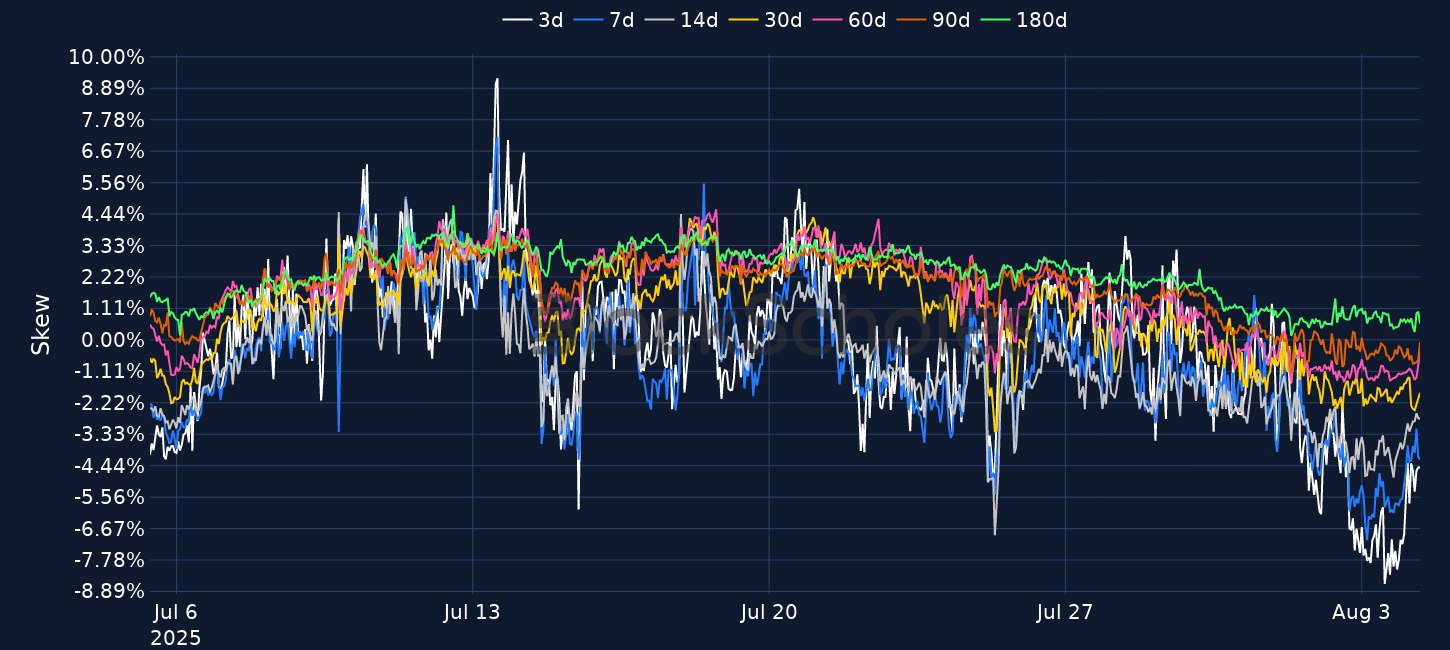

The latest US Nonfarm payrolls report showed the largest downward revision to jobs added by the US economy since the onset of the Covid pandemic. July jobs data came in weaker than expected, however the headline was an overstating of 258,000 jobs between May and June 2025. That has pushed markets to once more price in more than two rate cuts before the end of the year, while also sending crypto and US equity markets sharply lower. BTC fell to a low of $112K over the weekend while Spot BTC ETFs saw their second-largest single-day of outflows since launch in January 2024 (-$812M). Both BTC and ETH short-tenor volatility smiles are firmly skewed towards OTM put options. Meanwhile, Federal Reserve members continue to diverge on the path of monetary policy. Governor Waller stated that “the wait and see approach is overly cautious”, while Cleveland President, Beth Hammack stated the labour market is still "healthy" and "well in balance".

Last Friday was a stark reminder that President Trump’s volleyball style of tariff policymaking is not the only driver of US equity markets, bond markets, and cryptocurrency markets.

The latest Nonfarm payrolls report showed the US economy undershot estimates for the number of jobs added, which increased by 73,000 in July against expectations of 104,000, while the unemployment rate rose as expected to 4.2%. However it wasn’t the numbers for July that subsequently sent markets on a nose dive.

The report also showed the steepest downward revisions to US jobs since the onset of the Covid pandemic.

The Bureau of Labor Statistics revised down their estimates of nonfarm payrolls by 125,000 in May and 133,000 in June (a whopping 258,000 downward revision).

That meant that the number of jobs added in May came in at only 19,000 from the initially reported 144,000, while jobs added in June clocked in at a mere 14,000, down from an initial estimate of 147,000.

Those revisions also mean the average three-month gain in payrolls has dropped markedly from 150,000 to 35,000 — shedding a very different outlook on a labour market which even as recently as last Wednesday, Chair Powell defined to be “very solid”.

While the overstatement of jobs added by the economy in May and June was already a sign of growing cracks in the labour market, another sign of cracks was the concentration in where jobs were added in July.

According to the report, “in July, health care added 55,000 jobs, above the average monthly gain of 42,000 over the prior 12 months. Over the month, job gains occurred in ambulatory health care services (+34,000) and hospitals (+16,000). Social assistance employment continued to trend up in July (+18,000), reflecting continued job growth in individual and family services (+21,000).”

Therefore, job creation was narrowly based in healthcare and social assistance which made up nearly 95% of total jobs added. Federal jobs declined for another month by 12,000 jobs.

Additionally, the average duration of the number of weeks of unemployment rose to 24.1, the highest level since April 2022, while the number of individuals out of work for more than 27 weeks rose to 1.82M, the most since December 2021.

Markets reacted sharply. Treasuries surged as the two-year treasury yield fell more than 25bps. Market implied odds of a September rate cut shot up to 88%, from less than 40% only a day earlier, while markets also now price in 2.3 rate cuts before the end of the year (a 100% probability of two 25bps cuts and a 31.2% probability of a third).

The long end of the yield curve also saw a large, though slightly less dramatic move down as ten-year treasury yields fell 15bps.

The S&P 500 Index extended a four day retreat, falling as much as 1.6%.

Crypto markets were already in a downtrend since Thursday last week. While BTC very briefly rose on the release of the NFP report, the opening of US equity markets saw it continue that downward trend, falling from $116K to $114K. Then, over the weekend, it dropped to even lower levels, touching a local bottom of $112K.

Equally, Since July 31, ETH has fallen from $3,800 to just under $3,400, an 8.5% decline over the past week. After the entirety of July saw only one day of net outflows from Spot ETH ETFs ($1.9M of outflows), August has begun with an outflow of $152.3M.

BTC Spot ETFs saw even larger outflows on the first day of August. Collectively, the ETF products saw outflows of -$812.3M – their second-largest day of outflows since launch in January 2024.

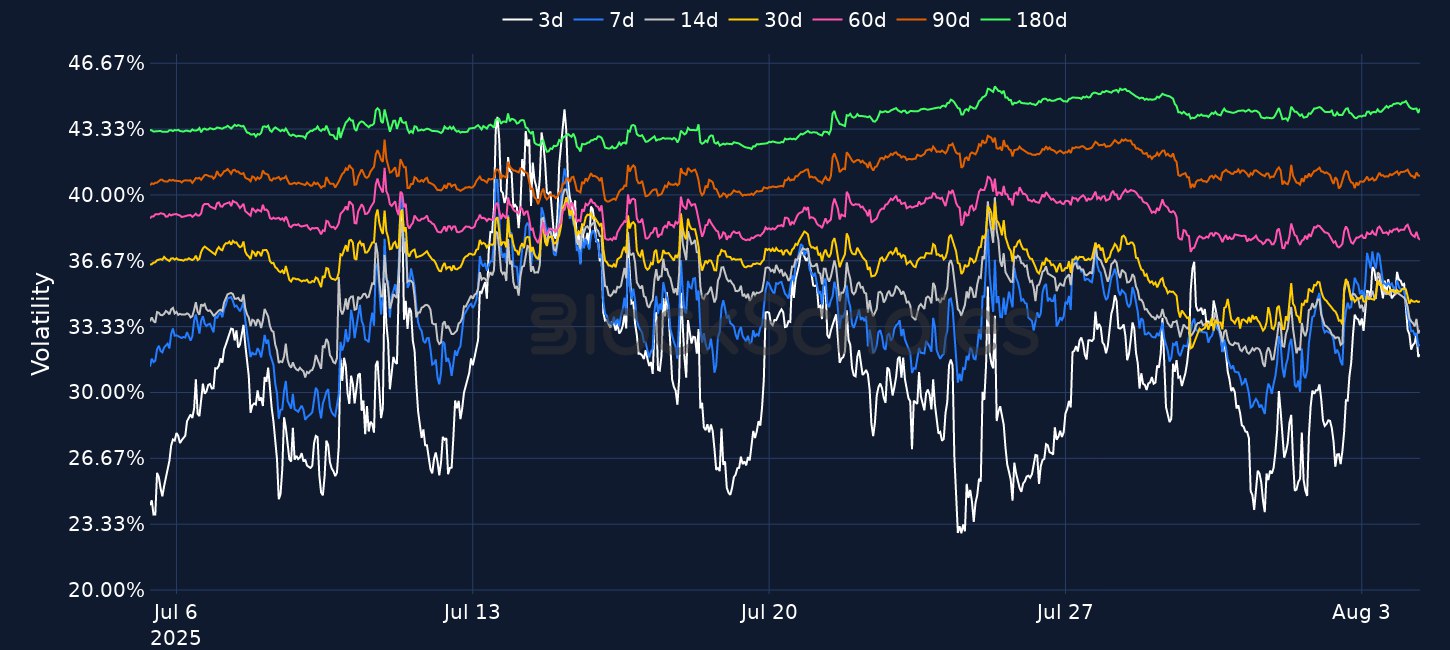

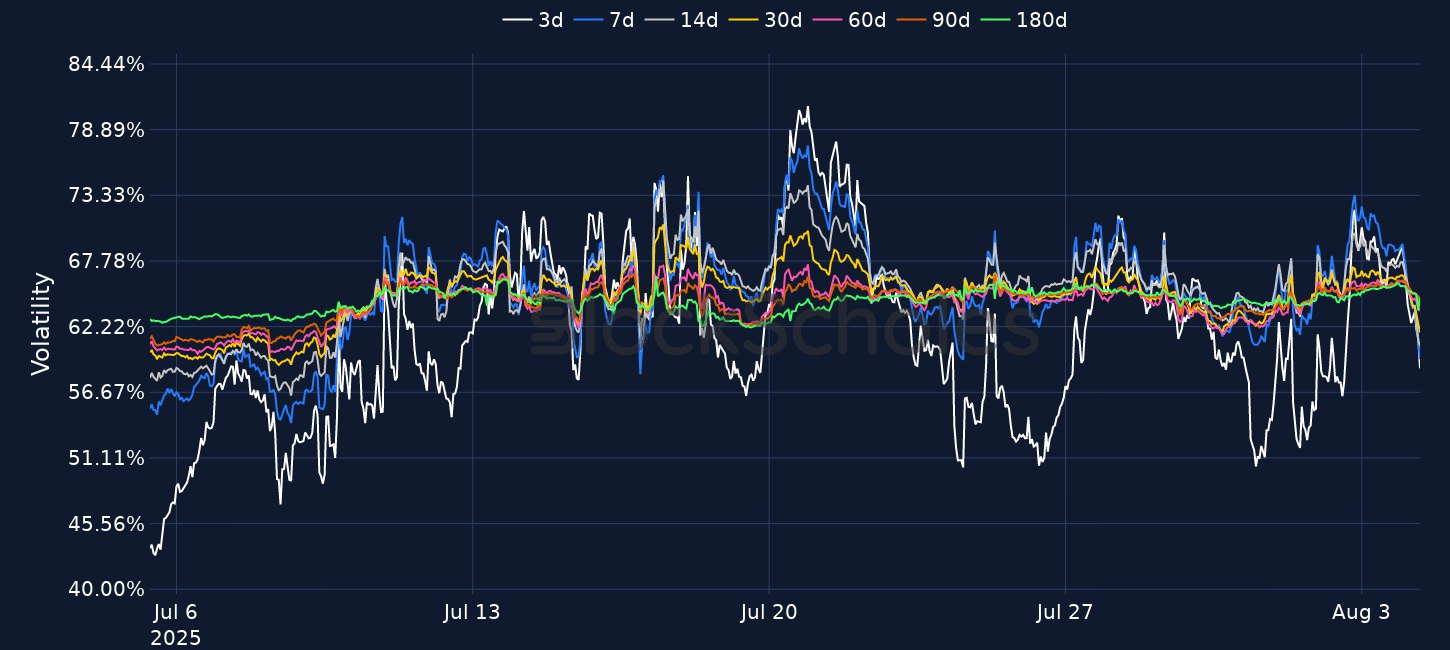

BTC and ETH funding rates, which were already below 0%, fell slightly lower over the weekend, with BTC rates reaching -0.018% on an eight-hourly basis. ETH’s term structure of volatility has flattened, with outright volatility levels between 63% and 65%.

Both asset’s short-tenor volatility smiles are now skewed towards puts. For BTC, 7-day options have a put-call skew of -3.85% while similar dated ETH options have a skew of -4.39% – that means puts are priced at a volatility premium to OTM call options.

As did financial markets, President Trump had an equally swift response to the payrolls report.

His response? To shoot the messenger — in a social media post the President stated “We need accurate Jobs Numbers. I have directed my Team to fire this Biden Political Appointee, IMMEDIATELY. She will be replaced with someone much more competent and qualified”. Consequently, later in the day, the BLS Commissioner, Erika McEntarfer was fired.

Unsurprisingly the anemic July report has called into question the Fed’s wait-and-see approach – and the response from Fed policymakers has varied.

Speaking on Bloomberg TV after the release, Cleveland Fed President Beth Hammack said “it was a disappointing report to be sure, but the confluence of data still shows “a healthy labour market that’s still well in balance but with some disappointing signs that we should watch very carefully”.

According to the Cleveland Fed President, “Having the headline numbers come down makes sense given what we’ve seen happening on the immigration side and the headline number on unemployment, which is the most reliable indicator we have, is still within that 4.1 to 4.3 range that it’s been at for the past year”.

To Hammack, the Fed is seeing more pressure on the inflation side of its mandate — “That’s where our mess has been bigger and has been lasting longer. We haven’t hit on inflation in four and a half years” and “Right now we’re missing by much more on the inflation side than we’re missing on the employment side”.

Regarding tariffs, she said “The $30B a month in tariff revenues is being paid by someone… We’re hearing from the businesses we talk to that they can't absorb those costs anymore and they will start pushing that out into prices to consumers”.

Prior to the release of the jobs report, the two dissenting FOMC members issued statements explaining their reason for dissent. Governor Waller stated the data argues that “monetary policy should now be close to neutral, not restrictive” and “while the labour market looks fine on the surface, once we account for expected data revisions, private-sector payroll growth is near stall speed” — something we saw later in the report. For that reason he believes “the wait and see approach is overly cautious”.

“It may take several months for clarity on the ultimate impact tariffs have on the economy” – months that Waller believes the Fed does not have. He added that “it is possible that the labour market falters before that clarity is obtained—if it ever is obtained. When labor markets turn, they often turn fast.”

Interestingly, the longest inter meeting period between FOMC meetings is the July and September period. That means the Fed will get two more inflation reports and one more employment report before meeting again. We can recall it was in this inter meeting period last year when a weak July jobs report led the Fed to cut rates by a larger 50 bps in September.

Bitcoin Mining Difficulty continues to reach new all time highs with the current difficulty set at over 127T. This represents an approximately 40% increase in difficulty in one year as more computing power is added to the network.

Sharplink has purchased an additional 15.8K ETH worth over $50M, this weekend according to onchain data. This brings their total holdings to around 480K ETH, worth around $1.65B.

Japanese Bitcoin treasury firm Metaplanet has purchased an additional 463 BTC at an average price of $115,895, bringing their total holdings to 17,595 BTC, worth around $1.78B, acquired at an average of $101,422 per BTC.

This follows Metaplanet’s Friday announcement that they have filed to raise up to ¥555B ($3.7B) with a two-year shelf registration, via Class A and B Perpetual Preferred Stock to fund further BTC purchases.

Last Friday was a stark reminder that President Trump’s volleyball style of tariff policymaking is not the only driver of US equity markets, bond markets, and cryptocurrency markets.

The latest Nonfarm payrolls report showed the US economy undershot estimates for the number of jobs added, which increased by 73,000 in July against expectations of 104,000, while the unemployment rate rose as expected to 4.2%. However it wasn’t the numbers for July that subsequently sent markets on a nose dive.

The report also showed the steepest downward revisions to US jobs since the onset of the Covid pandemic.

The Bureau of Labor Statistics revised down their estimates of nonfarm payrolls by 125,000 in May and 133,000 in June (a whopping 258,000 downward revision).

That meant that the number of jobs added in May came in at only 19,000 from the initially reported 144,000, while jobs added in June clocked in at a mere 14,000, down from an initial estimate of 147,000.

Those revisions also mean the average three-month gain in payrolls has dropped markedly from 150,000 to 35,000 — shedding a very different outlook on a labour market which even as recently as last Wednesday, Chair Powell defined to be “very solid”.

While the overstatement of jobs added by the economy in May and June was already a sign of growing cracks in the labour market, another sign of cracks was the concentration in where jobs were added in July.

According to the report, “in July, health care added 55,000 jobs, above the average monthly gain of 42,000 over the prior 12 months. Over the month, job gains occurred in ambulatory health care services (+34,000) and hospitals (+16,000). Social assistance employment continued to trend up in July (+18,000), reflecting continued job growth in individual and family services (+21,000).”

Therefore, job creation was narrowly based in healthcare and social assistance which made up nearly 95% of total jobs added. Federal jobs declined for another month by 12,000 jobs.

Additionally, the average duration of the number of weeks of unemployment rose to 24.1, the highest level since April 2022, while the number of individuals out of work for more than 27 weeks rose to 1.82M, the most since December 2021.

Markets reacted sharply. Treasuries surged as the two-year treasury yield fell more than 25bps. Market implied odds of a September rate cut shot up to 88%, from less than 40% only a day earlier, while markets also now price in 2.3 rate cuts before the end of the year (a 100% probability of two 25bps cuts and a 31.2% probability of a third).

The long end of the yield curve also saw a large, though slightly less dramatic move down as ten-year treasury yields fell 15bps.

Don't miss what's next

Upgrade your Block Scholes account to unlock this article and other exclusive insights

Last Friday was a stark reminder that President Trump’s volleyball style of tariff policymaking is not the only driver of US equity markets, bond markets, and cryptocurrency markets.

The latest Nonfarm payrolls report showed the US economy undershot estimates for the number of jobs added, which increased by 73,000 in July against expectations of 104,000, while the unemployment rate rose as expected to 4.2%. However it wasn’t the numbers for July that subsequently sent markets on a nose dive.

The report also showed the steepest downward revisions to US jobs since the onset of the Covid pandemic.

The Bureau of Labor Statistics revised down their estimates of nonfarm payrolls by 125,000 in May and 133,000 in June (a whopping 258,000 downward revision).

That meant that the number of jobs added in May came in at only 19,000 from the initially reported 144,000, while jobs added in June clocked in at a mere 14,000, down from an initial estimate of 147,000.

Those revisions also mean the average three-month gain in payrolls has dropped markedly from 150,000 to 35,000 — shedding a very different outlook on a labour market which even as recently as last Wednesday, Chair Powell defined to be “very solid”.

While the overstatement of jobs added by the economy in May and June was already a sign of growing cracks in the labour market, another sign of cracks was the concentration in where jobs were added in July.

According to the report, “in July, health care added 55,000 jobs, above the average monthly gain of 42,000 over the prior 12 months. Over the month, job gains occurred in ambulatory health care services (+34,000) and hospitals (+16,000). Social assistance employment continued to trend up in July (+18,000), reflecting continued job growth in individual and family services (+21,000).”

Therefore, job creation was narrowly based in healthcare and social assistance which made up nearly 95% of total jobs added. Federal jobs declined for another month by 12,000 jobs.

Additionally, the average duration of the number of weeks of unemployment rose to 24.1, the highest level since April 2022, while the number of individuals out of work for more than 27 weeks rose to 1.82M, the most since December 2021.

Markets reacted sharply. Treasuries surged as the two-year treasury yield fell more than 25bps. Market implied odds of a September rate cut shot up to 88%, from less than 40% only a day earlier, while markets also now price in 2.3 rate cuts before the end of the year (a 100% probability of two 25bps cuts and a 31.2% probability of a third).

The long end of the yield curve also saw a large, though slightly less dramatic move down as ten-year treasury yields fell 15bps.

Don't miss what's next

Upgrade your Block Scholes account to unlock this article and other exclusive insights

Premium

$30/mo

Access previous and future reports, market insights & deep dives.

A selloff in chipmakers, a sixth consecutive night of US strikes on Iran, and two Fed speakers setting out a more hawkish view all weighed on risk: the S&P 500 closed down 0.51% and the Nasdaq-100 fell 1.62%, while the Philadelphia Semiconductor index plunged 4.29%, taking its one-month loss beyond 10%. BTC was last at $62.8K and ETH at $1.83K, with Brent near $85 and on track for a 12% weekly gain as shipping halted in the Strait of Hormuz. Ondo Finance and SBI Group partnered to bring tokenized Japanese equities onchain, T. Rowe Price launched the actively managed TKNZ spot crypto ETF, Citadel Securities invested $400M in Crypto.com at a $20B valuation, and Multicoin backed Hyperliquid-based Trasia Labs.