Thahbib Rahman

Research Analyst

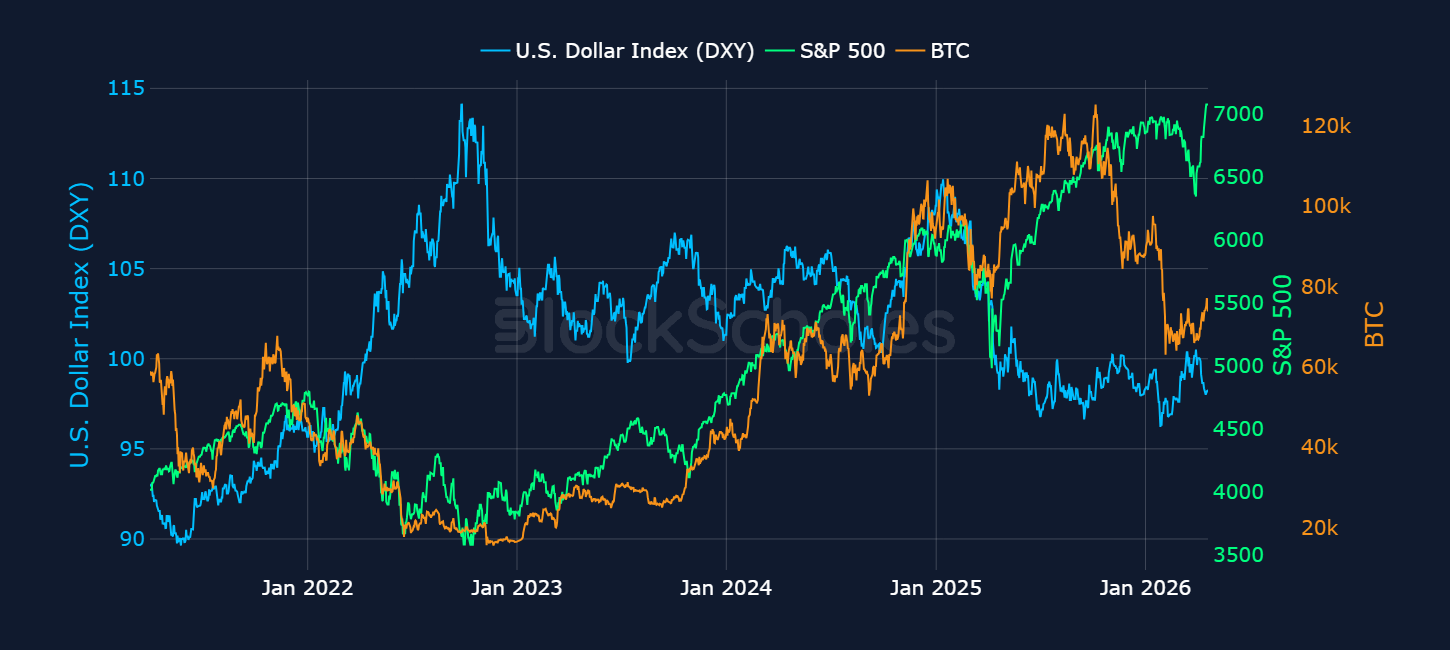

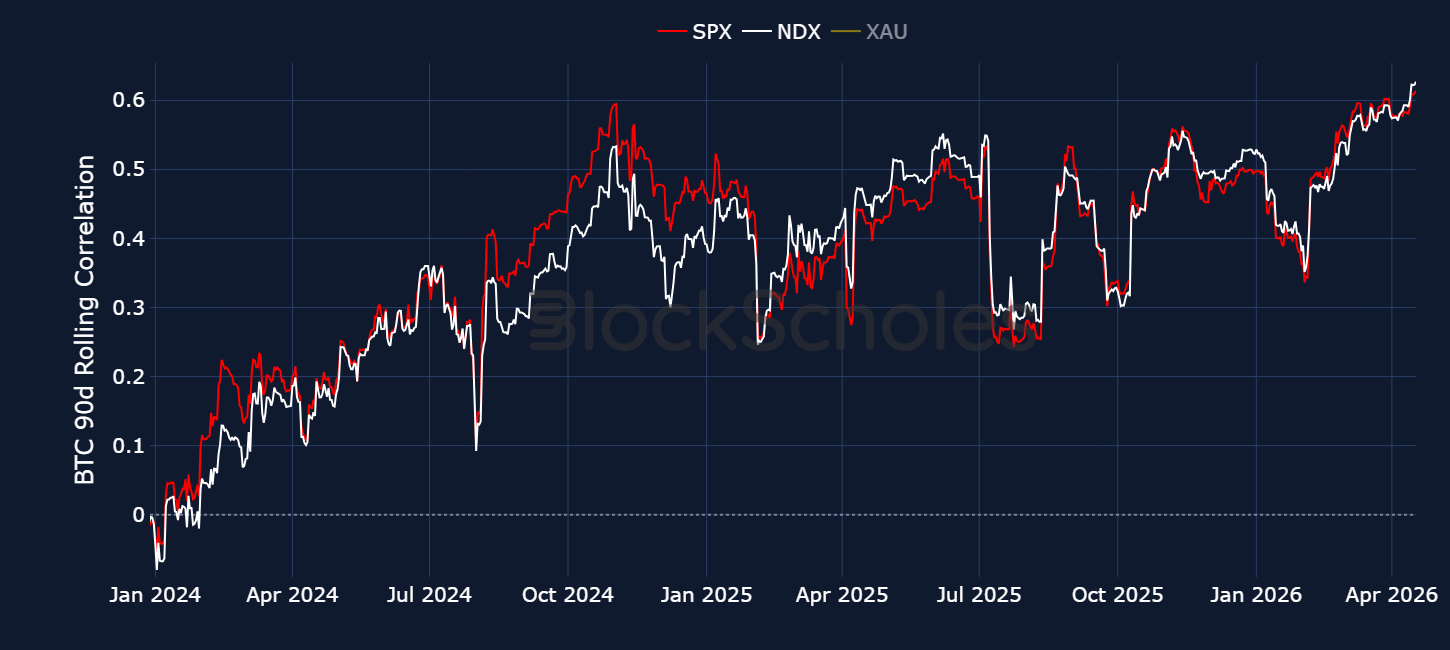

The first quarter of 2026 has so far delivered turbulent, cross-asset volatility spanning digital assets, precious metals, and US equities. BTC for example currently trades more than 40% below its all-time high. Part of that selloff can be attributed to crypto-specific shocks, namely October 10’s historic $19B liquidation event, however crypto sentiment has also been weighed down by a selloff in US equities, driven by fears over the ramifications of AI. Both crypto and equities have sold off in tandem year-to-date, bringing BTC's correlation with the S&P 500 and Nasdaq 100 to its highest since November 2025, yet it is still crypto assets that have borne the brunt of the pain; falling far more sharply in downturns while rebounding more softly in recoveries.

The first quarter of 2026 delivered turbulent, cross-asset volatility spanning digital assets, precious metals, and US equities. BTC for example currently trades around 40% below its all-time high. Part of that selloff can be attributed to crypto-specific shocks, namely October 10’s historic $19B liquidation event, however earlier in the year crypto sentiment had also been weighed down by a selloff in US equities, driven by fears over the ramifications of AI. Both crypto and equities sold off in tandem year-to-date, bringing BTC's correlation with the S&P 500 and Nasdaq 100 to its highest since November 2025, yet it is still crypto assets that borne the brunt of the pain; falling far more sharply in downturns while rebounding more softly in recoveries.

However, one other notable driver of macro asset price-action has been President Trump’s approach to foreign policy, with geopolitical tensions heavily weighing on crypto prices. This report examines the dynamics of the Q1 2026 macro asset selloff. As these major developments have taken place outside of traditional trading hours, the market for tokenised real-world assets (RWAs) has captured headlines. With Bitget offering traders access to a plethora of tokenised stocks, perpetual futures contracts on tokenised tickers and access to FX and commodities, traders have had a chance to respond to geopolitical tensions in real time, completely reshaping cross-asset hedging, price discovery, and market structure. Indeed, according to Bitget, during the first week of December it was able to capture more than $88 million in trading volume for Ondo tokenised stocks, equivalent to 73% of the total market share.

We utilize Bitget's TradFi platform which provides a wide coverage of global equity indices, forex, commodities, and precious metals, to compare the market’s real-time reaction to the US–Venezuela and US–Iran military interventions. In doing so, we assess the extent to which 24/7 tokenised markets are already functioning as hedging venues during periods of geopolitical stress, and what that means for the future of multi-asset trading.

Launched at the beginning of 2026, Bitget’s TradFi product lets users trade traditional markets directly using USDT as collateral, without a need to open a separate brokerage account or move money through a separate fiat funding process. Currently, Bitget supports a total of 79 “TradFi” trading instruments across four markets: FX, metals, indices, and commodities.

In parallel, Bitget extends the same “single venue” concept into tokenised RWAs, offering tokenised U.S. stock exposure onchain through its Onchain/Wallet rail, which broadens the inventory beyond macro contracts into equity-linked instruments.

At the core of Bitget’s positioning is the idea that the main industry bottleneck remains a lack of unification: market access is still fragmented across exchanges, brokerages, wallets, bridges, and funding rails. Bitget frames its UEX as a way to consolidate account access, custody, execution, and risk controls within a single operational stack and security perimeter.

Beyond Bitget’s integration of tokenized xStocks and Ondo Finance, users have access to Bitget Onchain, which enables them to access onchain tokens from an existing Bitget spot balance using USDT or USDC removing the need for chain switching and bridge-based transfers.

Four months in, 2026 has already delivered significant market turbulence, with digital assets, precious metals, and US equity indices charting sharply divergent paths. US equities and risk-on assets entered the year positively, with BTC rallying to around $94-95K, the S&P 500 hitting new highs, and the Russell 2000 outperforming. By January 8th, however, the equity rally had begun to lose steam, with stocks, the dollar, and Treasuries selling off in tandem, even as precious metals continued to climb.

By the end of January 2026, a confluence of macro events pushed equities lower still, most notably a sharp escalation in AI fears surrounding the profitability of the sector relative to the enormous capital being deployed by firms. Precious metals also crashed significantly: gold recorded its biggest slide in four decades, while silver plunged from $120 to $98. At the same time, markets began pricing in a less dovish Fed chair in Kevin Warsh.

The selloff deepened into early February, with BTC retreating to pre-election levels. Anthropic's announcement of new AI automation tools sent shockwaves through markets. Software stocks bore the initial brunt before the selloff broadened, as investor concerns shifted from AI spending to the wider threat of AI-driven disruption across industries. Amid the broader downturn, gold remained a relative safe haven, while digital assets including BTC and ETH continued to struggle. Silver, often characterised as the retail trade of the precious metals complex, behaved more like a speculative asset, tracking risk sentiment rather than following gold's defensive bid.

More recently, it is President Trump’s foray into the Middle East that has influenced price action. As the US and Iran continue to send conflicting signals regarding any potential offramp to end the war, risk-sentiment has fluctuated to the ebbs and flows of geopolitical headlines. While crypto assets have remained resilient to the conflict, precious metals have actually pared back some of their gains. US equities initially fell at the onset of the conflict, though have slowly returned closer to all-time high levels once more.

This divergent behaviour across asset classes has, however, highlighted the utility of venues that allow traders to flexibly move across asset classes without leaving the crypto-native trading stack. On Bitget’s UEX, tokenised RWAs and stablecoin-collateralised TradFi products sit alongside crypto and onchain tokens, allowing exposure to be adjusted without waiting for local cash-market sessions, broker cut-offs or jurisdiction-specific funding frictions.

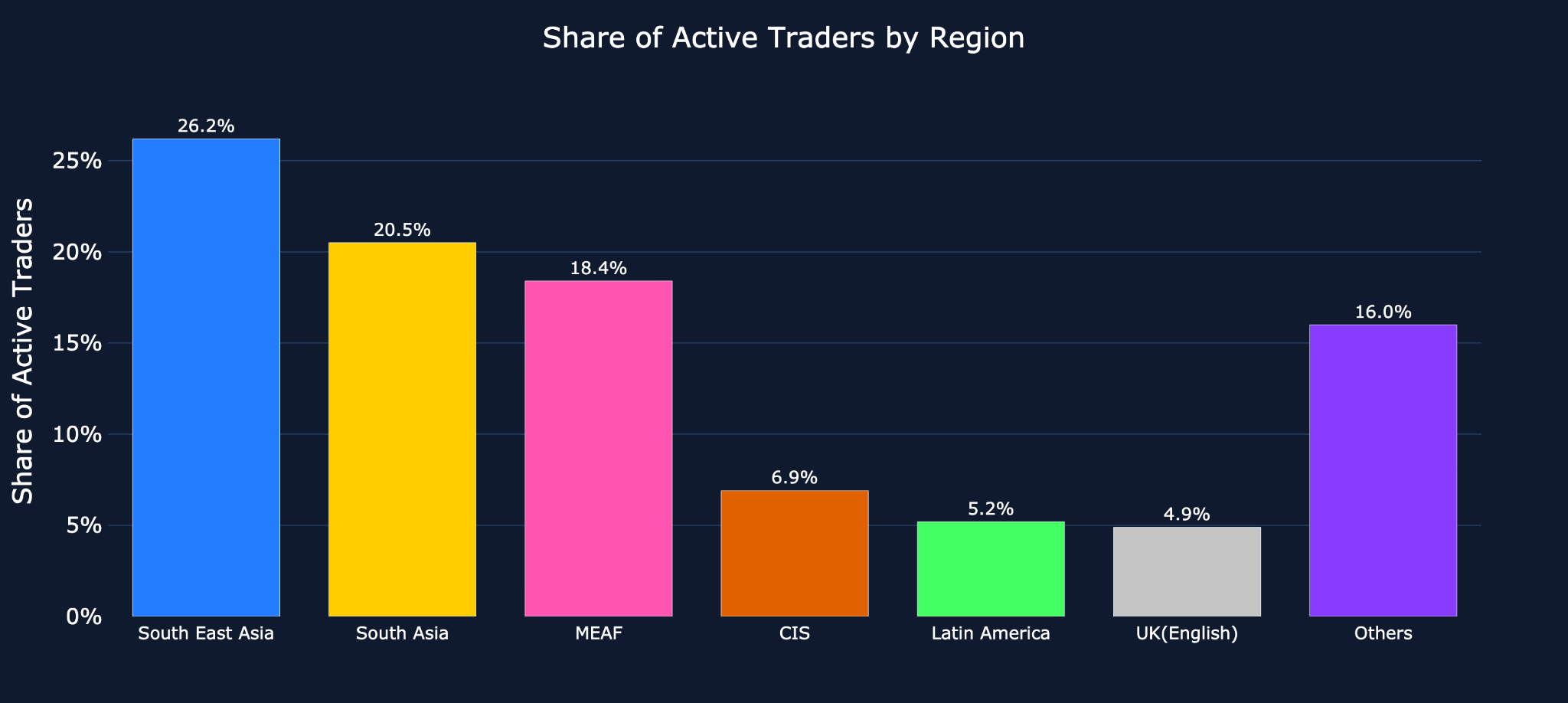

Bitget’s globally distributed user base plays a key role in supporting liquidity across 24/7 perpetual futures markets, where trading activity is no longer dictated by any single regional session or market open. This is reflected in the distribution of active traders, with Southeast Asia leading at 26.2%, followed by South Asia (20.5%) and the Middle East and Africa (MEAF) (18.4%), the Commonwealth of Independent States (CIS) (6.9%), Latin America (5.2%), and the UK (4.9%); all other regions account for less than 16%.

By providing exposure across multiple markets, traders are able to take advantage of diversification opportunities if timed correctly, such as rotating capital from gold into oil. Traders have indeed capitalised on that ease of trading in and out of crypto and TradFi assets: Bitget TradFi reached $2B in daily trading volume within three days of launch. That then quickly doubled to $4B by Jan 21, 2026. On Mar 20, 2026, Bitget TradFi recorded a single-day high for trade volume above $6B as gold had its worst week since 1983, while major volatility in energy prices saw Brent crude oil trade above $110 per barrel.

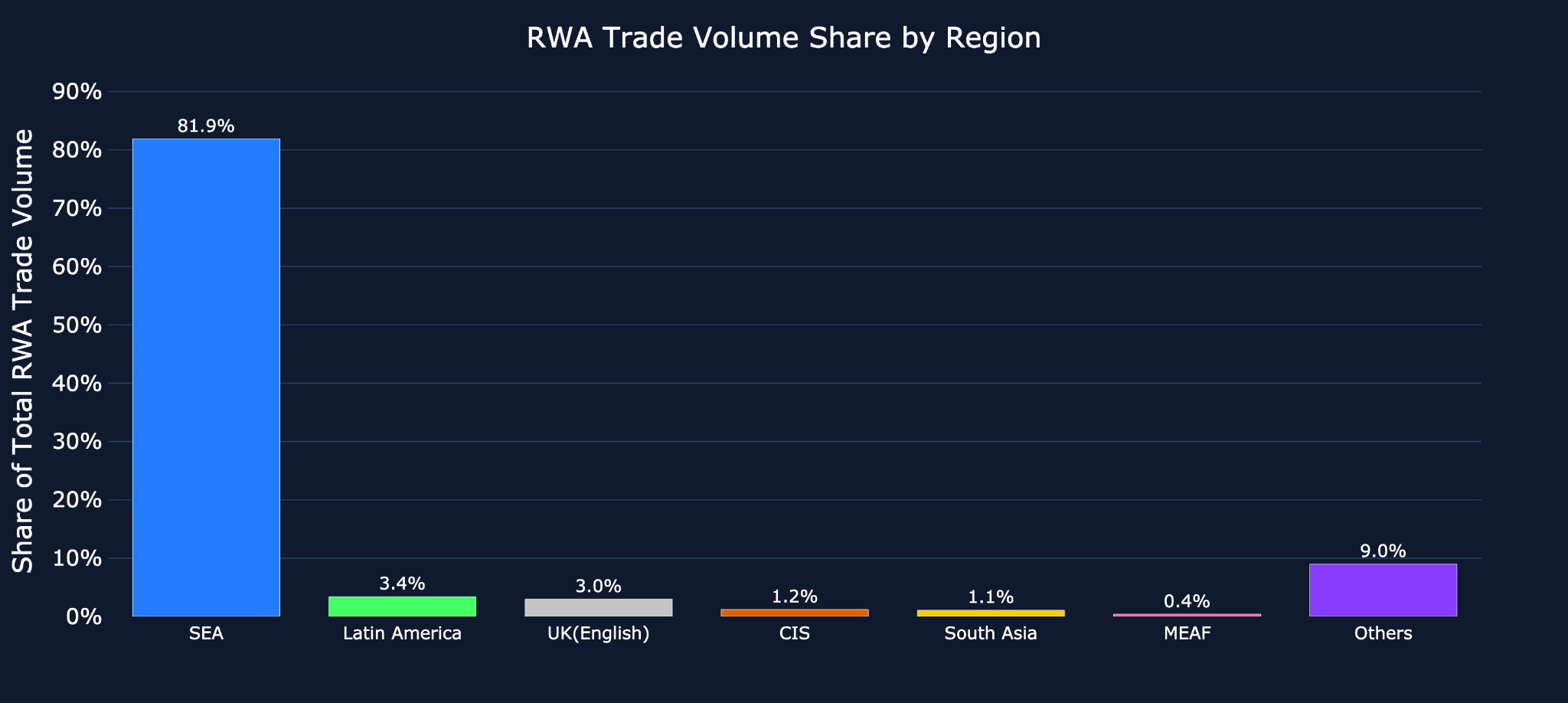

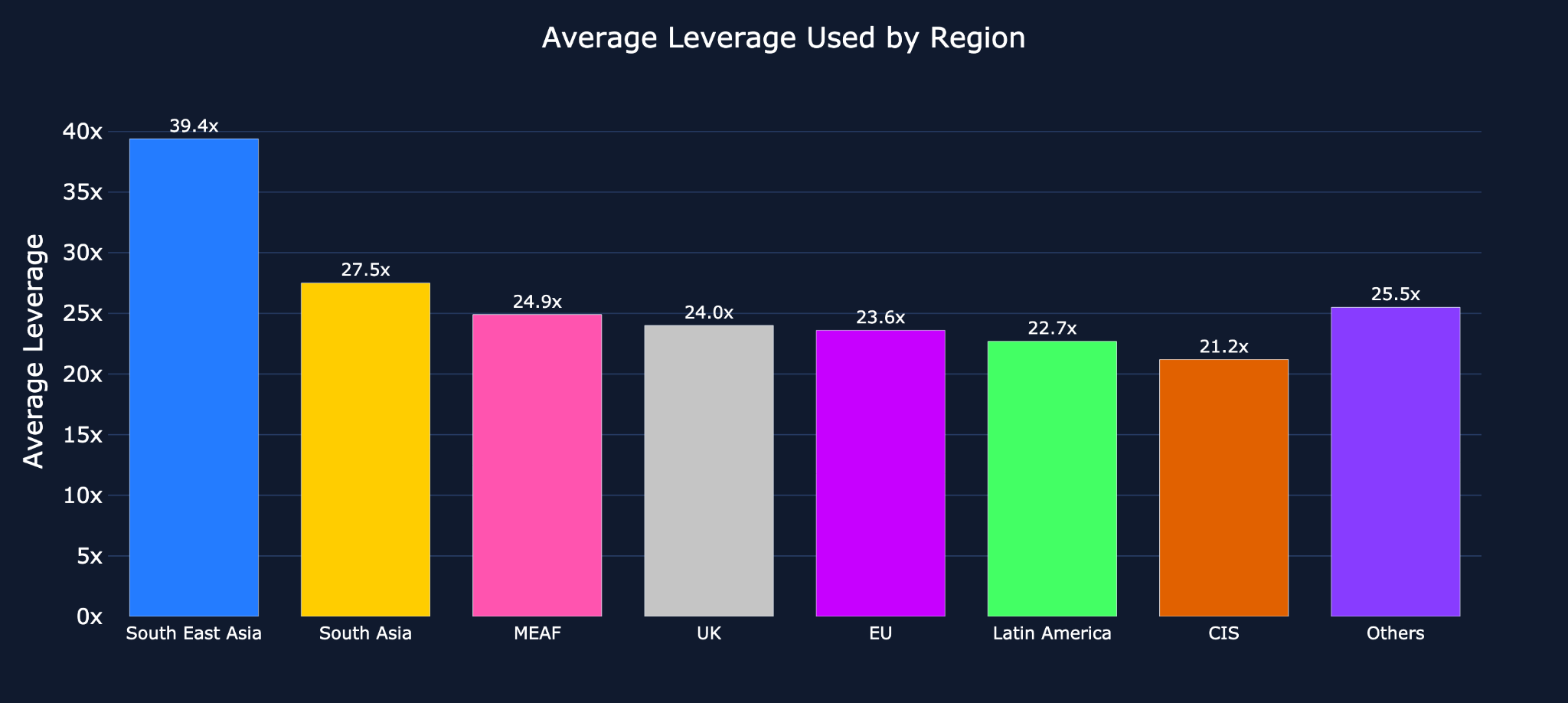

However, trading activity in RWAs has so far been highly concentrated in Asia, with South East Asia accounting for 81.9% of total RWA trade volume on Bitget. This means that much of the price action in these assets is likely to occur during Asian hours, suggesting that those traders in other timezones may be able to enjoy an informational edge against traders who are not active during traditional US market hours. Further, the SEA region also records the highest average use of leverage, at 39.4x. The higher use of leverage in perpetual futures can significantly amplify moves in those hours and result in larger than usual volatility levels.

A weaker US dollar is generally supportive of risk-on assets, as many key financial assets including US equities and BTC are priced in dollars. Yet, the shifting AI narrative, from spending concerns to fears of widespread employment disruption, as well as Trump’s escalating geopolitical manoeuvres in Venezuela and Iran, has left markets struggling to price not just individual assets, but the correlation between them.

The dollar found support from safe haven demand as tensions in the Middle East continued, while equities briefly stalled in what had been an imperious march toward 7,000 points. More striking still – BTC has underperformed equities year-to-date, appearing to break from the historically close relationship between crypto and equity markets. Despite the underperformance, BTC continues to be the most-traded asset on Bitget globally, with key exceptions including the Commonwealth of Independent States (CIS), the Middle East and Africa (MEAF), as well as South East Asia, where ETH leads trading activity.

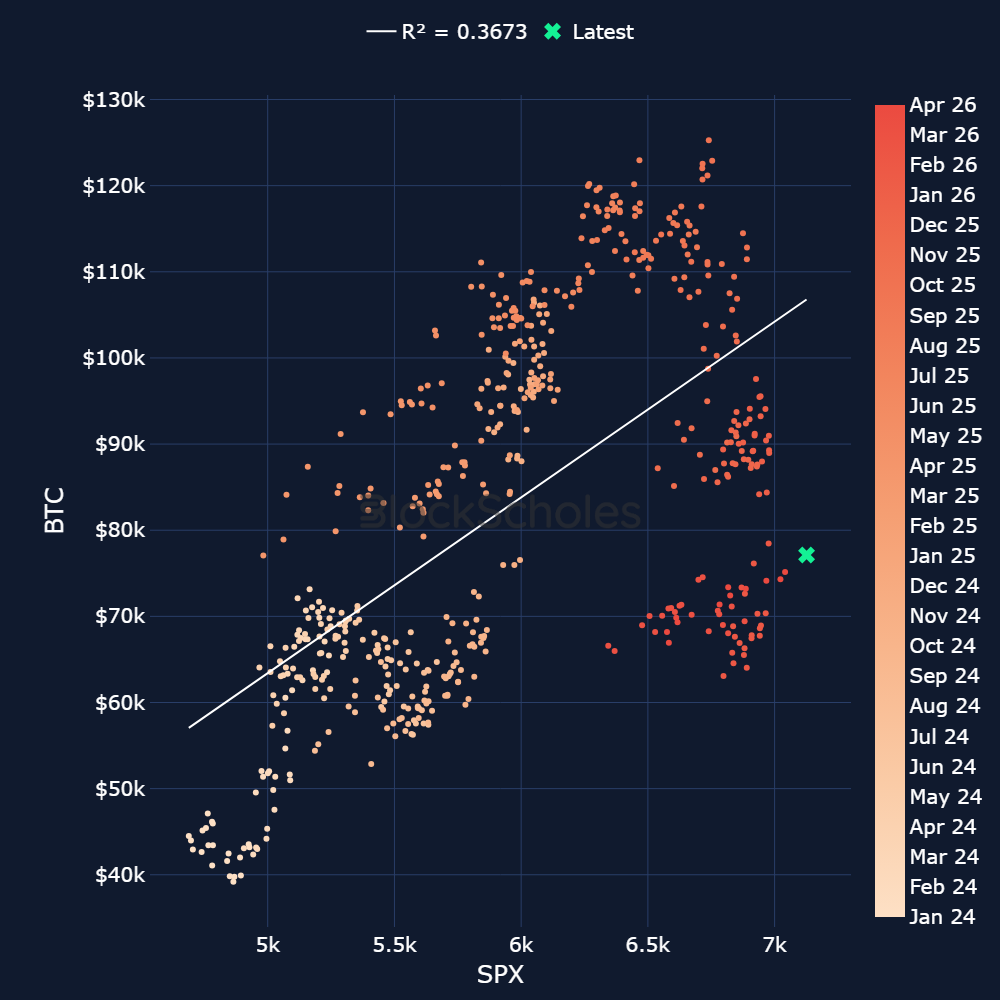

While the S&P 500 is now up 1.6% so far this year, BTC has dropped by a sharper 15% and currently sits around 40% below its all-time high. While all asset classes have been impacted, crypto-assets have suffered far larger losses in the lingering aftermath of crypto’s most devastating liquidation event, October 10, 2025, when $19B was forcibly wiped out and 1.6M traders were liquidated.

Despite this spot divergence, BTC’s correlation with the S&P 500 and Nasdaq 100 is at its highest level since November 2025. Crypto has always been a more volatile asset class, often acting like a leveraged trade on market sentiment, outperforming when markets rally and falling more sharply during downturns. So far this year, however, the dynamic looks different. While BTC’s correlation with equities remains dominant, it has been selling off far more aggressively in market downturns while rebounding far more softly in broader market recoveries.

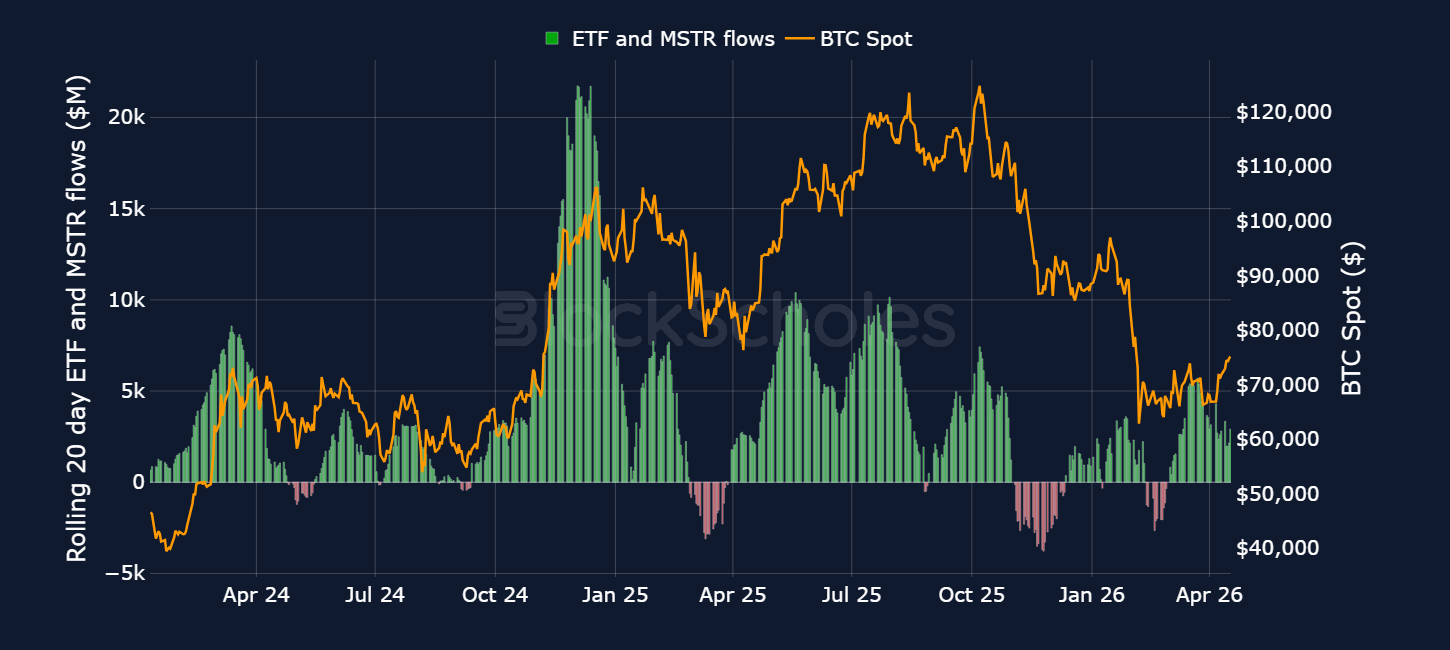

The high correlation to US equities is due in part to Spot BTC ETFs in the US, which have provided a regulated investment vehicle for TradFi institutions and retail participants to trade BTC in the same place and at the same time as other exchange-traded assets.

In addition to influencing the high correlation with US equities, ETFs also give us a clearer picture of demand for BTC via net inflows and outflow records. This, considered alongside public disclosures of bitcoin acquisitions by publicly traded Digital Asset Treasury companies (DATS) like Strategy (MSTR) provide a significant (in not exhaustive) picture of the demand for bitcoins.

The sell-off at the beginning of the year saw the rolling 20-day sum of that demand drop into negative territory as these groups were net sellers of BTC, far below the highs of 2025. However, since March 2026 inflows have dominated outflows once again.

Price action in the first few months of 2026 has highlighted the importance of agility in markets. Cross-asset correlations are continually shifting and access to a wider range of markets is now more vital than ever. At the same time, we are seeing a rapid development in the trading of perpetual swaps of Real World Assets (RWAs) such as equities, precious metals, and commodities to meet that surging demand. This global participation is reflected in the distribution of active traders, with Southeast Asia leading at 26.2%, followed by South Asia (20.5%) and MEAF (18.4%), while the CIS (6.9%), Latin America (5.2%), and the UK (4.9%) represent smaller but still meaningful shares; all other regions account for less than 16%.

In a stark departure from his predecessor’s approach to crypto, current SEC Chair Paul Atkins expects US financial markets to move on-chain “in a couple of years.” Bitget's own estimates put annualised trading volumes for equities between $160-$200T by 2030, with crypto markets facilitating between 20% and 40% of that volume.

As regulatory clarity continues to advance in the US and as institutions increasingly look to build onchain, we expect that the market for real-world assets will continue to grow exponentially. The reaction from onchain markets during the US-Iran strike announcement was preliminary evidence of our view that tokenised RWAs have and will continue to reshape hedging, liquidity and market structure dynamics over time.

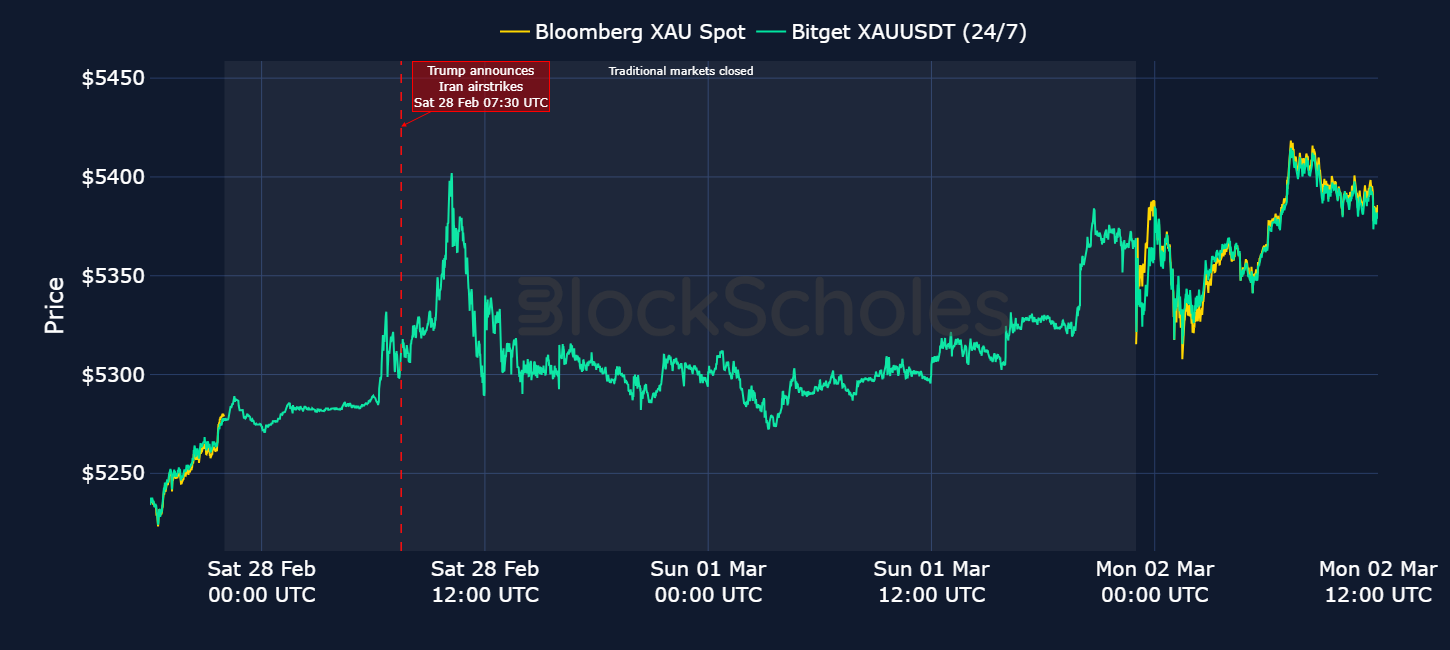

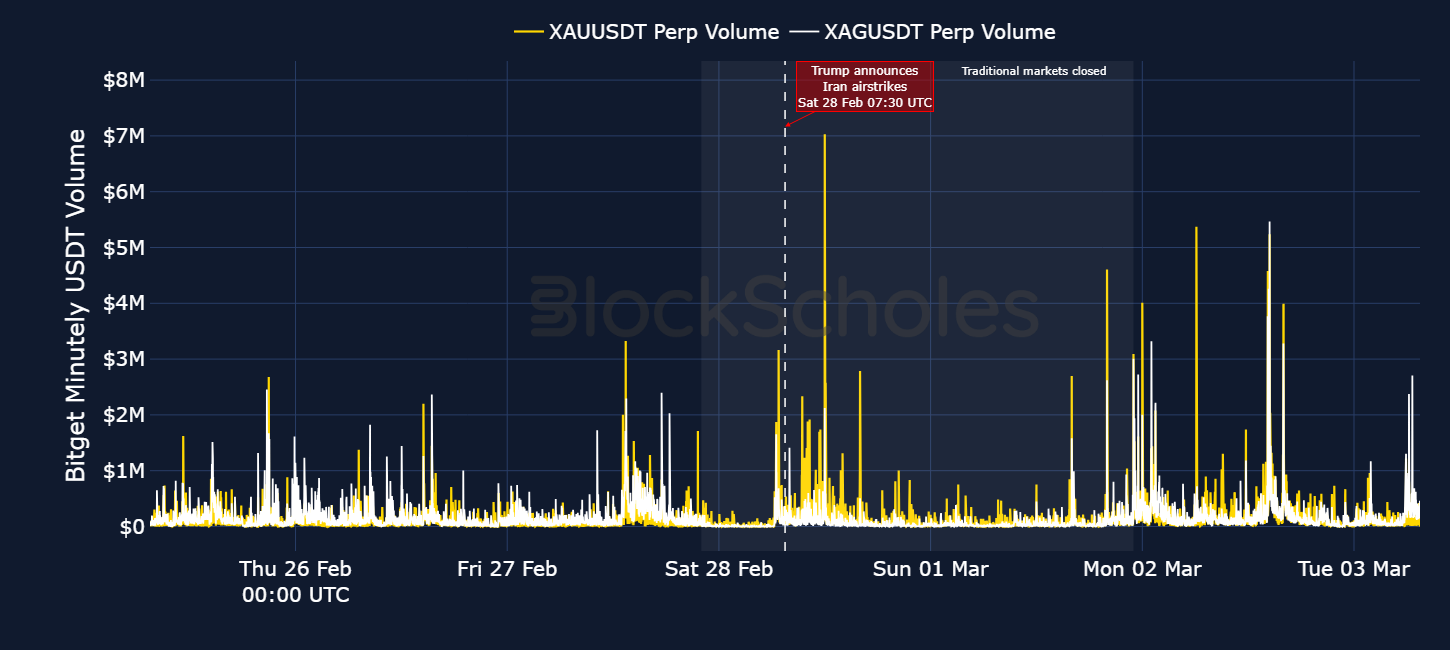

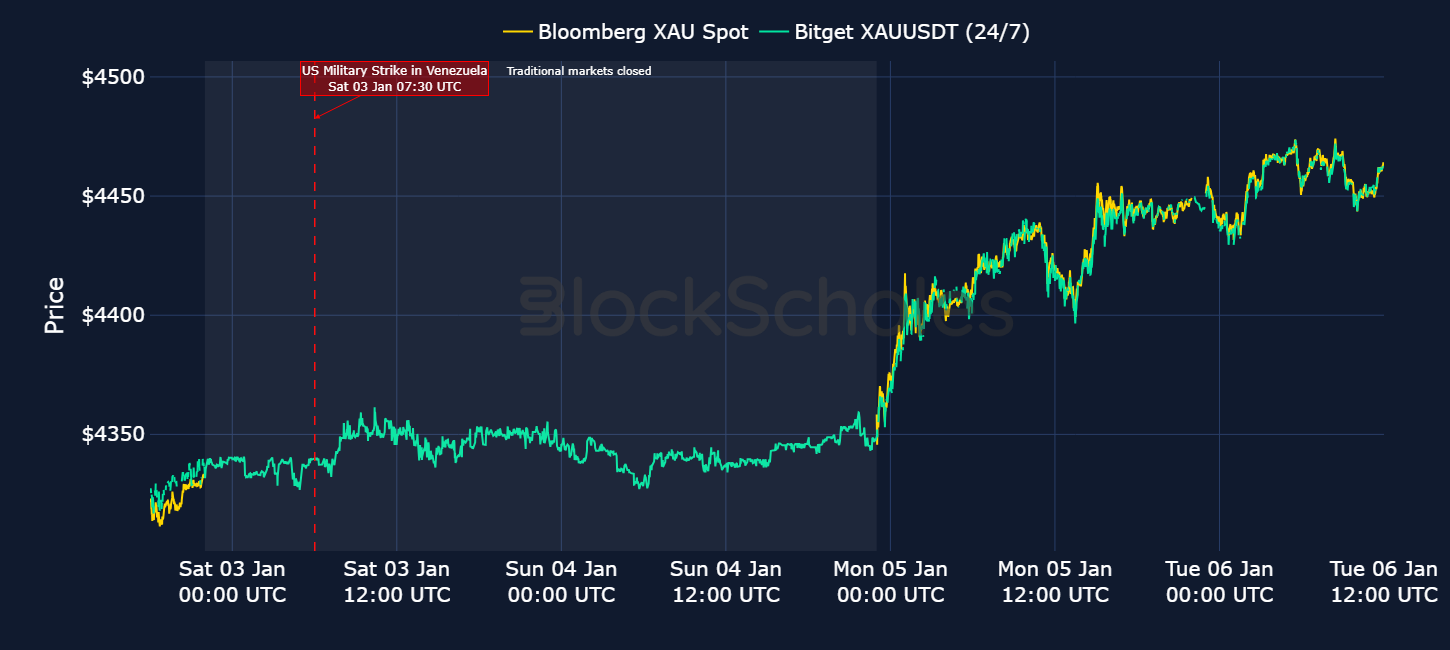

On the weekend of Feb 28, 2:30AM ET (7:30AM UTC), when the most liquid global financial markets were all closed, President Trump officially announced that the US had launched military airstrikes against Iran. Past major geopolitical shocks of this kind, outside of market hours, would have required investors to wait until the US futures market (6PM ET on a Sunday) or the US stock market opened, to hedge their positions and gauge the market’s sentiment. However, this time, traders were able to turn to crypto-native markets that trade 24/7.

The chart above shows Bitget’s tokenised XAU USDT perp price showing evident signs of price discovery over that weekend, while traditional markets were closed. Traders rushed to hedge positions and took advantage of the 24/7 mechanism of the perpetual futures contract.

In TradFi markets, Bloomberg recorded gold’s spot price closing at $5,279 on Friday Feb 27, 2026. Following Trump’s announcement, traders rushed to Bitget’s XAUUSDT perp, pushing its price up to a peak of $5,402 (+2.3% from Friday's TradFi close). Then on Monday Mar 2, 2026, spot gold price on traditional markets opened with a gap up from Friday, reflecting the already weekend-discovered move higher on Bitget. Bloomberg gold price opened at $5,315; while the XAU USDT perp traded at $5,329 (a $13.29 spread) at the TradFi market open.

That weekend price discovery (between Feb 27 and Mar 2) was also accompanied by a large spike in perpetual trade volumes. The chart below plots the minutely changes in volumes for Bitget’s XAU USDT perp and XAG USDT perp, gold and silver, respectively. Prior to President Trump’s announcement, minutely gold perp volume was around $200K. That increased to over $2M only two hours after the announcement and over $7M around 12PM UTC as the gold spot price rose from $5291 to $5340.

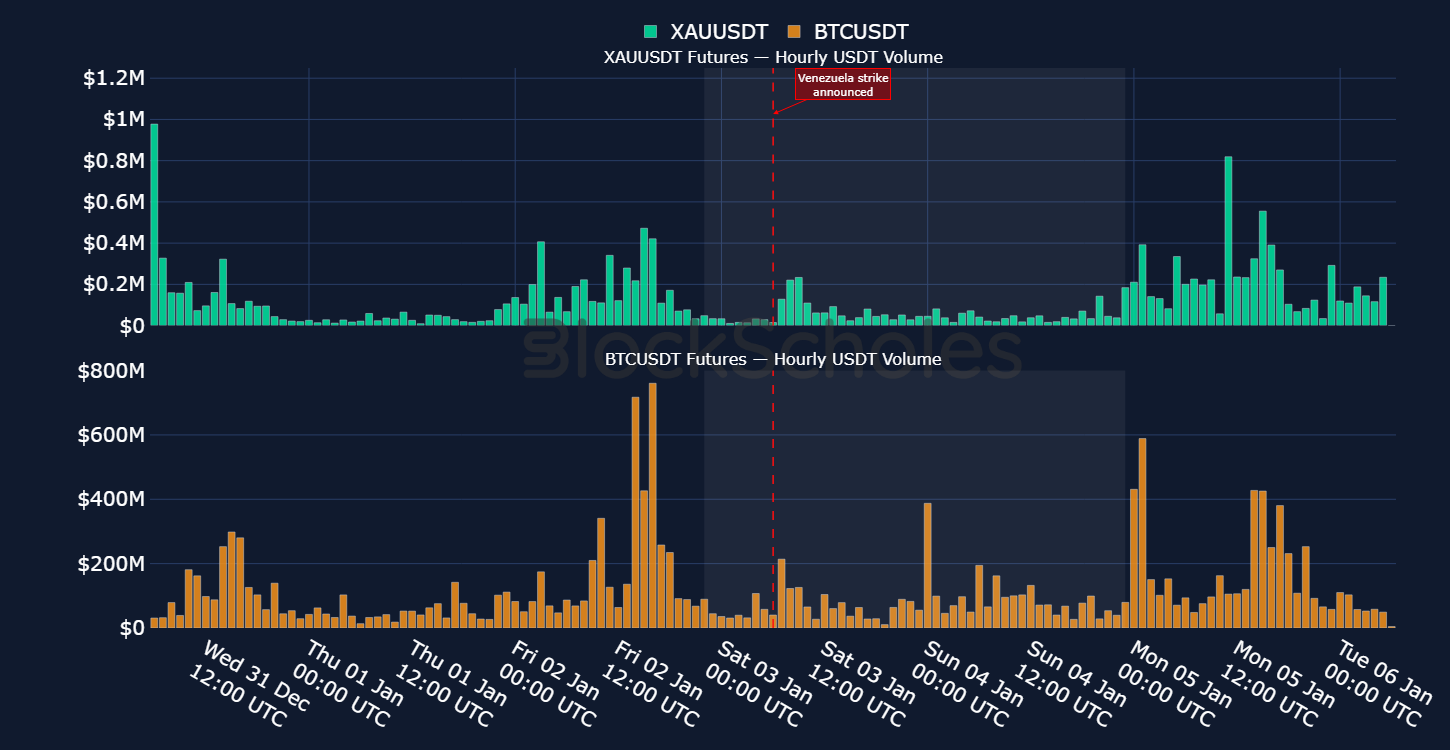

President Trump’s attack on Iran is not the first military intervention during his second presidency; nor is it the first to take place outside of market hours. On Sat Jan 3, 2026, the US launched a military strike in Venezuela which ended with the capture of incumbent President Nicolás Maduro.

Unlike the operation in the Middle East, however, during the weekend of the Venezuelan attacks, onchain gold prices barely registered any moves. In fact, the real move in onchain prices occurred after traditional markets had opened on the following Monday (Jan 5) and onchain prices followed traditional spot gold prices higher up towards $4,450 per ounce.

That minimal price discovery during the Venezuela case relative to Iran could be due to a number of reasons. The first is that the market may have looked through Trump’s actions in Venezuela as a “one-off event”, with further attacks seen as a tail-risk not a base-case scenario. There is partial evidence to support this. At the start of the year, risk-assets (BTC, S&P 500, and the Russell-2000) and precious metals were all rallying concurrently, suggesting that markets showed tentative signs of looking through the fallout in Caracas. Despite that, it is still difficult to definitively assign the lack of weekend price discovery to this alone. That’s because in the later part of the weekend, Trump claimed the US may launch a second military strike on Venezuela, or even carried out additional military interventions in the Latin American region. This theory is also less probable given that onchain prices moved, but only after global markets reopened.

The lack of moves on this occasion may be due to the changing market structure dynamics within crypto that have been enabled by the growth in tokenised RWAs. During the weekend of the Venezuelan intervention, hourly volumes on the BTC/ USDT perp contract spiked to as much as $400M as President Trump claimed that the United States was now “in charge” of Venezuela. Hourly volumes on Bitget’s gold perps also increased around the time of the invasion by more than 6x to $200K. However, on an absolute basis, volumes on these contracts were minimal relative to BTC spot volumes implying that these contracts would not have served as strong venues for hedging the geopolitical risk due to their low liquidity and volume. That was not the case during the intervention in Iran, suggesting a change in market maturity between the two events.

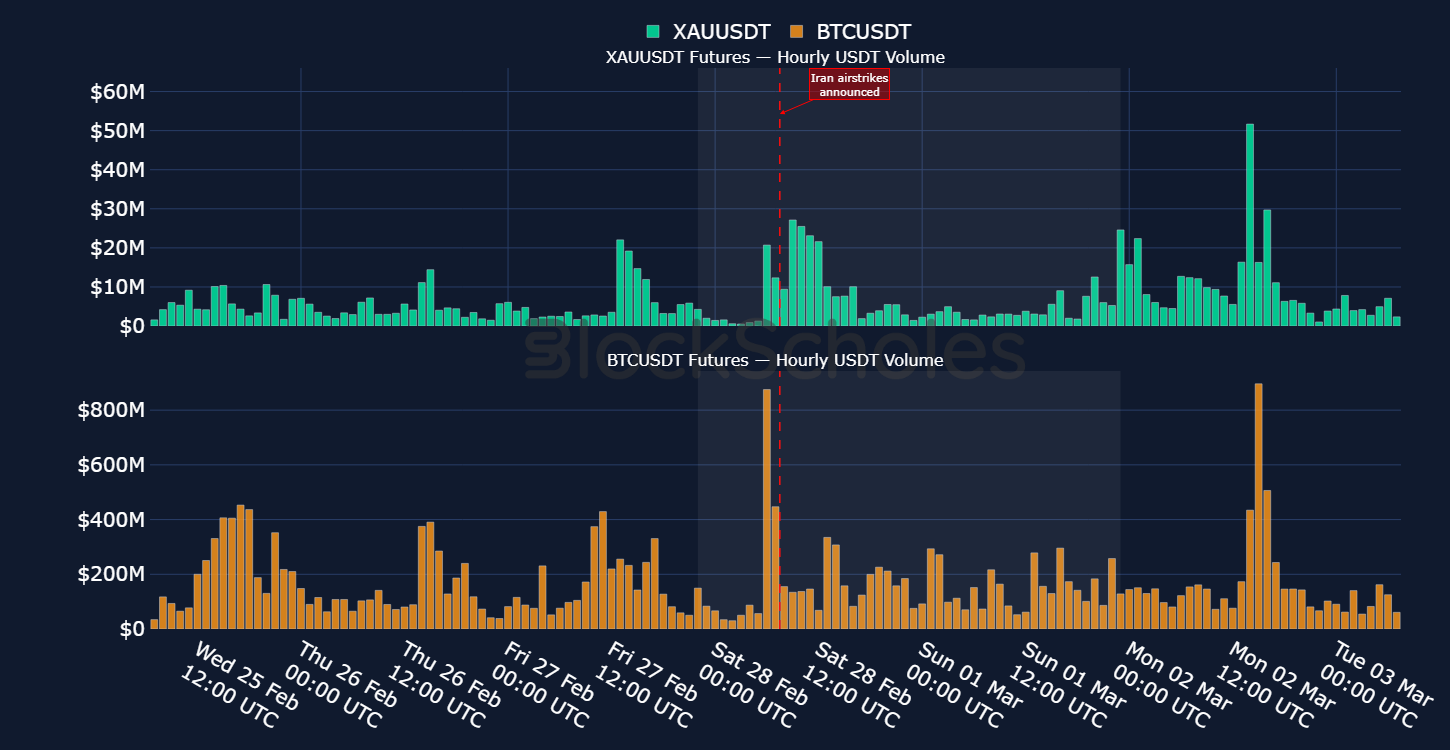

During the US-Iran announcement, attention (and volumes) in gold perp contracts on an absolute basis were already much higher around the time of the event. They then spiked by an even larger amount, jumping from $1M to a peak of $27M.

While that was still magnitudes lower than the $800M in hourly volumes on BTC perps, the diverging trend in volumes in the immediate aftermath of the announcement is revealing. BTC perp volumes declined and only spiked higher again when traditional markets reopened, while gold perp volumes remained high for a few hours before returning to their pre-trend, the clearest signal yet that this time around traders utilised the onchain 24/7 tokenised contracts when geopolitical stress hit.

Together, this reveals two things: the first is that during the start of the Iran intervention, traders showed a much stronger willingness to hedge and enter positions within gold perpetual contracts, relative to the earlier Venezuelan intervention and that in turn may partly explain why the weekend gold moves onchain echoed the traditional market ahead of time during the Iran strikes, but only moved higher after global markets opened during Maduro’s capture. Secondly, liquidity and volumes in both instruments tend to be much higher during traditional market open hours than outside them. In both military interventions, gold and BTC perp volumes were comparatively much higher during hours that coincide with the period when global markets are open than during the weekends.

Volume doubled from $2B to $4B in just two weeks in January 2026, as "event-driven" traders looked to hedge against macro volatility took advantage of Bitget’s selection of 100+ tokenized stocks and 200+ CFD instruments (Forex, Gold, Oil) alongside 2M+ crypto tokens. This is particularly relevant in the current regime, where rapid cross-asset repricing has increased the value of continuous access and fast reallocation across asset classes.

The opening months of 2026 have underscored the increasing interconnectedness of crypto and traditional markets. BTC's elevated correlation with US equities, combined with crypto-specific liquidation cascades and macro headwinds, produced one of the most prolonged drawdowns in recent memory. At the same time, precious metals have also experienced sharp reversals, leaving few corners of the market unscathed.

Against this backdrop, tokenised RWAs have begun to demonstrate their practical value to crypto-native traders. The contrast between the US-Venezuela and US-Iran is revealing: during the earlier intervention, onchain gold volumes were too thin to support meaningful price discovery over the weekend and by the time of the Iran strikes, traders were actively using gold perpetual contracts to hedge and position ahead of the traditional market opening, foreshadowing Monday's gap-up in spot gold.

As cross-asset correlations continue to shift and geopolitical risk remains elevated, continuous market access is more valuable than ever. Bitget's unified exchange model combines crypto-native markets, tokenised TradFi instruments, and onchain assets within a single venue and margin system thereby offering a framework for capital rotation management that this environment demands. The first quarter of 2026 suggests that the convergence of crypto and traditional finance is already underway.

.jpg)

.jpg)

.jpeg)

.jpg)