nuanced category. Contracts on CPI, non-farm payrolls, unemployment, Fed funds decisions, inflation prints, or election outcomes are not direct derivatives on tradable assets, but the events they reference can materially affect bonds, rates, FX, equities, commodities, and crypto markets. However, the hedge is imperfect because the contract pays according to the data or policy outcome itself, not the market reaction to that outcome.

The dispute over sports-based prediction markets falling under statewide sports-gambling rules has continued to expand across states. According to the CFTC, New Mexico joins a growing list of states involved in litigation over whether state gaming laws can be applied to CFTC-registered prediction-market venues, following cases in Arizona, Connecticut, Illinois, New York, Minnesota, Rhode Island, and Wisconsin.

On 12 June 2026, the CFTC filed a federal lawsuit against the state of New Mexico, seeking to block the state from applying its gaming laws to CFTC-registered contract markets. Importantly, the CFTC’s complaint seeks a declaratory judgment confirming the CFTC’s authority over these markets as part of the case.

Former SEC and CFTC Chair Gary Gensler filed an amicus brief, a legal filing by an external party that offers information or arguments to help a court decide a case, to the U.S. Court of Appeals (Sixth Circuit), arguing that the Dodd-Frank Act, which expanded the CFTC’s regulatory powers over swaps and derivatives markets after the 2008 financial crisis, did not give the CFTC authority over sports betting or sports-related prediction markets. His filing challenges the position of both Kalshi and current CFTC leadership, arguing that sports-related contracts are not swaps and are rarely, if ever, used for hedging.

“If Dodd-Frank had preempted the states on sports betting, it would have been one of the biggest stories about Dodd-Frank at the time. But nobody ever mentioned it.”

— Gary Gensler, amicus brief

The SEC has published its Draft Strategic Plan for Public Comment for Fiscal Years 2026–2030, which sets out its priorities in a high-level policy roadmap.

In the draft, the SEC has signaled a shift from treating crypto primarily as an enforcement problem toward building a clearer regulatory framework for digital assets, distributed ledger technology, and on-chain financial infrastructure. It places crypto inside the SEC’s core regulatory-policy agenda and says the agency wants a “rational, coherent, and principled” approach that supports innovation while maintaining investor protection and market integrity.

The crypto element focuses on clarifying where existing securities law applies to digital assets, enabling compliant capital formation through tokenized offerings, and supporting regulated development of on-chain financial infrastructure. It also highlights the need for workable oversight of custody, trading, and staking services, with the aim of avoiding duplicative or conflicting requirements for firms operating across crypto market activities.

The plan also points to closer SEC/CFTC coordination to define jurisdictional boundaries between securities and commodities regulation, which is especially important for the future of spot crypto markets, derivatives, and tokenized assets. Its enforcement language suggests a preference for targeting clear policy rather than relying on ad hoc enforcement to define the rules. Although the intentions behind the draft seem positive, it does not include any enforcement mechanism to ensure these rules are developed.

1) Bitmine Immersion Technologies, the largest public Ethereum treasury company, said its holdings reached 5.62M ETH, equal to 4.66% of the total ETH supply, after acquiring 76,881 ETH over the past week.

The company reported $10.4B in crypto, cash, marketable securities and “moonshot” holdings, including 204 BTC, $502M in cash and marketable securities, a $180M stake in Beast Industries and an $88M stake in Eightco Holdings.

Bitmine said 4.72M ETH, or more than 83% of its ETH holdings, are staked, with projected annualized staking revenues of about $226M, while its 9.50% Series A Perpetual Preferred Stock is expected to begin trading on the NYSE under BMNP on June 16.

2) TON blockchain’s native token, Toncoin ($TON), has been rebranded to $GRAM, with a new name, ticker and logo. The TON blockchain and network remain unchanged.

All TON holdings convert 1:1 to GRAM automatically, with no swap, migration or action required from holders.

3) French bitcoin treasury firm Capital B is preparing to launch a digital credit instrument for European investors, modeled on Strategy’s STRC and Strive’s SATA, announced at a speech at BTC Prague.

The Paris-listed company plans to use its bitcoin treasury as the underlying asset for a yield-focused product designed around Europe’s regulatory and tax environment. Capital B currently holds 3,139 BTC and aims to reach 15,000 BTC by the end of 2027.

Board director Alexandre Laizet said the instrument could target double-digit yields while keeping volatility below double digits, arguing that bitcoin treasury companies can support such products through the long-term appreciation of their BTC holdings.

4) Avalanche Treasury Co., an AVAX-focused treasury company, began trading on Nasdaq under the ticker AVAT on June 11, following the completion of its $675M SPAC merger that was first announced in October 2025. Shares closed down 40% on their first day of trading.

The company plans to deploy capital across the Avalanche ecosystem and has previously outlined ambitions to acquire more than $1B worth of AVAX, while investing in areas including Avalanche validator infrastructure, protocol development and enterprise partnerships.

5) BlackRock has filed a Form 8-A for its proposed iShares Bitcoin Premium Income ETF (BITA), a key regulatory step that typically signals a fund is nearing launch.

The filing follows BlackRock’s recent fourth amendment to the ETF registration, which “typically means launch in one week” according to Bloomberg ETF analyst Eric Balchunas.

The form set a 0.65% sponsor fee and outlined a strategy of generating yield by selling call options primarily against IBIT, the firm’s spot bitcoin ETF. Balchunas added that if he had to bet, “next Thursday BITA goes live.”

6) Citigroup is launching a blockchain-based platform for wealthy and institutional clients to trade tokenised shares of private companies, with the rollout initially limited to foreign investors, according to The Wall Street Journal.

The platform is aimed at giving clients exposure to large private companies, as investor demand builds around names such as SpaceX, Anthropic and other late-stage private firms.

7) A bipartisan group of senior Senate and House lawmakers — Tim Scott, Elizabeth Warren, French Hill and Maxine Waters — has agreed on an updated version of the 21st Century ROAD to Housing Act, giving the legislation bicameral momentum and a clearer path through Congress.

While the bill is primarily focused on housing affordability and supply, it also includes language that would prevent the Federal Reserve from issuing a CBDC, or any substantially similar digital asset, until the end of 2030, reflecting continued political resistance to a U.S. digital dollar.

8) A coalition of national gaming, tribal, state and labor organizations urged the U.S. Senate to include language in crypto market structure legislation that explicitly bans event contracts tied to sports and casino-style gaming.

The groups argued that sports-related prediction markets have expanded gambling nationwide without state or tribal authorisation, allowing some users as young as 18 to place bets and marketing gambling products as “investments.”

9) China’s digital yuan international operation centre, managed by the People’s Bank of China, has signed direct participant agreements with 26 financial institutions in Shanghai to expand cross-border e-CNY payment services.

The agreements allow institutions to join Cross-border e-CNY Transfer Services (CBETS), a settlement platform designed to support round-the-clock digital payment links with foreign central banks and overseas financial institutions.

10) LG Electronics, the South Korean consumer electronics giant, revealed plans on June 11 to launch a blockchain-based advertising network built with Arbitrum.

The platform is designed to place and track digital advertisements onchain through a shared database of ad inventory and user interactions, allowing advertisers and publishers to buy, sell and monitor ad placements using the same transparent record of campaign performance and user engagement.

11) MNX, a decentralised futures exchange being built on MegaETH, raised $6.4M in a pre-seed round at a $40M valuation to develop trading markets focused on the AI economy, including AI company valuations, compute infrastructure, and prediction markets.

The platform plans to launch on mainnet later this summer and will use MegaETH’s low-latency infrastructure, while targeting traders seeking exposure to prediction markets on AI model benchmarks, product launches, company performance and geopolitical developments alongside futures and perpetual contracts designed for AI-related assets.

12) Figure Technology Solutions, a blockchain-based capital markets platform, has agreed to acquire real estate lending platform Kiavi in a $717M transaction, with a joint venture between Figure and Sixth Street purchasing Kiavi’s balance sheet assets.

The deal is expected to add more than $7B in annual first-lien loan volume to Figure’s marketplace and bring residential transition loans and rental-property lending products onto its tokenised infrastructure, which the company says represents a roughly $200B annual addressable origination opportunity.

Fluence Energy, Inc. (Nasdaq: FLNC) is a publicly listed energy storage and grid technology company.

The company provides large-scale battery energy storage systems, software, and related services for utilities, renewable energy developers, independent power producers, and large electricity users.

In simple terms, Fluence helps electricity grids store power, manage renewable generation, and improve reliability as the energy system becomes more dependent on intermittent sources such as solar and wind.

Fluence was created in 2018 as a joint venture between Siemens and AES, two major global energy and infrastructure companies. That background is important because grid-scale storage is not just a technology product; it is a complex infrastructure business involving project delivery, safety, warranties, grid integration, and long-term operational performance.

Fluence benefits from having roots in two companies with deep experience in power systems and utility-scale energy projects.

The company’s core business is utility-scale battery energy storage.

Its systems are designed to absorb electricity when supply is high or prices are low, then release that electricity when demand rises, renewable generation drops, or the grid needs support.

This makes storage increasingly important as power markets add more renewables and face higher volatility in supply and demand. Fluence’s products are used for applications such as renewable energy integration, grid stability, peak demand management, capacity support, and energy trading.

Fluence is not only a hardware supplier. One of its more distinctive features is that it combines battery storage systems, operational services, and software. Its software platforms help asset owners optimize how batteries and renewable assets operate in power markets, while its services business supports projects after installation. This matters because the economics of battery storage depend not only on the physical asset, but also on how effectively it is operated, maintained, and monetised over time.

A key part of Fluence’s positioning is that it sits at the intersection of several major energy themes: renewables growth, grid reliability, electrification, and rising power demand from data centres and AI infrastructure. As electricity systems become more strained, storage is becoming a critical tool for balancing the grid.

Fluence is therefore exposed to a structural growth market rather than a short-term energy trend.

The company’s unique details are its:

There are relatively few public companies that give investors direct exposure to utility-scale battery storage as a core business.

That makes FLNC notable for investors, partners, and customers looking at the energy transition and the infrastructure required to support it.

The importance of Fluence is that battery storage is becoming essential infrastructure. Renewable power cannot scale efficiently without storage, because solar and wind output do not always match electricity demand. Storage helps bridge that gap, improves grid resilience, and can reduce reliance on fossil-fuel peaker plants.

.jpg)

.jpg)