For the first time since 1993 two FOMC members dissented the decision of the committee to keep the benchmark federal funds rate unchanged at 4.25%-4.50%. Chair Powell doused expectations of a September rate cut, while highlighting on several occasions that the “Labour market looks solid” though “inflation is above target”. Markets took the presser as a hawkish one, with expectations of a September pause increasing, the 2-year treasury rising 7bps and the S&P 500 dropping more than 0.5%. BTC temporarily followed risk-on assets lower, though has now recovered back above $118K. Funding rates for ETH turned negative for the first time since late June 2025. On the other hand, President Trump announced a number of tariff developments, while JP Morgan and Coinbase announced a strategic partnership.

“The Treasury secretary has said recently that it would be confusing for the markets if you stayed on as a governor after your term as chair ends. And I was wondering if you had any update for us on a decision on that front?”

“Sorry. I do not have any update for you.”

That sharp dismissiveness and blunt response at the end of yesterday’s FOMC press conference from Chair Jerome Powell was perhaps a fitting end to the conference itself.

Powell said that “There are many, many uncertainties left to resolve” and “a long way to go” to fully understand the impact of tariffs, as the FOMC voted to keep rates paused at 4.25%-4.50% for the fifth consecutive meeting.

Powell also doused expectations of a September rate cut on multiple occasions, stating that interest rate policy is currently “modestly restrictive”.

Interest-rate futures now indicate a 57% probability of a pause in September, having assigned a 75.4% probability of a cut only a month earlier.

It was also the first FOMC meeting since 1993 where two Fed officials had voted against the committee’s decision. Governors Christopher Waller and Michelle Bowman had both been vocal for a quarter-point reduction in July in the run-up to the meeting.

When asked specifically about a September rate cut Powell responded “We have made no decisions about September” and that “it seems to me and to almost the whole committee that the economy is not performing as though restrictive policy is holding it back inappropriately and modestly restrictive policy seems appropriate”.

Powell said separately “I just think we’re going to need to see the data. And it can go in many different directions, the inflation data and the employment data”.

He mentioned that his framework for deciding when it will be right to eventually resume the cutting cycle is when “the risks to the two goals” are “fully in balance”. When that is the case, it “would imply that you should move toward a more neutral stance of policy. This is the special situation we’re in, which is we have two-sided risk, risk to both of our goals”.

While saying that the “next steps we take are likely to be in that direction”, i.e., cutting towards a neutral rate of interest, Powell highlighted several times that the “Labour market looks solid”, while “inflation is above target”:

“If you look at the labour market, what you see is, by many, many statistics, the labour market is kind of still in balance.”

“You do not see a weakening in the labour market.”

“We do see downside risk in the labour market.”

With regards to tariffs, Powell said “what we see now is basically the very beginnings of whatever the effects turn out to be on goods inflation”. Whether that effect is higher or lower than forecasters' expectations, Powell said one thing is certain: “They’re not going to be zero. Consumers will pay some of this”.

“Companies will raise prices when and as they can” – the Chair highlighted the case of washing machines and dryers in President Trump’s first term in office. While the latter was not tariffed, the price of dryers went up along with washing machines, which were tariffed.

Overall, markets digested Powell’s conference as one that was more on the hawkish scale; and the evidence is in the response from various different assets.

As mentioned, traders have pared back expectations of a rate cut, the US 2s10s yield curve flattened as the 2-year treasury yield rose 7bps, the dollar surged higher and the S&P 500 fell more than 0.5% (though clawed back some of those losses to close 0.1% lower on the day).

US treasuries had begun falling even earlier than Powell’s presser as inflation-adjusted GDP in the US grew at an annualised rate of 3% in Q2, above economist expectations and the 0.5% contraction in Q1.

However, while the pace in Q2 was strong, overall for the first half of the year, economic growth has averaged 1.25%, a percentage point cooler than the pace in 2024.

Consumer spending, which accounts for two-thirds of GDP, advanced 1.4%, far lower than the pace of growth seen in previous quarters, matching Powell’s comments that “consumer spending had been very, very strong for the last couple of years and repeatedly forecasters, not just us, had been forecasting it would slow down and now maybe it finally has”.

BTC followed suit with US equities. It fell vertically lower from $117K to $116K before similarly posing a rebound. That rebound has extended into today and the largest cryptocurrency by market cap is trading back at the same levels pre-FOMC meeting ($118K).

The rest of the crypto market has recovered similarly, with ETH trading just shy of $3,900, having fallen as low as $3,600.

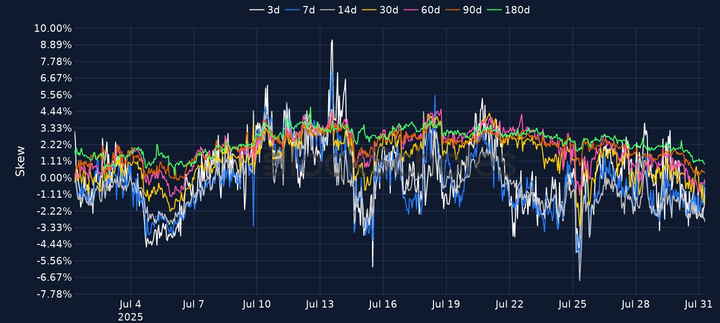

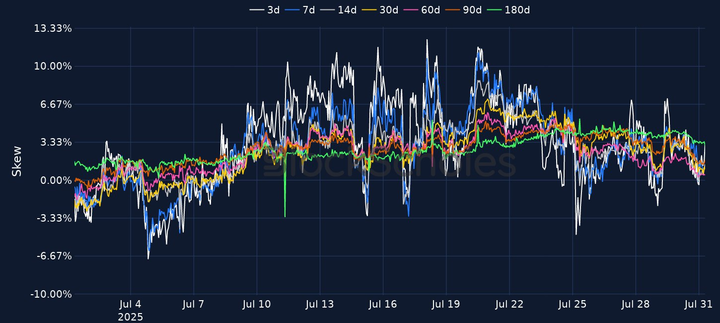

At-the-money implied volatility for both BTC and ETH options has declined, with 7-day BTC options now trading with an implied volatility back below 30%, while put-call skew is tilted towards OTM put options for all options with a tenor of 60 days or less. Only 90 and 180 day options currently have a volatility premium assigned to OTM calls, though that premium is also less than a full percentage point.

Both assets have seen a drop in their futures implied spot yields and ETH funding rates have turned negative for the first time since June 27, 2025.

Yesterday was also marked by multiple tariff developments from President Trump.

Starting Friday, the US president said he will impose a tariff of at least 25% on goods from India due to their tariffs on US goods being “among the highest in the world” and for being “Russia’s largest buyer of ENERGY”. Speaking at the White House he later said “We’ll see what happens”, opening the door for some more negotiation.

The president also signed an executive order which suspends the de minimis exemption, a law that had allowed for inbound goods into the US valued at up to $800 (per person, per day) to be exempt from any duties or taxes. That means these goods will now also be subject to tariffs and will likely have an outsized impact on online retailers that ship products directly to the US, such as Shein and Temu.

The White House referred to the exemption as “a catastrophic loophole used to, among other things, evade tariffs and funnel deadly synthetic opioids as well as other unsafe or below-market products” into the US.

Separately a trade deal was reached between the US and South Korea which will see goods from the region subject to a 15% tariff when entering the US and Trump delayed a 50% tariff that was due to be applied on goods from Brazil by an additional 7 days.

JP Morgan and Coinbase have announced yesterday a strategic partnership that will allow for JPM Chase customers to “seamlessly link” their Chase accounts to Coinbase, providing another avenue to enter crypto from the rails of traditional finance. Chase customers will also be able to purchase cryptocurrencies on the Coinbase app via their Chase credit cards later in the year.

Nasdaq-listed Fundamental Global, now rebranded to FG Nexus, have announced the creation of a $200M Ethereum treasury reserve funded via private placement by issuing 40M prefunded warrants at $5 each.

Key investors include Galaxy Digital who will also manage treasury operations and yield strategies and Kraken who will provide staking and blockchain infrastructure support.

Ether generation company, The Ether Machine has purchased nearly 15,000 ETH at $3,809.97 USD, totaling approximately $56.9M, as part of its long-term accumulation strategy. This brings the total ETH acquired to 334,757.

The purchase was funded by The Ether Reserve LLC using a portion of the $97M in cash proceeds from its previously announced private placement. Additionally, they have committed up to $407M in remaining capital for further ETH acquisitions, with more purchases to be announced in the coming days.

“The Treasury secretary has said recently that it would be confusing for the markets if you stayed on as a governor after your term as chair ends. And I was wondering if you had any update for us on a decision on that front?”

“Sorry. I do not have any update for you.”

That sharp dismissiveness and blunt response at the end of yesterday’s FOMC press conference from Chair Jerome Powell was perhaps a fitting end to the conference itself.

Powell said that “There are many, many uncertainties left to resolve” and “a long way to go” to fully understand the impact of tariffs, as the FOMC voted to keep rates paused at 4.25%-4.50% for the fifth consecutive meeting.

Powell also doused expectations of a September rate cut on multiple occasions, stating that interest rate policy is currently “modestly restrictive”.

Interest-rate futures now indicate a 57% probability of a pause in September, having assigned a 75.4% probability of a cut only a month earlier.

It was also the first FOMC meeting since 1993 where two Fed officials had voted against the committee’s decision. Governors Christopher Waller and Michelle Bowman had both been vocal for a quarter-point reduction in July in the run-up to the meeting.

When asked specifically about a September rate cut Powell responded “We have made no decisions about September” and that “it seems to me and to almost the whole committee that the economy is not performing as though restrictive policy is holding it back inappropriately and modestly restrictive policy seems appropriate”.

Powell said separately “I just think we’re going to need to see the data. And it can go in many different directions, the inflation data and the employment data”.

He mentioned that his framework for deciding when it will be right to eventually resume the cutting cycle is when “the risks to the two goals” are “fully in balance”. When that is the case, it “would imply that you should move toward a more neutral stance of policy. This is the special situation we’re in, which is we have two-sided risk, risk to both of our goals”.

While saying that the “next steps we take are likely to be in that direction”, i.e., cutting towards a neutral rate of interest, Powell highlighted several times that the “Labour market looks solid”, while “inflation is above target”:

“If you look at the labour market, what you see is, by many, many statistics, the labour market is kind of still in balance.”

Don't miss what's next

Upgrade your Block Scholes account to unlock this article and other exclusive insights

“The Treasury secretary has said recently that it would be confusing for the markets if you stayed on as a governor after your term as chair ends. And I was wondering if you had any update for us on a decision on that front?”

“Sorry. I do not have any update for you.”

That sharp dismissiveness and blunt response at the end of yesterday’s FOMC press conference from Chair Jerome Powell was perhaps a fitting end to the conference itself.

Powell said that “There are many, many uncertainties left to resolve” and “a long way to go” to fully understand the impact of tariffs, as the FOMC voted to keep rates paused at 4.25%-4.50% for the fifth consecutive meeting.

Powell also doused expectations of a September rate cut on multiple occasions, stating that interest rate policy is currently “modestly restrictive”.

Interest-rate futures now indicate a 57% probability of a pause in September, having assigned a 75.4% probability of a cut only a month earlier.

It was also the first FOMC meeting since 1993 where two Fed officials had voted against the committee’s decision. Governors Christopher Waller and Michelle Bowman had both been vocal for a quarter-point reduction in July in the run-up to the meeting.

When asked specifically about a September rate cut Powell responded “We have made no decisions about September” and that “it seems to me and to almost the whole committee that the economy is not performing as though restrictive policy is holding it back inappropriately and modestly restrictive policy seems appropriate”.

Powell said separately “I just think we’re going to need to see the data. And it can go in many different directions, the inflation data and the employment data”.

He mentioned that his framework for deciding when it will be right to eventually resume the cutting cycle is when “the risks to the two goals” are “fully in balance”. When that is the case, it “would imply that you should move toward a more neutral stance of policy. This is the special situation we’re in, which is we have two-sided risk, risk to both of our goals”.

While saying that the “next steps we take are likely to be in that direction”, i.e., cutting towards a neutral rate of interest, Powell highlighted several times that the “Labour market looks solid”, while “inflation is above target”:

“If you look at the labour market, what you see is, by many, many statistics, the labour market is kind of still in balance.”

Don't miss what's next

Upgrade your Block Scholes account to unlock this article and other exclusive insights

Premium

$30/mo

Access previous and future reports, market insights & deep dives.

A selloff in chipmakers, a sixth consecutive night of US strikes on Iran, and two Fed speakers setting out a more hawkish view all weighed on risk: the S&P 500 closed down 0.51% and the Nasdaq-100 fell 1.62%, while the Philadelphia Semiconductor index plunged 4.29%, taking its one-month loss beyond 10%. BTC was last at $62.8K and ETH at $1.83K, with Brent near $85 and on track for a 12% weekly gain as shipping halted in the Strait of Hormuz. Ondo Finance and SBI Group partnered to bring tokenized Japanese equities onchain, T. Rowe Price launched the actively managed TKNZ spot crypto ETF, Citadel Securities invested $400M in Crypto.com at a $20B valuation, and Multicoin backed Hyperliquid-based Trasia Labs.