Thahbib Rahman

Research Analyst

On June 25, 2025, the Federal Reserve and the Office of the Comptroller of the Currency (OCC) unveiled a plan to change a key banking capital rule known as the enhanced supplementary leverage ratio, or eSLR on G-SIB banks and their subsidiaries. In this note, we aim to answer what exactly might an SLR revision mean for Bitcoin?

On June 25, 2025, the Federal Reserve and the Office of the Comptroller of the Currency (OCC) unveiled a plan to change a key banking capital rule known as the enhanced supplementary leverage ratio, or eSLR on G-SIB banks and their subsidiaries.

The supplementary leverage ratio (SLR) was initially implemented following the 2008 financial crisis. The ratio determines how much capital a bank must hold in relation to its total leverage exposure, which includes exposure to US treasuries. It is calculated by dividing a bank’s tier-1 capital (numerator) by its total assets, or total leverage exposure (denominator).

Most banks in the US must have a minimum ratio of 3%, while the 8 largest US banks (G-SIBs – Global Systemically Important Banks) are subject to an enhanced SLR (the eSLR) which includes an extra 2% buffer – bringing the total minimum ratio to 5%. Further, subsidiary institutions that are owned by US GSIBs are subject to the standard 3% plus a slightly higher 3% buffer, for a combined 6% total requirement. According to the Federal Reserve Bank of Boston, the SLR is a measure of a bank’s ability to absorb losses in a period of financial stress, and helps to “protect the stability of the banking system by preventing excessive leverage”.

Tier-1 capital is made up of common equity capital (CET1) and additional tier capital (AT1). This includes the total value of common equity, retained earnings, and other related surplus/ disclosed reserves a bank may have – in other words, it represents the core capital a bank owns and uses to fund its day-to-day operations. The denominator comprises all on-balance-sheet assets, including US treasuries, deposits at the Federal Reserve, real estate, and loans, as well as specific off-balance sheet items, such as derivative exposures.

Crucially, the SLR does not distinguish between assets based on risk and treats all exposures of a bank equally. For this reason, a bank that holds a large amount of US treasuries, and therefore has a large denominator, is required to hold more capital to back that exposure, even though a large portion of its ‘exposure’ is in US treasuries – the general benchmark for the risk-free rate.

Why does this matter? President Trump’s administration has not been shy in its desire to lower treasury yields in the US, in particular the 10-year treasury yield – we mentioned that here. Treasuries are ultimately a crucial component of the global financial system and one of the primary means of financing for the US government – a government which has ~$11T due to be refinanced over the next 12 months. Separately, financial regulators including the Federal Reserve aim to ensure the treasuries market is as liquid as possible: Chair Powell said back in February 2025 that he had been “somewhat concerned about the levels of liquidity in the Treasury market” for a long time.

In this note, we aim to answer what exactly might an SLR revision mean for Bitcoin?

The Fed has published a notice of proposed rulemaking (NPR) where it outlines its main policy proposal which is to “set the eSLR standard for GSIBs to half of their method 1 surcharge, instead of the two percent buffer” that currently exists. Additionally, “the proposal would set the eSLR buffer standard to half of the method 1 surcharge of their parent holding companies”. So what exactly does that mean?

GSIBs are subject to a separate risk-based capital surcharge. To identify whether a bank is eligible as a GSIB and in turn their GSIB surcharge, they are assessed on 5 systemic factors:

The bank must calculate a ‘score’ for each of the mentioned indicators, relative to an aggregate global measure. That is then weighted and multiplied by 10,000 (to get the value in terms of basis points) and summed across all indicators to determine a ‘method 1 score’. A bank with a score above 130bps is considered a GSIB and, depending on their bps score, they may be subject to a method 1 surcharge which ranges from “1.0 to 2.5 percent”. Readers are directed to find more details here, and an example calculation here.

Based on this dynamic GSIB method 1 calculation, the proposal means that “the enhanced supplementary leverage ratio standard would range from 3.5 percent to 4.25 percent depending on a banking organization’s risk profile”. That would apply for a GSIB holding company and also its subsidiary bank. For example, JPMorgan Chase & Co is the former, and JPMorgan Chase Bank is the latter. Therefore, non-GSIB banks and non-GSIB subsidiary banks are still subject to a minimum 3% SLR (as the proposed change is focused on the eSLR, not the SLR).

The NPR also consists of four other policy alternatives, though it is the main proposal explained above which Fed members have voted for already. Nonetheless, the alternatives are as follows:

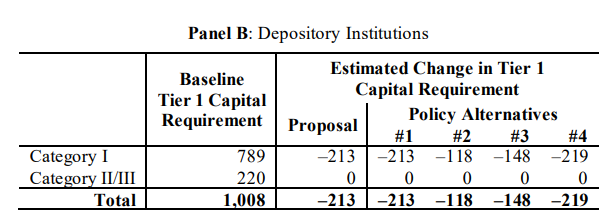

What impact will the change to the eSLR have on US banks? According to the Federal Reserve, “the aggregate reduction in tier 1 capital requirement would be $13B for GSIBs”, or 1.4% of their baseline tier 1 capital requirement, and “$213B for their major depository institution subsidiaries”, or equivalently "about 27 percent aggregate reduction”.

Additionally, that ‘freed’ capital would then have a “level effect” that would “enable these banking organizations to substantially increase low-risk asset holdings without raising their tier 1 capital requirements” – low risk-assets such as US treasury bills and bonds. The proposal would also “reduce disincentives for these banking organizations to engage in low-risk activities, such as U.S. Treasury market intermediation”. The level effect will also manifest itself into another benefit: “banking organizations could add certain lowrisk assets to their balance sheets without increasing their tier 1 capital requirements”.

Indeed, Treasury Secretary Scott Bessent referred to the SLR as “a capital charge to banks for buying treasury bills”, and proposed that if US treasuries were removed from the SLR calculation “we might actually pull treasury bill yields down by 30 to 70bps” – that estimate likely stems from US banks using the $200B plus ‘freed capital’ to buy US treasuries, pushing yields lower. He then added “Every basis point is a billion dollars a year”, in reference to the fact that the US government could save $1B of interest on its debt per year (recall the $11T due to be refinanced). In a separate interview Bessent said “I have seen estimates that it could bring yields down by tens of basis points”.

As stated in the previous section, while the current proposal is not to remove treasuries from the SLR calculation, it is outlined as one “reasonable alternative” in the document. Secondly, according to the report, the “proposed recalibration of the eSLR standards would help mitigate potential disincentives for GSIBs and their depository institution subsidiaries from holding low-risk assets in general”.

We noted that the aggregate reduction in tier 1 capital for subsidiaries of GSIBs is estimated to be $213B. The Fed notes that the ‘freed’ capital will have a “level effect” that would “enable these banking organizations to substantially increase low-risk asset holdings without raising their tier 1 capital requirements” – low risk-assets such as US treasury bills and bonds. The proposal would also “reduce disincentives for these banking organizations to engage in low-risk activities, such as U.S. Treasury market intermediation”. The level effect will also manifest itself into another benefit: “banking organizations could add certain lowrisk assets to their balance sheets without increasing their tier 1 capital requirements”.

The Fed even attempts to quantify the “available capacity of GSIBs to increase reserves or U.S. Treasury securities held as investment securities at their depository institution subsidiaries" should the change be implemented (though acknowledges it does not have the information for a completely precise estimate). Available capacity is defined as the “dollar amount” of low-risk assets that banks “could add to their balance sheets without raising their or their consolidated holding company’s tier 1 capital requirements above baseline levels”. Their estimate?

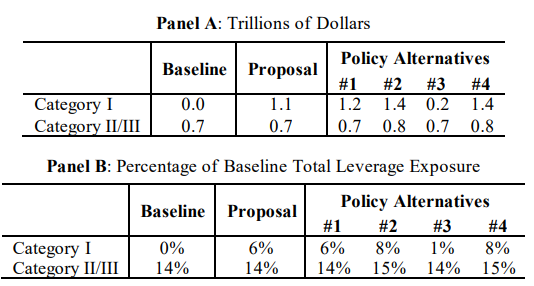

“Under the proposal, the agencies estimate that GSIBs’ available capacity for such assets would increase from nearly zero to $1.1 trillion, in aggregate, which is about 6 percent of their aggregate total leverage exposures”

That is to say, according to the Fed, the $213B of tier-1 capital reduction may potentially support an extra $1.1T in US treasury holdings by GSIB banks before the banks reach their risk-based tier 1 capital requirement limit. That dry powder would mean a significant marginal buyer for US treasuries that could help bring down government borrowing costs – potentially by the “30 to 70bps” predicted by Scott Bessent. This wouldn’t be the first move towards finding new buyers for US treasuries in the vein of lower interest rates by the Trump administration either.

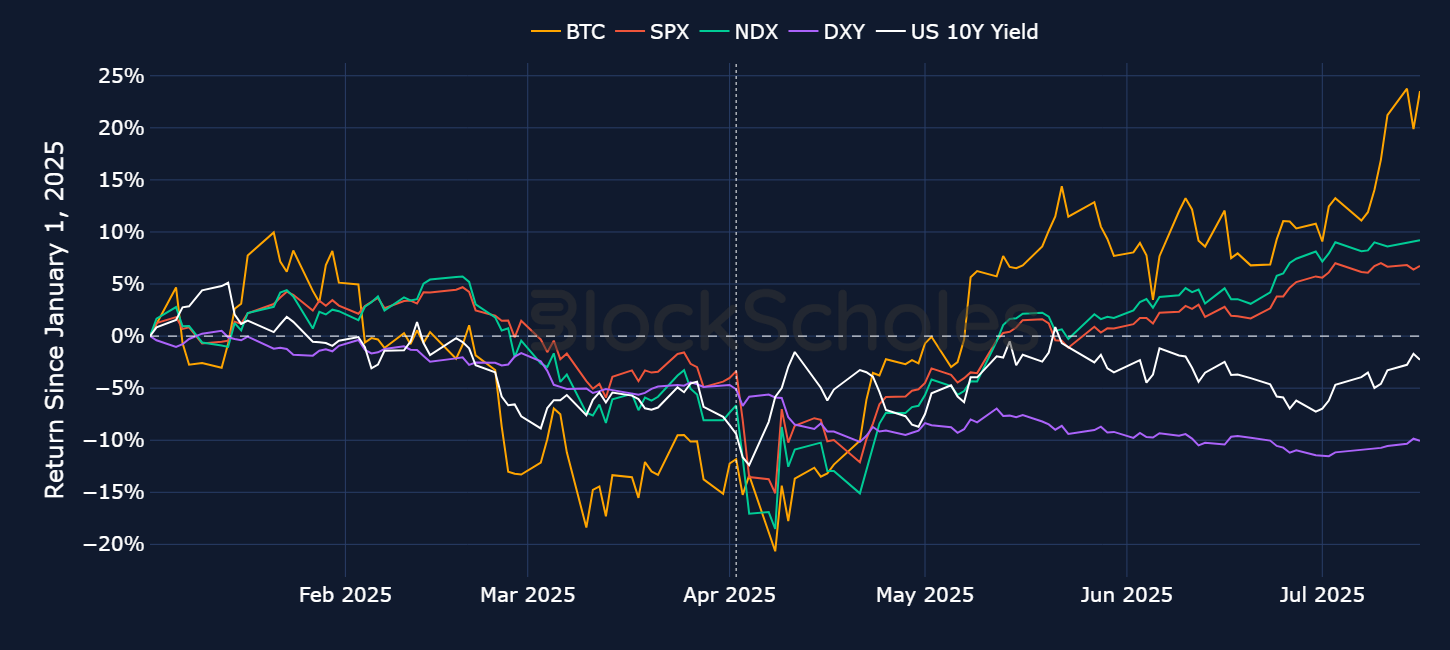

Lower treasury yields can lure investors away from ‘safer’ assets since they return a lower yield, and instead push investors further up along the risk curve. That can result in a shift of capital towards riskier equities, such as US stocks, as well as cryptocurrencies, such as Bitcoin. Both the S&P 500 and Nasdaq-100 recently touched new all-time highs – that has occurred while BTC’s correlation with those assets remains close to historically high levels too (currently above 0.5). Not long after, BTC also rallied to new all-time highs of $123K – while that rally was not just due to its correlation with macro risk-on sentiment and due to other idiosyncratic drivers unique to crypto, the correlation with US equities remains above 0.5.

BTC and the 10 year treasury yield have also been tracking each other closely since January 2024. In a previous macro report, we commented that fiscal deterioration in the US which was partly pushing up treasury yields may have supported price action since President Trump’s onslaught of tariffs earlier in the year. Lower treasury yields could result in a snap of that correlation, but the easing of liquidity as a result of lower government yields will more broadly support risk-on sentiment.

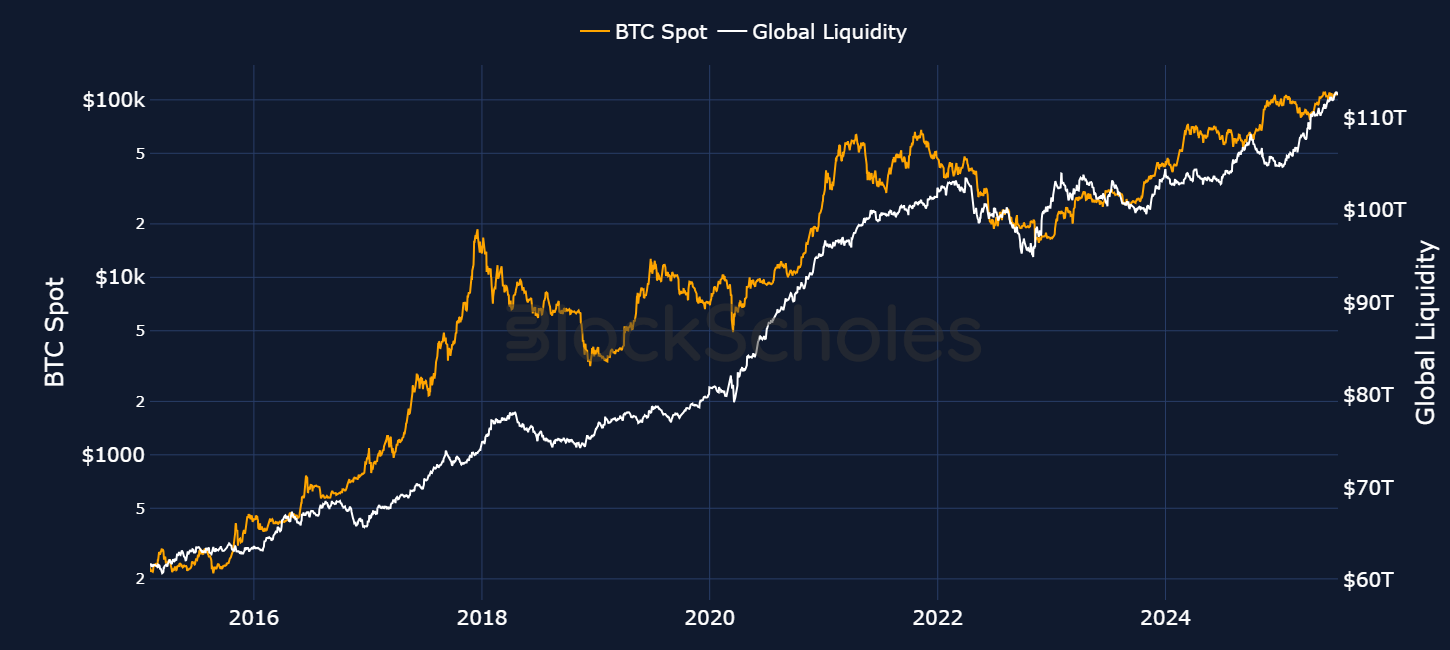

If the change to the eSLR goes through as planned, it will be akin to an ease of monetary conditions and increased liquidity in the financial system. That’s because it frees up space on major US banks’ balance sheets for further lending and investing activity, without risk of reaching capital requirement ratio limits. While it is difficult to attribute all short-term price movements in risk-on assets directly to global liquidity levels, in the long-run, an easing of liquidity supports risk-on assets such as Bitcoin.

The US 10 year treasury yield and the US dollar (as measured by the DXY) historically track one another. While that relationship broke during the reciprocal tariff turmoil back in April, a reconvergence back to that relationship in the direction of a weaker dollar and lower yields will also form a more favourable backdrop for riskier assets.

After all, among the consortium of risk-on assets, it is BTC which has outperformed the most since the start of the year amidst the backdrop of a 10% weakening in the US dollar.