Thahbib Rahman

Research Analyst

In 2025, we predicted that stablecoin market, widely accepted as the first successful use case of real world asset (RWA) tokenisation, would grow significantly in both supply and volume. That prediction was due in part to their role in fulfilling a number of stated goals of the Trump 2.0 administration, as well as regulatory advancements in the US to establish guard rails for crypto assets and stablecoins (such as the GENIUS Act and CLARITY Act). As seen in Figure 1 below, growth in tokenised assets in crypto has begun to scale exponentially, particularly since 2024. That was driven by a combination of institutional and retail user interest.

In 2025, we predicted that stablecoin market, widely accepted as the first successful use case of real world asset (RWA) tokenisation, would grow significantly in both supply and volume. That prediction was due in part to their role in fulfilling a number of stated goals of the Trump 2.0 administration, as well as regulatory advancements in the US to establish guard rails for crypto assets and stablecoins (such as the GENIUS Act and CLARITY Act). As seen in Figure 1 below, growth in tokenised assets in crypto has begun to scale exponentially, particularly since 2024. That was driven by a combination of institutional and retail user interest.

A tokenised asset is essentially an on-chain representation of an off-chain asset, such as 1 USDT or USDC representing $1 off-chain. Stablecoins were the first layer of tokenisation, with the second layer being the tokenisation of further offchain, RWAs such as equities and commodities. In our view, the next phase of RWAs and a potential major trend of 2026 will be the development of perpetual futures contracts on those same RWAs (in equities, foreign exchange, commodities and more).

Perpetual contracts have long been the most popular derivatives instrument to trade in crypto by notional daily trade volumes, exceeding that of spot, futures and options markets.

Like perpetual swap contracts on crypto-currencies, equity perps are cash-settled derivatives contracts that give traders synthetic, linear, and leveraged exposure to a traditional, offchain index, equity price, or other real-world asset (RWA). Equity perpetual contracts maintain their peg to the value of the underlying asset’s spot price through the use of funding rates.

This distinguishes them from tokenised equities, which instead track the value of the underlying off-chain asset via the promise of minting and redeeming at the face value of the off-chain asset itself. From a legal standpoint, tokenised equities from popular issuers such as Ondo and xStocks, are a type of structured product. According to Ondo’s documentation, “An Ondo tokenized stock is a structured note” designed such that the “amount payable to the token (note) holder changes in value based upon the change in value of the corresponding underlying asset.” The tokens themselves are also “fully backed on a 1:1 basis (plus a buffer) by the corresponding underlying securities held via a regulated custodial broker-dealer (and cash in transit).”

Additionally, while the holder of a tokenised equity has the right to redeem their tokens for the then-market value of the underlying asset, Ondo says that “Like with brokerage accounts, you will not see your name on the share register for the underlying assets — they are held in the name of, or for the benefit of, the Issuer [Ondo]”. That also means tokenholders “do not have shareholder voting rights, shareholder information rights or other shareholder rights from the issuer of the underlying securities.” xStocks tokenised equities are treated similarly — “Token ownership does not grant any voting or shareholder rights in the underlying asset.” When it comes to dividends, Ondo ensures that “dividends are automatically invested back into the token” and “reflected in token pricing”, while xStocks states that “Any dividends are reinvested into the underlying collateral asset.” (Note – not all implementations of tokenised equities follow the same description as above).

Therefore, while both equity perps and tokenised equities are on-chain representations of some off-chain asset (and both do still give economic exposure to the underlying), they vary in how they maintain a peg to the value of the off-chain asset.

This important distinction means that the tokenized equity market is strictly bounded by the size of its respective underlying market — you cannot tokenise more NVIDIA shares than that which exist. Whereas with perp derivatives, the market can be multiples larger than the underlying (as are options on US equities).

Perpetual futures contracts allow traders to take leveraged long or short positions on the underlying index provided that they maintain sufficient margin. To ensure the price of a perp contract is anchored to the underlying index price, exchanges use funding rates — a periodic (usually every 8 hours) payment from longs to shorts (or shorts to longs) depending on the price of the perp relative to the oracle-fed spot price. Equity perps work the same way; however the difference is that the underlying that is tracked is the value of a real-world asset, rather than a crypto-currency.

During traditional market hours, an oracle feeds the real-time price data (collected from various sources such as NASDAQ, NYSE, CBOE) from the Trad-Fi market into the on-chain smart contract. Take the example of BitMEX (a centralized exchange that nonetheless highlights the implementation of both CEXs and DEXs): “During US trading hours, our index price for Equity Perps is dominated by the real-time TradFi prices”. After-hours, however, alternative reference feeds such as tokenised stocks, or equity futures markets are used — “However, outside of these hours (overnights, weekends, holidays), the index is maintained by referencing tokenised spot prices from other centralised exchanges.” Therefore, in this example the funding rate calculation partly relies on a tokenised equivalent of the underlying asset (particularly when the traditional market closes).

While perpetual futures are cash-settled and do not require traders to hold the underlying asset, we believe that equity perp markets are more likely to grow when market makers have access to a continuously traded, tokenised version of the underlying — enabling them to hedge risk more efficiently outside of traditional market hours and thus improving their ability to quote prices. However, not all implementations of equity perps do require a tokenized asset to provide an out-of-hours mark price. According to XYZ docs, a provider of equity perps on Hyperliquid, “During active sessions, the oracle consumes price data for the underlying asset from institutional liquidity providers”, however

More details on their methodology can be found here – in short, these equity perps do not require a tokenised equity of the underlying asset to exist.

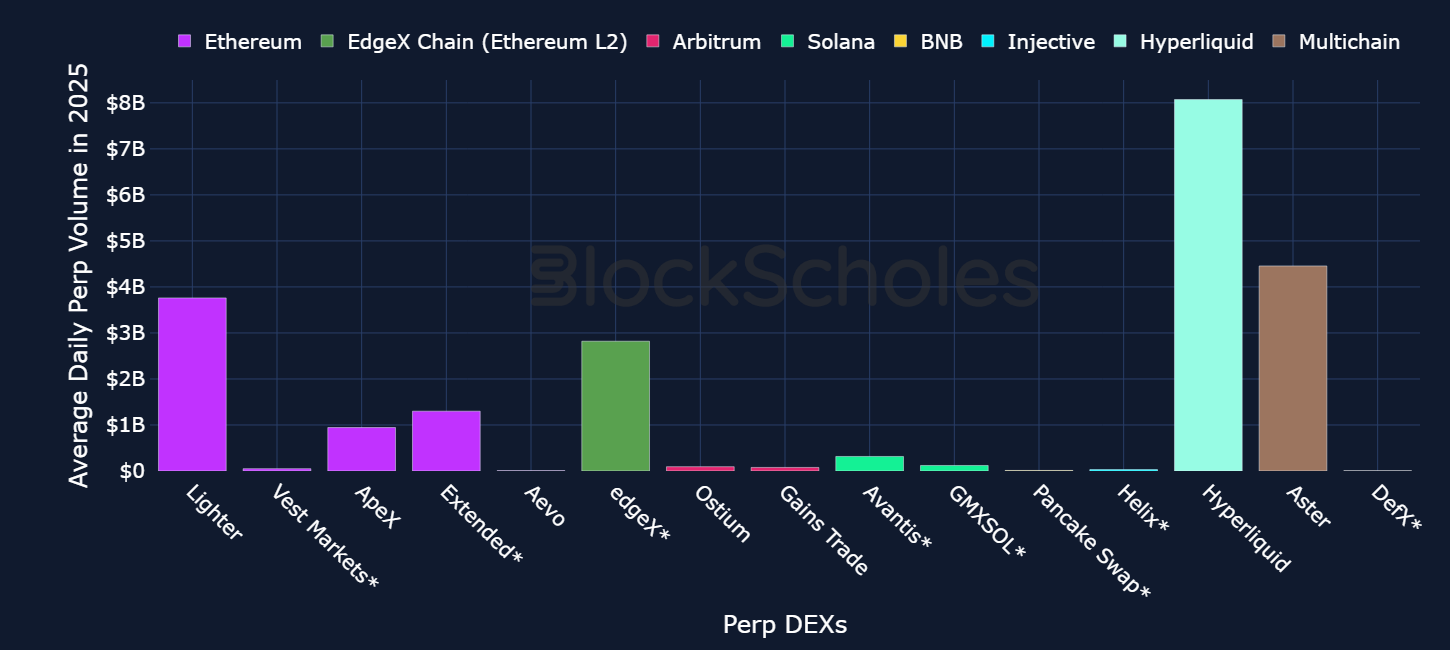

In order to size the RWA market, we summarised a list of decentralised exchanges that already offer equity perps, and recorded the average daily notional volume of all perps on those exchanges. Across the exchanges that already offer RWA perps, Hyperliquid, Aster and Lighter accounted for 70% of the total volumes (roughly $20B) across perpetuals on all underlyings offered by the DEXs in our list.

For these three exchanges, we then calculated the proportion of total perp volume that was in RWA-related perps (based on the past 24-hours volume of RWA-perps). On Hyperliquid for example, 13.8% of the total daily average perp volume came specifically from RWA perps. While RWA-activity was proportionally lower across Lighter and Aster, 5.03% of the total volume on the top three perp DEXs is already from RWA perps. Assuming that the proportion is representative of the full perp DEX market, this puts the RWA perp market at roughly $1B in daily volumes (as 5% of the $20B recorded across all underlyings on the selected DEXs).

At the start of 2025, perp volume on Hyperliquid was $2B. By the end of the year however, daily perp volume came in at $8B, marking a 4x increase in growth. In fact, over the year, Hyperliquid consistently recorded days where perp volumes exceeded $10B. As a conservative base case however, if we assume Hyperliquid (the leader of the space) sees the same 4x growth in daily perp volume as it did last year, in 2026 we could potentially see an average perp volume of $32B per day on the platform.

Extending that same growth rate to the other major perp DEXs (Hyperliquid, Aster and Lighter), which currently have around $20B of notional volume per day, we could see the perp market grow to an average of $80B per day and the RWA-specific segment of the perp market grow from $1B per day to $4B.

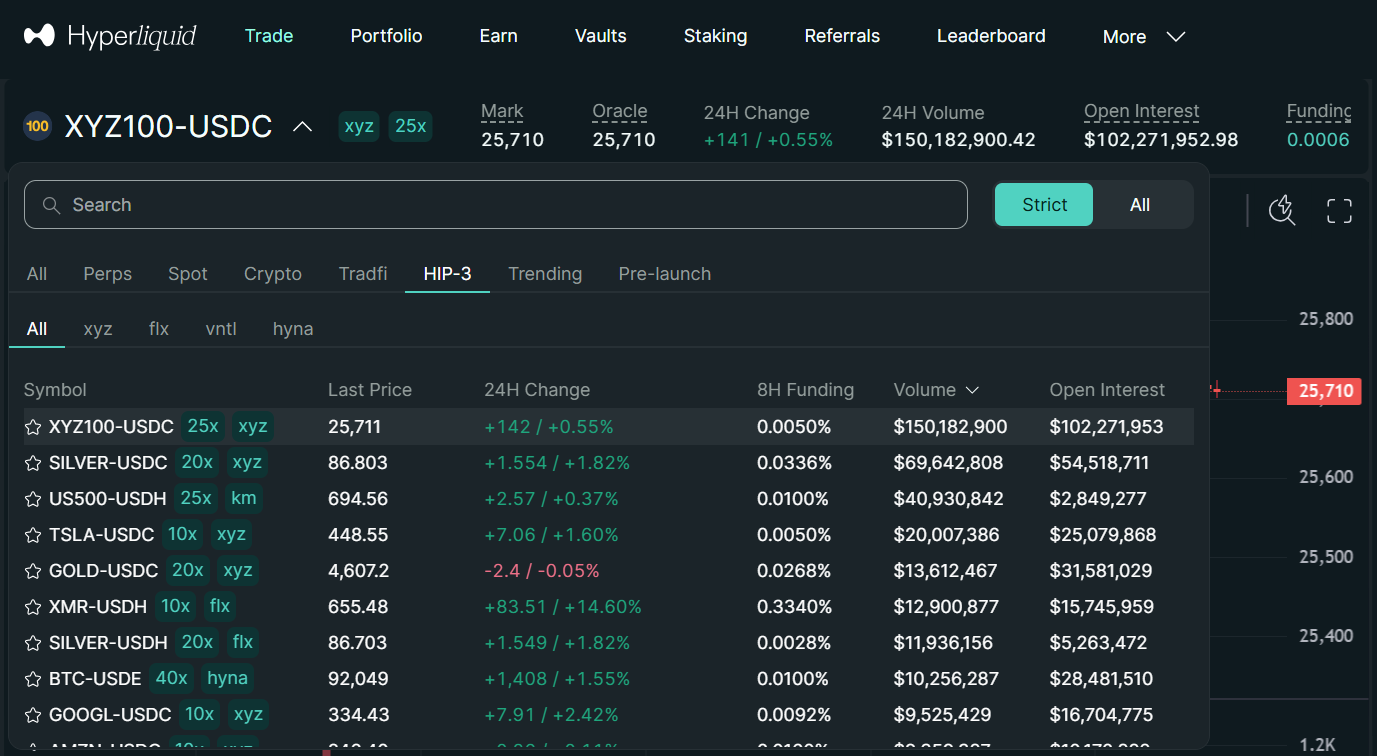

On October 13, 2025, Hyperliquid launched its HIP-3 network upgrade to mainnet. According to Hyperliquid docs, HIP-3 enables the Hyperliquid protocol to “support permissionless builder-deployed perps, a key milestone toward fully decentralizing the perp listing process”. That is, the HIP-3 upgrade allows for permissionless perpetual contract building, without the need for centralised approval.

In order to deploy a perpetual contract market, a developer needs to stake 500,000 HYPE tokens (equivalent to $11M at the time of writing), which acts as a security bond and safeguard against spam perp listings. Once deployed, builders must provide their own liquidity, oracles, and front-end interfaces, but are eligible to earn 50% of the trading fees from the markets they create.

In the Figure above, we showcase some of the perp contracts listed on Hyperliquid via HIP-3. So far, almost all of the perps are RWA-related, such as XYZ100, which “tracks the value of a modified capitalization-weighted index of 100 large non-financial companies listed on a U.S. exchange.”

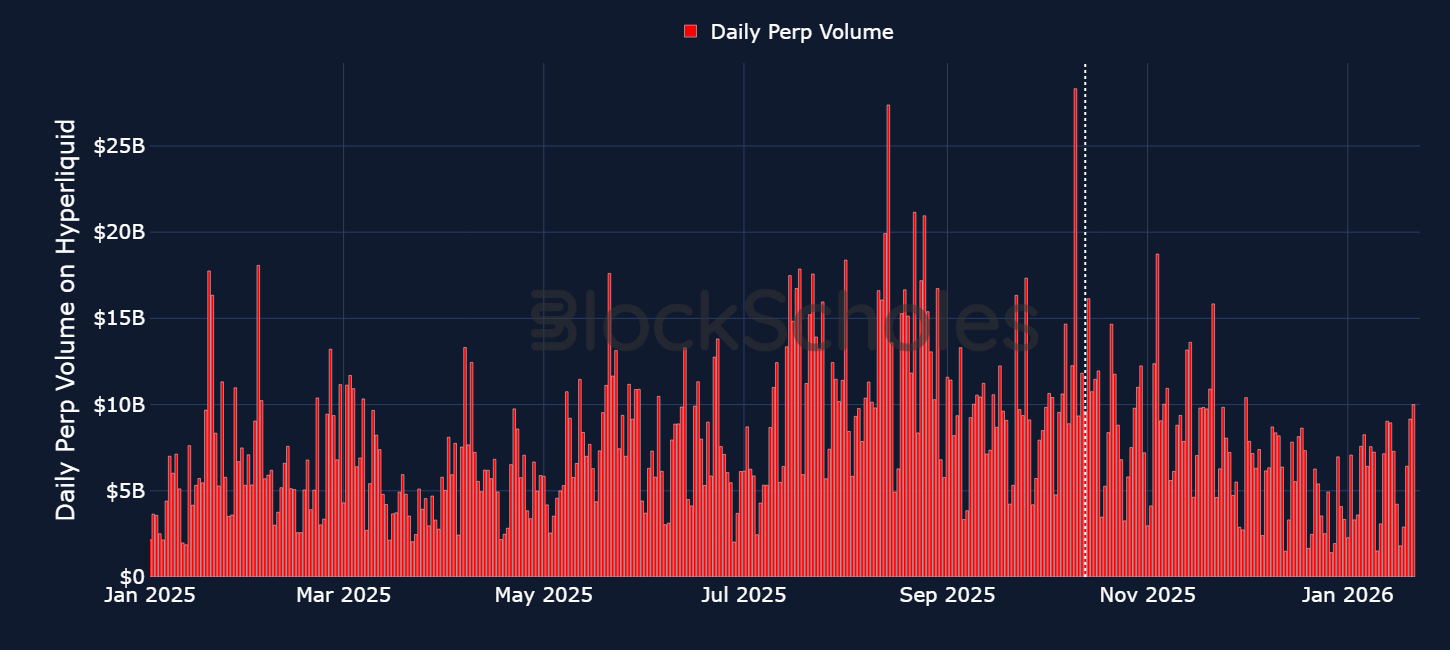

We are yet to see an obvious impact on total daily perpetual’s volume since the launch of these equity perps on Hyperliquid. In the chart below we plot total daily perp volume (which measures the volume of all perps on Hyperliquid, including equity perps), with the vertical dotted line marking the launch of HIP-3. The major spike up corresponds to the Oct 10, 2025 liquidation event. So far there isn’t an obvious upward trend to suggest total daily perp volumes have increased post HIP-3 — however firstly, we are still early. Many projects may currently be in the process of acquiring the relevant HYPE tokens needed to launch perps, as well as finalising other moving parts in the process, such as front-end interfaces, oracles and more; thus the impact of HIP-3 may show up in the upcoming months. Secondly, since the October 10 event, we have seen volumes across all markets, including perps having fallen.

Nonetheless, given that Hyperliquid has the ‘first mover advantage’ in the perp equity space, it is reasonable to assume that over time we may begin to see a notable increase in total perp volume stemming from equity perps.

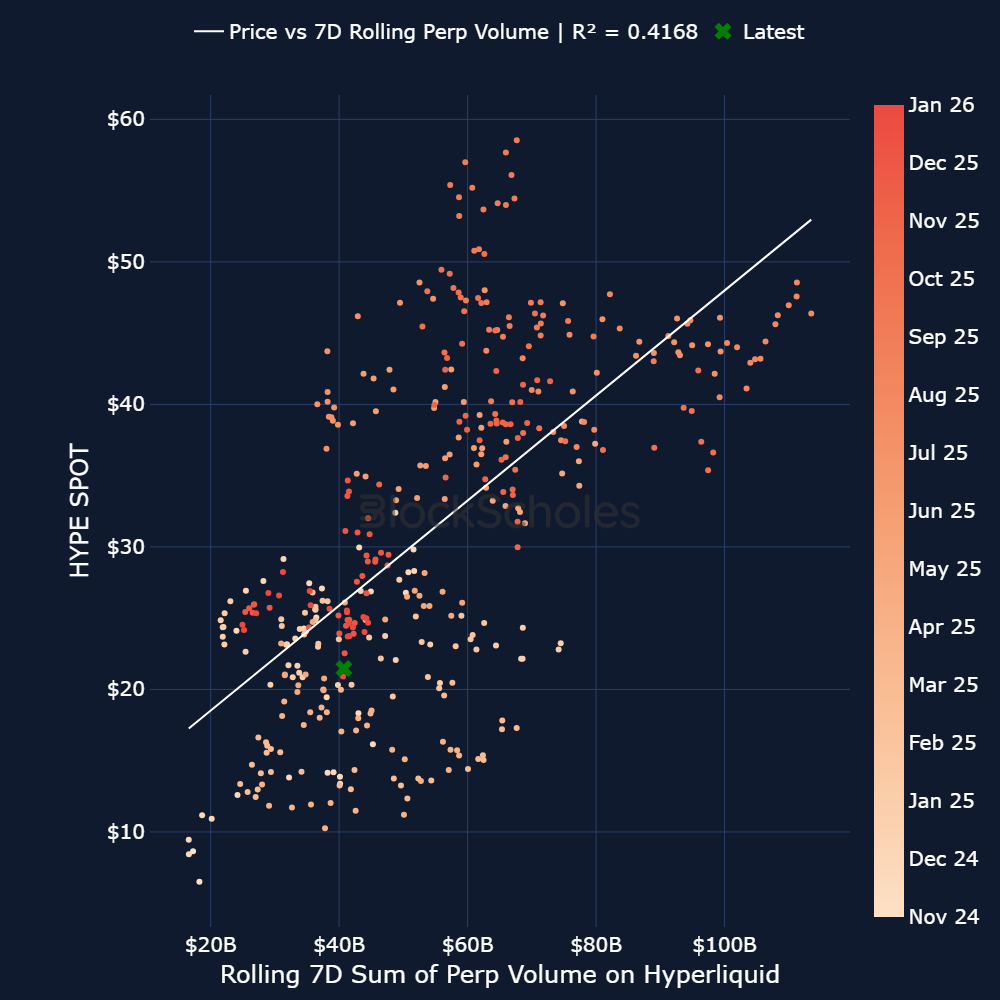

According to Artemis data, on average, 98% of total volumes on the Hyperliquid chain come from perp volumes alone. In the previous section we estimated that average daily perp volume on Hyperliquid could potentially grow from $8B to $32B.

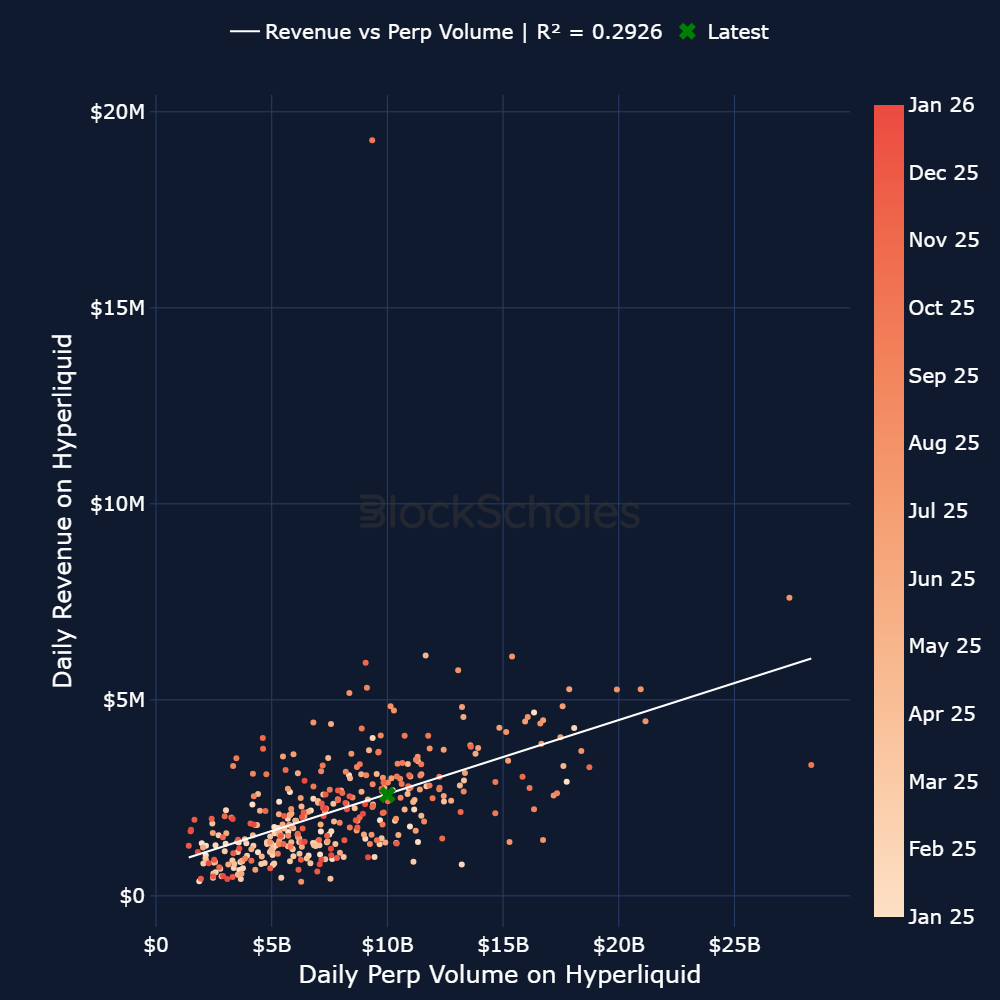

A linear relationship between the rolling 7-day sum of perp volumes on Hyperliquid and the HYPE tokens spot price suggests an increase in daily perp volumes to the size of our estimates could have a significant implication for HYPE’s spot price.

Another way to analyse this is through the lens of token buybacks. 97% of Hyperliquid’s revenues are allocated to an assistance fund that uses the funds to buy back HYPE tokens. For example, on Jan 13, 2026, when HYPE traded around $25, the total dollar value of HYPE buybacks was equal to $2,318,302. Assuming an average acquisition price of $25, that was equivalent to approximately 92,000 tokens bought from the buyback program (compared to the current daily token unlock of 217,155 HYPE tokens).

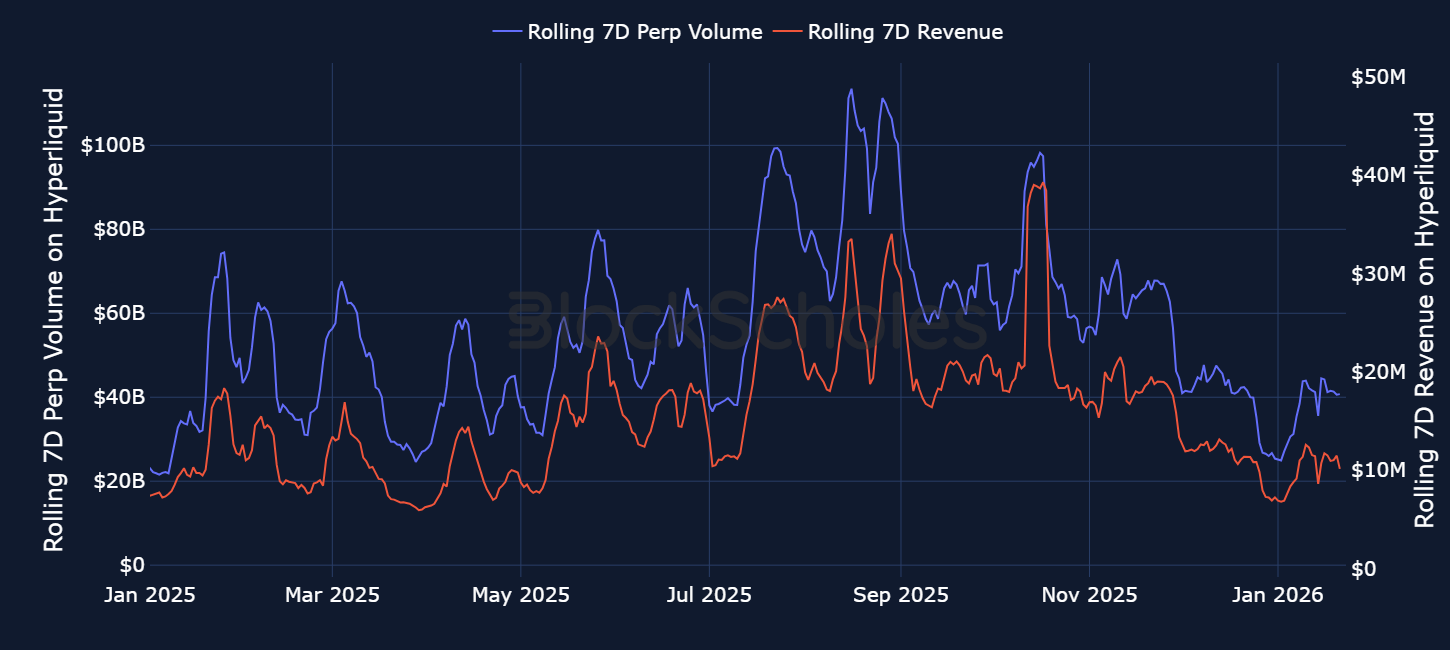

Below we plot the rolling 7-day perp volume alongside the 7-day rolling revenue of the Hyperliquid platform. The two clearly move in line with each other, with higher volumes on perps resulting in higher fees paid to the network and thus higher revenue for the protocol.

There is a linear relationship between daily perp volume and daily revenues on Hyperliquid. According to that relationship, volumes of $32B per day would be roughly equivalent to $6.76M of daily revenue. Given that 97% of revenues are used to buyback HYPE tokens, that would also result in roughly $6.76M worth of HYPE tokens being purchased daily. To put that into comparison, the daily dollar average purchase size of HYPE tokens in 2025 was $2.3M, implying nearly a 3x increase in daily token buyback stemming from the growth in equity perps. A consistent reduction in the supply of the token through buybacks of this size could then provide further support for the native HYPE token.

Stablecoins were the first real use case of real world asset tokenisation, proving compatibility with both the institutional and retail audience. This sets the scene for the tokenisation of further TradFi asset classes, such as equities and commodities. We believe the next phase of RWA tokenisation growth lies in perpetual futures contracts with assets from TradFi as the underlying. Perpetual futures on real world assets provide synthetic, linear, and most importantly, 24-7 exposure to assets from the traditional finance world; which, like stablecoins, opens them up to both retail and institutional interest. We have already seen early signs that the RWA perps are accounting for a larger percentage of the broader perpetual futures contract market and anticipate that growth will continue into 2026.

Hyperliquid’s HIP-3 protocol upgrade is at the centre of the development in the RWA perp space, allowing anyone to permissionlessly deploy perpetual markets and has positioned the protocol as the dominant market leader in the space. Increased overall perp volumes from equity perps are likely to translate into higher protocol fees and revenues, which have historically shown a meaningful relationship to the growth in the native HYPE token (in part due to a 97% of revenue buyback program).

In summary, our view is that in 2026 RWA perps could integrate themselves as one of the strongest use cases of real world asset tokenisation, as did stablecoins before them.