Thahbib Rahman

Research Analyst

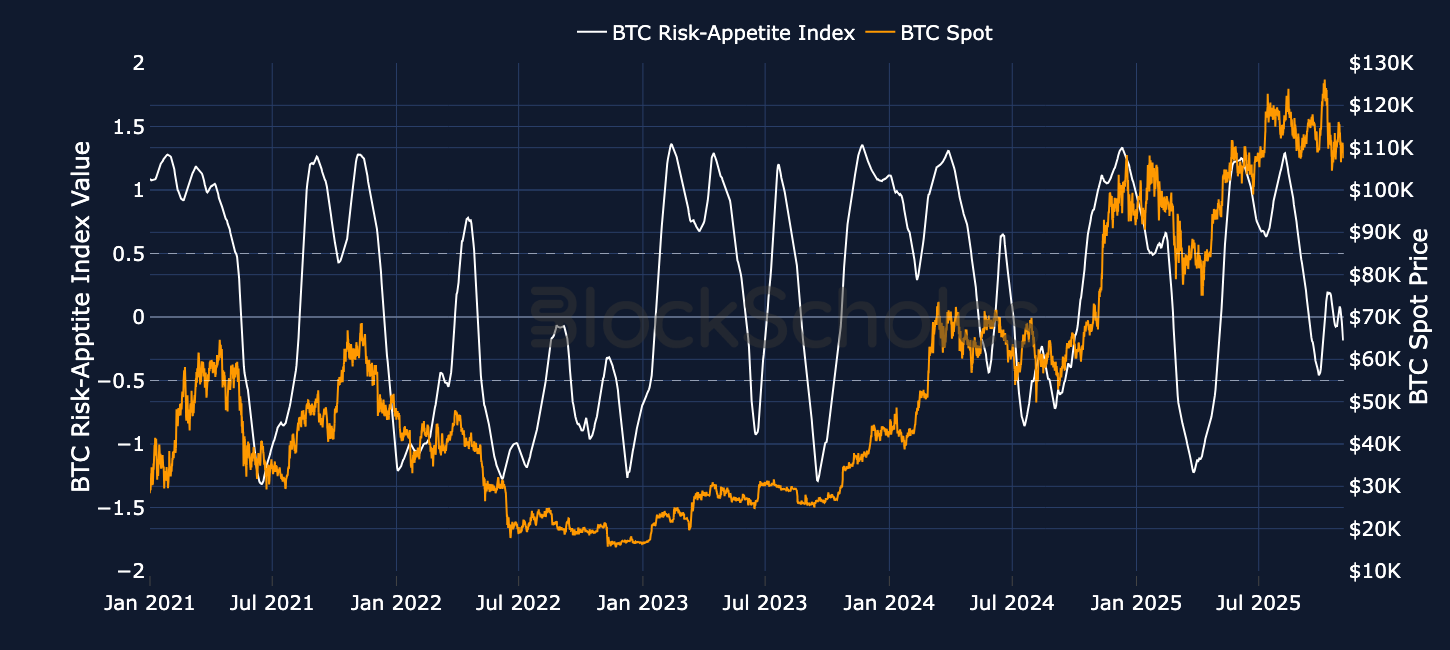

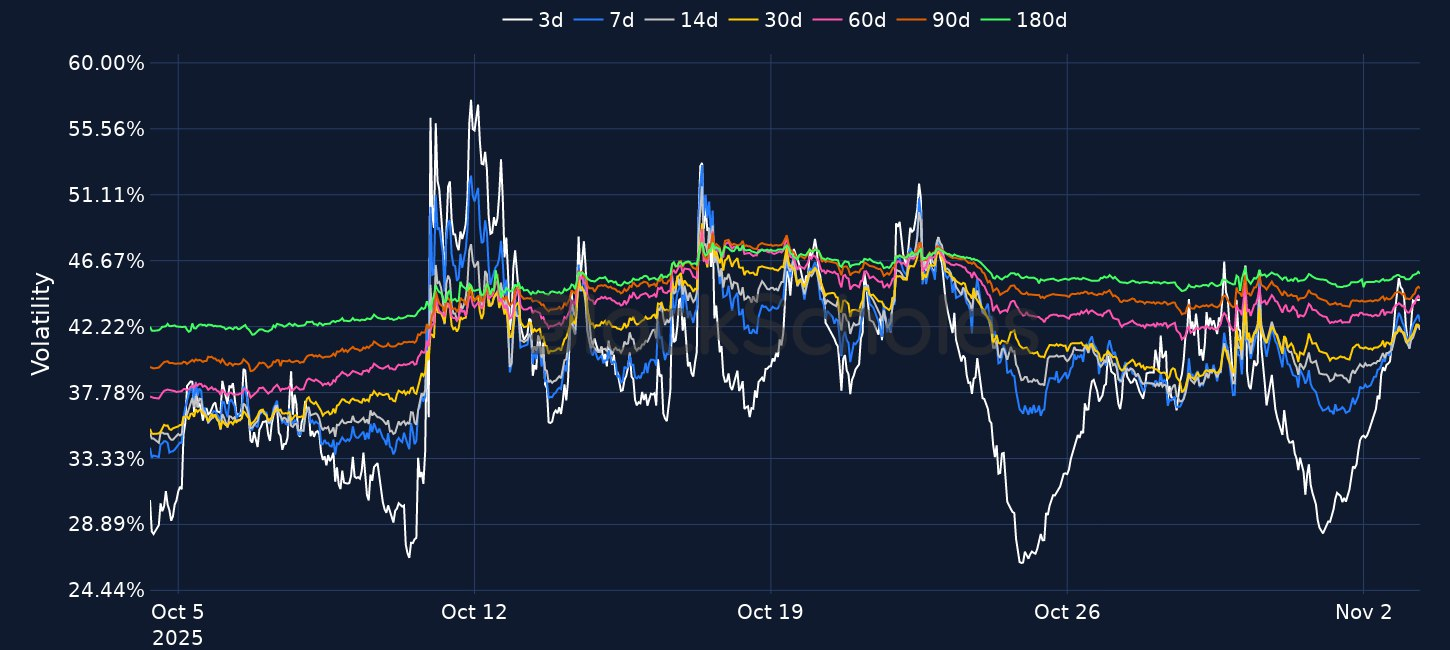

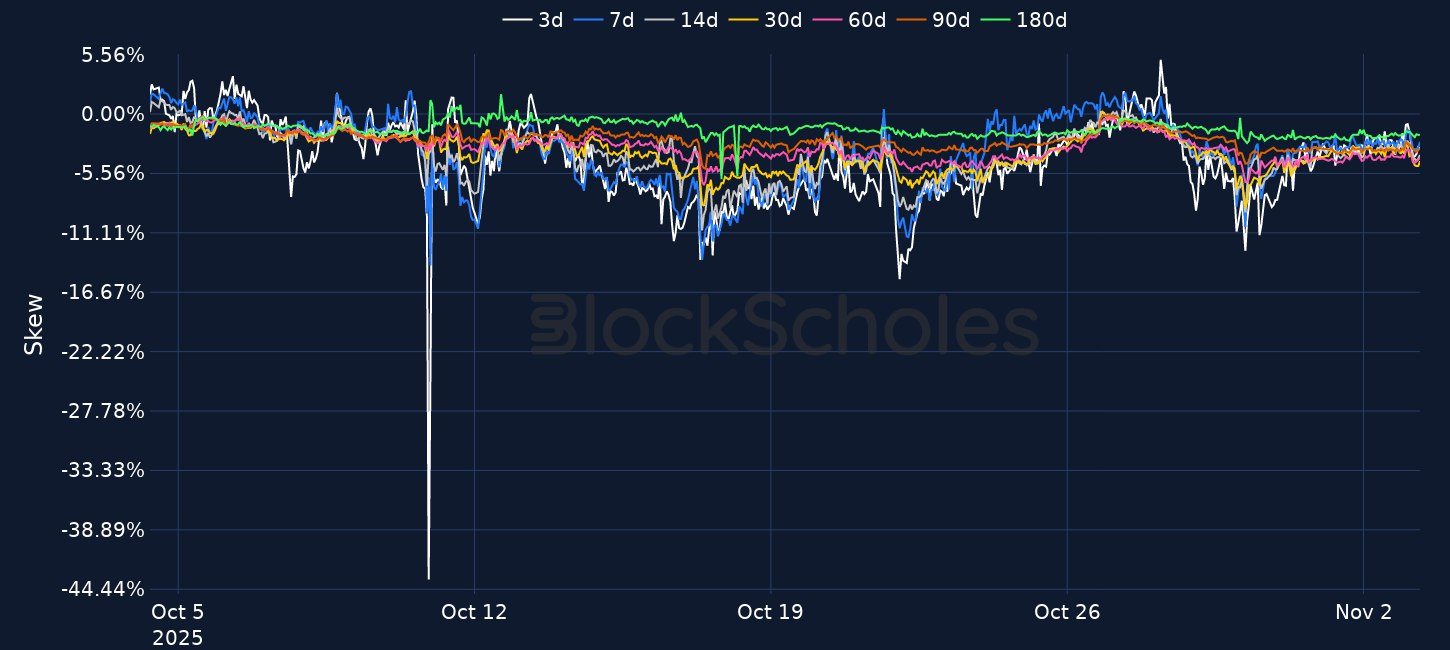

After sideways weekend trading, BTC is currently hovering above $107K, while ATM implied volatility across the term structure remains elevated between 43% and 45%. Chair Powell’s recent hawkish comments regarding the December FOMC meeting was followed by comments from a slew of other Fed officials who raised concerns over the October rate cut. Nonvoting members Beth Hammack and Lorie Logan both emphasised the importance of getting inflation back down to the 2% target before cutting rates further. Elsewhere, the National Assembly in France has approved an amendment introducing a 1% annual tax on “unproductive wealth,” which includes cryptocurrencies.

.png)

.png)