Fed Chair Powell reiterated in his congressional testimony that the FOMC is in a wait-and-see mode as it expects higher tariff-induced inflation over the summer. While the Chair said he is "perfectly open" to a weaker-than-expected pass through from tariffs into inflation, given that "all forecasters are expecting" significant inflation soon, the FOMC "can’t just ignore that". US equities and crypto rallied on the fragile Middle East ceasefire, with the Nasdaq-100 hitting a new all-time high. BTC is up 1.6% to over $106K and ETH is just below $2,500 (+2.3%). 7-day ATM implied volatility for BTC has dropped to 32%, the lowest all month, even as realised volatility has jumped from 30% to 43% in the space of five days. ETH’s term structure has normalised, but short-tenor options still slightly favour OTM puts. BTC and ETH Spot ETFs saw inflows of $588.6M and $172M respectively.

During his testimony to congress at Capitol Hill yesterday, Federal Reserve Chair Powell repeated some of the points made in his FOMC presser last week: that the central bank still needs time to assess whether tariffs will drive inflation higher; and, for that reason, the Fed is on wait-and-see.

On multiple occasions, Powell stressed that the FOMC expects higher inflation:

“If you just look in the rearview mirror and just look at the existing data that we’ve seen, you can make a good argument that that would call for us to be at a neutral level, which would be a couple of cuts, maybe more kind of thing. The reason we’re not is the forecast by all professional forecasters that I know on the outside and the Fed do expect a meaningful increase in inflation over the course of this year”.

“We hadn’t expected inflation to move up much. We do expect it to move in the summer and if we see it not happening, we’ll learn from that”.

“We do expect tariff inflation to show up more, but I want to be honest, we really don’t know how much of that’s going to be passed through to the consumers, we just don’t know. It could be lower than we expect, it could be higher. We have to wait and see which is kind of what we’re doing”.

“If you just look at the basic data and don’t look at the forecast, we would have continued cutting. The difference of course is, at this time, all forecasters are expecting pretty soon that some significant inflation will show up from tariffs. We can’t just ignore that – we’re just saying let’s wait and see more. You will have noticed a substantial majority of the committee has written down rate cuts in the remaining four meetings this year”.

That expectation of higher inflation warrants the FOMC’s patient approach – something aided by a “still strong” labour market. Powell made it clear that if the FOMC did see weakness in the labour market, “that would change things”.

The Chair also acknowledged that the committee could be wrong on their views of inflation:

“I think many paths are possible here. We could see inflation come in not as strong as we expect and if that were the case that would tend to suggest cutting sooner. We could see the labour market weakening and that would also suggest cutting sooner”.

“There aren’t historical experiences we can consult here really. It may turn out that the pass through is less or more than we think. As we go through the summer we should start seeing this [inflation], and if we don’t, we’re perfectly open to the idea that the pass through will be less than we think, and if so, that will matter for our policy.”

When asked directly about a July rate cut, Powell responded “if it turns out that inflation pressures do remain contained, then we will get to a place where we cut rates, sooner rather than later. But I wouldn't want to point to a particular meeting, I don’t think we need to be in any rush, because the economy is still strong, the labour market is still strong”.

Interest rate swaps markets are currently pricing in two full rate cuts by the end of the year, with the likelihood of the initial move beginning in September much higher than in July. Still, bets on a July move are not completely priced out despite Powell, at least partially, pouring some cold water over a summer rate cut in his testimony. According to CME’s FedWatch, the probability of a July cut rose above 20% yesterday, from 12.5% last week.

Bullish momentum extended over both US equities and crypto markets amid the albeit fragile ceasefire in the Middle East. The Nasdaq-100 rallied 1.5% to reach a new record all-time high – the first since February. From the April 8 bottom, following Trump’s Liberation Day tariffs, the NDX is now up 29.8%.

WTI crude oil prices continued their plunge down, now trading around $65 per barrel, a more than 15% drop from only two days ago.

That breathing space from easing tensions has supported BTC and altcoins too – over the past 24 hours, Bitcoin is up 1.6%, trading above $106K while ETH trades slightly short of $2500 (+2.3%).

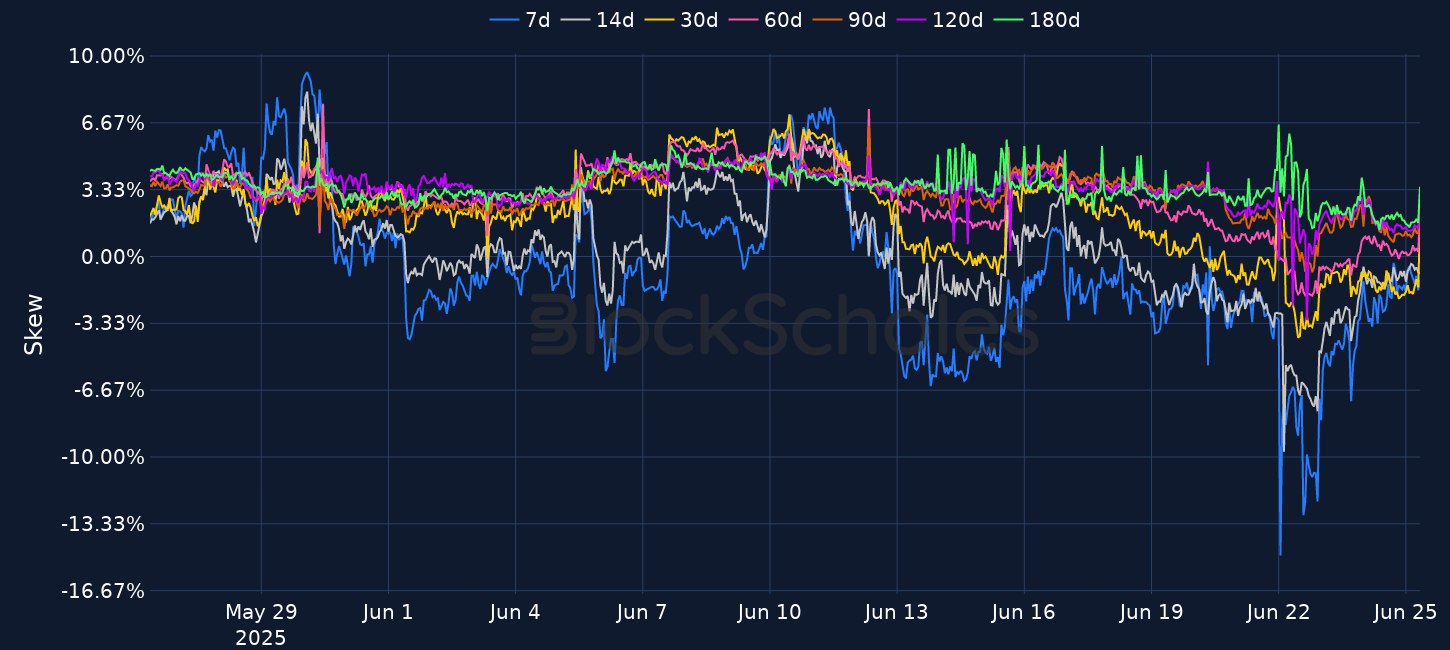

At-the-money implied volatility for BTC options has been trending lower, hitting its lowest level of the month at 32% for 7-day expiries. Interestingly, the steady chop down in implied volatility has occurred as 7-day realized volatility has moved up from 30% only last Friday to 43% currently (see that in Charts of the Day).

For Ethereum, we now see a resolution in its term structure inversion – 7-day ETH options trade with a slight 3% discount to their 180-day counterparts, however its volatility smile is skewed less towards OTM calls compared to BTC, with the 7- and 14-day expiries actually still favouring OTM puts.

US Spot BTC ETFs added $588.6M yesterday, continuing Monday’s net inflows of $350.6M. ETH ETFs were positive too, adding $172M across the same period.

Net inflows to both BTC and ETH ETFs have accelerated strongly since April 21st, adding an average of $28.9M and $191.2M per day respectively since that date. The pace of ETH accumulation has increased further since the SEC’s clarification that staking was not a securities transaction boosted chances of offering a yield – in line with the increase in ETH staked on the Beacon chain.

Bank of Korea Deputy Governor Ryoo Sangdai reported that he wants banks to take the lead in issuing a won-denominated stablecoin. Speaking at a press briefing, Ryoo said stablecoin issuance should begin with regulated commercial banks to provide a safety net and minimize market risk.

Despite the support, the Bank of Korea still remains cautious. Ryoo warned that introducing stablecoins could trigger faster capital outflows and potentially undermine Korea’s long lasting policies on foreign exchange control.

China based Aurora Mobile (NASDAQ: JG), has announced its Board of Directors approval to invest up to 20% of its cash reserves in cryptocurrencies and digital assets, including Bitcoin, Ethereum, Solana, SUI, and others.

SharpLink Gaming (NASDAQ: SBET) has added 12,207 ETH between June 16 and 20, at an average price of $2,513 per token, bringing its treasury holding to 188,478 ETH. This makes SharpLink Gaming the second-largest corporate holder of ETH after the Ethereum Foundation. From staking all of its ETH, SharpLink Gaming have received 120 ETH (approximately $300k) in rewards since June 2.

During his testimony to congress at Capitol Hill yesterday, Federal Reserve Chair Powell repeated some of the points made in his FOMC presser last week: that the central bank still needs time to assess whether tariffs will drive inflation higher; and, for that reason, the Fed is on wait-and-see.

On multiple occasions, Powell stressed that the FOMC expects higher inflation:

“If you just look in the rearview mirror and just look at the existing data that we’ve seen, you can make a good argument that that would call for us to be at a neutral level, which would be a couple of cuts, maybe more kind of thing. The reason we’re not is the forecast by all professional forecasters that I know on the outside and the Fed do expect a meaningful increase in inflation over the course of this year”.

“We hadn’t expected inflation to move up much. We do expect it to move in the summer and if we see it not happening, we’ll learn from that”.

“We do expect tariff inflation to show up more, but I want to be honest, we really don’t know how much of that’s going to be passed through to the consumers, we just don’t know. It could be lower than we expect, it could be higher. We have to wait and see which is kind of what we’re doing”.

“If you just look at the basic data and don’t look at the forecast, we would have continued cutting. The difference of course is, at this time, all forecasters are expecting pretty soon that some significant inflation will show up from tariffs. We can’t just ignore that – we’re just saying let’s wait and see more. You will have noticed a substantial majority of the committee has written down rate cuts in the remaining four meetings this year”.

That expectation of higher inflation warrants the FOMC’s patient approach – something aided by a “still strong” labour market. Powell made it clear that if the FOMC did see weakness in the labour market, “that would change things”.

The Chair also acknowledged that the committee could be wrong on their views of inflation:

“I think many paths are possible here. We could see inflation come in not as strong as we expect and if that were the case that would tend to suggest cutting sooner. We could see the labour market weakening and that would also suggest cutting sooner”.

“There aren’t historical experiences we can consult here really. It may turn out that the pass through is less or more than we think. As we go through the summer we should start seeing this [inflation], and if we don’t, we’re perfectly open to the idea that the pass through will be less than we think, and if so, that will matter for our policy.”

Don't miss what's next

Upgrade your Block Scholes account to unlock this article and other exclusive insights

During his testimony to congress at Capitol Hill yesterday, Federal Reserve Chair Powell repeated some of the points made in his FOMC presser last week: that the central bank still needs time to assess whether tariffs will drive inflation higher; and, for that reason, the Fed is on wait-and-see.

On multiple occasions, Powell stressed that the FOMC expects higher inflation:

“If you just look in the rearview mirror and just look at the existing data that we’ve seen, you can make a good argument that that would call for us to be at a neutral level, which would be a couple of cuts, maybe more kind of thing. The reason we’re not is the forecast by all professional forecasters that I know on the outside and the Fed do expect a meaningful increase in inflation over the course of this year”.

“We hadn’t expected inflation to move up much. We do expect it to move in the summer and if we see it not happening, we’ll learn from that”.

“We do expect tariff inflation to show up more, but I want to be honest, we really don’t know how much of that’s going to be passed through to the consumers, we just don’t know. It could be lower than we expect, it could be higher. We have to wait and see which is kind of what we’re doing”.

“If you just look at the basic data and don’t look at the forecast, we would have continued cutting. The difference of course is, at this time, all forecasters are expecting pretty soon that some significant inflation will show up from tariffs. We can’t just ignore that – we’re just saying let’s wait and see more. You will have noticed a substantial majority of the committee has written down rate cuts in the remaining four meetings this year”.

That expectation of higher inflation warrants the FOMC’s patient approach – something aided by a “still strong” labour market. Powell made it clear that if the FOMC did see weakness in the labour market, “that would change things”.

The Chair also acknowledged that the committee could be wrong on their views of inflation:

“I think many paths are possible here. We could see inflation come in not as strong as we expect and if that were the case that would tend to suggest cutting sooner. We could see the labour market weakening and that would also suggest cutting sooner”.

“There aren’t historical experiences we can consult here really. It may turn out that the pass through is less or more than we think. As we go through the summer we should start seeing this [inflation], and if we don’t, we’re perfectly open to the idea that the pass through will be less than we think, and if so, that will matter for our policy.”

Don't miss what's next

Upgrade your Block Scholes account to unlock this article and other exclusive insights

Premium

$30/mo

Access previous and future reports, market insights & deep dives.

A selloff in chipmakers, a sixth consecutive night of US strikes on Iran, and two Fed speakers setting out a more hawkish view all weighed on risk: the S&P 500 closed down 0.51% and the Nasdaq-100 fell 1.62%, while the Philadelphia Semiconductor index plunged 4.29%, taking its one-month loss beyond 10%. BTC was last at $62.8K and ETH at $1.83K, with Brent near $85 and on track for a 12% weekly gain as shipping halted in the Strait of Hormuz. Ondo Finance and SBI Group partnered to bring tokenized Japanese equities onchain, T. Rowe Price launched the actively managed TKNZ spot crypto ETF, Citadel Securities invested $400M in Crypto.com at a $20B valuation, and Multicoin backed Hyperliquid-based Trasia Labs.