Thahbib Rahman

Research Analyst

Despite a more dovish-than-expected Jackson Hole speech from Chair Powell, BTC's spot price has failed to recover to its pre-Jackson Hole level, while risk-on sentiment in altcoins and US equity markets still seems to be intact. Skew in BTC options and IBIT options also suggest continued downside price action.

Markets have taken Chair Powell’s final Jackson Hole speech last Friday as surprisingly more dovish than expected. While acknowledging that “The effects of tariffs on consumer prices are now clearly visible” and that the “labor market appears to be in balance”, Powell still opened the door for a rate cut as soon as September: “with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance.”

Now, markets are pricing in an 88.2% probability that the Fed cuts the federal funds rate by 25bps — a strong indication of their conviction that Powell has signalled a resumption of the easing cycle that first began back in September, one year ago.

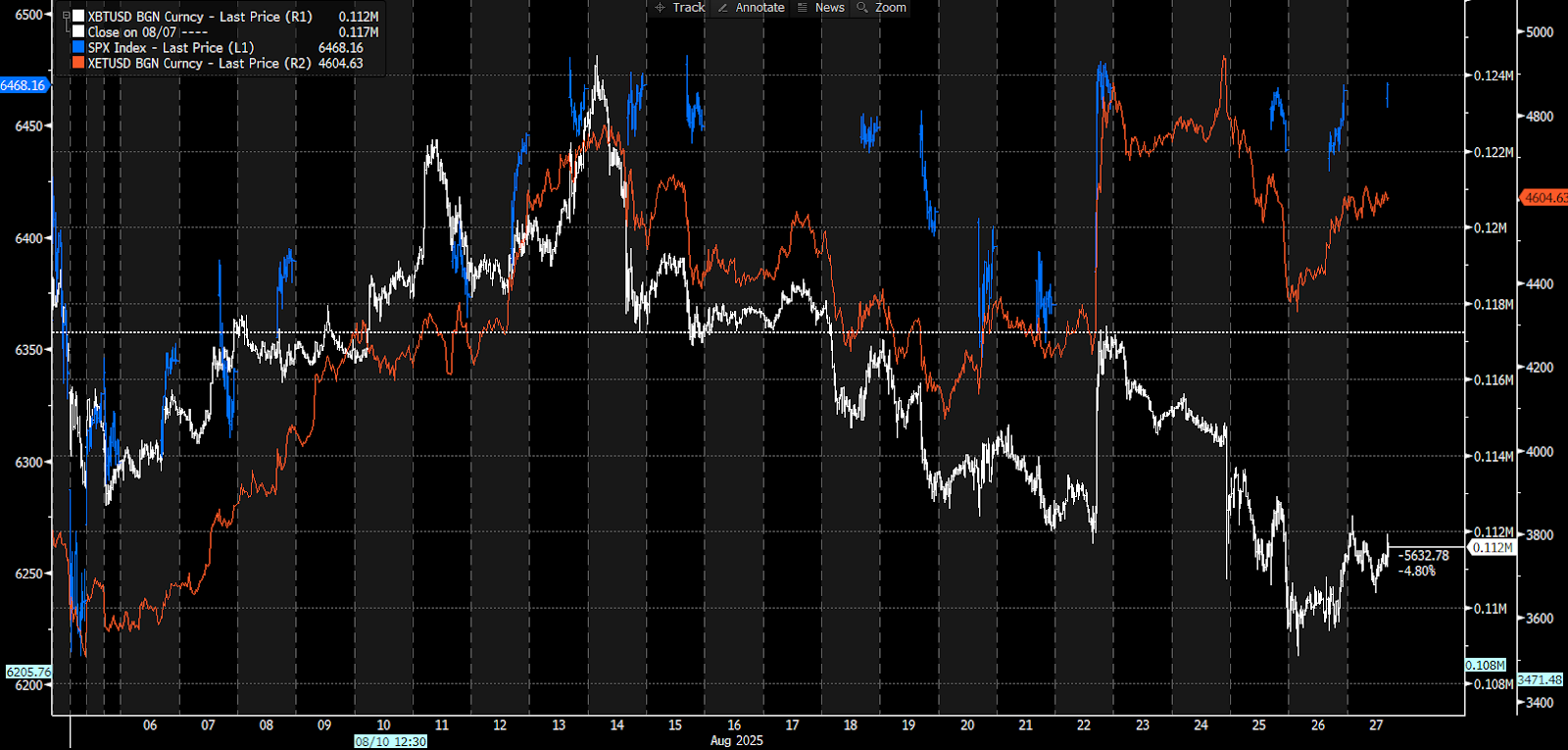

In fact, in the immediate aftermath of Powell’s speech, we saw “a rising tide lifts all boats" reaction from risk-on assets, as crypto markets and US equity markets alike surged higher. Altcoins led the way in those gains — Ether rallied more than 15% on the Friday reaching a new all-time high, before breaking to another ATH over the weekend. While BTC rallied from $112K to $117K, its move since then is more odd.

As traders took profit at record highs for Ether, its spot price pulled back. However, at the time of this writing, ETH is still significantly higher than its pre-Jackson Hole levels and only 6% below the ATH it broke following Powell’s speech. BTC, on the other hand, has not only failed to recover to the $117K level it rallied to but also is still below its pre-Jackson Hole level.

Divergences are also apparent in Spot ETF inflows between both assets. Over the course of August so far, Spot ETH ETFs have purchased $3.6B worth of Ether, while Spot BTC ETFs have sold -$882.8M of bitcoins — potentially evidence of a rotation of capital that we covered in more detail here.

This stands out to us because the bearishness in BTC is not reflected in the wider altcoin market or in ETH, and neither is it part of a wider macro bearish positioning — the S&P 500 has traded rangebound at the highs of its post-Jackson Hole move. Even if we look at positioning in options markets for the S&P 500, we find a positive skew towards call options (albeit falling slightly post JH).

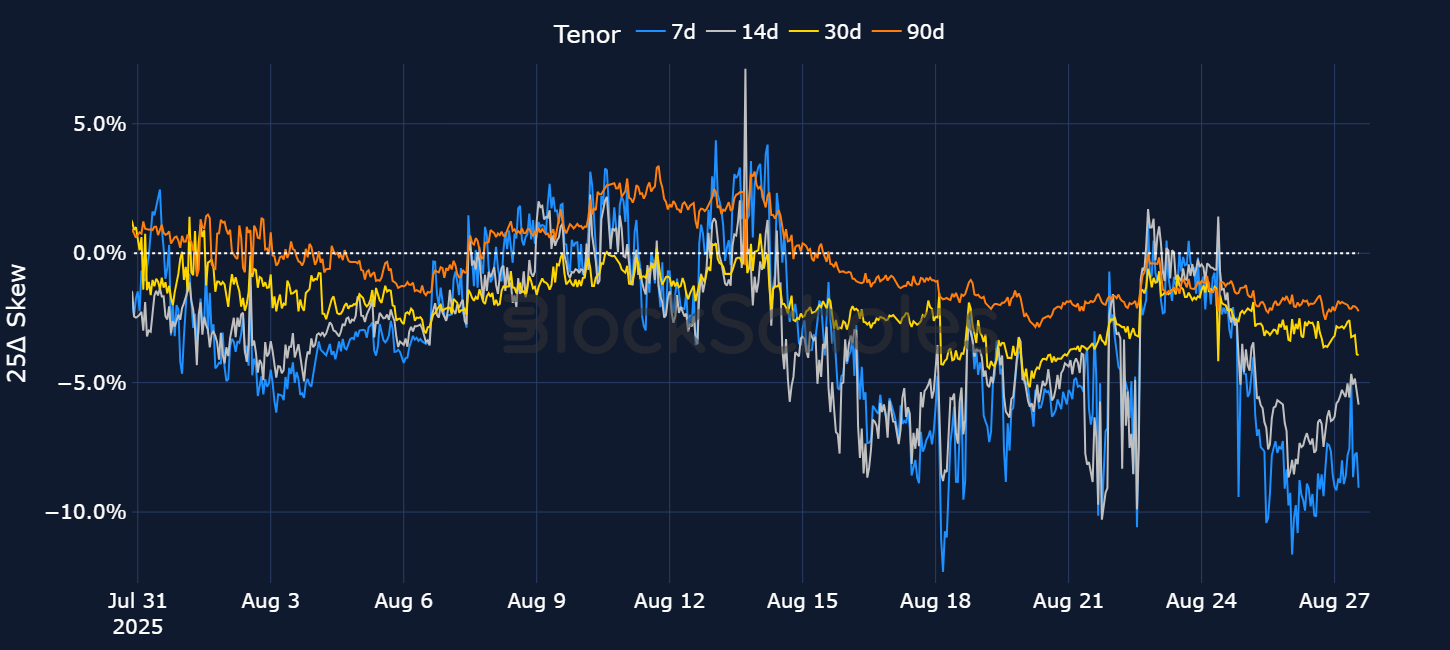

On the other hand, the 25-delta skew for BTC options across the term structure of volatility remains tilted towards OTM puts. That suggests that traders are paying a significant premium for protection against a further downside blowup both in the short-and mid-to-long term.

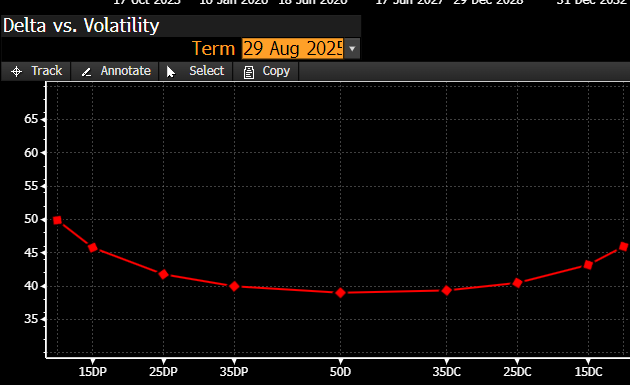

The skew towards puts is also apparent in positioning in BlackRock’s IBIT’s options. IV is significantly higher in OTM put options for Aug 29, 2025 contracts than in calls of equivalent moneyness.

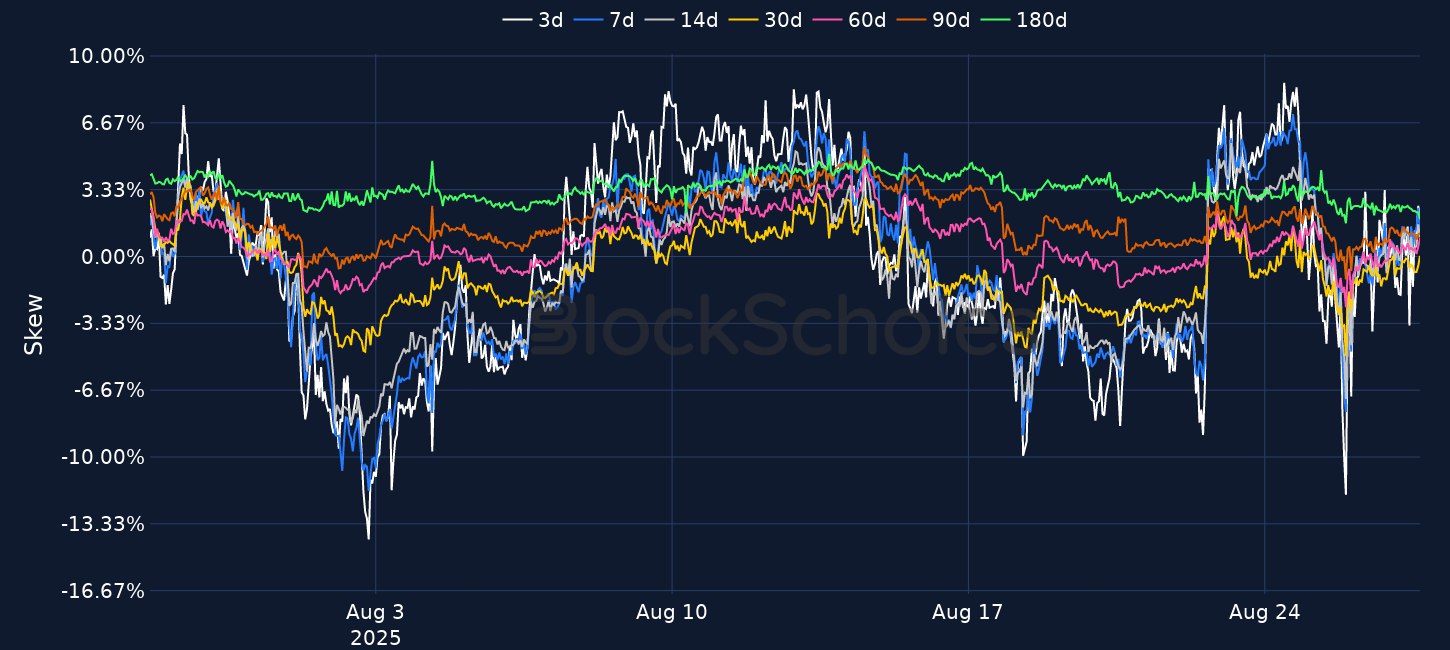

We can contrast that to the skew in options premiums across the term structure for ETH. Short-tenor ETH skew has shifted from a -7% skew towards put options during the dip below $4,400, however is now once more tilted slightly towards out-of-the-money call options.

The question remains: Is BTC simply lagging behind the rest of the market currently or is there a fundamental reason behind BTC’s isolated bearishness relative to the rest of the market?