Thahbib Rahman

Research Analyst

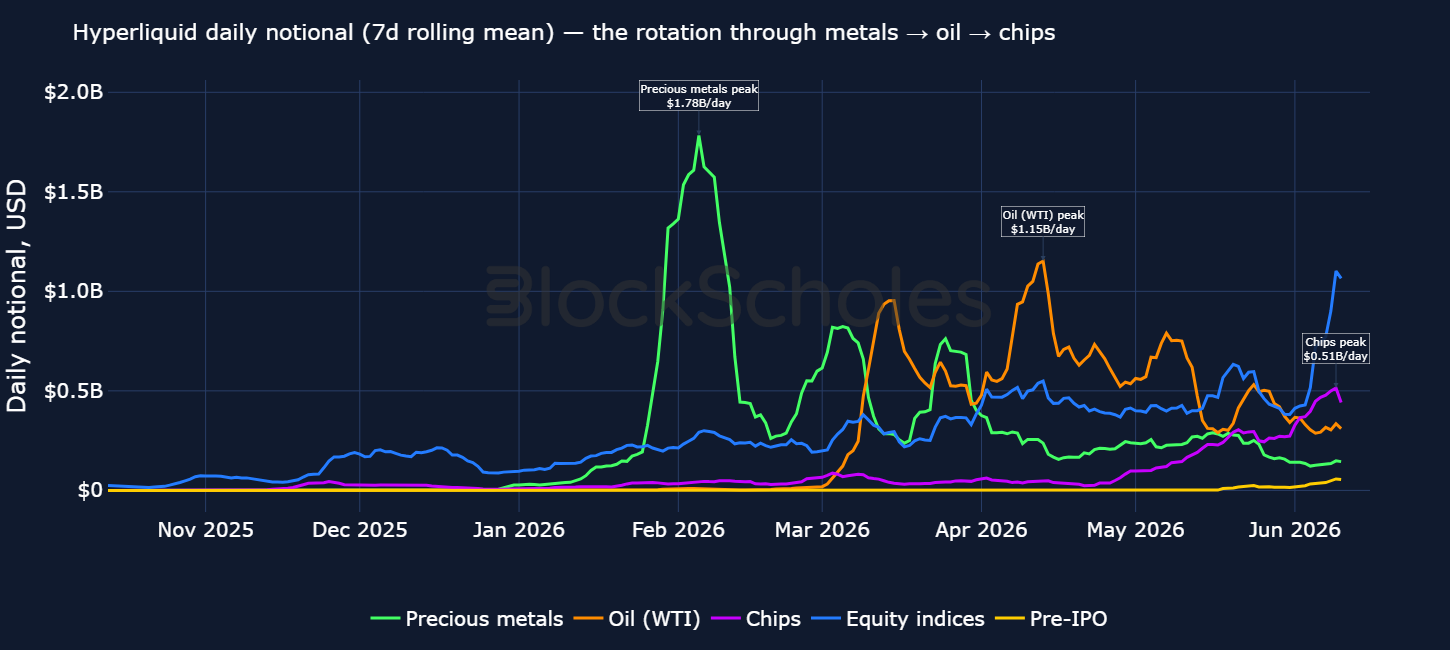

Over the past eight months, a striking pattern has played out on Hyperliquid — the largest onchain venue for price discovery outside of traditional market traded hours: capital and attention has shifted through a sequence of macro themes that have stolen retail attention share from crypto-assets. The movement of capital and attention first began with precious metals in early 2026. Average rolling 7-day notional volume on Trade.xyz’s gold and silver perp contracts peaked at $1.78B/day in early February — coinciding with the late-January precious metals blow-off top and subsequent spot price crash.

Over the past eight months, a striking pattern has played out on Hyperliquid — the largest onchain venue for price discovery outside of traditional market traded hours: capital and attention has shifted through a sequence of macro themes that have stolen retail attention share from crypto-assets.

The movement of capital and attention first began with precious metals in early 2026. Average rolling 7-day notional volume on Trade.xyz’s gold and silver perp contracts peaked at $1.78B/day in early February — coinciding with the late-January precious metals blow-off top and subsequent spot price crash.

Not long later, the onset of the US-Iran conflict in late February saw traders rotate into oil contracts (with the predominant market on Hyperliquid being xyz's WTIOIL-USDC perp). On April 13, 2026, the rolling 7-day mean of notional volume reached a top of $1.15B. Most recently, with US equities and major US tech stocks outperforming crypto markets, attention has now shifted towards chip stocks, as well as the pre-IPO market.

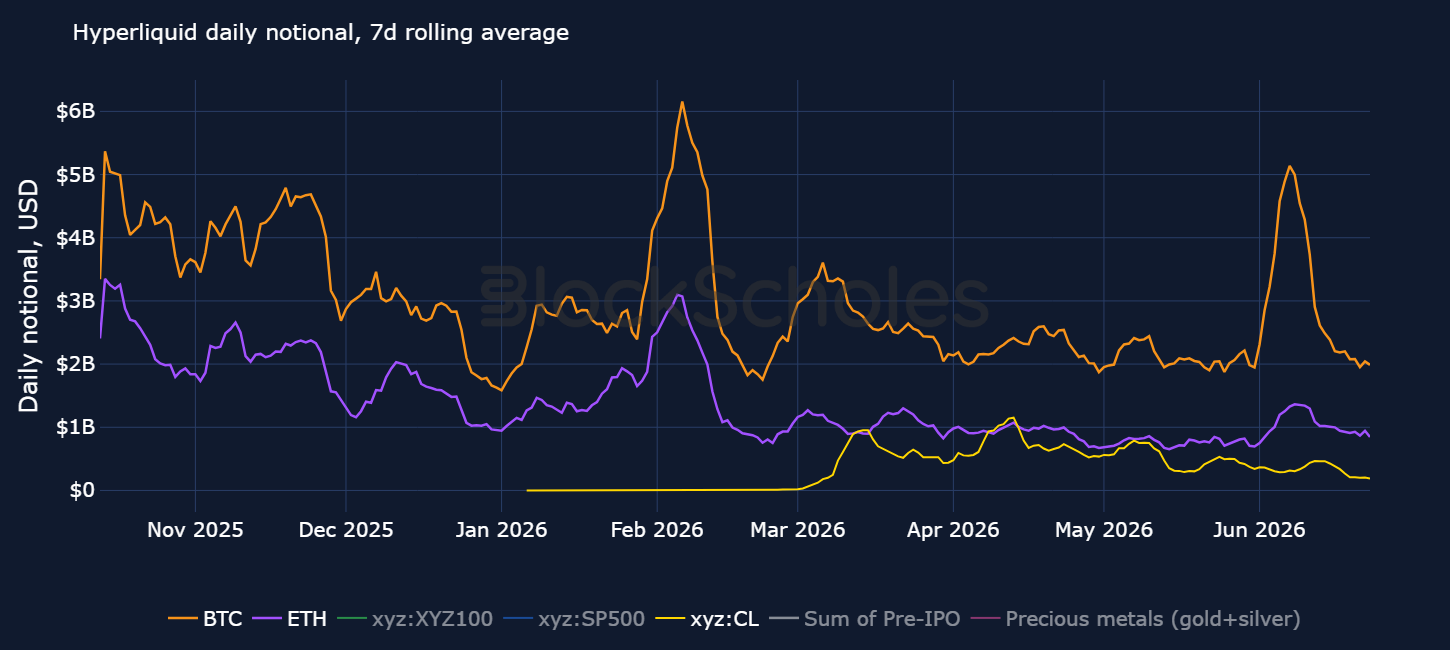

Each sector-specific wave has shown partial evidence of drawing leveraged capital away from crypto's core. For example, between February and April 2026, BTC and ETH perp volume fell more than 50% from their respective highs of $6B and $3B while volumes in xyz’s WTI oil perp rose from negligible levels to more than $1B.

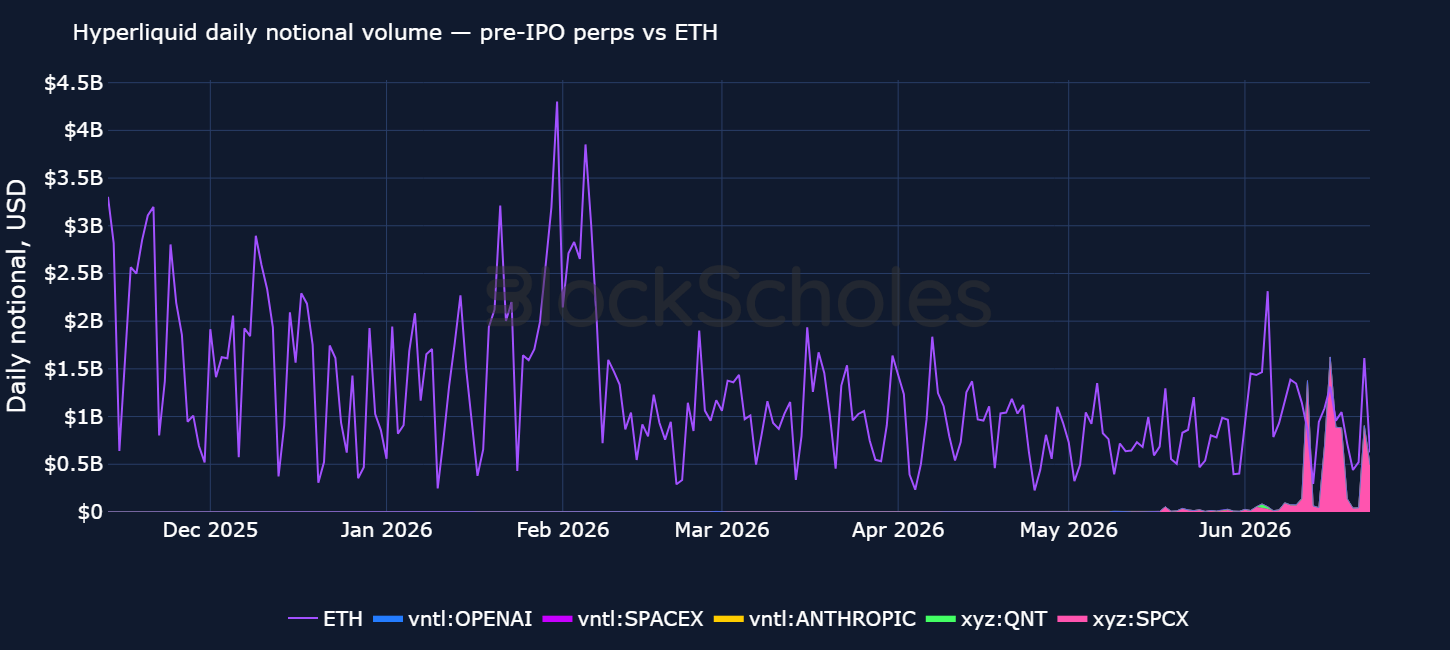

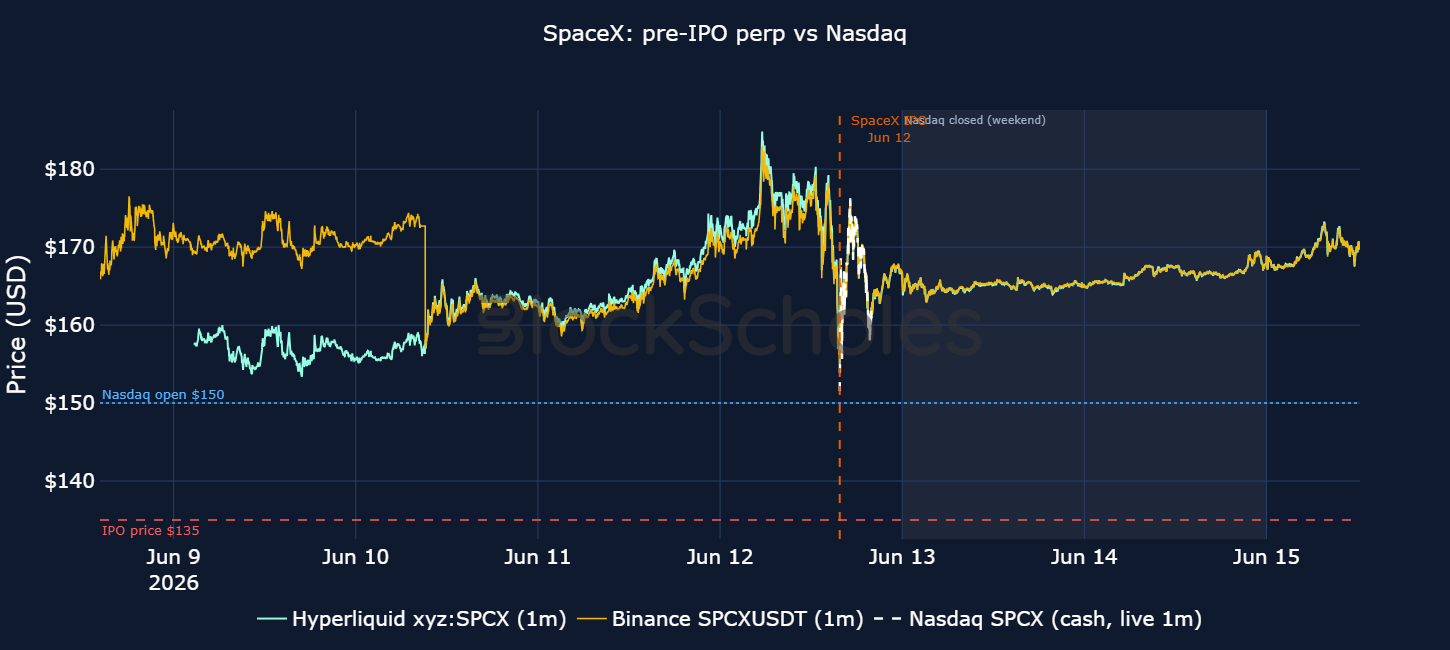

The newest (and ongoing) phase of that attention rotation has been rooted in pre-IPO perpetual futures contracts. On June 12, 2026, SpaceX had its public Nasdaq debut and Hyperliquid pre-IPO perps recorded $1.392B in notional volume. 98.5% of that ($1.371B) was driven by xyz’s SPCX perp contract alone, which recorded almost double the $861M daily ETH volume.

Some of the most valuable private companies in the world have recently filed for or (in the case of SpaceX) completed an IPO. Historically, before a company would go public, only employees or accredited investors early on in the lifecycle of those firms would have the opportunity to get economic exposure to these companies.

However, two on-chain tokenisation mechanisms have tried to solve this access issue, allowing anyone to trade pre-IPO firms:

Perpetual futures (perps) are cash-settled derivatives contracts that let a trader bet on an asset's price without owning the underlying asset itself. For a pre-IPO company in particular, these contracts can be appealing: shares of the private company cannot be bought or sold short easily, so a cash-settled perp provides an alternative way to take a position on the value of the company — long or short, with leverage, 24/7, and with no shares to custody/ claim on shares.

The price of a perp is set by ordinary supply and demand, i.e., buyers lift the perp price up, and sellers push it down. However, as the name suggests, without an expiry there is no mechanistic convergence to the underlying index promised by settlement. Instead, perps solve this with funding rates — a recurring payment, made every funding interval (hourly on Hyperliquid, every eight hours on Binance), exchanged directly between longs and shorts.

Funding rates ensure a normal perp’s price is aligned with its underlying index price by comparing the tradeable price to the oracle:

For a standard listed-equity perp, the index price is simply the real, external price of the stock, aggregated from the outside venues and exchanges where it trades. Funding therefore continuously ties the perp to the genuine external market price. When that external feed is briefly unavailable — over a weekend when the market is shut for example — the oracle falls back on an internal mechanism until traditional market trading resumes.

Pre-IPO perps rely on that internal mechanism throughout. There is no continuous external price on an outside venue to peg the pre-IPO market to. Hence the protocol builds the index price out of the only information it has: the perp's own order book. In this case, the index price is a lagged version of the market price — a function of itself.

Therefore, the price of a pre-IPO perp is just the market's collective estimate of the price of the underlying. Once the company officially lists, all positions held in the pre-IPO perp are converted into the subsequent equity perp that inherits those positions. Since funding rates on that equity perp will then be calculated relative to the live public stock price, pre-IPO prices are expected to converge toward the underlying share price which is now known. This is because at this point, a real external price now exists — the stock is trading on the Nasdaq, for example. Both Hyperliquid and Binance then switch the oracle from the internal, book-derived value to that external price.

The natural question that follows then is: how close were these pre-IPO market estimates, once a first traded price was recorded on the external off-chain exchanges?

Three high-profile companies have listed in the past two months, giving us a number of case studies to explore: Cerebras (CBRS), the AI wafer-scale chipmaker; Quantinuum (QNT), the quantum-computing firm; and SpaceX (SPCX), Elon Musk’s spaceflight and telecommunications company.

Each traded as a pre-IPO perp on Hyperliquid and (in two of three cases) on Binance, which is typically the deeper venue (on SpaceX's listing day, 12 June, Binance handled $5.85B of SPCX perp volume to Hyperliquid's $1.37B).

Focusing only on the minutes around the official Nasdaq price of each listing and the perps showcase a strong degree of accuracy. Using SpaceX as an example, underwriters set the IPO price at $135, while the IPO cross price, when market makers and the exchange (in this case the Nasdaq) determine the first-traded price, was $150 at 15:46 UTC June 12. In the final minute before the cross the Hyperliquid perp was trading at $158.88 and the Binance perp at $158.25 — within $0.63 of each other and ~6% above the open.

However, that narrow view overstates the quality of the price discovery on pre-IPO contracts. A newly listed stock doesn't begin trading at the opening bell. As that orderbook fills pre-IPO cross, the stock’s indicative price and order imbalance are published and widely reported, so by the final minute the cross price is effectively public. A perp matching this is not exactly estimating price in advance as the information is already available.

Note: Underwriters determine the IPO price, the price at which shares are allocated to chosen investors. This is often set lower than fair value/ market value to incentivise buyers and an industry-standard built-in clause often requires underwriters to hold unsold stock. The cross is a separate, market-set open price on an exchange.

Underwriters gauge investor demand through a process known as book-building. This involves investors submitting "indications of interest," outlining how many shares they are willing to buy at what prices. This is then compiled by the underwriter into an order book; if there is high demand, underwriters may raise the price range; if demand is weak, they will lower it to entice buyers.

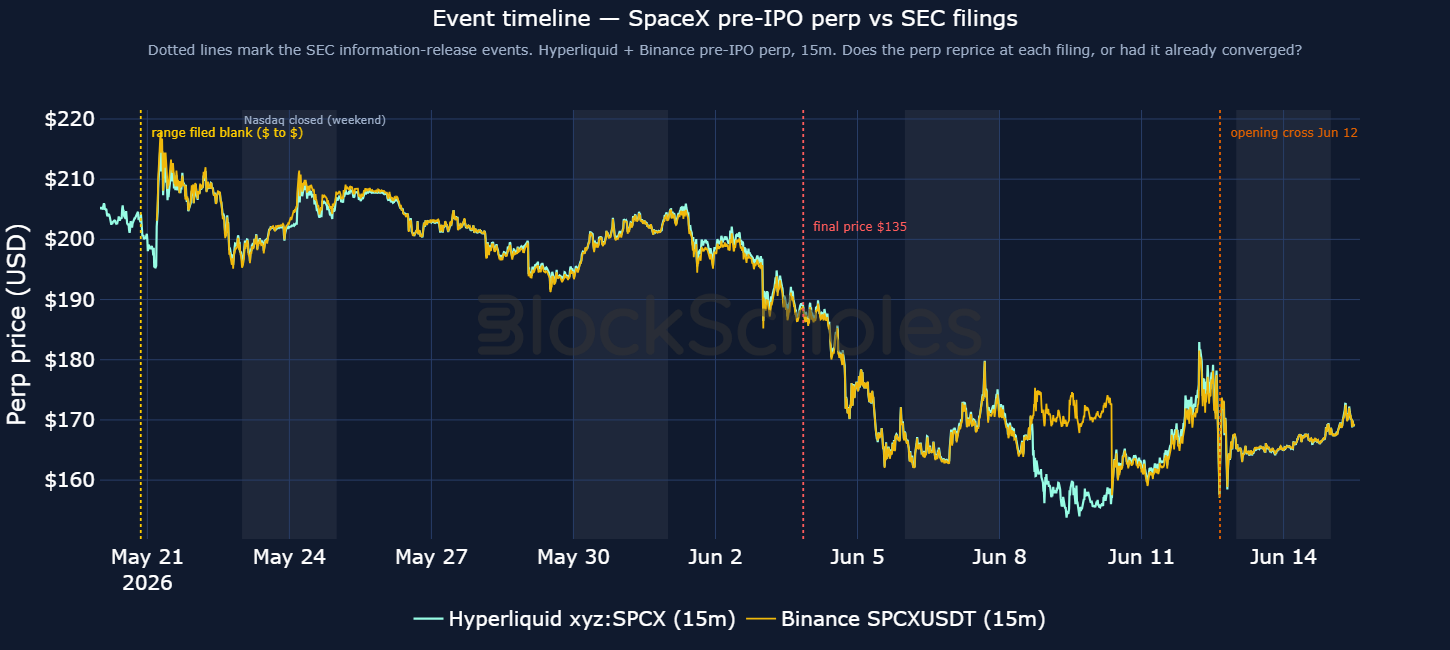

Therefore, if we zoom out, we can see how the perps traded before this information was available. The clearest way to see this is to mark the dates on which the underwriters filed their expected price with the SEC. If the perp market had genuinely priced-in the opening level, traders would have repriced the perp within a close range to the open-price. Instead, we find evidence that the pre-IPO perps did not accurately reflect the eventual Nasdaq open price in the days leading up to the open.

From its first trade (17 May) the SPCX perp on Hyperliquid and Binance traded between $190–215 for two weeks. On 3 June underwriters filed with the SEC a take-it-or-leave fixed $135 IPO price (after leaving the price blank in its initial filing). Following that initial offering price of $135, the SPCX perp fell towards the mid-$100s over the following days. The perp eventually settled around mid-$160s and traded at $157.59 one minute before the NASDAQ IPO cross price which printed $150 a minute later.

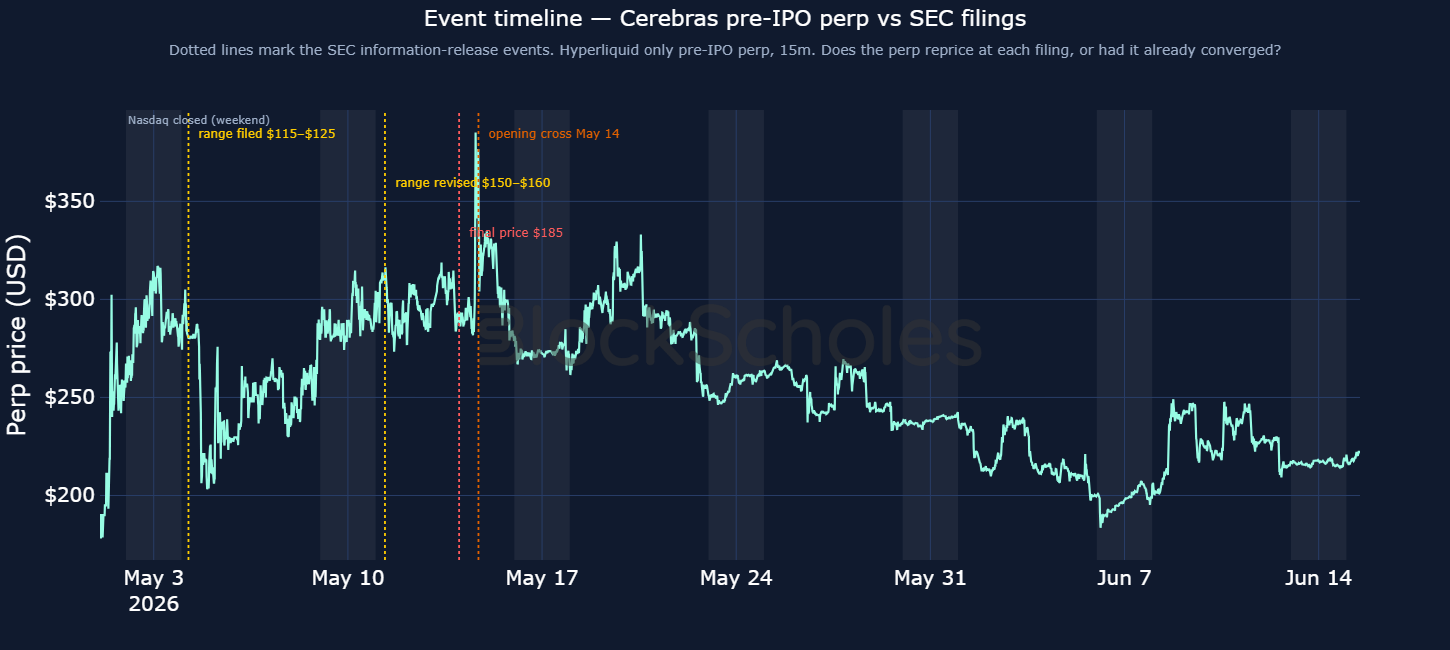

CBRS’s perp behaved similarly. Prior to any SEC filings, the perp traded around $280–310 until 4 May, coinciding with the underwriter’s initial filing of a $115-125 IPO price range, when it drifted lower to $200. The perp price slowly recovered back to $300, until the 11 May amendment filing which lifted the IPO price range to $150–160 and pushed the perp price slightly lower.

Across the entire pre-listing window and three SEC filings, the perp never reached $350 — the eventual Nasdaq open price — in the days leading to the IPO; instead it traded within a lower $200–300 price band.

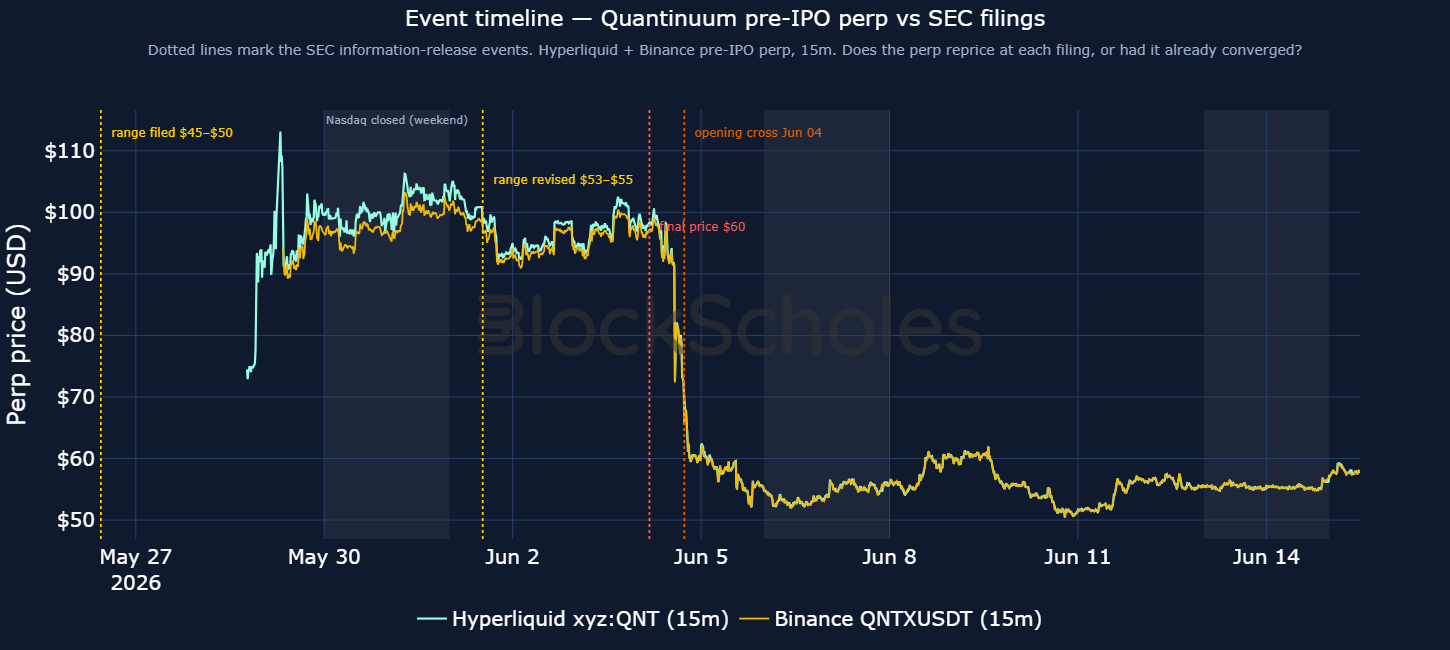

QNT-USDC was not listed on Hyperliquid at the time of Quantinuum’s first S-1 filing. Underwriters, however, noted high demand and requested a second filing, with an upwards revision in the IPO price from the $45-50 range to $53-55. A final IPO price of $60 per share was sent by underwriters to the SEC on June 3, 2026, a day before the IPO. Unlike CBRS, where the perp price always traded below the eventual Nasdaq cross, Hyperliquid and Binance QNT perps were less accurate for a different reason: the QNT perp consistently traded between $90-100 in the days leading up to the IPO — above the eventual $68 Nasdaq cross price.

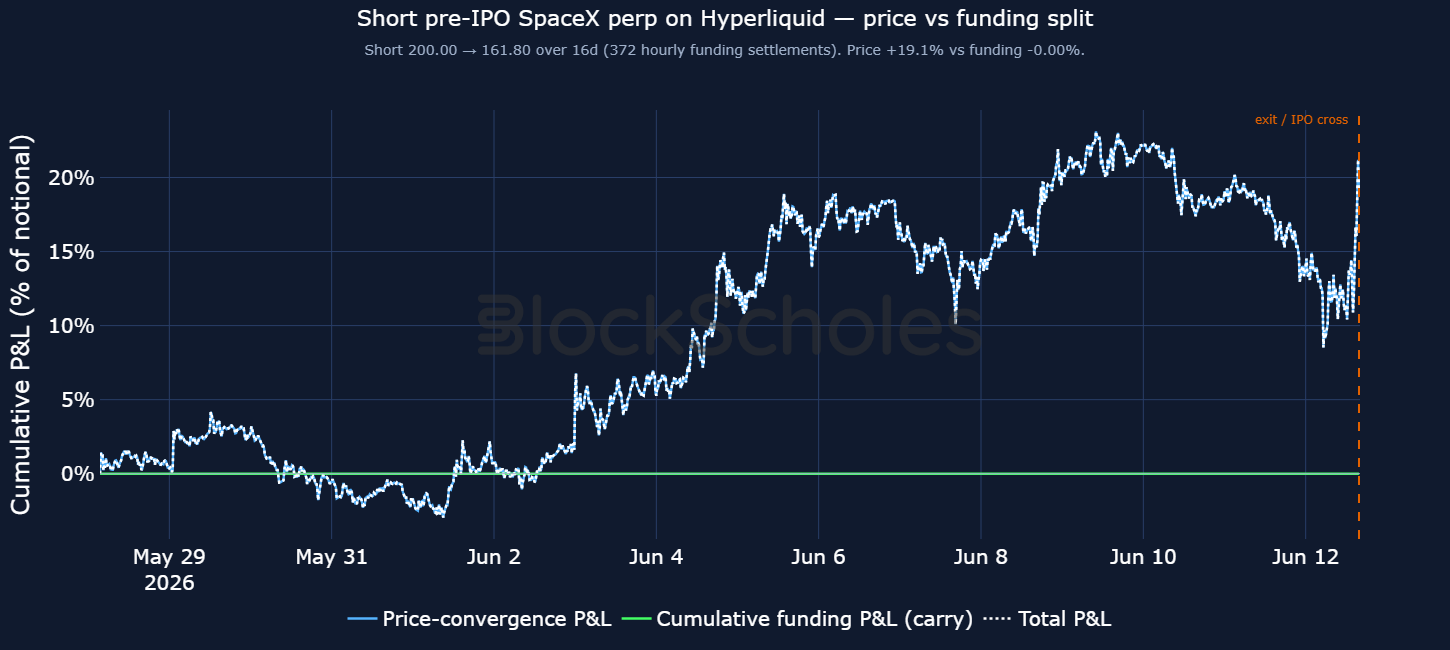

Given that two of the three mentioned perps (SPCX) and (QNT) largely traded above the Nasdaq IPO cross price for much of the pre-IPO period, how would a trader who judged that the perp price was potentially overblown, relative to the open price, have fared? What exposure to the underlying would their position have actually taken, and did funding rates mean they were paying to hold the position or being paid?

On a conventional perp, a persistently large funding can be interpreted as a signal of whether market positioning is crowded, i.e., high positive funding rates are a bullish sign that long traders are willing to pay a fee to shorts to stay long.

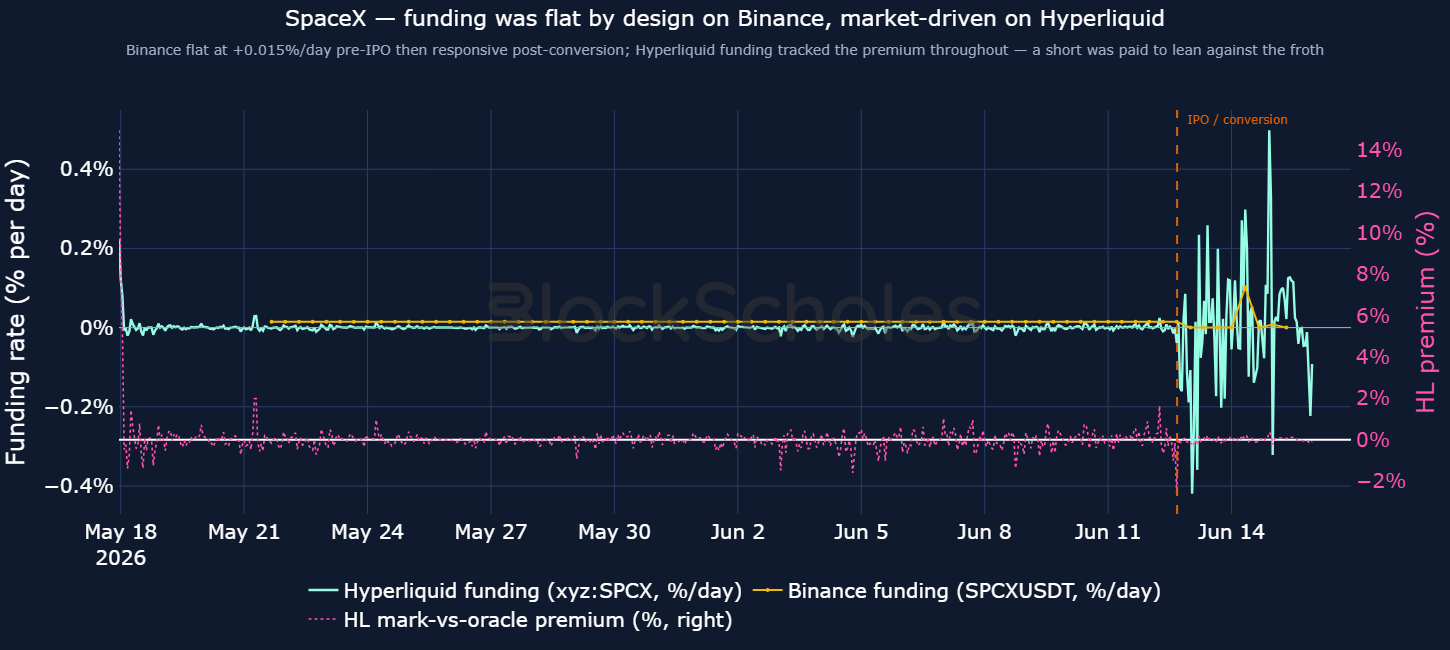

Funding on pre-IPO perps is slightly different. As mentioned in section 2, given the lack of a continuously traded external price, the index price that the perp is aligned with is built from the perp’s own order book. As such, the funding rate is just nudging the perp price towards an oracle price derived from itself, hence is deliberately suppressed or even fixed across venues:

The self-referencing peg only changes once the company lists; then both venues switch the index price definition from the internal, book-derived value to the live external price, and the contract converts into an ordinary equity perp. As an example, for SpaceX, that switch came on Binance at 16:15 UTC on 12 June, roughly half an hour after the stock had opened at $150 on the Nasdaq.

Taking SPCX as an example, a short position at $200 (close to the peak on-chain price) would have netted close to 20% profit for a trader, with very little paid in the way of funding payments. We see that below as funding predominantly stayed flat around 0% for most of the pre-IPO period.

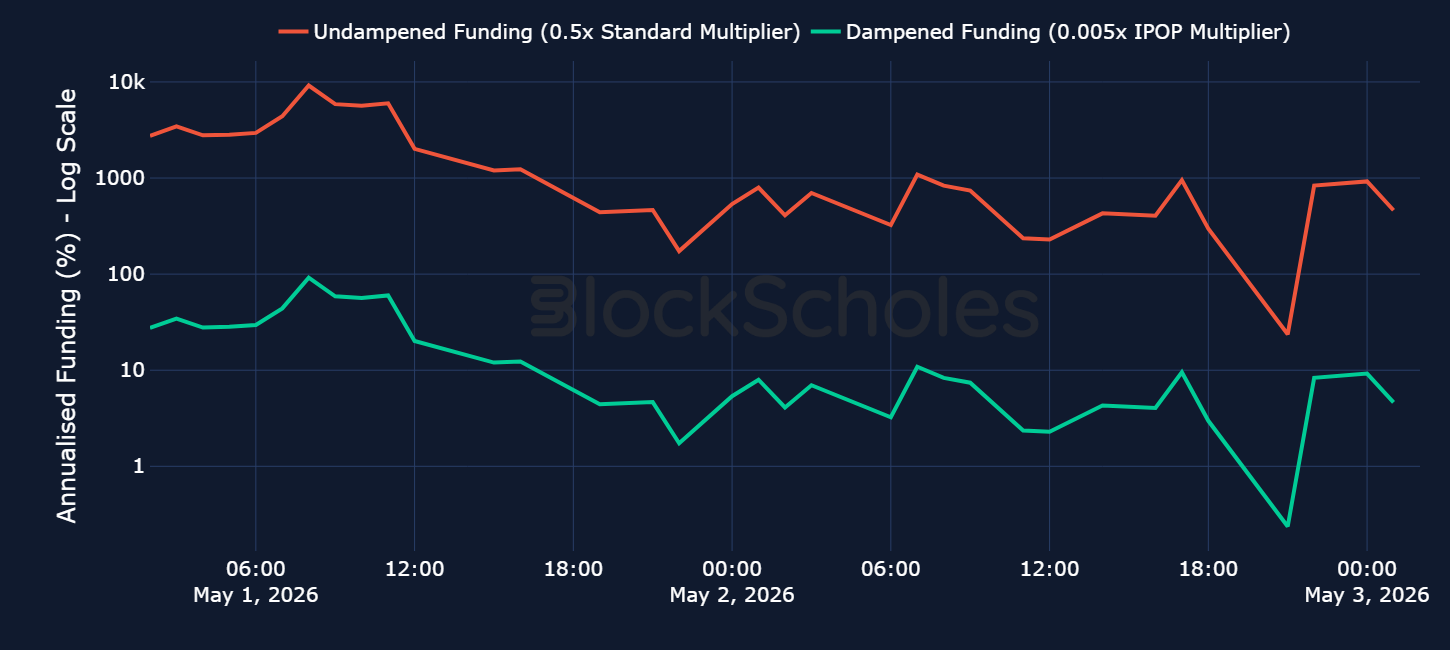

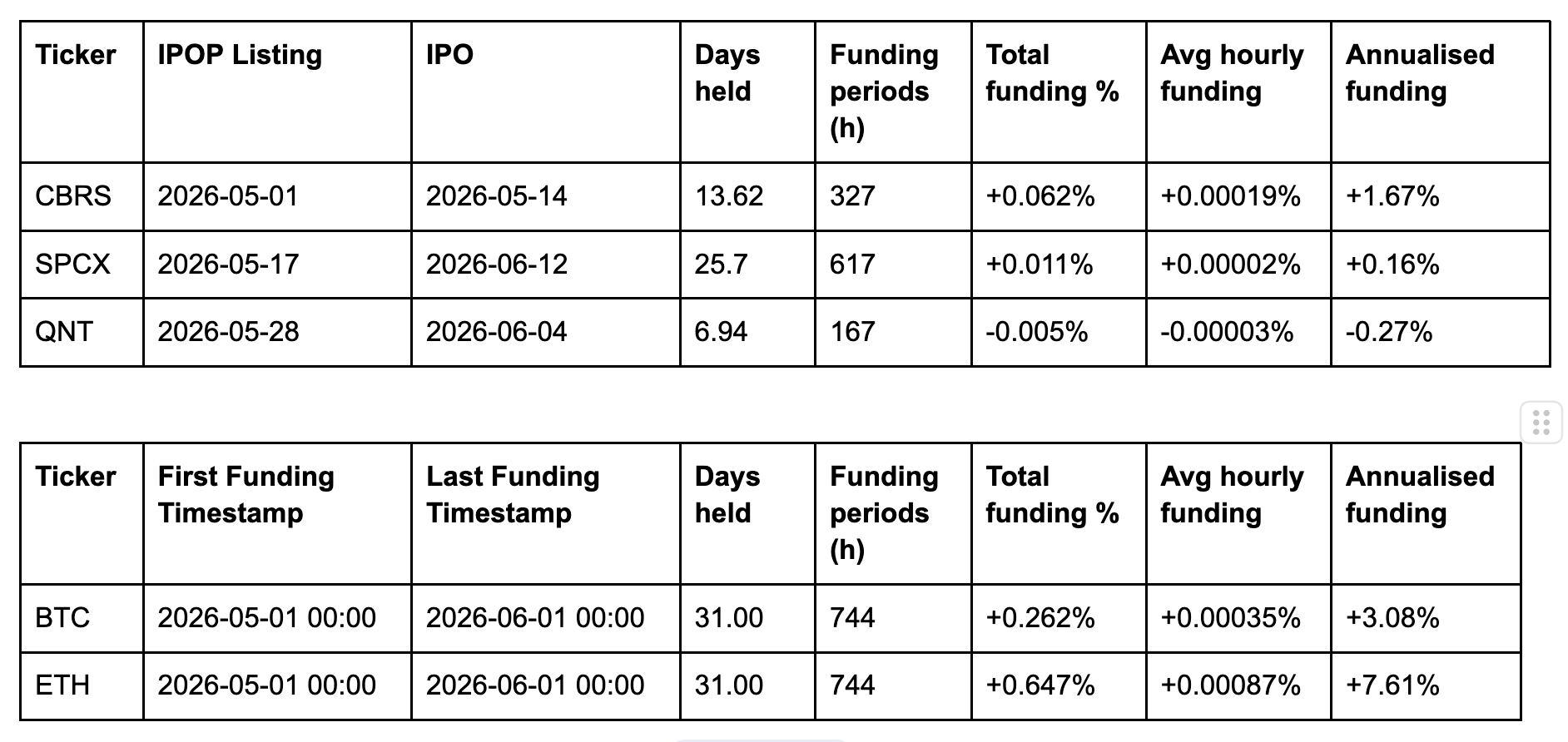

Despite the 0.005x multiplier designed to dampen funding rates on pre-IPO market positions, one exception among the three perps was Cerebras. CBRS exhibited relatively high positive funding rates during the first day of its Hyperliquid listing, causing annualised funding to exhibit numbers comparable to majors, averaged over a similar period of time:

This was due to a divergence between mark price and a lagging internal oracle, causing a consistent premium so large that funding rates spiked to 0.0105% at its peak. Had TradeXYZ not enforced the dampening rule, an un-dampened formula would have resulted in a funding of over 1.05% per hour.